.svg)

Growth stocks tend to reach an inflection point when the underlying business begins to generate operating income. That's both good and bad news for Twist Bioscience.

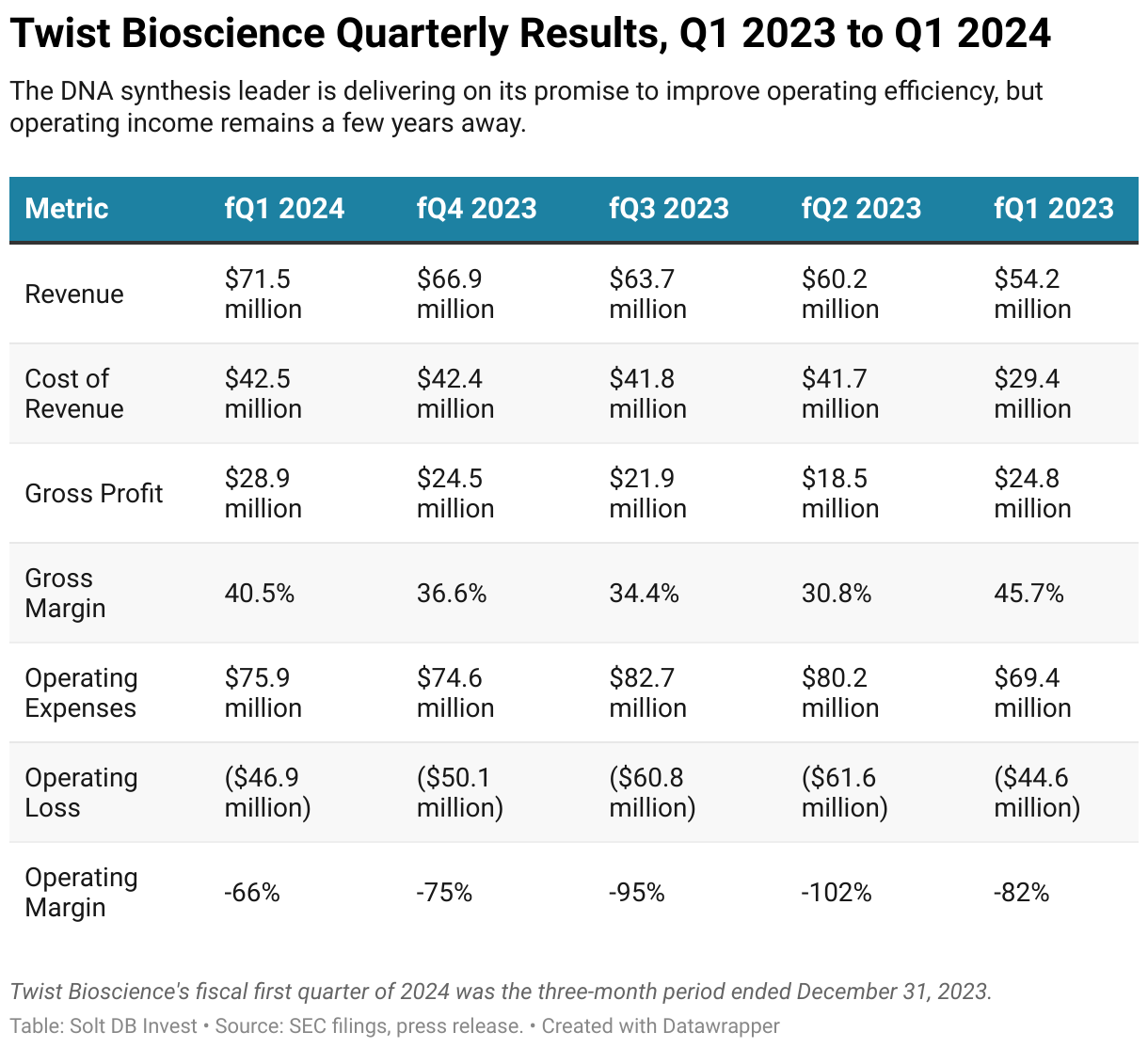

On the one hand, the business is delivering on its promise to improve operating efficiency and remain fiscally disciplined. In the fiscal first quarter of 2024 (the three months ended December 31, 2023), the DNA synthesis leader reported an operating margin of negative 66%. That's not great, but it was the best in the company's history. Quarterly operating margin was negative 133% just 24 months ago.

