World's Bestselling Drugs Addicted to Broken U.S. Healthcare System

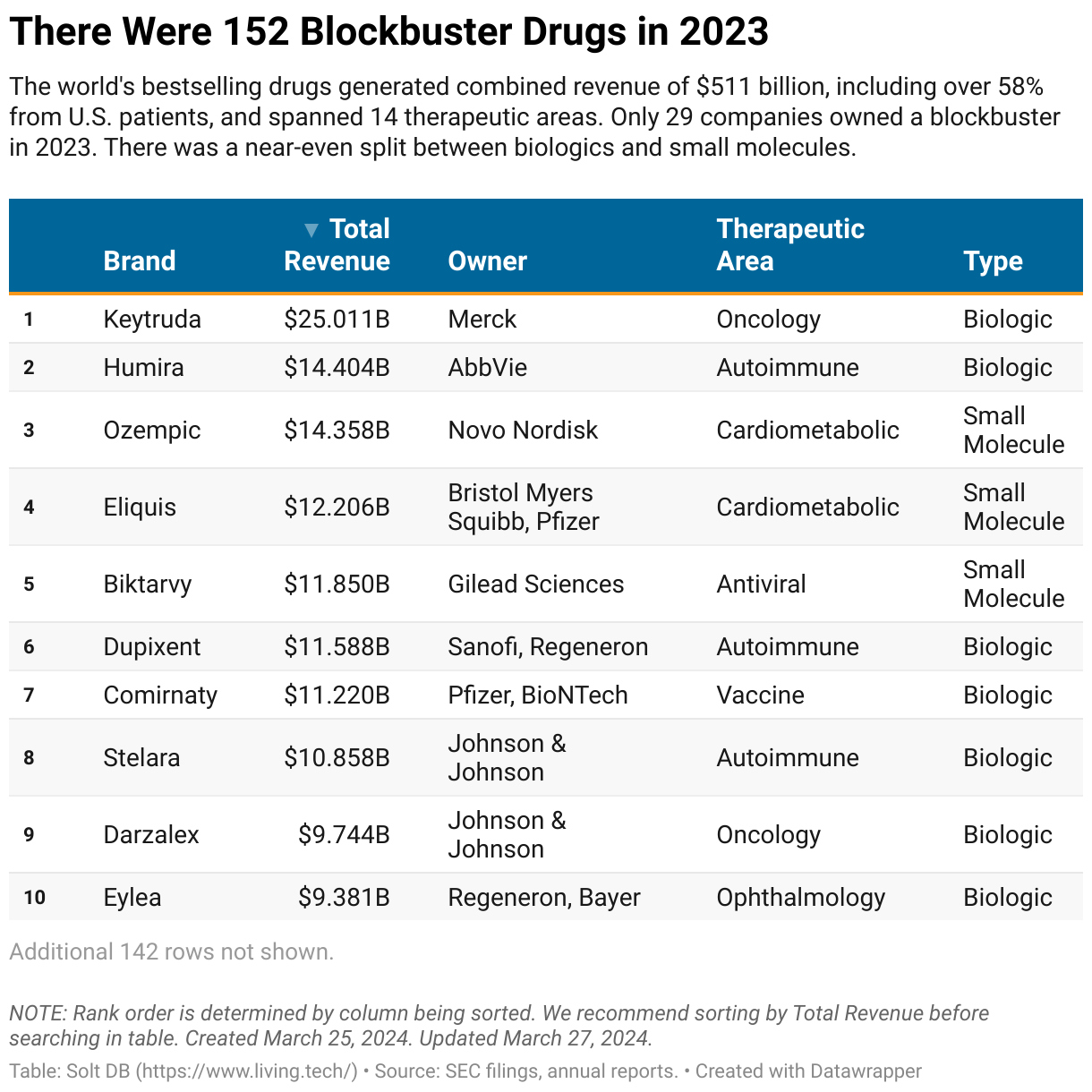

The global drug development industry boasted 152 blockbuster drugs that generated combined revenue of $511 billion in 2023. Over 58% percent ($298 billion) was generated from patients in the United States.

By

Maxx Chatsko

Updated

February 4, 2026

Published

March 25, 2024

00

minute read

Blockbuster drugs, defined as therapeutic products generating at least $1 billion in annual revenue, are the key to outsized success for drug developers.

Emerging drugmakers that own even one bestselling drug are always among the world's largest drug developers by market cap – and are often acquired. Incyte is the smallest company to wield a blockbuster. It weighs in at a healthy $12.7 billion market valuation, which makes it one of the largest 45 drug developers globally.

