.svg)

Relay Therapeutics originally designed the ReFocus study to enable speedy approval of its lead drug candidate in a rare type of bile duct cancer. After establishing a foothold, the company planned to follow with approvals in other tumors harboring similar genetic alterations.

A confluence of factors has changed that strategy.

New data from non-liver cohorts demonstrated promising activity for RLY-4008 (lirafugratinib) in FGFR2-altered cancers. When coupled with an unforgiving environment for cash-hungry businesses and changes in how drug approvals are treated under the Inflation Reduction Act (IRA), Relay Therapeutics has opted to pursue approval for all tumor types at once.

The new strategy will delay approval from the original timeline, but help to extend the cash runway by 12 months into the second half of 2026. It also positions RLY-4008 for a significantly larger opportunity in FGFR2-altered cancers.

The ReFocus Study, Explained

The ReFocus study is a phase 1/2 clinical trial evaluating RLY-4008 in cancers with an FGFR2 alteration. Patients are being separated into seven unique cohorts so doctors can evaluate the drug candidate based on various criteria.

Patients are primarily grouped by where their tumor originated.

- Patients with a rare bile duct cancer called cholangiocarcinoma (CCA), or sometimes referred to as intrahepatic cholangiocarcinoma (ICC) when it impacts the liver, were evaluated in four cohorts.

- Patients with any other type of tumor were evaluated separately from CCA in three cohorts.

After being separated by the location of their primary tumor, patients are further grouped by two other criteria.

- Patients in the CCA cohorts are also grouped by treatment history. Some have previously received another FGFR inhibitor or other types of treatment such as chemotherapy. Others haven't received prior treatment at all.

- Patients in the other solid tumor cohorts are also grouped by their specific type of FGFR2 alteration, which can be a fusion, amplification, or mutation. A small group of CCA patients are also grouped by alteration type, although most have FGFR2 fusions.

In April 2023, Relay Therapeutics reported preliminary data from the CCA cohort evaluating patients with FGFR2 fusions who hadn't received an FGFR inhibitor before. RLY-4008 achieved a preliminary objective response rate (ORR) of 82% (14/17) in this population. An objective response is a partial response or better, generally defined as tumor shrinkage of at least 30% from the time treatment started. All individuals experienced tumor shrinkage at the data cutoff. By comparison, the best performing FGFR inhibitor on the market achieved an ORR of 42% in this patient population.

Relay Therapeutics enrolled the 100th patient in this cohort in September 2023, which means it's fully enrolled. Although the original plan was for this to be the pivotal cohort, meaning it would be sufficient in the eyes of the U.S. Food and Drug Administration (FDA) to make an approval decision, the company will now wait to generate data from non-CCA tumors before submitting a regulatory application.

Drug candidates being developed for FGFR2-altered cancers generally begin with CCA because it's the best-defined patient population, but it's also one of the smallest. Of an estimated 13,000 new cases of FGFR2-fusion cancers in the United States each year, an estimated 1,000 are CCA.

Unfortunately, FGFR inhibitors developed to date have struggled to prove effective in non-CCA tumors. The FDA hasn't approved a treatment for FGFR2-altered cancers outside of CCA and urothelial cancer.

This is what makes the October 2023 data readout from ReFocus, and the broader opportunity in FGFR2-altered cancers, so important.

The Tumor-Agnostic Data, Explained

Relay Therapeutics reported preliminary data for RLY-4008 across all three tumor-agnostic cohorts. These patients were grouped by the type of FGFR2 alteration. Across all cohorts:

- Patients with efficacy outcomes were heavily pretreated, with 81% (68/84) having received at least two previous lines of treatment. No patients were previously treated with an FGFR inhibitor, but 94% (79/84) previously received chemotherapy.

- There were 18 different tumor types included in the data cutoff, although only seven tumor types had at least four evaluable patients.

- The largest populations represented were gastric cancer (26/84, 31% of total) and breast cancer (14/84, 17% of total).

