.svg)

Selecta Biosciences has planted a "For Sale" sign in the front yard. Will it work?

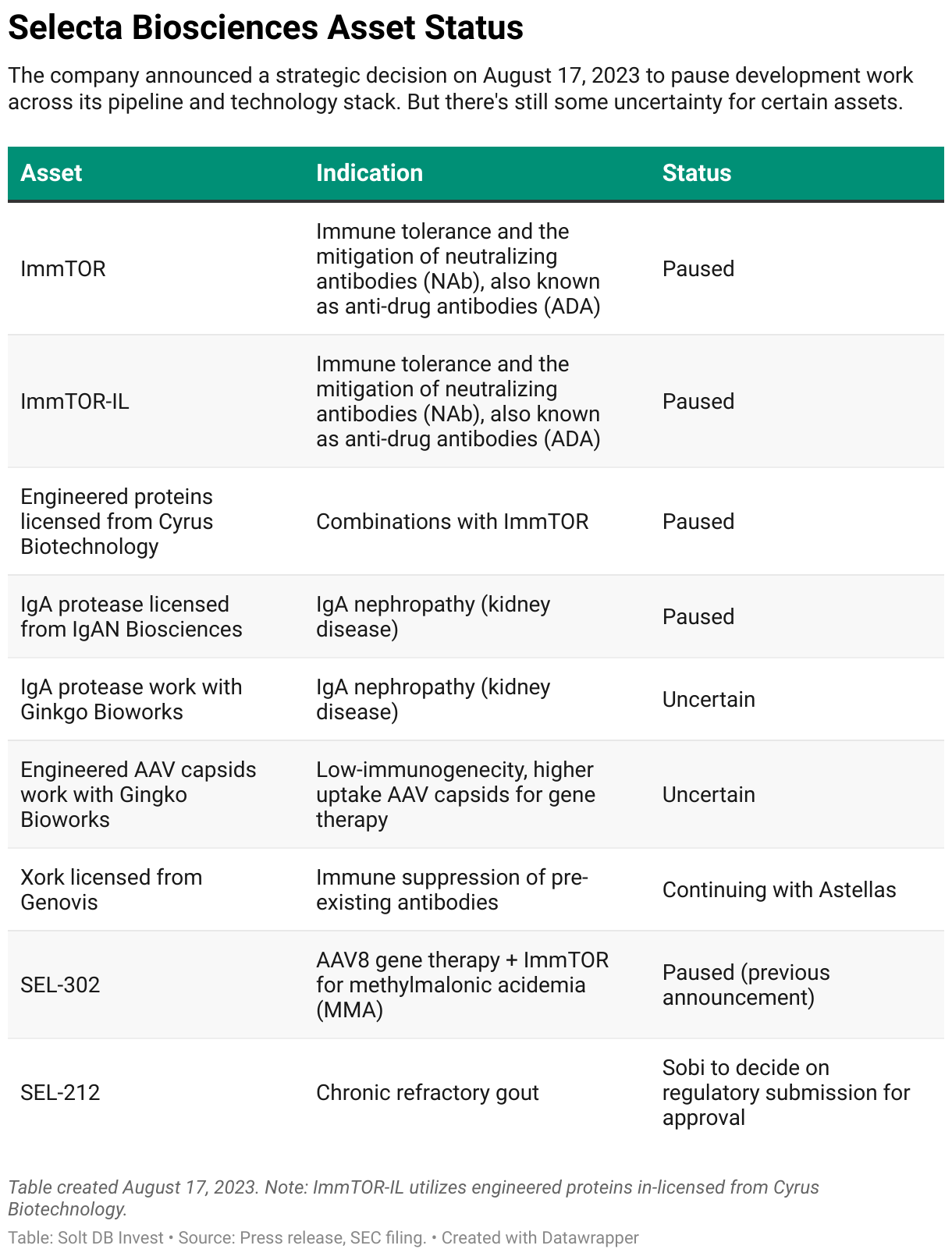

The precommercial drug developer announced a strategic decision to pause all development work aside from contractual obligations to Astellas for the immunoglobulin G (IgG) protease asset named Xork. The business will seek to outlicense rights to all other assets, discontinue assets that cannot be monetized via business development, and focus remaining bandwidth and resources on supporting SEL-212 in chronic refractory gout.

