A Bloated Share Structure Hurts Investors

Whereas venture-backed startups need to manage their cap table, publicly-traded companies need to manage the number of shares outstanding. It has important ramifications for remaining in compliance with major stock exchanges, the liquidity of the stock (how easily it can be traded), and the ability to raise capital in the future.

A company's valuation is determined by multiplying the number of shares outstanding by the price per share. A company with 50 million shares outstanding and a share price of $20 per share has a valuation of $1 billion (50 million shares x $20 per share = $1 billion total).

One of the important differences between an IPO and a SPAC is that the latter fixes the share price at $10 per share. This removes the ability of a company to control the number of shares outstanding, which can be problematic when management is attempting to maximize the overall valuation, as Ginkgo Bioworks did.

- A company preparing for an IPO will determine a valuation investors are willing to accept and set a share price range for the initial sale of securities. For example, if a business debuts at a valuation of $1 billion and wants to set a share price range near $20 per share, then it will have roughly 50 million shares outstanding. This allows a company more control over the number of shares outstanding and the debut share price.

- A company preparing for a SPAC is forced to debut at $10 per share. That's true whether a business sports a $100 million or $10 billion valuation. For example, if a business debuts at a valuation of $1 billion and wants to utilize a SPAC (fixed at $10 per share), then it will need to have 100 million shares outstanding.

