The darling of synthetic biology has sworn off manufacturing and scale-up assets, opting to build a horizontal technology platform serving all biotech sectors. The lack of vertical integration could hurt the business in the long run.

By

Maxx Chatsko

Updated

April 19, 2024

Published

November 30, 2022

Solt_DB

The ceiling of the Sistine Chapel depicts nine scenes from the Book of Genesis in the Old Testament, including the Creation of Adam. These figures are among the most important in Judaism and Christianity, although the legends, stories, and myths they represent are heavily borrowed from older cultures in Mesopotamia. They're not original, but that detail is overshadowed by a simple cultural truth: winners get to write history.

Stories and myths also play an important role in the world of startups and the urban hubs that nurture them. Here, too, the winners get to write history. But there's uncertainty in the moment. You're never quite sure which way the arc of history will bend when you're living on its edge. What seems inevitable or indisputable often becomes relegated to a footnote, or worse, cast into the dustbin.

In mythology and startups, the most important lessons are embedded in mistakes and failures, from eating forbidden fruit to making the wrong technical bets. The dynamism of the moment can lead to the wrong lessons being learned, which compounds mistakes until entrepreneurs and investors collectively arrive at the truth (or get closer to it). Adopting a pragmatic and ruthlessly objective interpretation of events can increase your accuracy as they unfold.

What many observers miss about Ginkgo Bioworks is that the horizontal technology platform for engineering cells as a service was built in part by learning some of the wrong lessons from earlier failures in synthetic biology. Industrial biotech companies haven't failed because they vertically integrated. They often failed due to poor process economics. After all, you can't make money from a product if you can't physically make the product.

By shunning products (and therefore the most reliable recurring revenue streams), the business will subject Wall Street to frustratingly choppy revenue for the foreseeable future. That could be navigated by royalty streams and milestone payments. By shunning downstream process optimization, the business leaves the most significant bottleneck in industrial biotech at the feet of its customers. That reduces the likelihood of earning royalty streams and milestone payments.

The avoidance of commercialization process scale-up and know-how remains the company's original sin – and one that hampers the business more than is publicly acknowledged.

Need more finch? Here's our newsletter.

Welcome to The Voyage!

Oops! Something went wrong while submitting the form.

The "Other" Translational Gap

Image Soruce: National Cancer Institute on Unsplash.

As previously reported, Solt DB made a Freedom of Information Act (FOIA) request with the U.S. Securities and Exchange Commission (SEC) for the 2016 partnership agreement between Ginkgo Bioworks and Amyris. The document reveals Ginkgo Bioworks has commercialized only three of more than 21 specialty chemicals contributed to the partnership. Amyris has only commercialized five of more than 19 specialty chemicals contributed to the partnership. The success rate of the combined portfolio is less than 11% -- no better than drug development.

Why is the commercial success rate so low over six years later? Technical advances have been made in the field broadly and for the technology platform specifically. Why haven't more products been commercialized for customers in recent years?

The difficulty of downstream processing plays a significant role in the commercialization success and stumbles of both Amyris and Ginkgo Bioworks. That is, what happens when a fermentation run is complete? How do you purify and separate the product from the fermentation broth? What recovery loss will you have to live with – and how much will it cost?

Downstream processing is not as sexy as cell engineering. It doesn't receive nearly as much attention or investment, but it's quietly the key to enabling the bioeconomy. It's sitting in plain sight.

Amyris has commercialized a number of unique fermentation processes, but has mostly had success with alcohols. Commercialized ingredients include sclareol (an amber fragrance), santalol (a sandalwood-like fragrance), manool (an amber fragrance), bisabolol (a chamomile ingredient for cosmetics), and patchoulol ("patchouli"). The suffix "-ol" signifies an alcohol, which means there are relatively tried-and-true downstream processing approaches such as distillation. The company has struggled with most other ingredients that aren't alcohols or derived from farnesene.

Ginkgo Bioworks has optimized three strains for customers in flavors and fragrances (F&F) that made it to commercial production. The two known commercialized ingredients are gamma-decalactone and massoia lactone. Many of the most advanced programs in the partnership document are alcohols or lactones (hinting at the third commercialized ingredient). Lactones can be purified using liquid-liquid extraction and/or chromatography.

These are the boring chemical engineering details. No one becomes a PhD in molecular biology or joins a synthetic biology lab to learn about downstream processing steps – and that's a major problem facing the field heading into 2023.

Success in developing commercial downstream processing steps for one chemical class doesn't automatically translate into cell programs for another. Downstream processing for industrial biotech cannot be reliably scaled up from benchtop to commercial scale in the same way ambr250 systems allow for bioprocesses. It's not impossible, but few are focused on it right now. It makes sense.