These decisions are expected to extend the company's cash runway into 2027, although that includes receiving potential regulatory and commercial milestones for the regulatory submissions and market launch of SEL-212. If Sobi decides not to proceed with the asset for any reason, then Selecta Biosciences will be severely and negatively impacted.

There are a handful of additional details that aren't evident from reading the press release alone. Additionally, there are a few different ways the strategic decision could shake out.

Hitting Pause on the Pipeline and Technology Stack

Selecta Biosciences announced in a press release it will pause nearly all development of preclinical and clinical assets, then proceeded to list most assets. The key phrases in that sentence are "press release," "nearly all", and "list most."

The press release made no mention of two development projects with Ginkgo Bioworks. Additionally, the press release mentioned "the immunoglobulin A (IgA) protease for IgA nephropathy (IgAN)." This is presumably a reference to the asset in-licensed from IGAN Biosciences, but Selecta Biosciences technically has an active project with Ginkgo Bioworks for a separate IgAN asset.

Curiously, the quarterly filing with the U.S. Securities and Exchange Commission (SEC) is careful to include language that development work has been paused when discussing each asset. It doesn't include this language when discussing development projects from Ginkgo Bioworks.

That's not necessarily a good thing.

Selecta Biosciences may be unable to cancel the development agreements with Ginkgo Bioworks without incurring certain costs, or not until a specified point in time. For example, the company will need to issue 1.339 million shares of common stock to Ginkgo Bioworks in the third quarter of 2023 for the successful completion of a development for engineered AAV capsids achieved in milestone in July 2023.

There are other potential reasons for the careful wording in the 10-Q.

Ginkgo Bioworks likely needs to manage optics for the strategic decision from Selecta Biosciences, too. Although the horizontal cell engineering platform added agreements with $2 billion in combined potential milestones in 2022, over half were from the agreement with Selecta Biosciences for engineered AAV capsids. The company recently reduced full-year 2023 revenue guidance, so having the largest source of potential milestones terminate development work weeks later wouldn't help.

Anyway, Ginkgo Bioworks will be in our coverage ecosystem expansion soon, so let's get back to Selecta Biosciences. What happens next?

Multiple Paths Forward for the Tech Stack

Selecta Biosciences announced it intends to reserve resources and bandwidth for supporting commercial preparation activities for SEL-212. The company revealed internal peak annual sales estimates of over $700 million. While investors might question the timing of coughing up that projection, Solt DB Invest has previously estimated peak annual sales potential of at least $500 million for SEL-212. As we wrote in March 2023:

SEL-212 is unlikely to dislodge Krystexxa as the market leader (or even come close), but it boasts a clear advantage in convenience and could relatively easily compete on price. The drug product should generate peak annual sales of at least $500 million.

There are a few paths forward for Selecta Biosciences.

Scenario 1: A pause really could be just that – a pause. If the company monetizes its rights to SEL-212, then it could receive a significant upfront cash payment exceeding $200 million. That could extend the cash runway past 2027 while resuming development work across the pipeline.

Selecta Biosciences is eligible to receive:

- $65 million in milestones for regulatory and commercial launch milestones, which can be earned in full by earned U.S. Food and Drug Administration (FDA) approval and dosing the first patient.

- $550 million in sales milestones, which would take years to earn and are unlikely to be fully earned in any scenario. For example, commercial sales milestones are often achieved by notching certain annual sales levels. If $250 million of the total is payable for achieving $1 billion in annual sales, then that will take a very long time to occur – and is unlikely to occur at all.