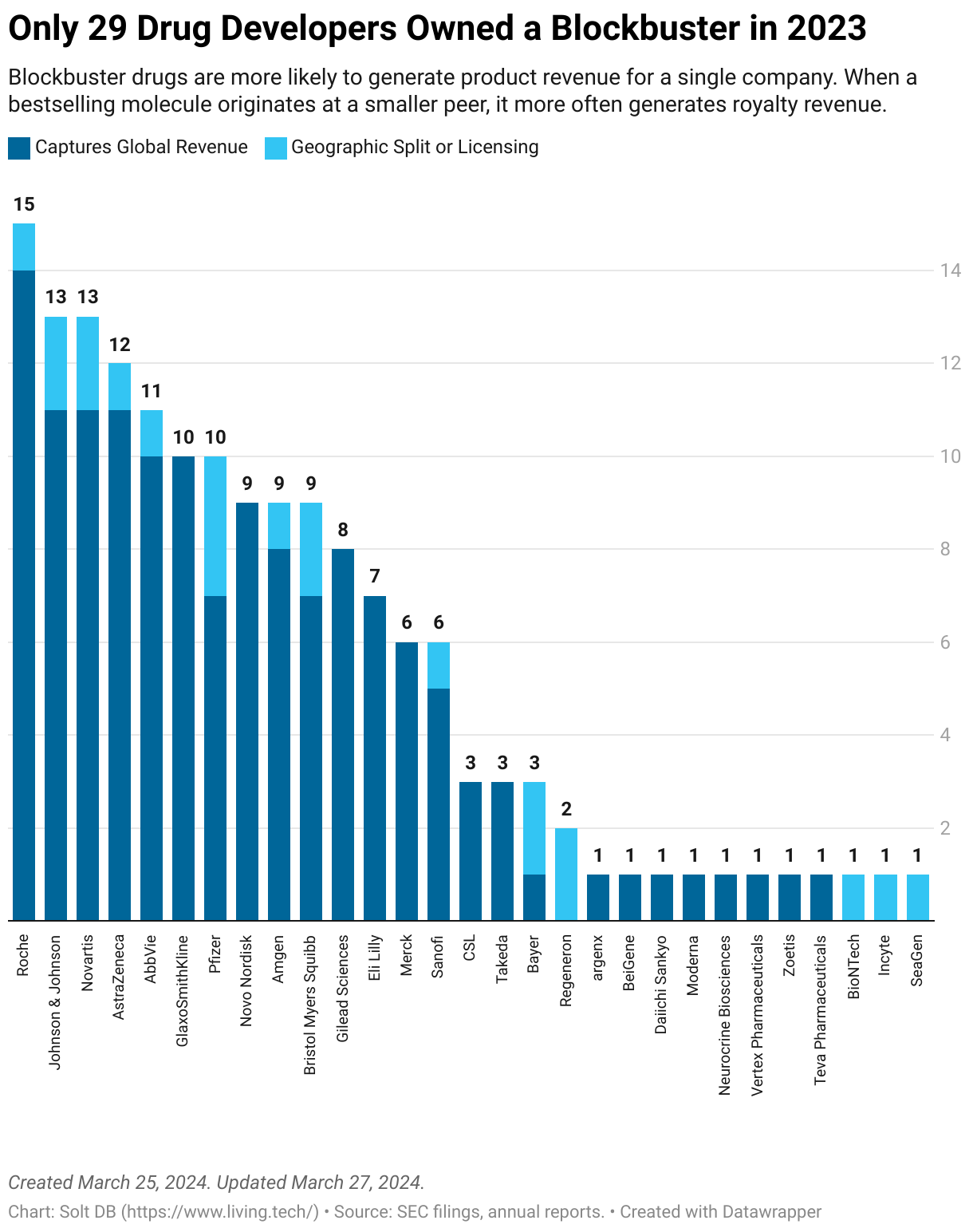

Meanwhile, industry titans need a steady stream of bestselling drugs to offset revenue churn from products in decline, a unique (and frustrating) characteristic of commercializing therapeutics. That helps to explain why all the world's blockbusters are concentrated among just 29 different companies.

That's the high-level overview. The most valuable insights come from digging much deeper.

Solt DB compiled the most comprehensive dataset of global blockbuster drugs ever made. As a one-person public benefit company, I'm making it freely available – with no ads, clickbait, or email capture.

The dataset offers unparalleled insights allowing scientists and investors to better understand the strategic decisions made by industry leaders – and just how much the global industry relies on America's broken healthcare system.

Need more finch? Here's our newsletter.

Welcome to The Voyage!

Oops! Something went wrong while submitting the form.

How Many Blockbuster Drugs Were There in 2023?

There were 152 drug products with at least $1 billion in full-year 2023 revenue. Solt DB only included revenue generated between January 1 and December 31 for companies with non-standard fiscal years. When a business had a non-standard fiscal year, we stitched together quarterly revenue totals to align with the calendar. This provides a more accurate comparison by normalizing regulatory changes, competitive launches, and so on.

Eight therapeutics eclipsed $10 billion in annual revenue – and two reached that level from U.S. sales alone (Keytruda and Humira). For perspective, five years ago only one blockbuster crossed this sales level on a global basis (Humira) – and only four had reached this milestone in history as of 2018 (Lipitor, Sovaldi, and Harvoni).

How Many Companies Had a Blockbuster Drug in 2023?

Only 29 drug developers boasted a blockbuster drug product in 2023. That tally includes Adcetris from SeaGen, which was acquired by Pfizer during the year.

Seven drug developers wielded at least 10 blockbusters during the period. This group had an average market valuation of $228 billion, with GlaxoSmithKline ($87.8 billion) being the smallest and AbbVie ($319 billion) being the largest pure-play drug developer. The latter excludes Johnson & Johnson ($392 billion), which has a large medical devices segment.