Downstream process development requires intricate knowledge of each process, which can only be gathered by having scaled a product. What is the chemical composition of the fermentation broth? What chemical class is being worked with? How efficient is your centrifugation or other mechanical system? Worse yet, you only get so many cracks at the commercial side of things. It's tough to scale down when minimum volumes are measured in tens of thousands of liters. In other words, these questions cannot always be answered at lab or pilot scale.

Ginkgo Bioworks doesn't bother with downstream processing steps, which significantly hampers the success rate of customers. The business can generate revenue from cell engineering as a service, but that won't fund the operating expenses of the foundry unless customers commercialize products to generate meaningful milestones and royalty revenue.

The Foundry delivered revenue of $90 million and an operating loss of $188 million in the first nine months of 2022. The operating loss would've been worse if share-based compensation wasn't excluded.

The liability imposed by the blind spot of downstream processing will directly impact the valuation multiples applied to a contract research organization (CRO) for synthetic biology.

The Right Bet at the Wrong Time

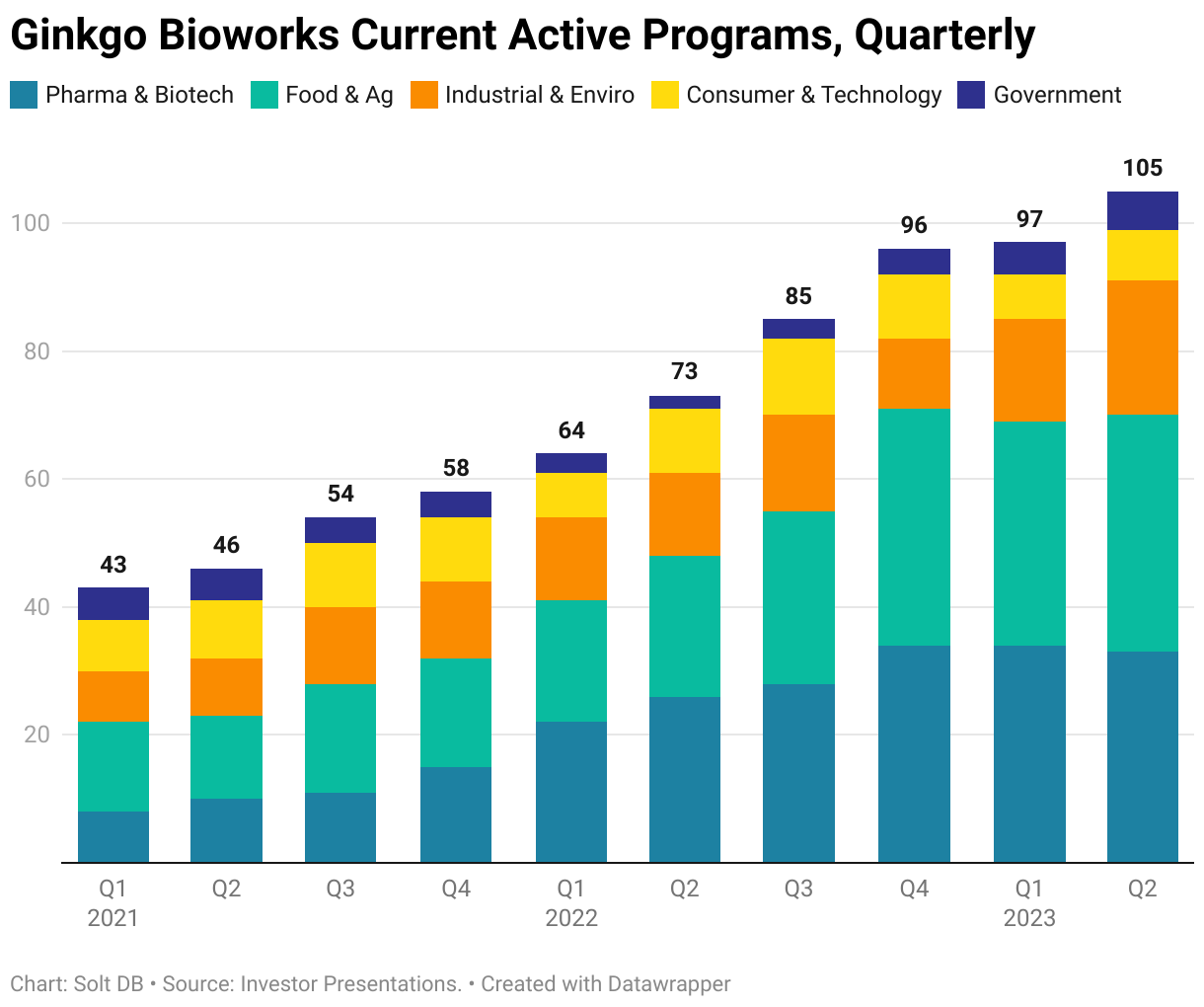

A horizontal cell engineering platform isn't necessarily a bad idea, but it may be too early in 2022. High-throughput experiment platforms such as foundries and cloud labs currently have a blind spot to downstream processes. This is evident in Ginkgo Bioworks' recent focus in pharma & biopharma and food & nutrition verticals, which comprised two thirds of current active programs at the end of the third quarter of 2022.

