.svg)

Whereas an inhibitor drug product blocks a cellular receptor to reduce its activity, an agonist drug product binds to a cellular receptor to increase its activity. GLP-1 agonists replicate the role of a hormone called GLP-1, which is produced after eating to provide a feeling of fullness and help control blood glucose levels.

Initially developed to treat type 2 diabetes, GLP-1 agonists are now driven by the potential to treat obesity.

Obesity drugs are expected to quickly ascend the global blockbuster leaderboard and demolish records for annual and all-time drug product revenue. Why? Because *gestures broadly at Americans*… and unhealthy, unbalanced, and overworked lifestyles are the post-industrialized economy's default setting.

In 2023, Ozempic (global sales rank: 3) trailed Humira by only $46 million in total global revenue. As noted above, it probably shouldn't have been anywhere near the top 10, but off-label prescriptions for obesity drove its revenue surge.

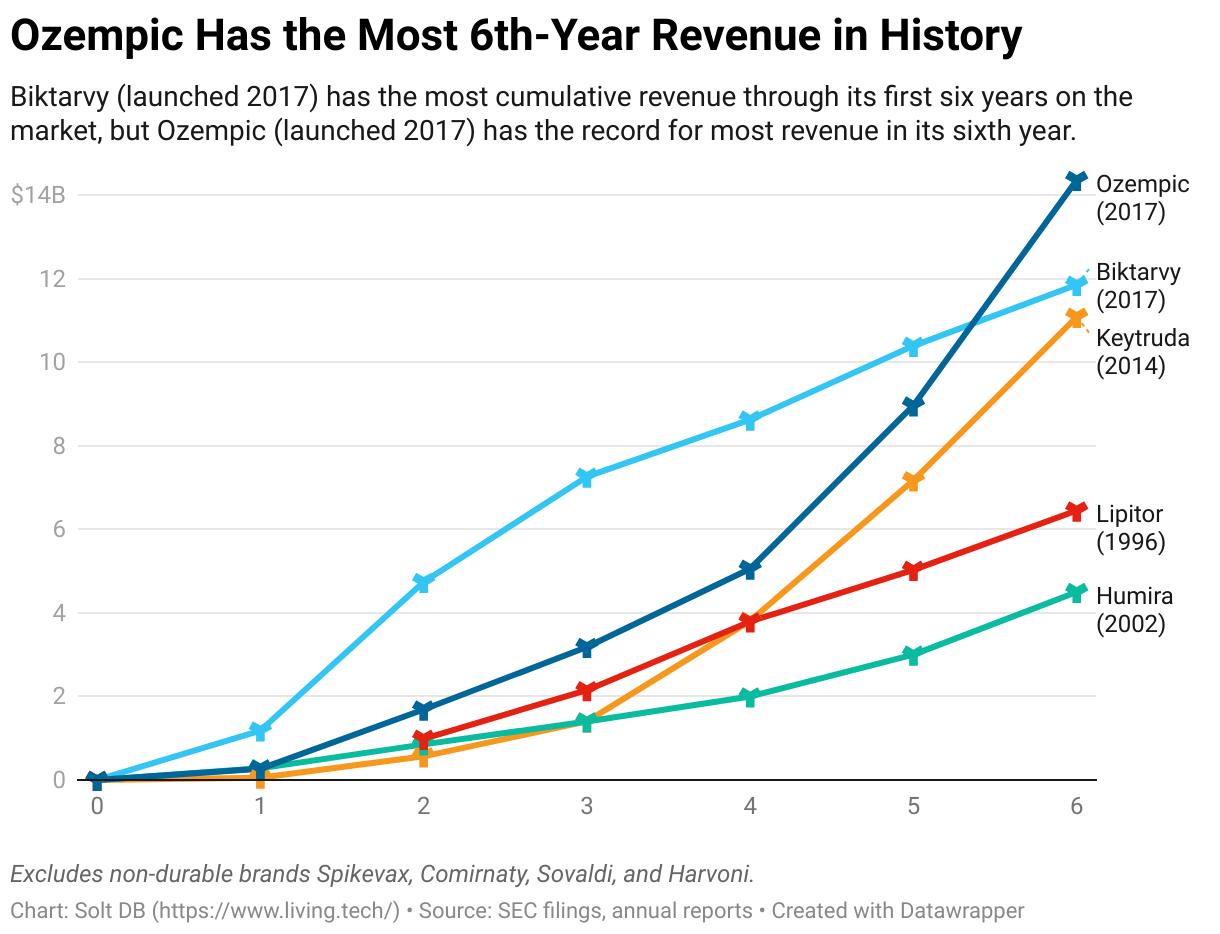

Ozempic has easily outpaced the trajectory of history's previous bestselling drug products through its first six years on the market.

The off-label use of both Mounjaro from Eli Lilly (global sales rank: 26) and Ozempic are expected to decline as drugmakers offer separate, obesity-focused brands. Zepbound (using the same active ingredient as Mounjaro) and Wegovy (using the same active ingredient as Ozempic) should ramp very quickly in the next few years. Peak annual sales estimates are as high as $45 billion apiece, although Wall Street tends to be overly bullish when predicting drug product revenues.

.svg)

.svg)

.svg)