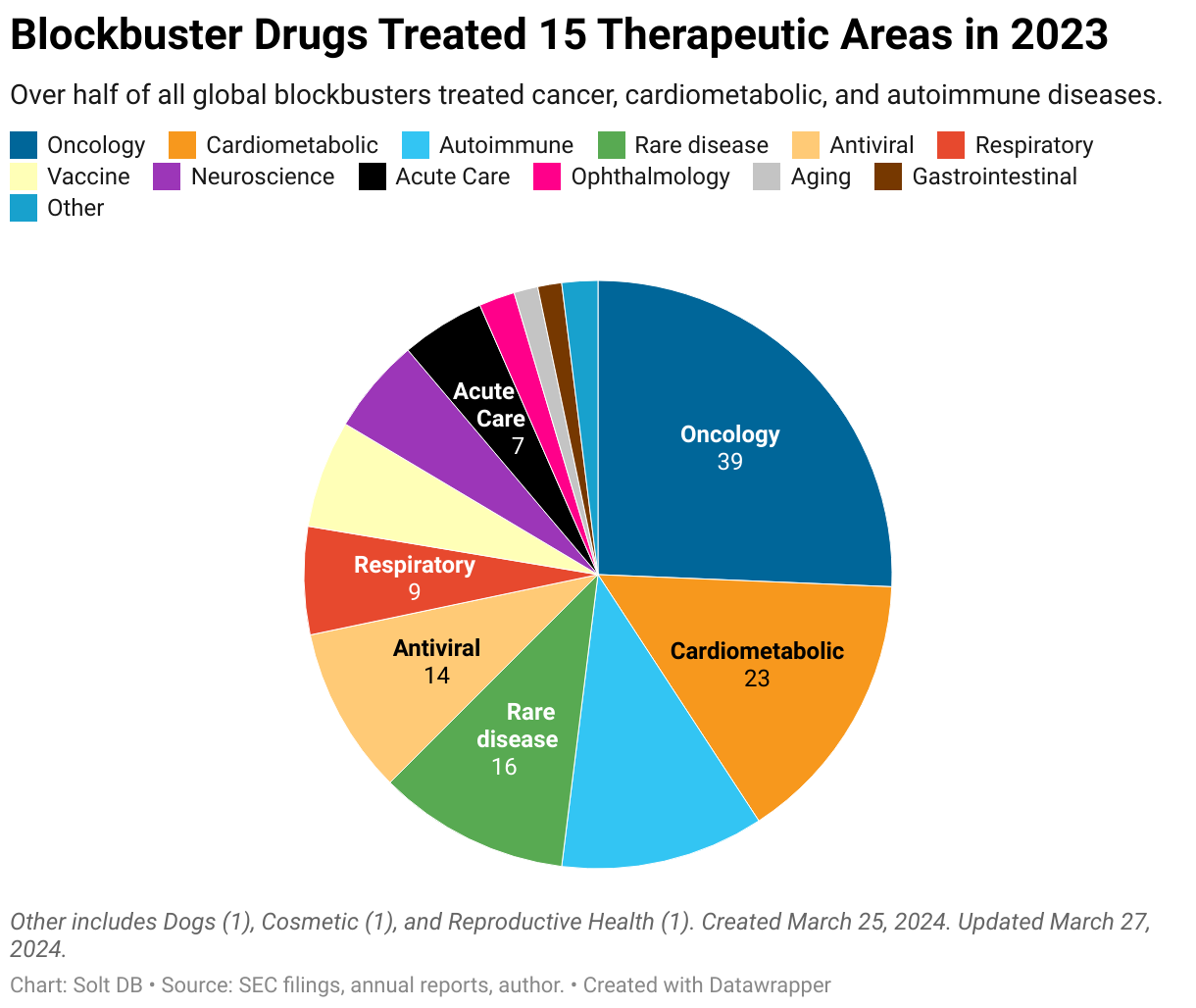

What Medical Conditions Did Blockbuster Drugs Treat in 2023?

There were 15 unique therapeutic areas represented among blockbuster drugs in 2023, including one solely for dogs (unless your husband or boyfriend has fleas…).

A therapeutic area describes the type of diseases treated by a molecule. For example, oncology is the therapeutic area for cancer drugs, whereas cardiometabolic treatments include things like insulin and obesity medications.

Therapeutics for oncology (39/152, 25%), cardiometabolic diseases (23/152, 15%), and autoimmune disorders (17/152, 11%) were the most common. This trio of therapeutic areas represented just over half of all global blockbusters. They represented seven of the top 10 bestsellers, or eight of the top 10 if the coronavirus vaccine Comirnaty from Pfizer and BioNTech is excluded.