Cell programs with large drug developers are partially de-risked due to the experience and know-how in downstream processing. Mammalian cell culture isn't without headaches, but downstream purification and filtration steps are pretty well figured out thanks to Repligen. Similarly, agricultural biologicals involve "simply" growing soil bacteria to sufficient concentrations for pellet production – there's no downstream processing of metabolites.

And although there are fewer examples, the ability to attract scale-down programs from already-scaled industrial biotechs such as Genomatica and Bolt Threads provides a reliable path to generating cash flows from these individual programs in the form of milestones or royalties.

It's smart for Ginkgo Bioworks to focus bandwidth and foundry capacity on these customers. They're the most likely to enjoy commercial success. This was one of the driving factors behind the company's decision to bring Joyn Bio in house, although a lack of execution within the original Bayer agreement, dwindling deferred revenue amounts for the foundry, and falling behind competitors also played a role.

However, delivering a 100% success rate within these programs wouldn't drive the business to all-time highs.

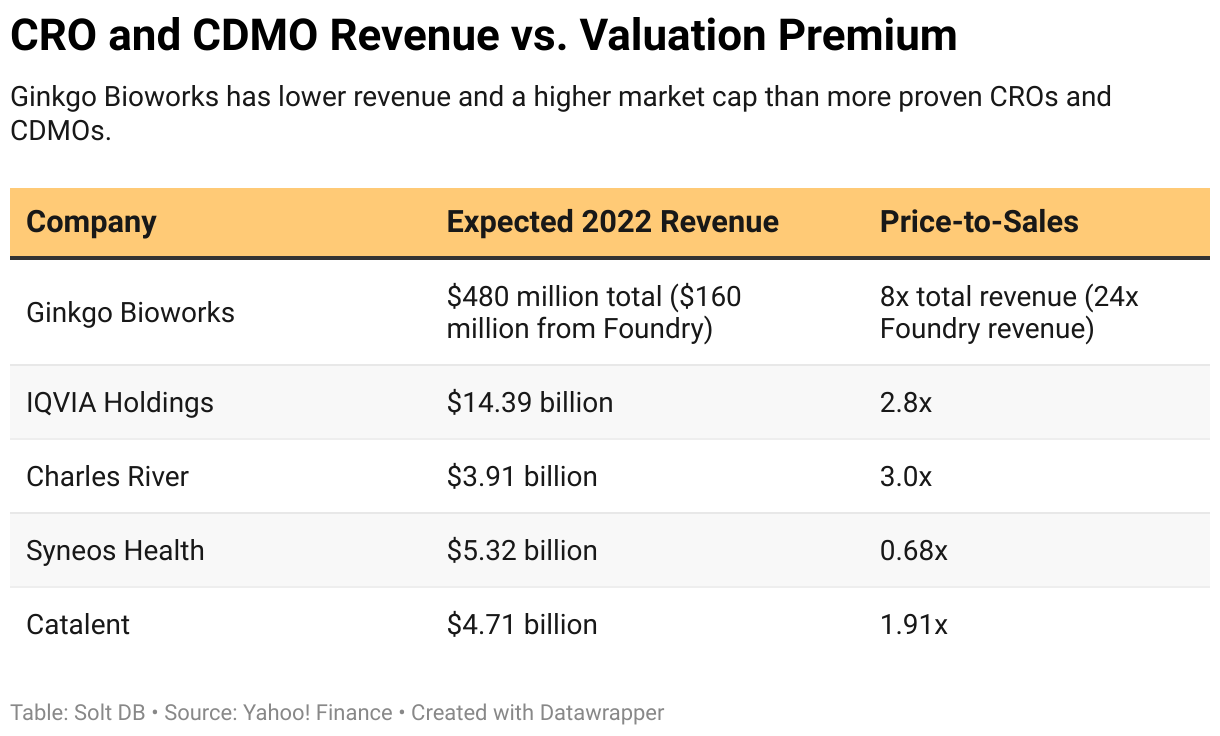

Consider the annual revenue and current valuation multiple of several leading CROs and contract development and manufacturing organizations (CDMOs).

