.svg)

Biosimulation promises to increase the efficiency of drug development – the primary challenge facing the global industry as it wrestles with ballooning R&D expenses. It's already delivered on that promise in many ways.

By combining experimental and computational datasets to predict how molecules interact with human biology, biosimulation gives drug developers the power to better understand potential side effects for new chemistries, optimize dosing for novel molecules, design optimized clinical studies, earn more favorable labels from regulators, and in a growing number of cases avoid additional clinical trials altogether. The return on investment is off the charts if used correctly.

It should therefore come as no surprise that 90% of new drug approvals in the United States since 2014 have used Certara's platform.

What might be more surprising is that, despite all that, Certara expects to grow by only single digits for the second consecutive year in 2024.

Although the business is no slouch – it expects to generate full-year 2024 revenue of at least $380 million and has generated positive operating cash flow for at least 19 consecutive quarters – the biosimulation industry suffers from the same familiar headwinds heading into 2025. Fragmentation, regulatory guidelines that don't require biosimulation, and cautious spending from large pharma companies.

By the Numbers

Certara can only do so much to accelerate the shift toward a model-informed future, but it's making an admirable effort.

- To address fragmentation (many small companies littered across the globe), Certara continues to acquire competitors and consolidate the field. The 20th acquisition (Applied BioMath) and 21st acquisition (Chemaxon) were for more mature businesses that will contribute revenue and earnings immediately.

- To nudge regulators to expand guidelines and hopefully require biosimulation, Certara is a key player in the Model-Informed Drug Development (MIDD) Program of the U.S. Food and Drug Administration (FDA). The program replaces a prior pilot and runs through 2027. The goal is to help drug developers and regulators become more familiar with using biosimulation tools in new applications, which often leads to formal regulatory guidances for specific steps or therapeutic modalities. As Congress becomes more concerned with the inefficiency of drug development, potential legislation that requires biosimulation would be a huge boost for the business.

- To address cautious spending from large pharma companies, well, Certara simply must wait it out.

While inaction is expensive, so is action.

The late-2023 acquisition of Applied BioMath added the leading biosimulation platform for biologics (such as antibody drugs). The April 2024 launch of Certara Cloud brought all the company's software platforms under one roof for the first time. Multiple product upgrades to integrate new artificial intelligence features, such as adding generative AI capabilities to the company's regulatory writing software CoAuthor, intended to maintain competitive positioning.

