.svg)

Business is simple, but not easy. Get customers, make them happy, and ensure as many of them as possible keep coming back.

It's all those fickle humans – customers, vendors, employees, and that micromanaging asshole who just became your boss – that make business so difficult.

Twist Bioscience is doing an excellent job navigating financial markets, an increasingly competitive landscape, and making customers happy. The business is becoming more efficient (more revenue and fewer costs) and more diverse (more product offerings in disparate applications and industries). It's well positioned from a geopolitical perspective, too, with over 60% of revenue generated from the United States.

If investors wanted to nitpick, then the valuation is an easy place to start. Investors are forced to pay for future growth stretching years into the future, which introduces a valuation premium that can quickly unwind.

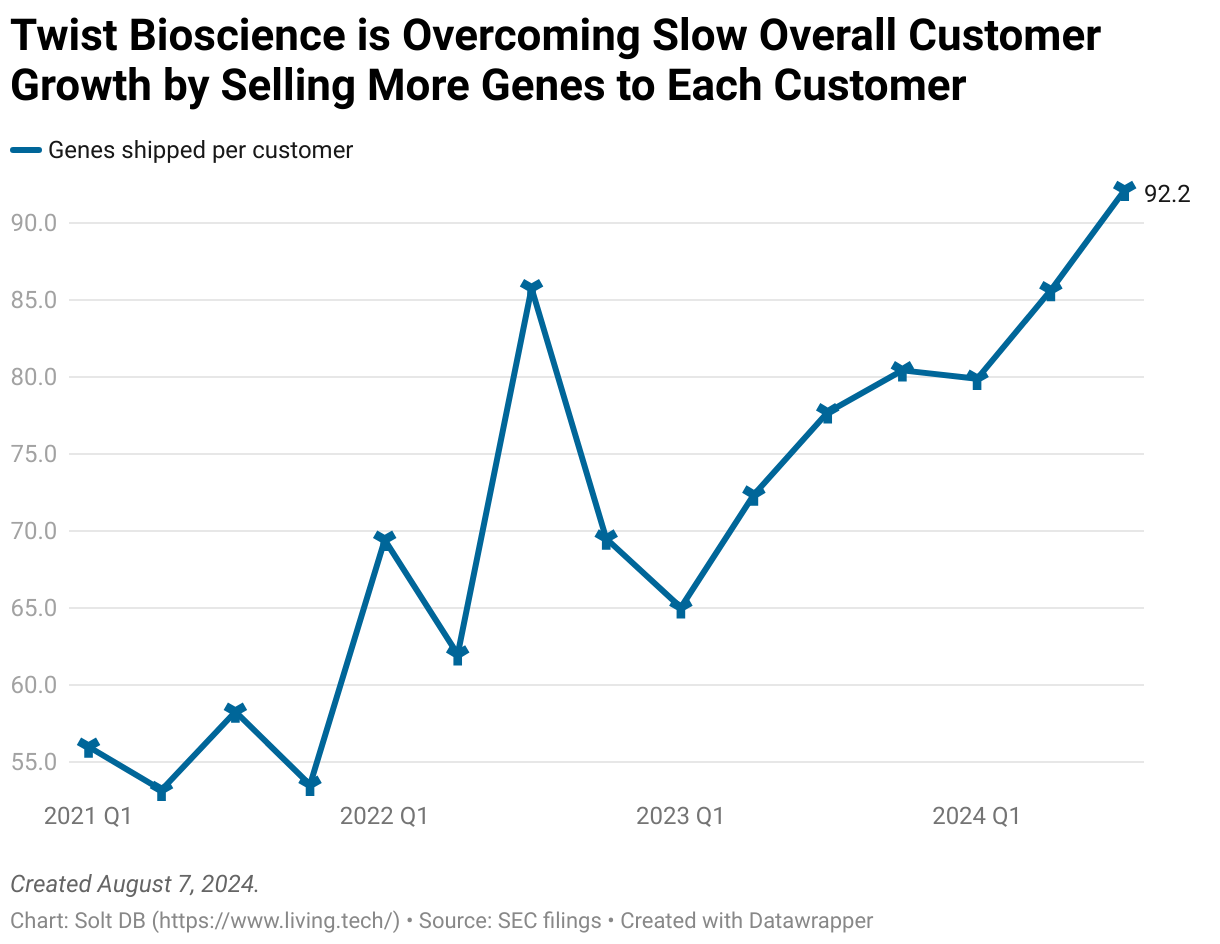

Dig a little deeper and the DNA synthesis pioneer is struggling to grow its customer base. That makes me a little uneasy given the competitive dynamics, especially considering DNA synthesis can become significantly cheaper – and many companies are trying. How many customers would flee if a competitor offered similar quality at lower prices?