Ginkgo Bioworks may not reclaim all-time highs until it reaches nearly $6 billion in annual revenue, or a 1,150% increase from 2022 levels.

For Ginkgo Bioworks, the decision to focus on horizontal cell engineering and forgo investments in downstream process engineering has hindered its ability to deliver within cell programs. The organism might be the product and Wall Street might pencil in future royalty revenue streams, but customers cannot sell products if they cannot make products.

One common criticism among current customers is that Ginkgo Bioworks charges too much for what is delivered. This could create a headwind for revenue growth even with growth in cell program count, especially with the emergence of cloud labs such as Emerald Cloud Lab that don't take any equity or royalties in customers.

Among prospective customers, the foundry's reluctance to take risks within certain verticals has been an annoyance. This is true even within well-funded verticals or related parties, such as personal care and cosmetics.

Ginkgo Bioworks' reliance on related parties is worth watching. CEO Jason Kelly modeled this aspect of the business on Intrexon, which was investigated by the SEC and eventually left the public markets due to fraud. For disclosure, I received a cease-and-desist letter from Intrexon for reporting on its "financial shenanigans" – since those asshole lawyers hated that phrase.

Ginkgo Bioworks generated 35% of Foundry revenue from related parties in the first nine months of 2022. That's equivalent to Intrexon's reliance on related parties, but there are more layers of separation between the company and related parties compared to Intrexon. Therefore, this does not appear to be as troubling, but should still be watched by investors. For example, Joyn Bio was absorbed once the deferred revenue total dwindled to be insignificant for Ginkgo Bioworks. If absorption or dissolution of other related parties occurs for similar reasons, then that would be a significant red flag.

Jason rarely accepts my Steelers vs. Patriots bets (that's worked out for me in recent years…), but he's eager to prove many people wrong about the business model for Ginkgo Bioworks. He can still be right. Unlike Amyris, the company has a well-rounded team of very competent executives.

Ginkgo Bioworks might shun downstream processing steps for customers, but the ability to focus on microbial fermentation of pharmaceutical ingredients could provide an opening. For example, if the foundries deliver on microbial fermentation of specific active pharmaceutical ingredients or shift antibody production from mammalian to microbial culture, then those customers would need to develop downstream processes. That knowledge could potentially be leveraged for industrial biotech customers that are currently struggling to utilize the platform from end to end. Of course, the significant economic differences between drug products and industrial biotech products would need to be considered.

Codebase is potentially valuable, but mostly over hyped and easily replicated. The increasing accessibility of whole genome sequencing tools and miniaturization and parallelization tools reduce the value of the foundries in this regard.

The near-term viability of the business might be determined by Biosecurity revenue. The business segment could generate meaningful revenue if governments buy in to the promise and necessity of biosurveillance tools, but austerity policies and conservative government control of finances could hinder progress. Nonetheless, if Ginkgo Bioworks can string together $500 million to $1 billion in recurring revenue from global biosecurity contracts within the next three to five years, then the company's valuation could be justified.

It's also worth acknowledging the company is swimming against powerful currents. Biology wants to be distributed and as close to free as possible. Centralized experiment platforms such as the foundries of Ginkgo Bioworks will always need to adapt to that reality. Perhaps the business adjusts and becomes more nimble over time, but the investor journey wouldn't be painless.

Ginkgo Bioworks can succeed with its current CRO business model, especially in ingredient categories that require minimal downstream processing (such as agricultural biologicals) and with established customers (such as large biopharma). But the technology platform cannot reach its full potential until the field at large develops more experience and know-how in commercial process development. That might not happen until 2030 at the earliest.

(free stuff and recent articles below)

Is that biotech stock a buy?

Solt DB is a public benefit company exploring the business of biotech. Subscriptions to investment research fund our work and keep us fiercely independent. For $25 per month or $225 per year, we help you identify attractive prices for the top biotech stocks in real time.

Jump into the database. The Solt DB Biotech Company Database is tracking every biotech company on the planet, past and present, to develop greater insights into the bioeconomy. It's free and open.

.svg)

.jpg)

.svg)

%20(thumbnail)%20(squoosh).jpg)

%20(squoosh).jpg)

.jpg)

%20(squoosh).jpg)

%20(squoosh%20cropped)%20(resized).jpg)

-cropped.svg)