On the other hand, the company's cost structure creates some speed limits on the path to profitability. It's going to take at least a few more years.

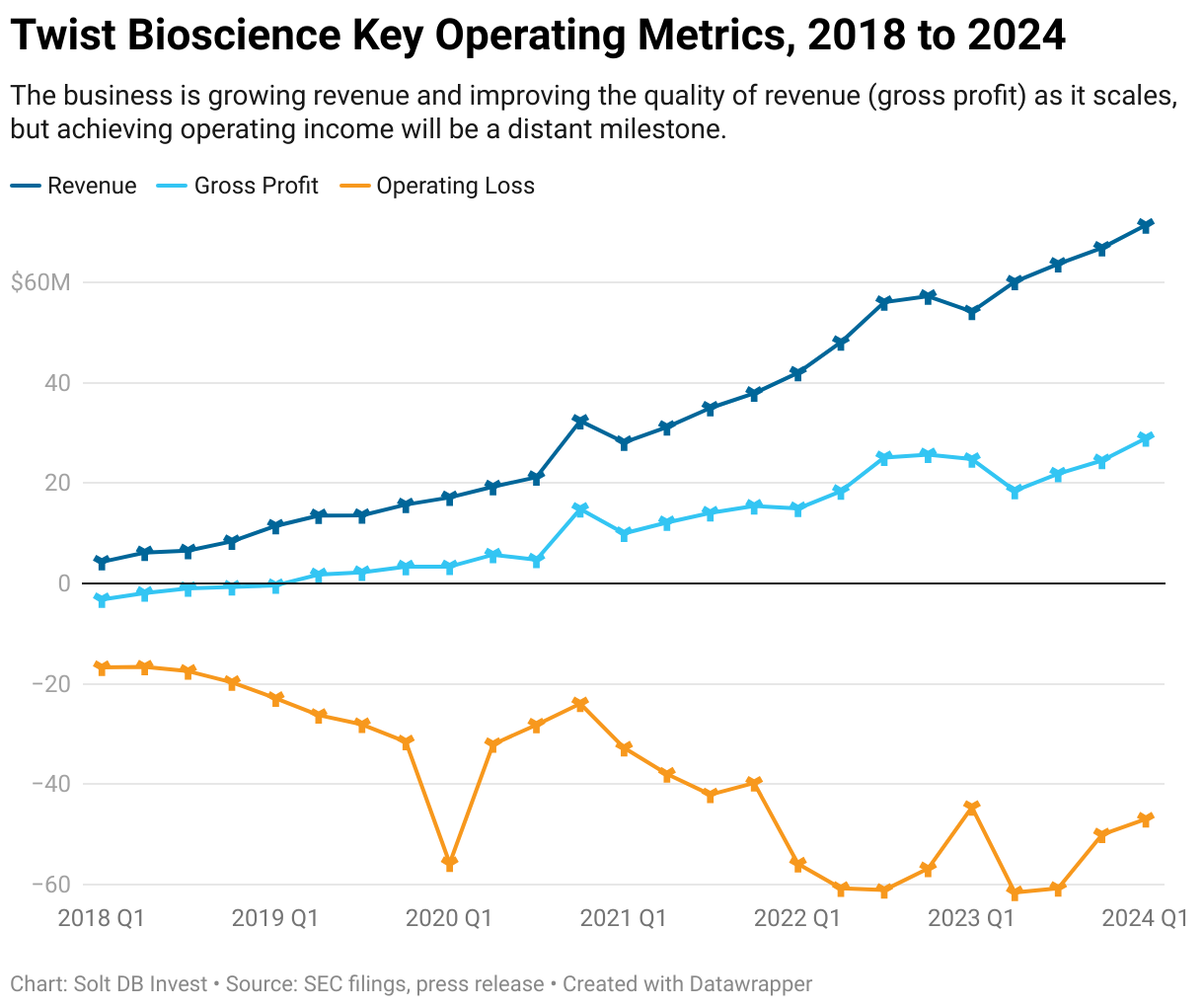

Every business takes the same journey to achieving operating income. Revenue minus the cost of goods sold results in gross profit, gross profit minus operating expenses results in operating income. For Twist Bioscience, it will need to more than double full-year 2024 revenue from $300 million to $600 million, and increase gross margin from 40% to 60%, before it can reliably generate operating income. That's unlikely before fiscal 2027.