For now, at least, shipment data suggest existing customers are becoming increasingly comfortable leveraging the platform. Twist Bioscience shipped 92 genes per customer during fiscal Q3 2024, up from an average of 55 throughout fiscal 2021.

That's just one of a handful of favorable long-term trends, which bodes well for the business heading into fiscal 2025.

By the Numbers

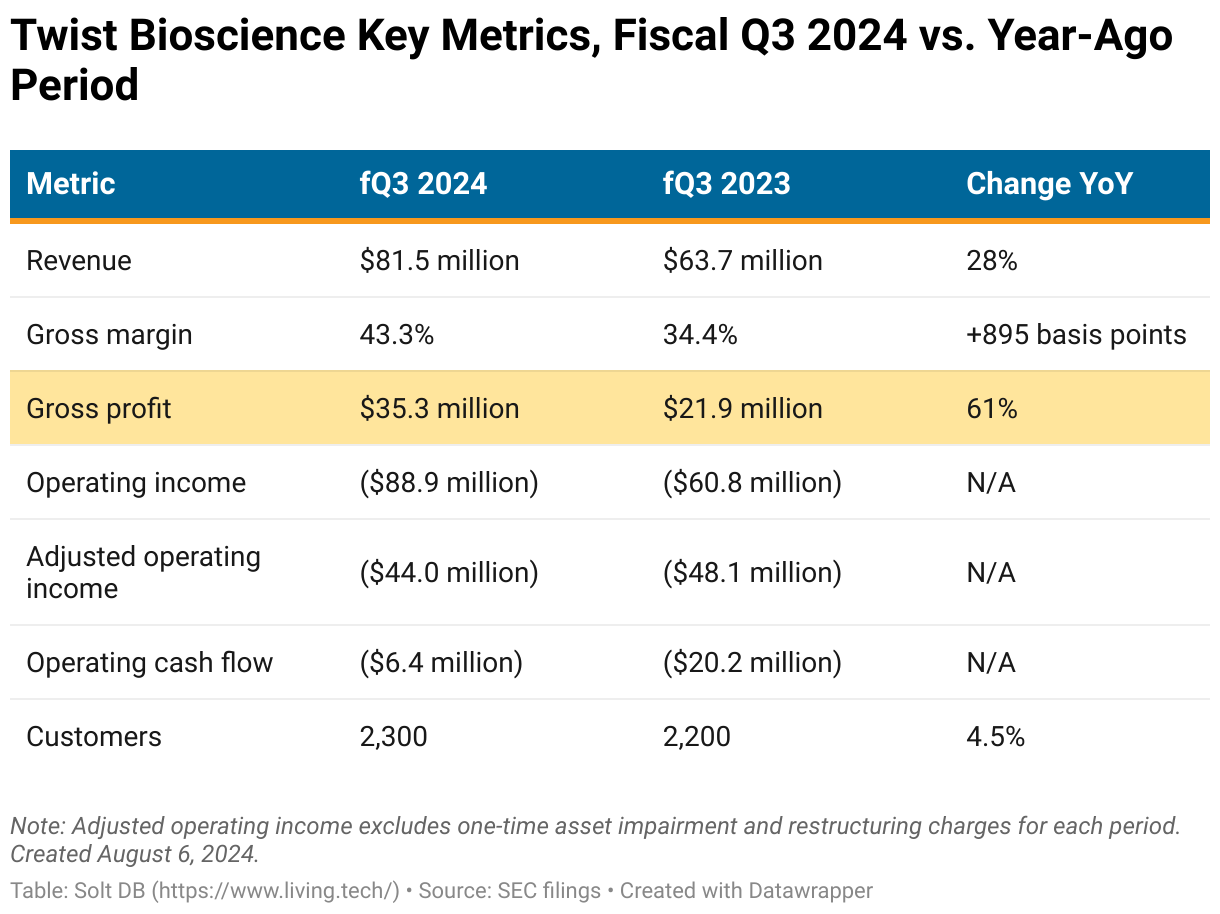

Twist Bioscience has become steadily more efficient since the business hit bottom in the fiscal second-quarter of 2023. Gross margin has increased from 30.8% to 43.3%. Operating margin has improved from negative 75.5% to negative 54.0% (adjusted to remove one-time charges in each quarter). The amount of cash used in operations has decreased from $46.9 million to just $6.4 million.

More revenue with better margins is almost always a winning formula.

The improvement in gross margin combined with solid revenue growth drove a 61% increase in gross profit (how much revenue a company keeps). Gross profit trickles down the income statement to self-fund R&D, sales, marketing, and so on. Any gaps must be funded by cash on hand, debt, or other people's money.

Twist Bioscience reports a customer base of about 3,450 accounts. While not every account places an order every quarter, the stagnant trend in customer growth adds a little wrinkle for investors. This doesn't appear to be a headwind right now, but it's the type of risk that can unravel an investing thesis relatively quickly. Keep a close eye on this metric and management's plans to expand the customer base over time.

How the heck has the company grown so quickly without adding more customers? The average account is ordering more genes than before. That's likely driven by a mix of factors, such as larger accounts becoming increasingly comfortable using the platform. For example, the number of genes per shipment hasn't increased much since fiscal Q1 2023. Customers simply appear to be ordering more frequently.