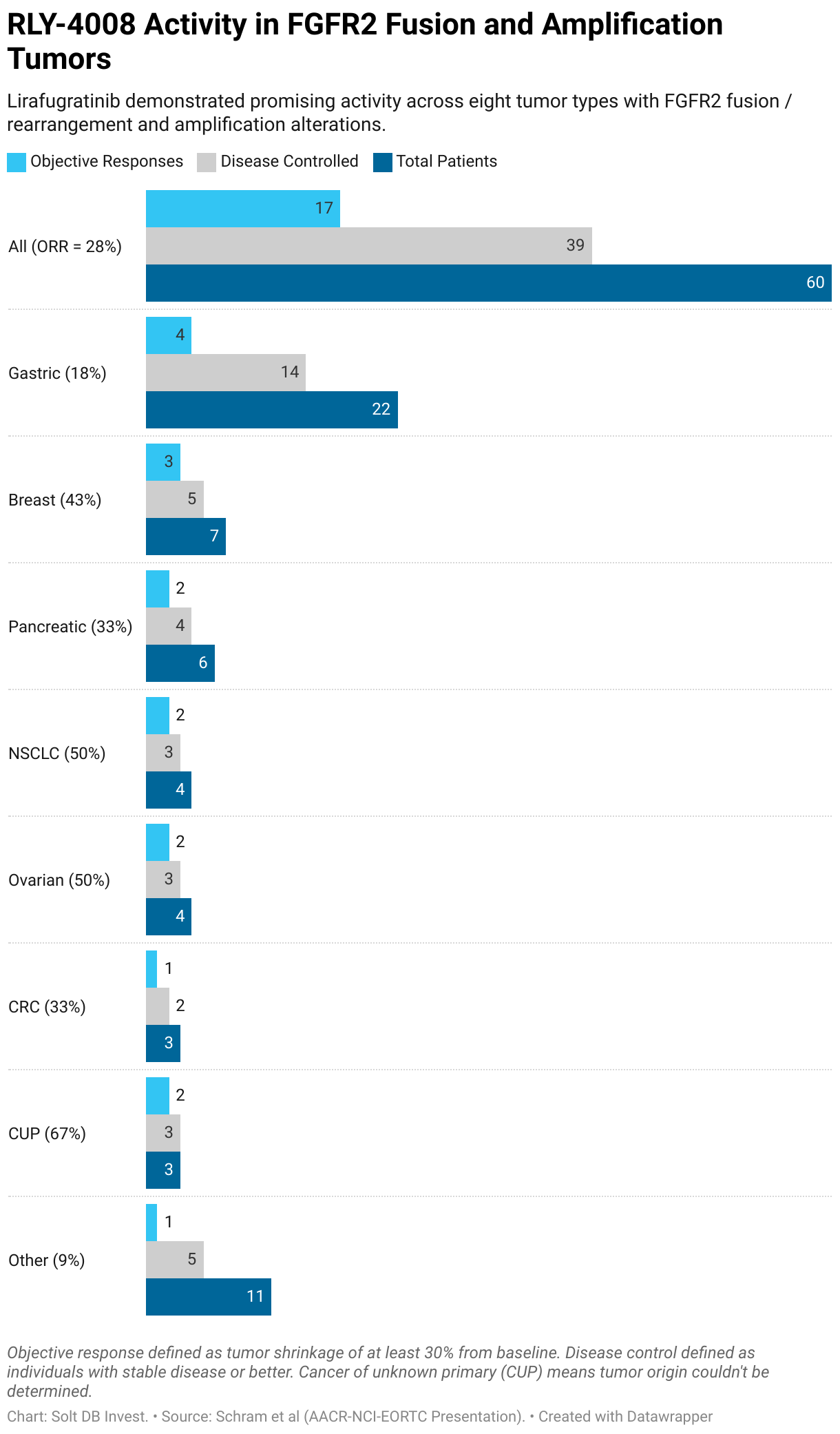

In tumors with FGFR2 fusions or amplifications, RLY-4008 demonstrated promising activity across eight tumor types, including gastric, breast, pancreatic, non-small cell lung cancer (NSCLC), ovarian, colon, and tumors of unknown origin (nerds in lab coats count this as a single, defined group).

The lead drug candidate achieved a preliminary ORR of 35% (9/26) across all FGFR2 fusions and an ORR of 24% (8/34) across all FGFR2 amplifications. The combined ORR in all fusions and amplifications was 28%.

In each cohort, responses were worse in tumors outside of the eight above. These were grouped together in the "other" category. Removing those from the calculation resulted in a combined ORR of 32.7% across all FGFR2 fusions and amplifications.

In tumors with FGFR2 mutations, RLY-4008 performed less impressively, but with additional nuances. These alterations are more common in different types of tumors, such as ameloblastic (a rare cancer that begins in bones of the jaw) and salivary cancers. This cohort achieved an ORR of 13% (3/24). If only the four primary types of tumors (ameloblastic, gastric, breast, and salivary) are included, then the asset demonstrated an ORR of 21%.

How Do These Data Compare to the Competitive Landscape?

Well, there's not much to compare against.

The competitive landscape boasts several FGFR inhibitors, but they aren't selective for FGFR2. A lack of selectivity contributes to significant dose-limiting toxicities, relatively low response rates, and relatively short duration of response across the competitive landscape.

- The best performing FGFR inhibitor in the competitive landscape achieved an ORR of 42% and a median duration of response (DOR) of about 10 months in CCA tumors with FGFR2 fusions. But in non-CCA solid tumors the best-in-class efficacy and durability fall to 15% and five months, respectively.

- RLY-4008 achieved an ORR of 82% in the same type of CCA tumors. In non-CCA solid tumors, the asset preliminarily achieved an ORR of 35% in fusions, 25% in amplifications, and 13% in mutations. It had a preliminary median DOR of eight months, although that includes ongoing responses, so the final median DOR hasn't been reached.