The good news for investors is that the business should begin generating cash from operations before achieving the long-awaited milestone for operating income. Investors can use the performance of the new Express Genes offerings in 2024 to gauge the trajectory.

By the Numbers

Twist Bioscience reported record quarterly revenue during the fiscal first-quarter of 2024. Then again, the business is in growth mode, so records will be a routine achievement. The underlying performance metrics are more important than latching onto mostly meaningless records.

Gross margin ascended to 40.5% during the final three months of calendar 2023 and has improved for three consecutive quarters. That's been driven by an impressive improvement in efficiency. The business has held the cost of revenue at roughly $42 million for four consecutive quarters despite growing quarterly revenue from $60.2 million to $71.5 million in that span. As a result, quarterly gross profit jumped from $18.5 million to $28.9 million in that period.

Having an extra $10 million in quarterly gross profit trickle down the income statement is a beautiful thing. Twist Bioscience reported an operating loss of $47 million in the most recent period, compared to an average quarterly operating loss of $59 million in 2022 and $54 million in 2023. That improvement can compound over the course of a fiscal year.

The company hasn't filed its quarterly report (10-Q) as of this writing, so I cannot break down the performance by industry, application, or geographic region on a quarterly basis. These often-overlooked indicators can provide important signals for the business and have meaningful influence on my models.