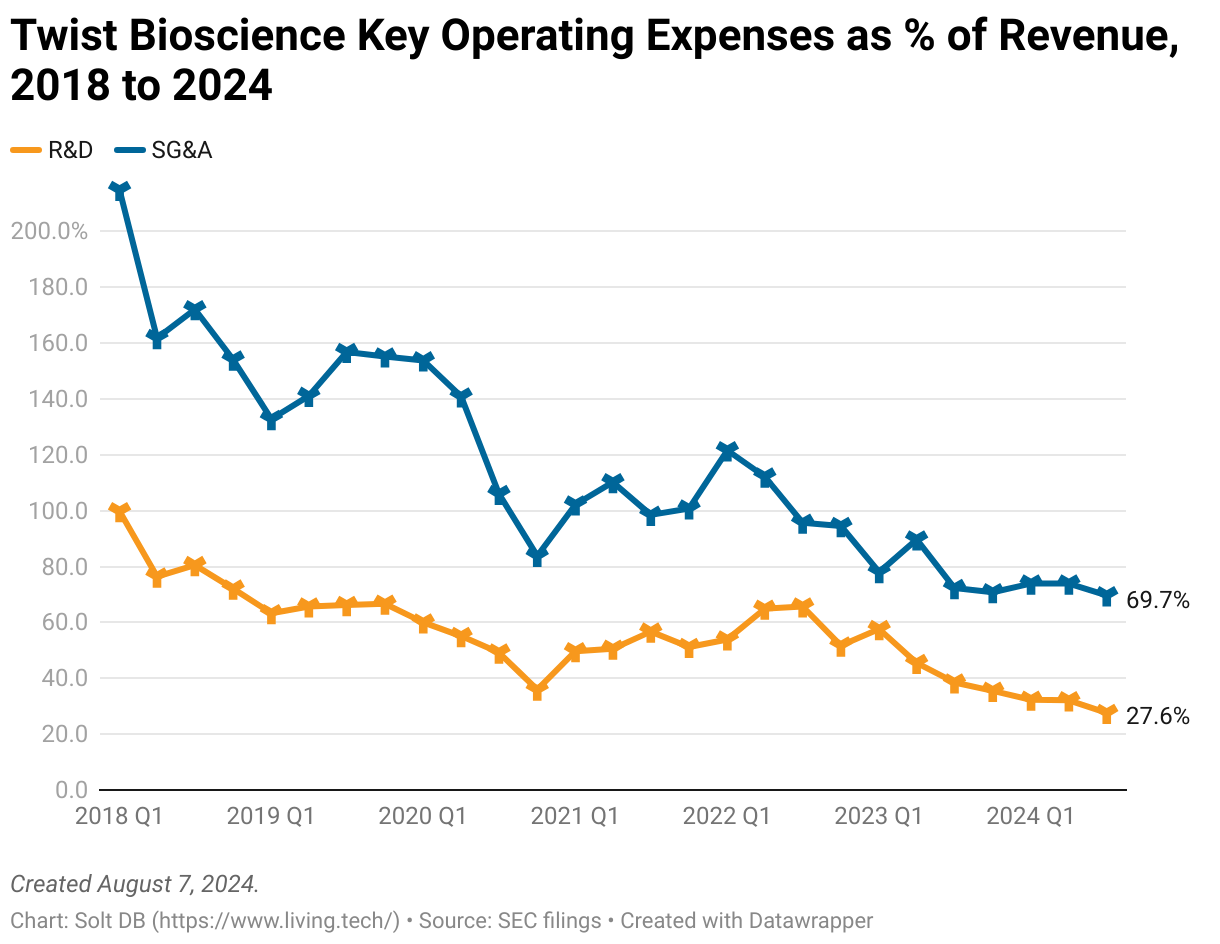

Happy customers are a good thing. That's especially true when operating expenses are being kept in check.

As a percentage of revenue, R&D expenses fell below 30% and selling, general, and administrative (SG&A) expenses fell below 70% for the first time ever. The 25% layoffs from 2023 certainly help, but the same favorable trend extends as far back as public financial metrics go.

