.svg)

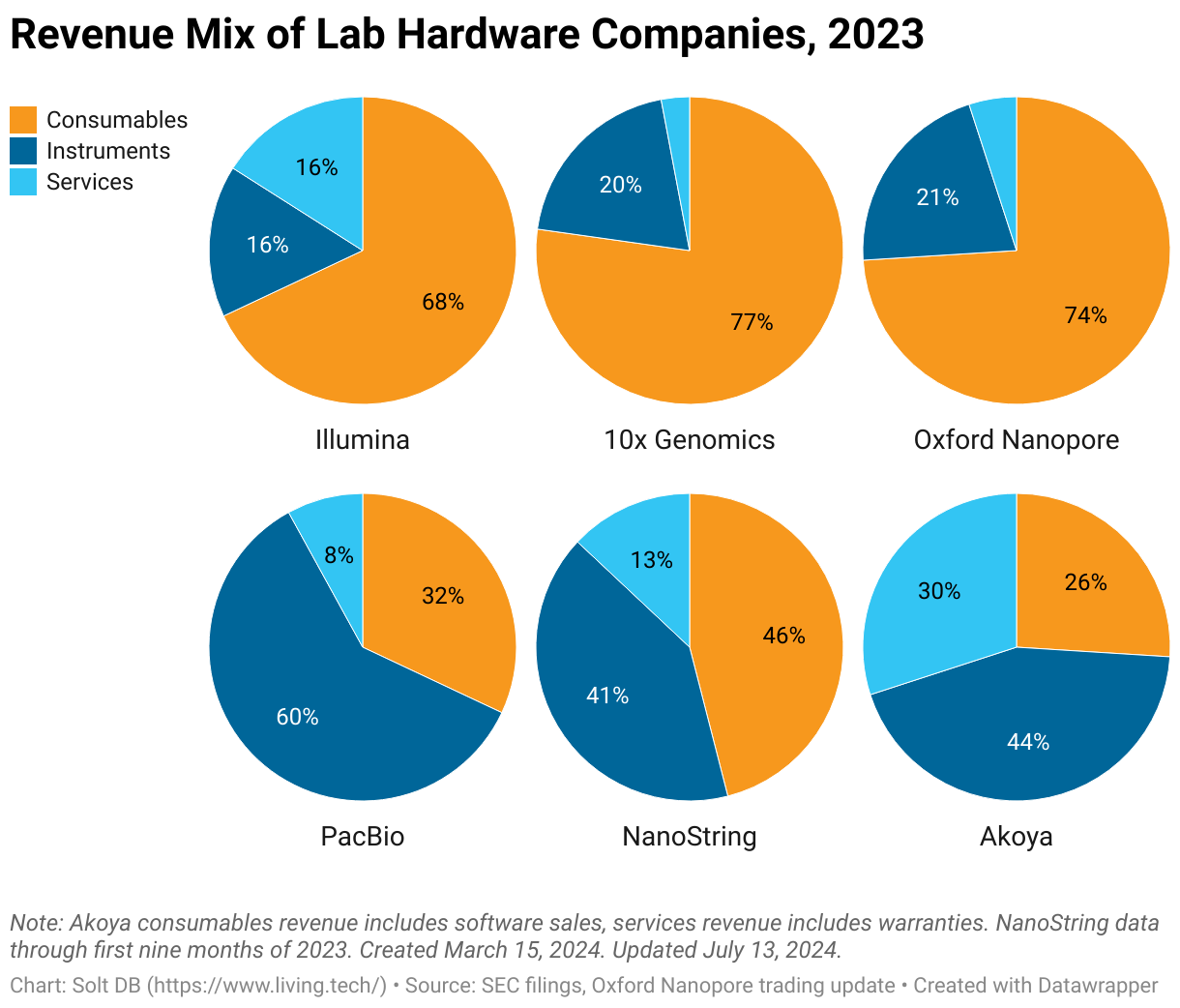

The business model for lab hardware companies is simple, but not easy. Success (and cash flow) is driven by optimizing the share of consumables revenue in the overall revenue mix.

In fact, there's even a quantifiable level investors can use to determine if a lab hardware business will be sustainable in the long run: 67%.

As in, businesses that generate less than two-thirds of total revenue from consumables often fail. This "rule" has held for the last two decades. All companies need to place enough instruments in the wild. Then, if utilized frequently enough, each instrument can generate steady consumables pullthrough over years -- and a stream of recurring, high-margin revenue.

Of course, data can only take you so far. There's always a healthy dose of context and nuance behind the numbers. A survey of the landscape in 2023 provides some great examples. Keep in mind that constrained lab budgets have significantly extended sales cycles for all companies, likely delaying growth for at least 2024.

- Illumina and 10x Genomics remain the leaders in their respective fields. Both expect to generate operating cash flow in 2024, which would be the 19th consecutive year for Illumina and first for 10x Genomics.

- Oxford Nanopore is using cheat codes for its business model. By keeping hardware costs to a minimum, its revenue mix has always been biased toward high-margin consumables. That's allowed it to grow total revenue much more quickly than much older peers. It now generates more annual revenue than PacBio.

- PacBio was transitioning from the Sequell II / IIe platform to Revio last year (Onso doesn't appear to be a big driver). That scrambled its revenue mix, which was historically near only 40% consumables. However, early signs are promising for Revio, which could help the business approach the coveted 67% level.

- NanoString has long struggled to reach escape velocity with its revenue mix, which has historically hit a ceiling near 50%. That, coupled with a higher share of maintenance (services revenue), played a role in the company's bankruptcy. And, you know, lawyers from 10x Genomics.

- Akoya Biosciences is an emerging business, which is reflected in its revenue mix. The spatial biology company is still in the "placing instruments" phase of its growth trajectory. Consumables revenue will increase over time. In fact, the business plans to achieve cash flow breakeven by 2025 -- a refreshing focus on operating efficiency.

.svg)

.svg)

.svg)