- Double-digit royalties, which can be earned beginning with the first prescription.

Scenario 2: Selecta Biosciences may not want to sell its rights to SEL-212. In an easy-to-overlook detail, the company in 2021 elected to opt out of the installment sale method of taxation for Sobi milestone and royalty revenue. That's a bean-counting mouthful, but it means the first $400 million or so of future revenue from SEL-212 is tax-free. However, this likely makes the asset more valuable to monetize upfront and could also make the company a more attractive acquisition target.

Scenario 3: Selecta Biosciences could be an acquisition target. This is fun to think about, but such a scenario is complicated by a few things.

First, the decision to pre-pay taxes on SEL-212 could make Selecta Biosciences an attractive acquisition target, including by a non-traditional suitor such as a private equity firm. The decision to pause all development work and seek licenses to existing assets could strengthen this type of acquisition.

Second, the competitive landscape for AAV gene therapy is separating into the haves and have nots. Whereas companies such as Takeda have discontinued all development work in AAV gene therapy (a potential headwind for Selecta Biosciences), companies such as Astellas and AstraZeneca have been making significant investments in the space (potentially providing a tailwind).

Third, it could make sense for Sobi to acquire Selecta Biosciences, which could be completed for a significant premium to the current share price while still saving money from long-term milestone and royalty payouts. But Sobi hasn't been as enthusiastic about SEL-212 in public comments as investors might have hoped. It could still decide to return the asset. Sobi is also the only entity in the world that wouldn't enjoy the tax-free benefits of SEL-212 by acquiring Selecta Biosciences.

Scenario 4: If Sobi returns the rights to SEL-212, then Selecta Biosciences could try to advance the asset through regulatory approval. The strategic decision to pause all development work preserves cash for this potential scenario. However, the company doesn't have enough resources to launch SEL-212.

Forecast & Modeling Insights

(Downgraded allocation suggestion.)

Solt DB Invest continues to model a fair valuation for Selecta Biosciences of roughly $450 million, which is primarily determined by the value of SEL-212. As we wrote in May 2023:

Aside from SEL-212, every other asset and piece of the company's technology stack remains in preclinical development. These assets do not make meaningful contributions to our model. As a result, so long as the opportunity with SEL-212 remains intact, so will our model. Regulatory and commercial plans are up to Sobi.

That model remains intact – for now. If Sobi walks away, then our model and fair valuation would be negatively impacted.

Solt DB Invest is updating its dilution estimate for its current model. We now account for all outstanding warrants, whereas our previous model only accounted for the 2022 Warrants. Additionally, we have accounted for the 1.339 million shares that will be issued to Ginkgo Bioworks during the third quarter of 2023. The diluted model now assumes 185.995 million shares versus 172.300 million previously.

As a result, our modeled fair valuation on a per share basis has been reduced to $2.42 per share, compared to $2.67 per share previously.

To account for the increased risk profile, Solt DB Invest has downgraded the suggested allocation to up to 2.5%, compared to up to 5% previously.

Margin of Safety & Allocation

(Updated dilution estimate, reduced allocation suggestion.)

Selecta Biosciences is considered a Growth (Speculative) position. The current modeled fair valuation for the company based on our 2023 model is below:

- Market close August 17: $1.12 per share

- Fair valuation: $2.42 per share

- Allocation Range: Up to 2.5%

Selecta Biosciences reported 153.428 million shares outstanding as of August 4, 2023. The modeled fair valuation above assumes 185.995 million shares outstanding.

Further Reading

- August 2023 press release announcing strategic decision and second-quarter 2023 business update

- August 2023 quarterly filing (10-Q) detailing second-quarter 2023 operations

- May 2023 research note analyzing recent developments in AAV gene therapy landscape

- March 2023 research note analyzing phase 3 outcomes for SEL-212 and market opportunity versus Krystexxa

.svg)

-cropped.svg)