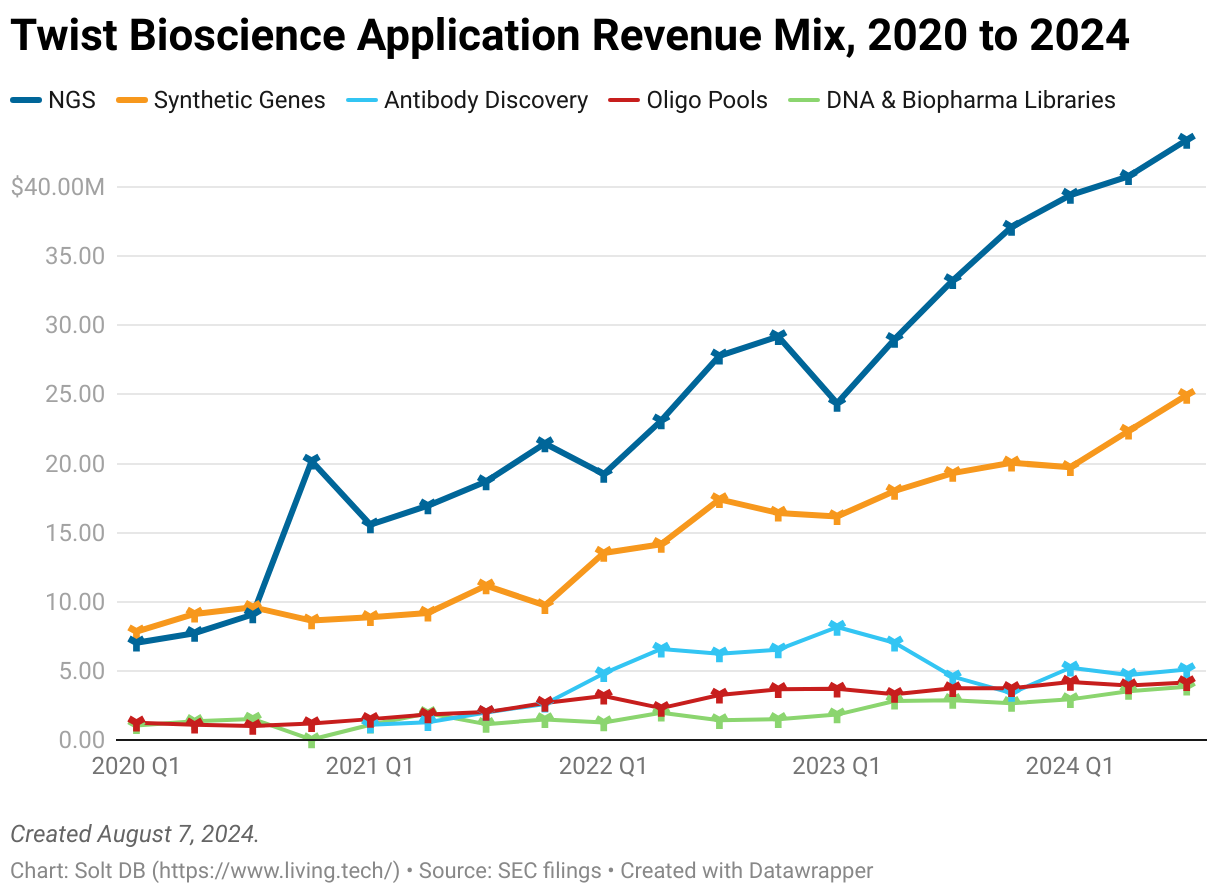

The business continues to lean heavily on the same familiar applications: NGS tools (53% of total revenue) and synthetic genes (31%). Twist Bioscience's recent foray into antibody discovery has stalled with revenue now back to early 2022 levels.

In fact, the reason I had to adjust operating income and operating margin above is because there was a one-time $45 million impairment during the most recent quarter. The company identified an "impairment indicator" related to a certain asset group in its antibody discovery portfolio, according to SEC filings.