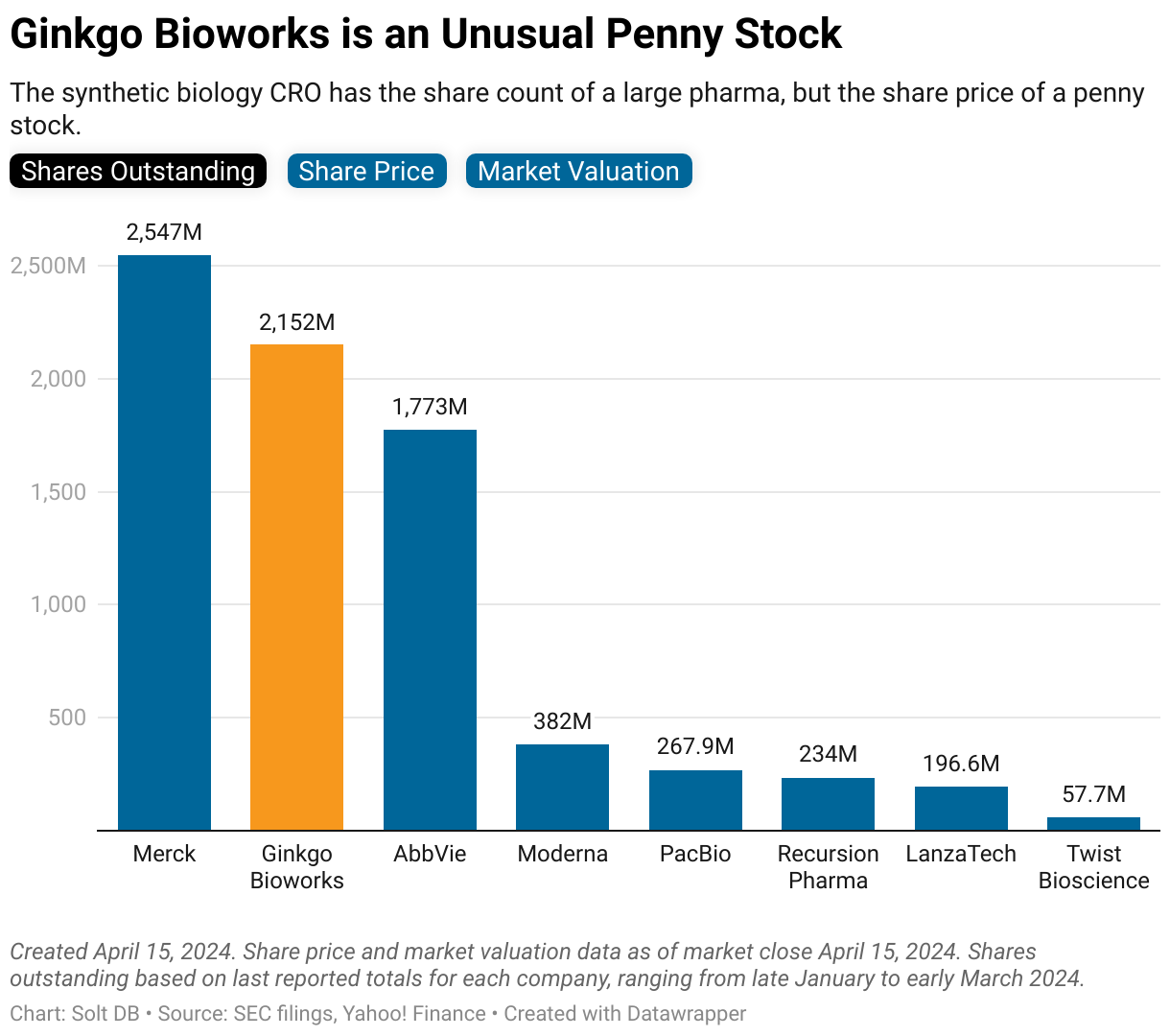

This was one of the largest tradeoffs made by the founders of Ginkgo Bioworks. To raise $1.51 billion in cash from the public debut, the business needed a valuation of $14.9 billion. To boast a valuation of $14.9 billion and utilize a SPAC, the business needed to have 1.49 billion shares outstanding. Not many companies ever reach that bloated level.

Consider how the number of shares outstanding for Ginkgo Bioworks compares to other popular biotech stocks and the world's largest drug developers. The business last reported 2.15 billion shares outstanding, which represents an increase of 45% since the public debut in 2021.

The problem facing Ginkgo Bioworks is now two-fold. It debuted at an unsustainable valuation – nearly 3x its last private valuation, all during a period of abnormally low interest rates – with an unsustainable number of shares outstanding.

Management can "fix" the share price by reducing the number of shares outstanding through a reverse stock split, but it won't be painless.

A Reverse Stock Split Solves 1 Problem, Creates Others

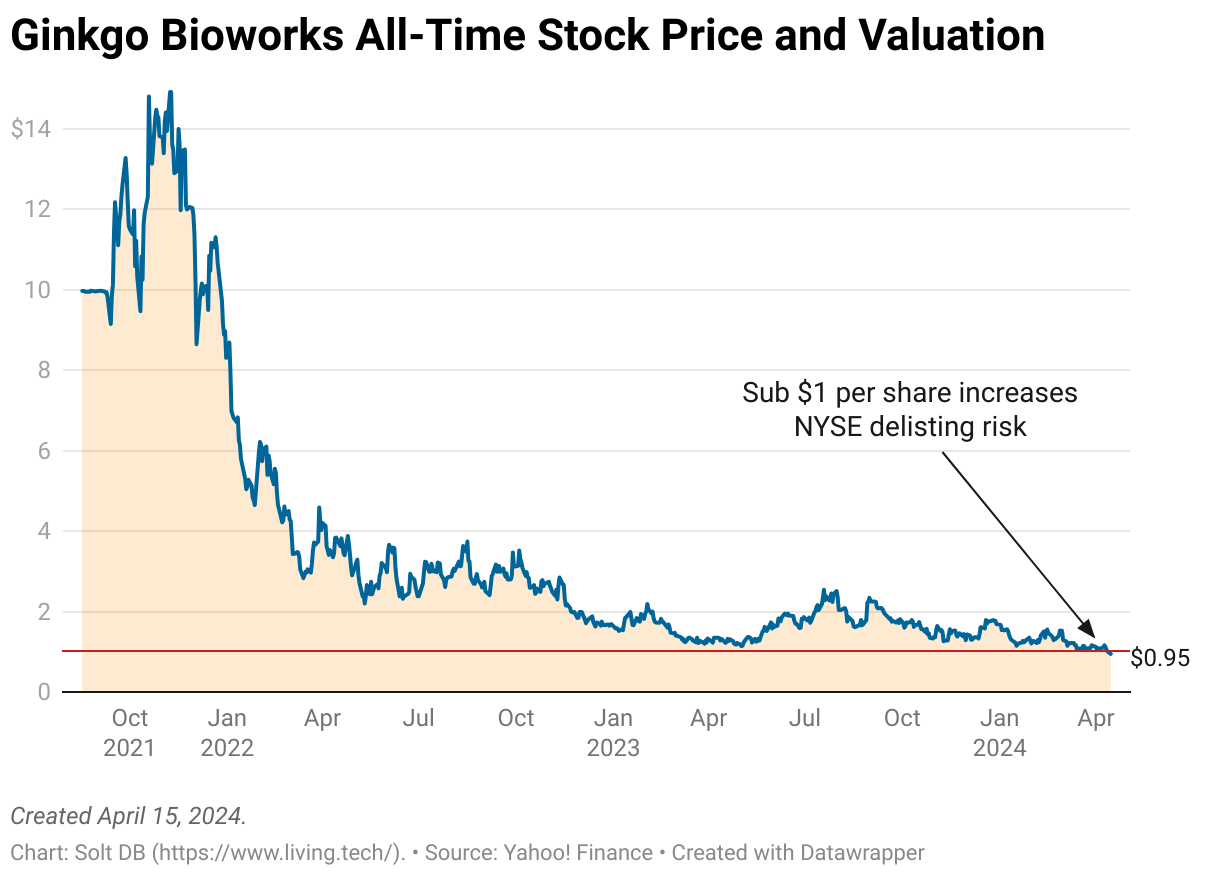

A stock price below $1.00 per share isn't just embarrassing. There are real-world consequences.