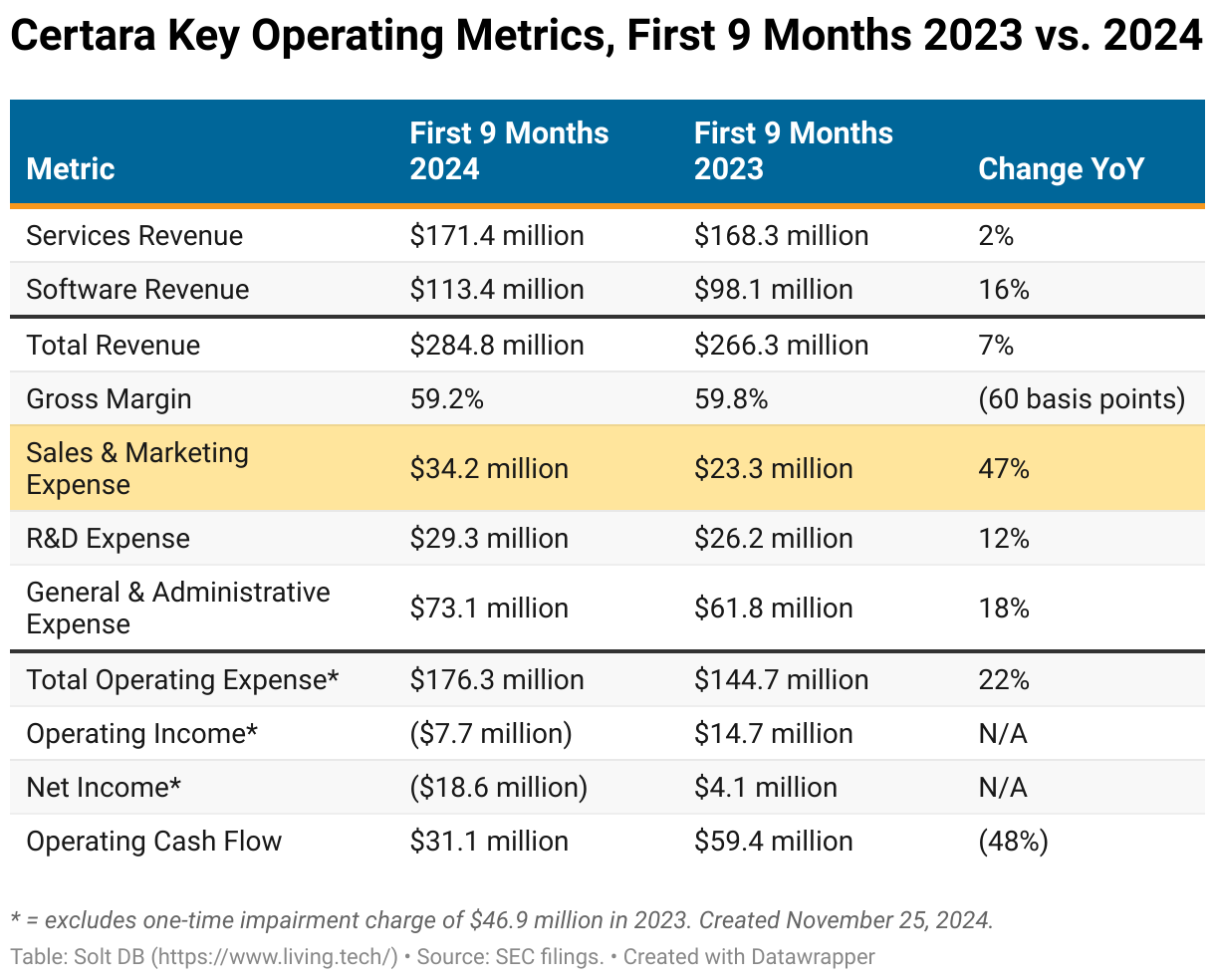

The investments kept software revenue growth humming along, but also resulted in a significant increase in operating expenses, especially sales and marketing expenses. Sluggish spending from customers meant the surge in expenses easily outpaced revenue, reversing the company's operating profit and net income in the first nine months of 2024 compared to the year-ago period.

The results aren't ideal, but the sky isn't falling for Certara.

Notice that operating cash flow remains strong. The business only had a net cash reduction of $40 million in the last 12 months, which includes the acquisition of Applied BioMath and the investments described above.