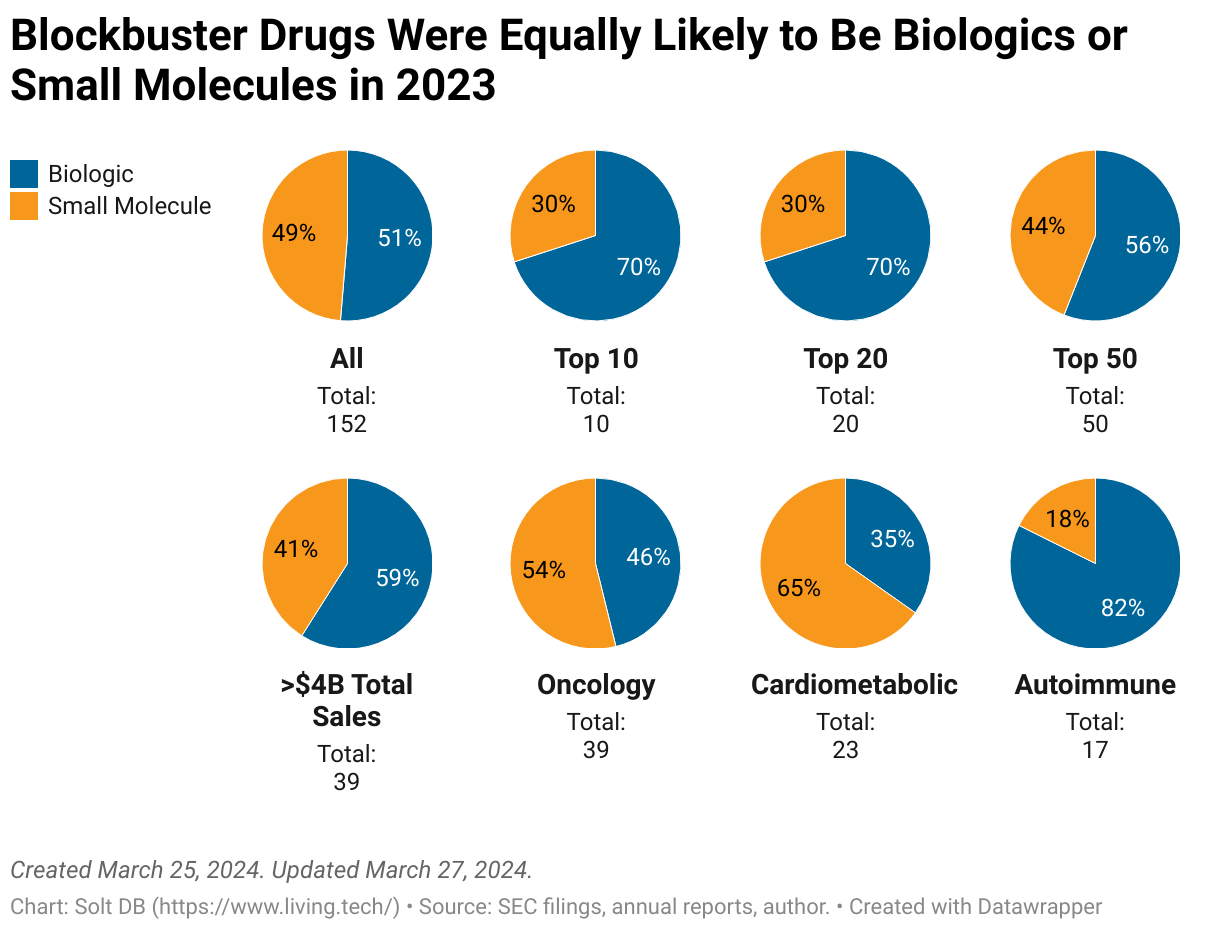

How Many Blockbuster Drugs Were Biologics or Small Molecules in 2023?

The word "biotech" is often used interchangeably with "drug developer," but that's incorrect. Imprecise language impedes our ability to understand and analyze our world.

To be accurate and precise, "biotech" means using biology as technology. There are six major biotech sectors, including biopharma, industrial biotech, agricultural biotech, and environmental biotech. Biopharma is different from pharma. The former develops biologic drugs (enzymes, antibodies, nucleic acids, gene therapies, gene editors, vaccines, and so on) and the latter develops small molecule drugs (inhibitors, antivirals, peptides, radiopharmaceuticals, and so on).

Among blockbusters in 2023, there was a near-even split between the number of biologics (78/152, 51%) and small molecules (74/152, 49%). However, 70% of the top 20 bestselling drugs globally (14/20) were biologics.

Biologics were responsible for 57% of total revenue from all blockbuster drugs, but that will change with the rise of drug products prescribed to treat obesity – including off-label use of type 2 diabetes medications. The trio of semaglutide brands from Novo Nordisk (Ozempic, Wegovy, and Ryvelsus) and the duo of tirzepatide brands from Eli Lilly (Mounjaro and Zepbound) utilize peptides, or short protein fragments, but are currently classified as small molecule drug products by regulators.