Ginkgo Bioworks listed on the NYSE so it could use the stock symbol "DNA." The exchange allows a stock to trade below $1 per share for 30 consecutive days before it warns the company about a possible delisting. The business then has a grace period to regain compliance or risk getting booted off the exchange.

What's the big deal? Well, many funds are barred from owning stocks that aren't listed on major exchanges, such as the NYSE or Nasdaq. If Ginkgo Bioworks got booted off the NYSE, then many institutional investors would need to sell their shares, creating a downward spiral in the stock price. The stock could get booted from major biotech ETFs, too.

Luckily, that won't happen. Ginkgo Bioworks is likely to conduct a reverse stock split in 2024. The transaction will intentionally reduce the number of shares outstanding to boost the stock price and remain in the good graces of the NYSE. Remember, a company's valuation is determined by multiplying the share price by the number of shares outstanding, so the valuation remains the same after a stock split.

- For example, a 1-for-10 stock split would reduce the number of shares outstanding from 2.15 billion to 215 million shares. As a result, the share price would increase by 10x, although the company's valuation would remain the same.

- A 1-for-20 stock split would reduce the number of shares outstanding from 2.15 billion to 107 million shares. As a result, the share price would increase by 20x, although the company's valuation would remain the same.

- If you're an existing shareholder, then you won't suddenly become richer. The number of shares you own will be reduced and each will be worth more, but the total amount of capital you have invested won't change.

Arithmetically, a stock split or reverse stock split doesn't have any impact on the company's valuation. The math always cancels out.

But the real world is powered by a different calculus.

Companies that issue stock splits (intentionally increasing the number of shares outstanding) typically see a bump in stock price, which analysts argue is because the stock price is more affordable to investors. Chipotle recently agreed to its first-ever stock split, which will drop the stock price from nearly $3,000 per share to just $60 per share. The business gained $4 billion (5%) in value on the news.

Companies that issue reverse stock splits (intentionally decreasing the number of shares outstanding) typically see a continuing decline in stock price. That's likely because companies issue reverse stock splits when things aren't going so well.

A Difficult Road Ahead

Ginkgo Bioworks doesn't harbor all the characteristics of a typical company forced to conduct a reverse stock split. It has meaningful traction for its services, a multi-year cash runway, and can likely raise money more easily than others. But even at its lowly stock price the business remains richly valued at a $2.17 billion market cap.

One thing investors misunderstand about the CRO business model of Ginkgo Bioworks is the time frame for delivering results. For example, in 2023 the company announced a drug discovery contract with Pfizer worth up to $331 million. The headline figure is great, but at least half of the deal value is based on reaching sales milestones.

Considering Ginkgo Bioworks operates primarily as a discovery-stage CRO partner, before preclinical and clinical and commercial efforts, sales-based milestones are roughly 10 years away for most programs – if they're realized at all.

That's a problem for the stock. Doubly so given its current premium valuation.

Less than 8% of drug discovery programs go on to earn U.S. Food and Drug Administration (FDA) approval, according to historical industry metrics. In other words, Ginkgo Bioworks needs 128 cumulative drug development programs to realize just 10 royalty-yielding products in the early 2030s. It had 41 active pharma programs at the end of last year.

The outlook outside of drug development isn't much better. As previously reported, Solt DB made a Freedom of Information Act (FOIA) request with the U.S. Securities and Exchange Commission (SEC) for the unredacted partnership agreement between Ginkgo Bioworks and Amyris. The document revealed Ginkgo Bioworks had a probability of success of less than 14% across food, flavor, and fragrance programs as of late 2022, nearly six years after forming the partnership.

The company's cash will run out well before meaningful downstream value – via milestones, royalties, and equity interests – is realized. Skepticism about the business model will put downward pressure on the valuation, which will further depress the stock price. That's an unfavorable environment in which to raise capital.

Wall Street will place a penalty on the company's valuation ahead of the next capital raise, while institutional investors (and/or a large pharma company) that participate in the next funding round will have more bargaining power. None of that will be favorable for the little guy who owns shares.

.svg)

.png)

.svg)

%20(squoosh).jpg)

.jpg)

%20(squoosh).jpg)

%20(squoosh%20cropped)%20(resized).jpg)

%20(squoosh).jpg)

-cropped.svg)