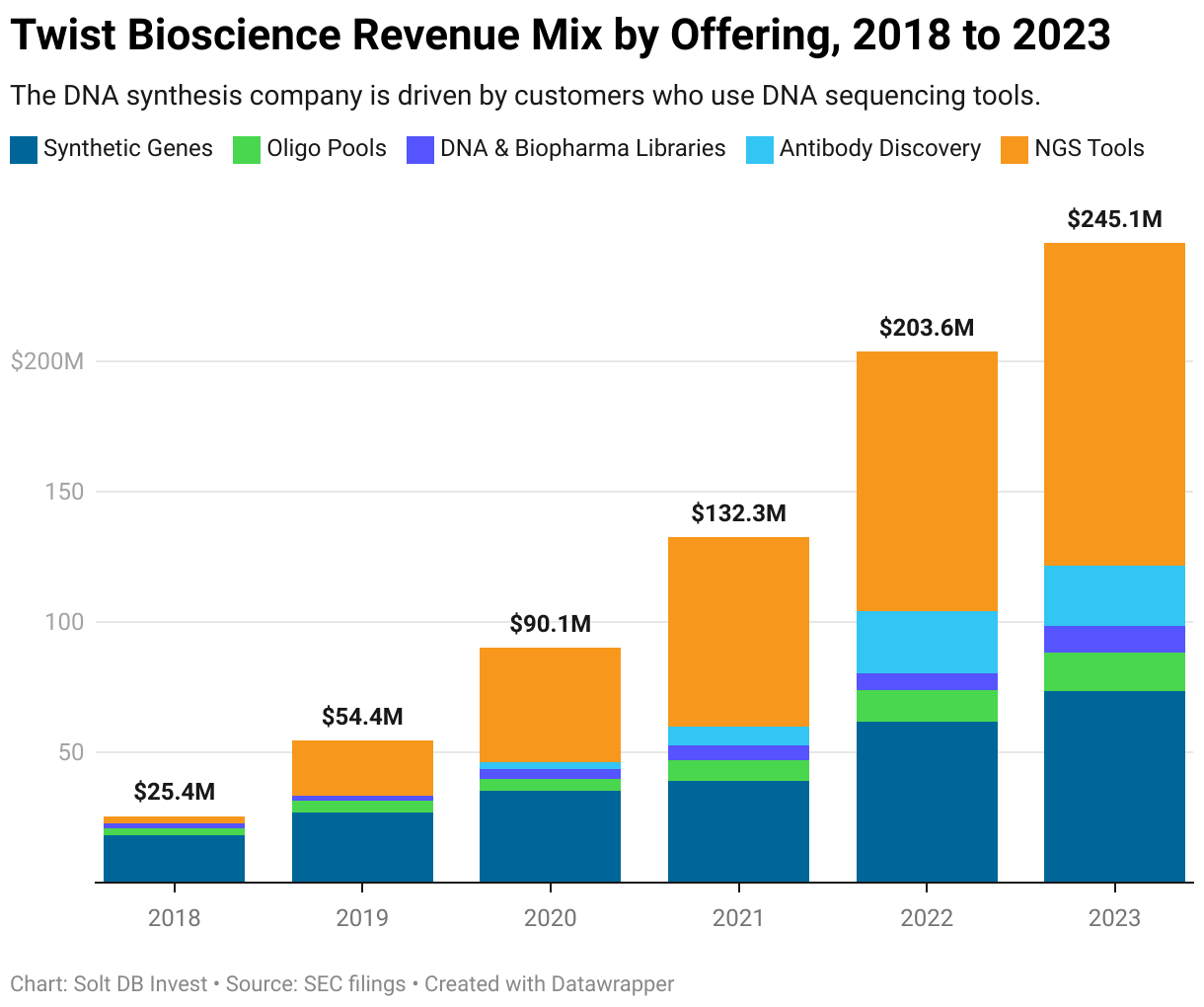

It appears Twist Bioscience is seeing stronger-than expected revenue from its next-generation sequencing (NGS) offerings. The company provides DNA that serves as a reference template for DNA tests, which is what patient samples are compared against to deliver DNA testing results. It's a little ironic. The best product in DNA synthesis (writing genes) relies on customers using DNA sequencing (reading genes).

These customers already represent the largest share of revenue at 52%, but that's a relatively positive trend, as healthcare companies are a more reliable source of revenue than industrial or agricultural biotech customers. This metric will serve as a gauge for the emerging opportunity in liquid biopsy and minimal residual disease (MRD) tools, a market which is expected to grow from $0.3 billion to $2.2 billion by 2027. It's likely contributing to growth in 2024.

Additionally, investors want to see Twist Bioscience maintain or increase its reliance on customers in the Americas. This revenue has the highest margins and highest average selling prices. It also avoids the geopolitical risks of selling to labs in China or the Middle East.

Looking Ahead

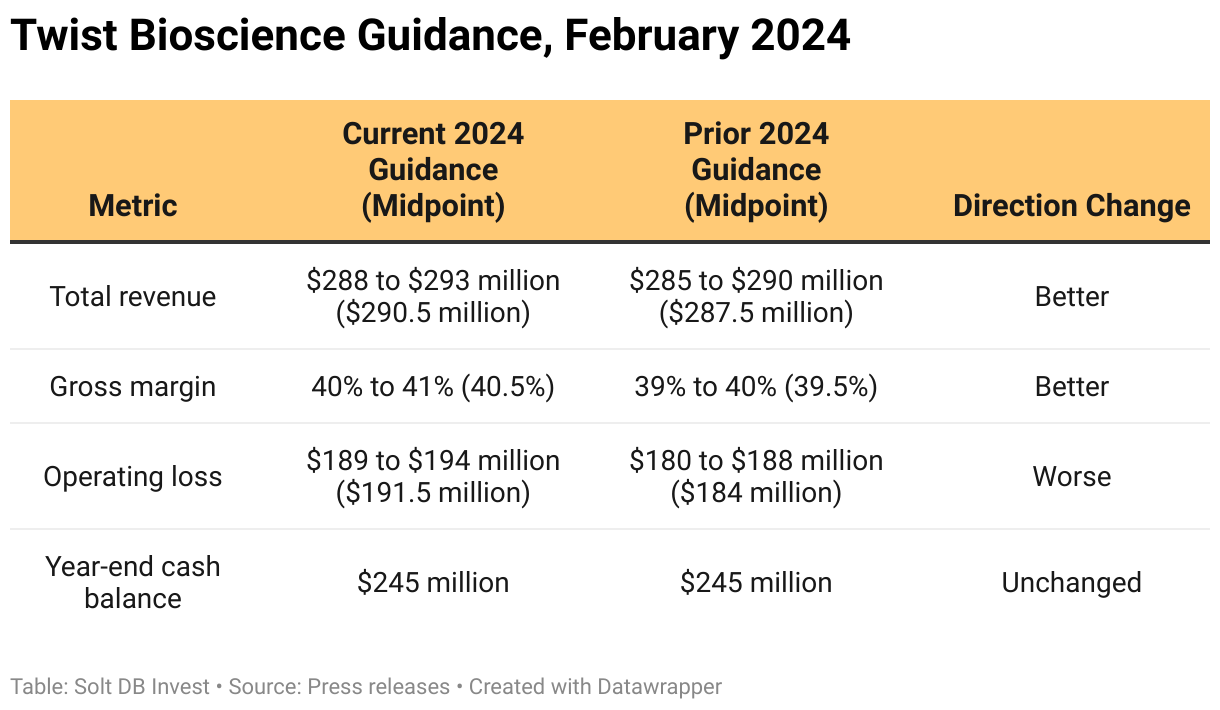

Twist Bioscience increased fiscal full-year 2024 guidance for revenue and gross margin, while increasing expectations for operating loss this year. Management typically underpromises and overdelivers – a great characteristic for investors.