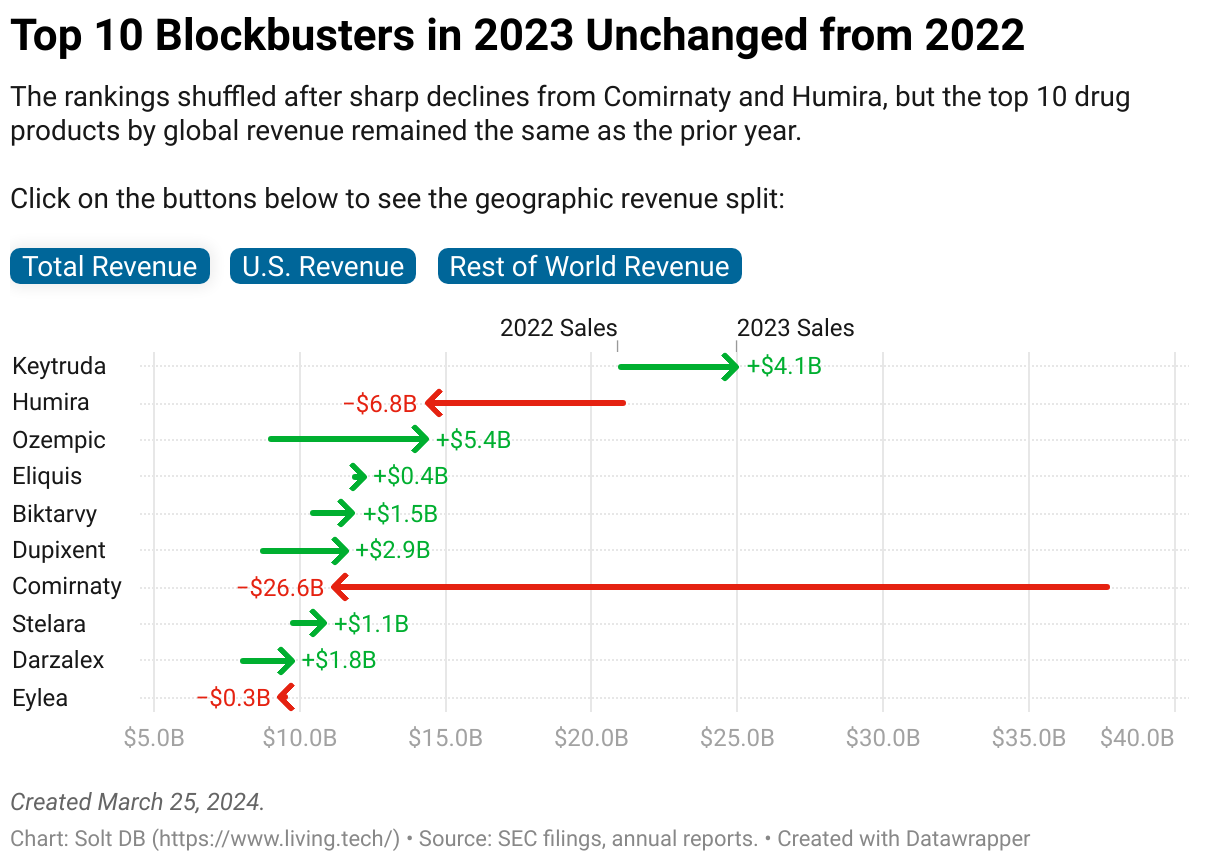

What Were the Bestselling Drugs in 2023?

The top 10 bestselling drug products of 2023 remained unchanged from the prior year, but the list will see significant changes in the next few years.

The do-it-all autoimmune therapy Humira (sales rank: 2) and world-leading coronavirus vaccine Comirnaty (sales rank: 7) are likely to fall from the top 10. Meanwhile, type 2 diabetes medication Ozempic (sales rank: 3) ranked highly in 2023 primarily because it was used off-label to treat obesity. It could be replaced by Novo Nordisk's approved obesity medication, the injectable Wegovy (sales rank: 29), which uses the same active ingredient as Ozempic.

The cancer immunotherapy Opdivo from Bristol Myers Squibb (sales rank: 11) and autoimmune treatment Skyrizi from AbbVie (sales rank: 14) are likely to replace the fallen brands in the top 10 by 2025. It's possible the recently-approved obesity medication Zepbound from Eli Lilly (unranked) will make an unprecedented run to crash the top 10 in the next few years, too.

The top three bestselling drugs of 2023 each capture a different part of a commercial drug product's lifecycle. They also represent the three bestselling drug classes of all-time – if the rise of obesity medications is penciled in prematurely.

The Most Successful Drug Class By Far (So Far)

Keytruda from Merck (sales rank: 1) became the new bestselling drug in the world in 2023. In fact, it generated the most revenue of any drug product in history in a single annual period, excluding coronavirus vaccines.

The cancer immunotherapy generated the most revenue of any drug product in both the United States and outside the United States in 2023. It generated twice as much ex-U.S. revenue ($9.897 billion) as the next closest non-vaccine drug brand (Ozempic was a distant second with $4.951 billion).

The PD-1 inhibitor blocks the PD-1 receptor on T cells, which allows them to avoid cancer cell defenses and kill cancer cells more effectively. The mechanism of action allows PD-1 / L1 inhibitors to be valuable foundations for combination therapies in both solid tumors and blood cancers.

There are nine approved drug products in this class, including four blockbusters. Keytruda leads a group including Opdivo from Bristol Myers Squibb (sales rank: 11), Imfinzi from AstraZeneca (sales rank: 34), and Tecentriq from Roche (sales rank: 36). Libtayo from Regeneron is likely on its way to becoming a blockbuster, but had $869 million in global revenue in 2023.

Although biosimilar competition will arrive for intravenously-administered PD-1 / L1 inhibitors in 2028, subcutaneous formulations are likely to keep generic competition at bay and continue the dominance of the leading brands.

The End of an Era

TNF-alpha inhibitors had a historic run, but it's now coming to an end as biosimilars, next-generation autoimmune disease targets, and more convenient oral formulations arrive.