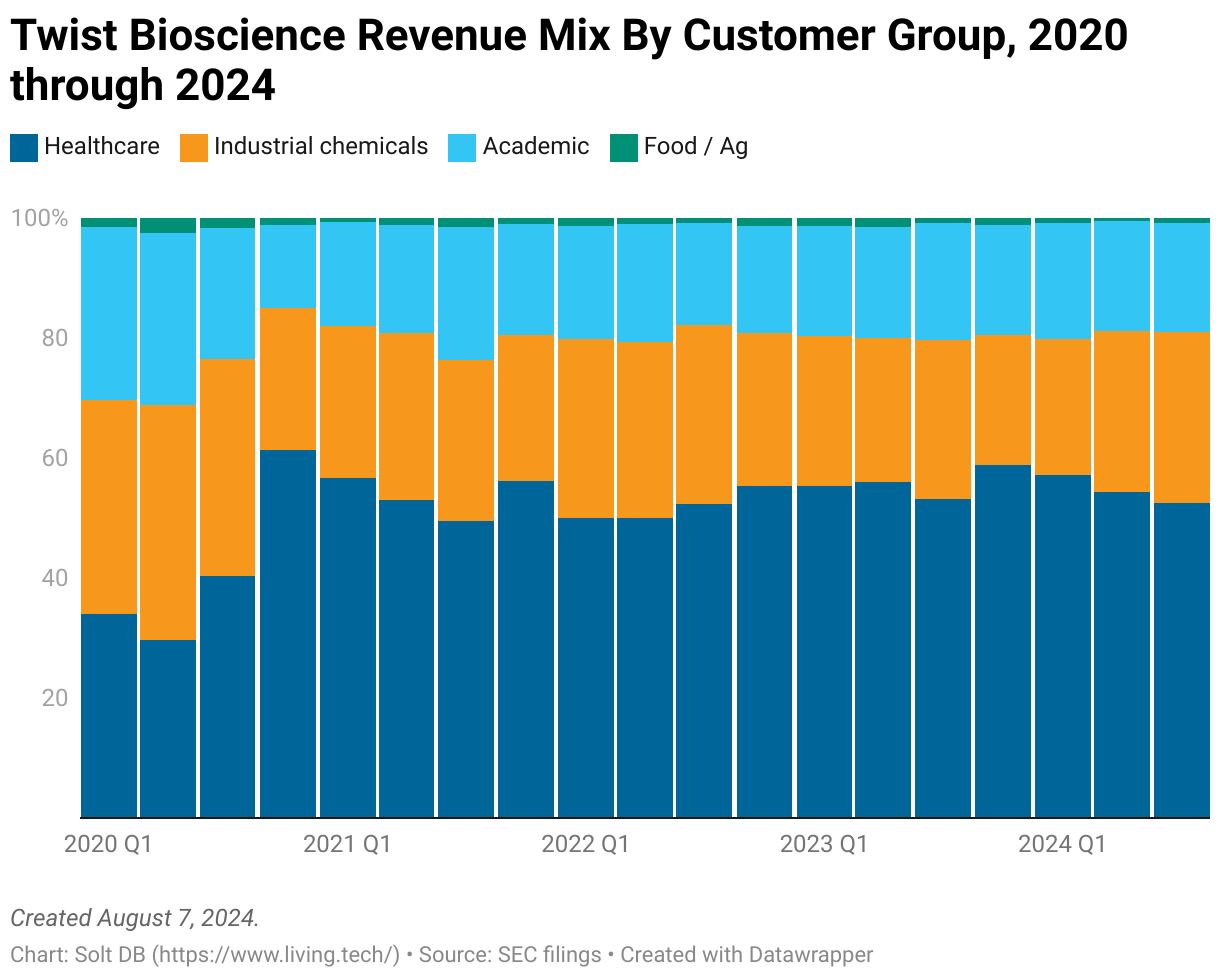

Whereas the bulk of revenue is dependent on only two applications, it's more diverse when viewed by customer group. Twist Bioscience is achieving similar rates of revenue growth across healthcare, industrial chemicals, and academic accounts.

This can be visualized by viewing the relative stability of revenue contributions from each customer group.

Forecast & Modeling Insights

(Introducing 2025 model.)

The estimated fair value and margin of safety calculation is now based on my 2025 model.

I increased my fiscal full-year 2024 model after fiscal Q2 2024 operating results were announced in May 2024. To recap fiscal Q3 2024 performance:

- Modeled revenue of $82.5 million vs. $81.5 million actual (guidance of $77 million and Wall Street consensus of $78 million)

- Modeled gross margin of 43.6% vs. 43.3% actual (guidance of 42.5%)

- Modeled operating income of negative $43.0 million vs. negative $44 million actual (no guidance)

For transparency, here's how my fiscal Q4 2024 model compares to Twist Bioscience's guidance and Wall Street expectations:

- Modeled revenue of $86.036 million vs. guidance of $82.5 million (Wall Street consensus of $373.170 million)

- Modeled gross margin of 44.2% vs. guidance of 44.0%

- Modeled operating income of negative $39.964 million

My fiscal 2024 model expects full-year revenue of $314.3 million vs. guidance of $310.5 million.