If the poor performance of the competitive landscape creates a wide-open opportunity for improved treatments across FGFR2 alterations, then the early data for RLY-4008 position Relay Therapeutics to take a decisive lead.

The preliminary ReFocus data included an ORR of 18% in gastric cancer driven by fusions or amplifications. Although that might not sound impressive, it compares favorably to the nearest competitor.

The lead drug candidate from Five Prime Therapeutics was an FGFR2b-selective monoclonal antibody called bemarituzumab. It achieved an ORR of 13% in FGFR2-altered gastric cancer in a phase 2 study. Thirty-four percent of patients discontinued treatment (bemarituzumab plus chemotherapy), while 83% experienced a grade 3 or higher treatment-related adverse event (TRAE). By contrast, only one of 124 patients (0.8%) enrolled in ReFocus have discontinued treatment due to TRAE. The most common grade 3 TRAE was mouth sores, which occurred in 11% of patients. RLY-4008 is also an oral medication administered by itself, providing a significant convenience advantage for patients.

Five Prime Therapeutics was acquired by Amgen for $1.9 billion, primarily to explore the potential of bemarituzumab in other tumor types. Relay Therapeutics is valued at $966 million as of market close on October 12, 2023.

Most importantly, Relay Therapeutics reported strong preliminary data in HR+, HER2- breast cancer across all FGFR2 alterations. RLY-4008 achieved an ORR of 40% (4/10) in this population, while 70% (7/10) saw their tumors shrink by any amount.

This type of breast cancer represents the largest population of FGFR2 altered tumors, representing an estimated 9,000 new cases per year in the United States. That's almost half of all FGFR2-altered cancers and 9x more prevalent than FGFR2-fusion CCA.

Additionally, Relay Therapeutics has focused the rest of its pipeline on HR+, HER2- breast cancer. That includes the company's PI3K-alpha inhibitors (RLY-2608 and RLY-5836) and paused programs for a CDK2 inhibitor (RLY-2139) and ER-alpha degrader. Within this context, it's easy to see why the company has carved out two opportunities for RLY-4008 in its pipeline: One for tumor-agnostic treatments (including CCA) and one specifically for breast cancer.

Forecast & Modeling Insights

Solt DB Invest's current model for Relay Therapeutics is already forward-looking by pricing in significant future value from RLY-4008.

On the one hand, the October 2023 tumor-agnostic data readout provides promising early signals for a broad opportunity in FGFR2. If maturing ORR data from breast cancer patients continue to demonstrate impressive activity, then that could positively impact our model. The next tumor-agnostic data readout is expected in 2024.

On the other hand, the new tumor-agnostic commercialization strategy for RLY-4008 shifts our expectation for FDA approval to the second half of 2025 or sometime in 2026. The decision to pause development of two unrelated assets in the pipeline to extend the cash runway into the second half of 2026 was directly related to this new timeline for RLY-4008. It's also possible regulators request a change in the study design to include more patients, especially since the company is studying FGFR2 alterations in at least nine tumor types.

To recap, the new tumor-agnostic commercialization strategy:

- extends the cash position (positive impact)

- delays an approval decision (negative near-term impact)

- potentially preserves a much larger commercial opportunity by protecting RLY-4008 from challengers for longer (positive long-term impact)

Given the strength of the preliminary data, RLY-4008 has the potential to earn Breakthrough Therapy designation in the tumor-agnostic setting, although that might not be granted until more mature data arrive in 2024. Solt DB Invest expects Breakthrough Therapy designation to be granted specifically in HR+, HER2- breast cancer.

As for news flow, investors can expect:

- RLY-4008 to have multiple additional data readouts (FGFR2 fusion CCA and tumor-agnostic FGFR2 alterations) in 2024

- The most important asset in the company's pipeline, the PI3K-alpha inhibitor RLY-2608, should have multiple data readouts in 2024. This may include additional data from a monotherapy regimen (only RLY-2608), more meaningful data from a combination regimen (RLY-2608 with chemotherapy) (the preliminary data spooked markets), and potentially an early look at a triple-combination regimen (RLY-2608, chemotherapy, and CDK4/6 inhibitor). The latter cohort isn't expected to begin until the end of 2023.

Margin of Safety & Allocation

(No change.)

Relay Therapeutics is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2023 model is below:

- Market close October 12: $7.91 per share

- Modeled Fair Valuation: $26.05 per share

- Allocation Range: Up to 15%

Relay Therapeutics reported 122.134 million shares outstanding as of August 4, 2023. The Margin of Safety range above assumes 134.347 million shares outstanding, which prices in 10% dilution.

Further Reading

- October 2023 press release announcing preliminary tumor-agnostic data from ReFocus

- October 2023 scientific poster presentation for preliminary tumor-agnostic data from ReFocus

- October 2023 scientific presentation for preliminary tumor-agnostic data from ReFocus

- October 2023 corporate presentation updated after reporting preliminary tumor-agnostic data from ReFocus

.svg)

-cropped.svg)