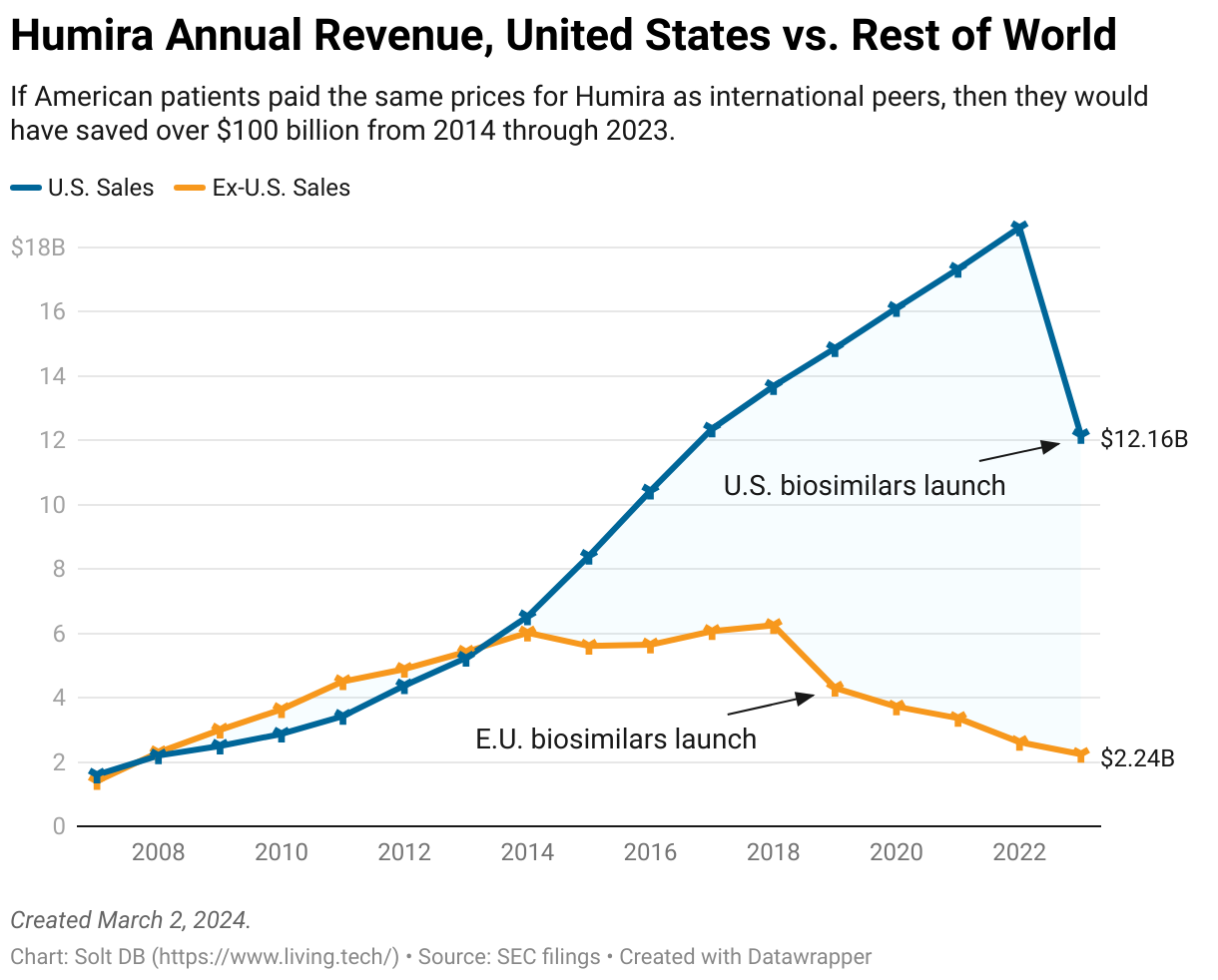

Humira from AbbVie (sales rank: 2), formerly the world's top seller, fell swiftly as biosimilars encroached on its turf in 2023. Sort of.

AbbVie increased the rebates and discounts offered to pharmacy benefit managers (PBMs) to keep biosimilars at bay – and it worked. The bestselling adalimumab biosimilar, Amjevita from Amgen, captured just 0.99% of total revenue from all adalimumab products. Competitors expect a slow ramp in 2024 to accelerate in 2025 when drug pricing components of the Inflation Reduction Act go into effect.

In February 2024, AbbVie issued initial guidance expecting Humira to generate $9.6 billion in full-year 2024 revenue. That's subject to change if the group of 10 approved biosimilars gain traction – or continue to struggle. Revenue will fall much more precipitously in 2025.

The Rise of GLP-1 Agonists for Obesity

Whereas an inhibitor drug product blocks a cellular receptor to reduce its activity, an agonist drug product binds to a cellular receptor to increase its activity. GLP-1 agonists replicate the role of a hormone called GLP-1, which is produced after eating to provide a feeling of fullness and help control blood glucose levels.

Initially developed to treat type 2 diabetes, GLP-1 agonists are now driven by the potential to treat obesity.

Obesity drugs are expected to quickly ascend the global blockbuster leaderboard and demolish records for annual and all-time drug product revenue. Why? Because *gestures broadly at Americans*… and unhealthy, unbalanced, and overworked lifestyles are the post-industrialized economy's default setting.

In 2023, Ozempic (sales rank: 3) trailed Humira by only $46 million in total global revenue. As noted above, it probably shouldn't have been anywhere near the top 10, but off-label prescriptions for obesity drove its revenue surge.