- The business now expects total revenue of $290.5 million for the year, representing year-over-year growth of 19%.

- Gross margin is now expected to be 40.5%, compared to 36.6% in fiscal 2023.

- Operating loss is now expected to be $191.5 million, compared to $217 million in fiscal 2023.

The most important development for fiscal 2024 will be the continued improvement in operating efficiency (higher gross profit and lower operating loss), which will be driven by new Express Genes offerings.

Let's review what the business does.

Twist Bioscience allows customers to design genetic sequences – from a fragment of DNA to a full-length gene – through a web dashboard and then have the custom synthetic DNA shipped to their lab. It takes time to receive the order, synthesize the genetic material, perform quality control, and then ship physical product out to customers. The length and complexity of the genetic material impacts the turnaround time, or the time from order to delivery.

That's always been a headwind for DNA synthesis companies, as it's relatively easy for customers to create genes (called cloning) in their own lab in a few days at most. These potential customers are called DNA makers. They represent a roughly $1.4 billion market opportunity, compared to the current market opportunity (DNA buyers) of just $0.5 billion (note this excludes the NGS market opportunity and primarily includes academic labs and private research labs). But DNA makers have proven difficult to crack.

It makes sense. If you're a cash-strapped academic lab with an army of cheap and free labor called grad students, then the convenience of DNA synthesis platforms generally doesn't outweigh the costs.

Twist Bioscience is hoping Express Genes can begin to change that.

- The Express Clonal offering launched in November 2023 reduces turnaround time from 10 or 11 days down to 5 or 7 days.

- An expansion of the Express Rapid Gene Synthesis offerings at the end of January 2024 could reduce turnaround time for larger genes from 13 days to 8 days.

To be blunt, Express Genes are unlikely to convert DNA makers requiring smaller amounts of DNA. It'll still be faster and lower cost to clone in your own lab, especially since Express Genes have premium pricing compared to the company's previous offerings.

But the company could realistically begin chipping away at the higher end of the DNA maker market, which is more lucrative anyway. Labs could still clone larger and longer amounts of DNA in their own lab, but if the turnaround time drops to 8 days, then maybe the cost can be justified.

Despite the company's focus on the DNA maker market (again, this is mostly academic labs), the launch of Express Genes should make a bigger difference among commercial customers. Drug developers or diagnostic manufacturers can more easily justify the premium pricing of the products, especially if turnaround times are greatly reduced. That can allow teams to move faster or accomplish more in the same amount of time.

Since Express Genes will have higher gross margins, the ability to drive revenue growth and margin expansion from existing customer groups should be the focus of investors. It will be the single-biggest determinant to the trajectory of the business as it exits 2024.

Forecast & Modeling Insights

(Increased and refined.)

All three metrics in my updated model are better than the company's updated fiscal full-year 2024 guidance. The updated 2024 model includes the following:

- Total fiscal full-year 2024 revenue of $304.831 million, up from a previous expectation of $300.496 million.

- Gross margin of 41.2%, up from a previous expectation of 40.5%.

- Operating loss of $187.644 million representing an operating margin of negative 62%.

The modeled fair valuation of the business is $1.719 billion ($28.39 per share), up from a previous model of $1.692 billion ($27.94 per share). Because Twist Bioscience hasn't filed its quarterly report as of this writing, I cannot update the last reported share count. This could slightly decrease the modeled fair valuation.

In the fiscal second-quarter of 2024, I'll provide more granular insights to expectations across the company's business segments (NGS, synthetic biology, and biopharma).

Margin of Safety & Allocation

Twist Bioscience is considered a Growth (Speculative) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close February 2: $36.94 per share

- Modeled Fair Valuation: $28.39 per share

- Allocation Range: Up to 2.5%

Twist Bioscience reported 57.674 million shares outstanding as of November 17, 2023. The modeled fair valuation above assumes 60.557 million shares outstanding, which is equivalent to 5% dilution.

Further Reading

- February 2024 press release announcing fiscal first-quarter 2024 operating results

- February 2024 investor presentation for fiscal first-quarter 2024 operating results

.svg)

-cropped.svg)