I typically introduce new forward-looking models after fiscal third quarter results are reported. That's right now for Twist Bioscience! This may look grossly optimistic compared to the company's initial fiscal full-year 2025 guidance expected to be issued in November 2024, but co-founder and CEO Emily Leproust has "underpromise, overdeliver" tattooed on her forehead.

- Modeled revenue of $400.733 million (Wall Street consensus of $81.89 million)

- Modeled gross margin of 46.3%

- Modeled operating income of negative $143.268 million, resulting in an operating margin of negative 36%

At the current trajectory, the business is on pace to achieve profitable operations (based on operating income) in fiscal 2027. Although it has enough cash on hand to eek it out, I would expect a capital raise or asset monetization in that time.

Margin of Safety & Allocation

Twist Bioscience is considered a Growth (Speculative) position. The current modeled fair valuation for the company based on my 2024 model is below:

- Market close August 6: $46.24 per share

- Modeled Fair Valuation: $36.74 per share

- Allocation Range: Up to 2.5%

Twist Bioscience reported 58.586 million shares outstanding as of July 31, 2024. The modeled fair valuation above assumes 61.515 million shares outstanding, which is equivalent to 5% dilution through the end of the fiscal year.

Further Reading

- August 2024 press release announcing Q1 2024 operating results

- August 2024 regulatory filing (10-Q) detailing Q1 2024 operating results

- May 2024 research note analyzing fiscal Q2 2024 operating results

-cropped.svg)