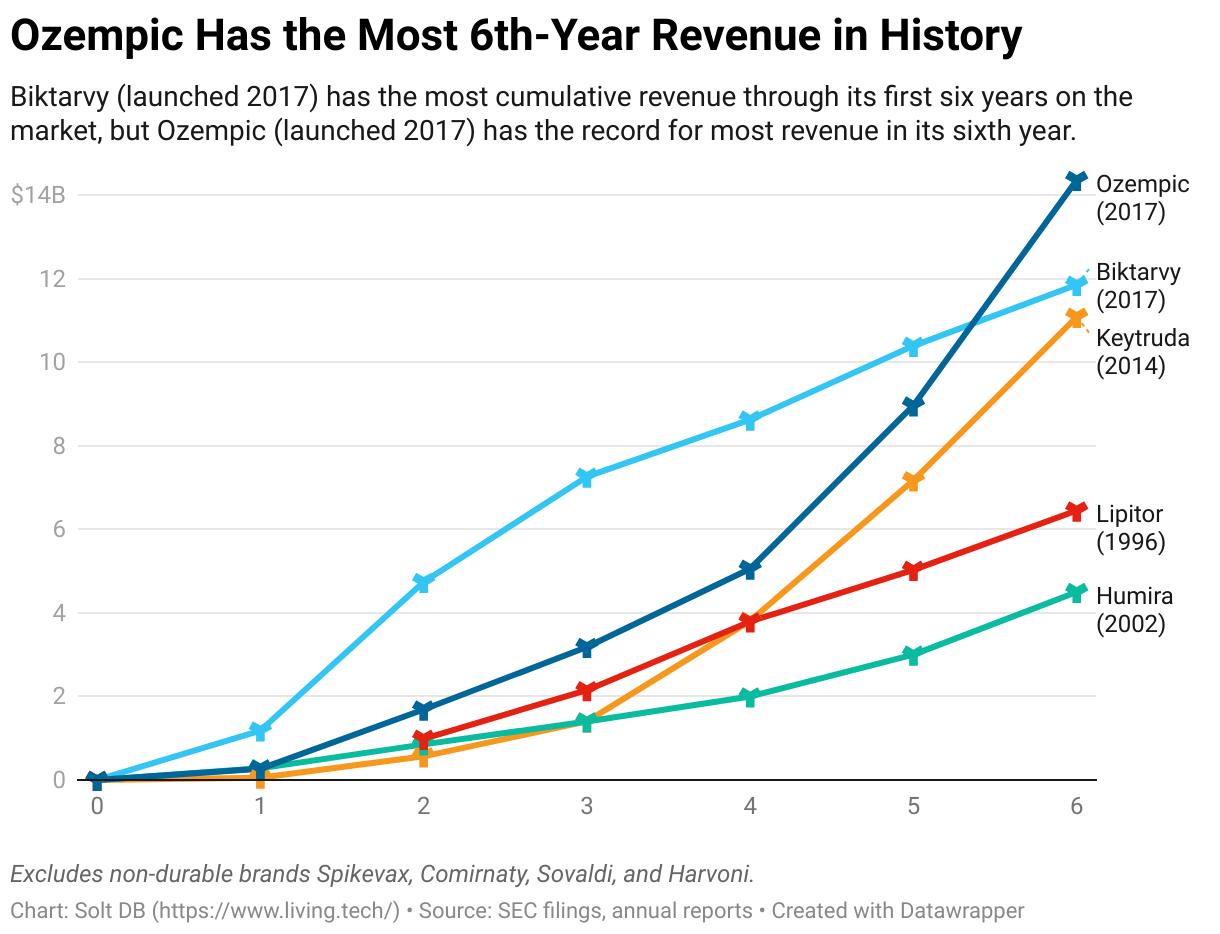

Ozempic has easily outpaced the trajectory of history's previous bestselling drug products through its first six years on the market.

The off-label use of both Mounjaro from Eli Lilly (sales rank: 26) and Ozempic are expected to decline as drugmakers offer separate, obesity-focused brands. Zepbound (using the same active ingredient as Mounjaro) and Wegovy (using the same active ingredient as Ozempic) should ramp very quickly in the next few years. Peak annual sales estimates are as high as $45 billion apiece, although Wall Street tends to be overly bullish when predicting drug product revenues.

Odds and Ends

There are some oddities in the blockbuster drug product dataset, too.

Generics Be Damned: Although generic competition often triggers the beginning of a bestselling drug's demise, it doesn't always knock products below the $1 billion mark. Roughly one-in-ten blockbuster drugs (15/152, 10%) had generic competition in 2023. That includes Lipitor from Viatris (sales rank: 104), which generated full-year 2023 revenue of $1.559 billion. The cholesterol medication has faced generic competition since May 2012.

Who's a Good Boy?: One blockbuster drug product helps dogs keep ticks, fleas, and other parasites at bay. Simparica and Simparica Trio from Zoetis (sales rank: 143), formerly the animal health division of Pfizer, generated full-year 2023 revenue of $1.111 billion.

The Anti-Blockbuster: Due to an accounting quirk, Paxlovid from Pfizer (sales rank: 126) had full-year 2023 revenue of negative $1.289 billion in the United States. It generated $2.568 billion in international sales, or $1.279 billion worldwide.

United States Remains the Global Industry's Gold Mine

The top 20 bestselling drugs of 2020 generated 64% of their global revenue from the United States, according to Axios. Solt DB's dataset shows not much has changed in the last three years.

The top 5 bestselling drugs generated 70.7% ($55.010 billion) of revenue from the United States in 2023.

The top 10 bestselling drugs leaned on American patients for 64.6% ($84.398 billion) of global revenue in 2023.

The top 20 bestselling drugs settled at 61.6% ($126.645 billion) in 2023.

There were 145 blockbusters that reported geographic revenue splits, or 144 excluding Paxlovid (which had negative revenue in the United States in 2023). Among that group, the United States was responsible for 59.3% ($298.233 billion) of total revenue.

When the list of 144 blockbusters with available data is further truncated to exclude the three coronavirus vaccines (including Johnson & Johnson's unbranded product), which generate no more than 26% of revenue from the United States, the world's blockbuster drugs generated 60.8% of revenue from American patients in 2023.

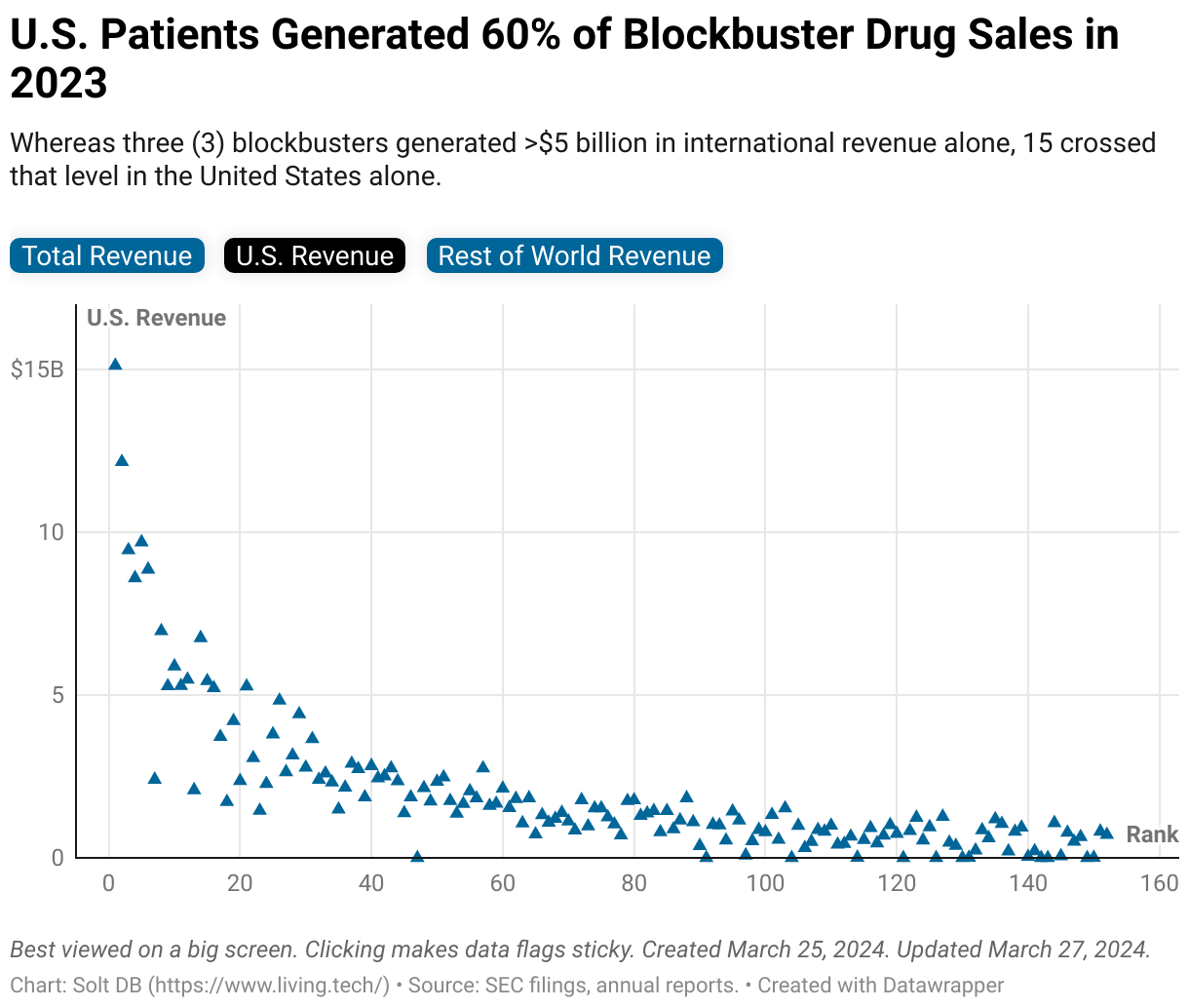

Whereas only three drug products generated over $5 billion in annual revenue from international markets alone, 15 blockbusters reached that level from sales in the United States alone. Two that just missed the mark, Mounjaro ($4.834 billion) and Wegovy ($4.415 billion), will likely join the group in 2024.

Consider the geographic revenue split between the United States and the rest of the world for all 152 blockbuster drugs in 2023. This interactive chart is best viewed on a big screen.

Why is the United States responsible for the overwhelming majority of global drug product revenue?

The primary reason is U.S. Congress hasn't legislated for federal agencies to regulate drug prices in a meaningful way. That may begin to change when key pieces of the Inflation Reduction Act (IRA) go into effect in 2026. If industry challenges don't disrupt the timeline or details, then Medicare will gain the ability to negotiate prices for 10 drug products in 2026, an additional 15 drug products in each 2027 and 2028, and up to 20 additional drugs each year after that.

Medicare will only be negotiating prices for up to 80 drug products total by 2030. As this dataset shows, that would capture just 54% of all global blockbuster drugs in 2023. By the start of the next decade, there will likely be more than 149 blockbuster brands – and not every expensive or overpriced drug becomes a blockbuster.

Despite loud protests from drug developers, there are some large caveats to the drug pricing components of the IRA. It's better than nothing, but it doesn't represent meaningful drug pricing regulation within the United States for all Americans.

Prices negotiated by Medicare are unlikely to match international prices for the same drug products, which can sometimes cost hundreds of times less overseas.

Medicare will select drug products based on which prescriptions cost the most for the program, not necessarily the most disproportionately priced medications on the market.

Those costs will be determined on a gross basis, but the true costs are offset by rebates received and other mechanisms used by drug developers.

To be clear, many blockbuster drugs will not be impacted by Medicare's limited new price negotiation powers.

One notable exclusion from price negotiations is the HIV therapy Biktarvy from Gilead Sciences (sales rank: 5). The antiviral costs between $15 to $30 per month in India, France, Germany, and other European countries. It costs over $4,000 per month in the United States. Although patients with insurance might not pay that directly, the broken American healthcare system pays the full cost. That impacts everyone in the form of higher insurance premiums and larger federal budget deficits.

Biktarvy generated 82%, or $9.692 billion, of its total global revenue from patients in the United States. It generated just 13% of its revenue from Europe, where there are twice as many HIV patients than the United States. From 2022 to 2023, the blockbuster grew U.S. revenue by $1.182 billion and European revenue by just $150 million.

The global drug development industry will continue to leverage significant price discrepancies between the United States and the rest of the world until meaningful drug pricing regulations become law.

Yes, biotech stocks can beat the market.

Solt DB is a biotech equities research firm. As of December 31, 2025, our real-money investment portfolio is outperforming the S&P 500 by 29.9%, Nasdaq 100 by 24.3%, XBI by 14.5%, and Ark Genomic Revolution ETF by 30.4%.

Subscriptions to investment research fund our mission as a public benefit company and keep us fiercely independent -- so we can keep giving tech bros the bird. No ads, no clickbait, no hype. Join today for $26.25 per month.

.svg)

.svg)

%20(squoosh).jpg)

%20(squoosh).jpg)

%20(thumbnail)%20(squoosh).jpg)

.svg)

.svg)

.svg)