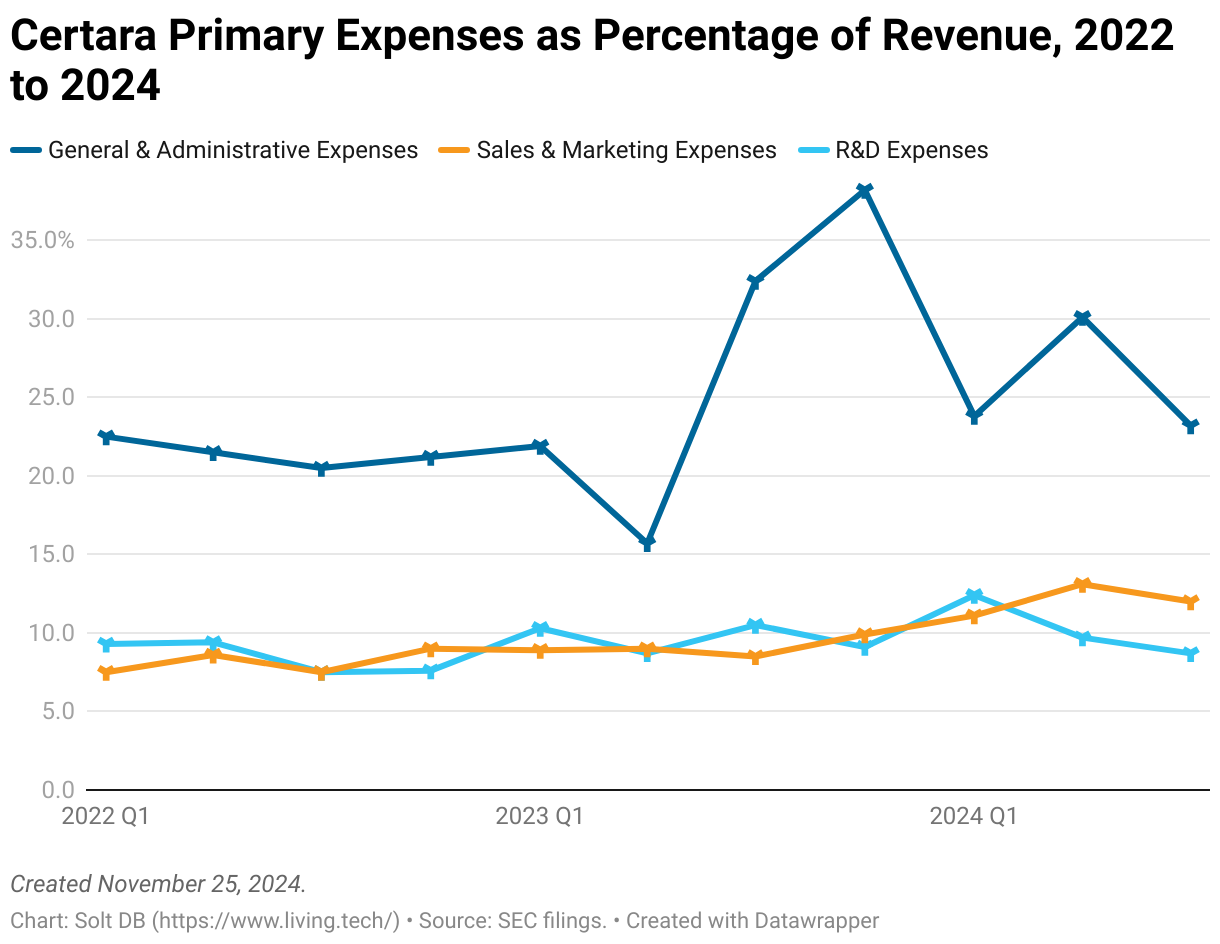

Investors should still keep an eye on operating expenses as a percentage of revenue.

Until total revenue growth returns to the historical 15% to 18% range, sales and marketing expense is likely to hover near 10% of revenue. That's a few ticks higher than the historical average. General and administrative expenses have surged, too, but most of the increase in the visualization below was driven by non-cash accounting expenses. It looks much worse in the graphic below.

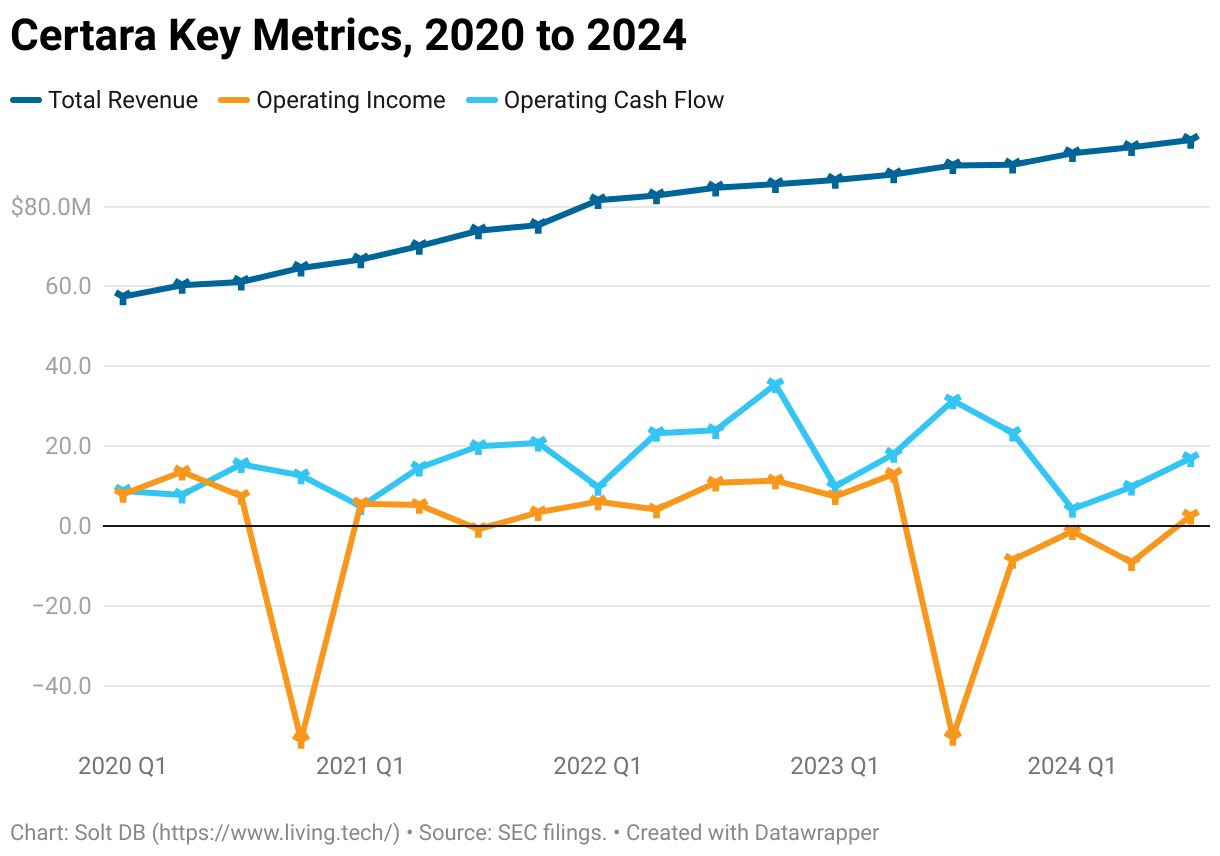

Zooming out to view the long-term trend of key operating metrics shows management has things under control.

It makes sense to invest in growth, especially if Certara can self-fund the investments. Doubly so if it can gobble up top competitors who are falling on hard times. Although operating metrics might take a temporary hit while customers remain cautious with spending, making strategic investments today will allow the business to launch itself into the industry's inevitable recovery.

In fact, the groundwork being laid today suggests the business might be able to top its historical growth rate during the recovery.

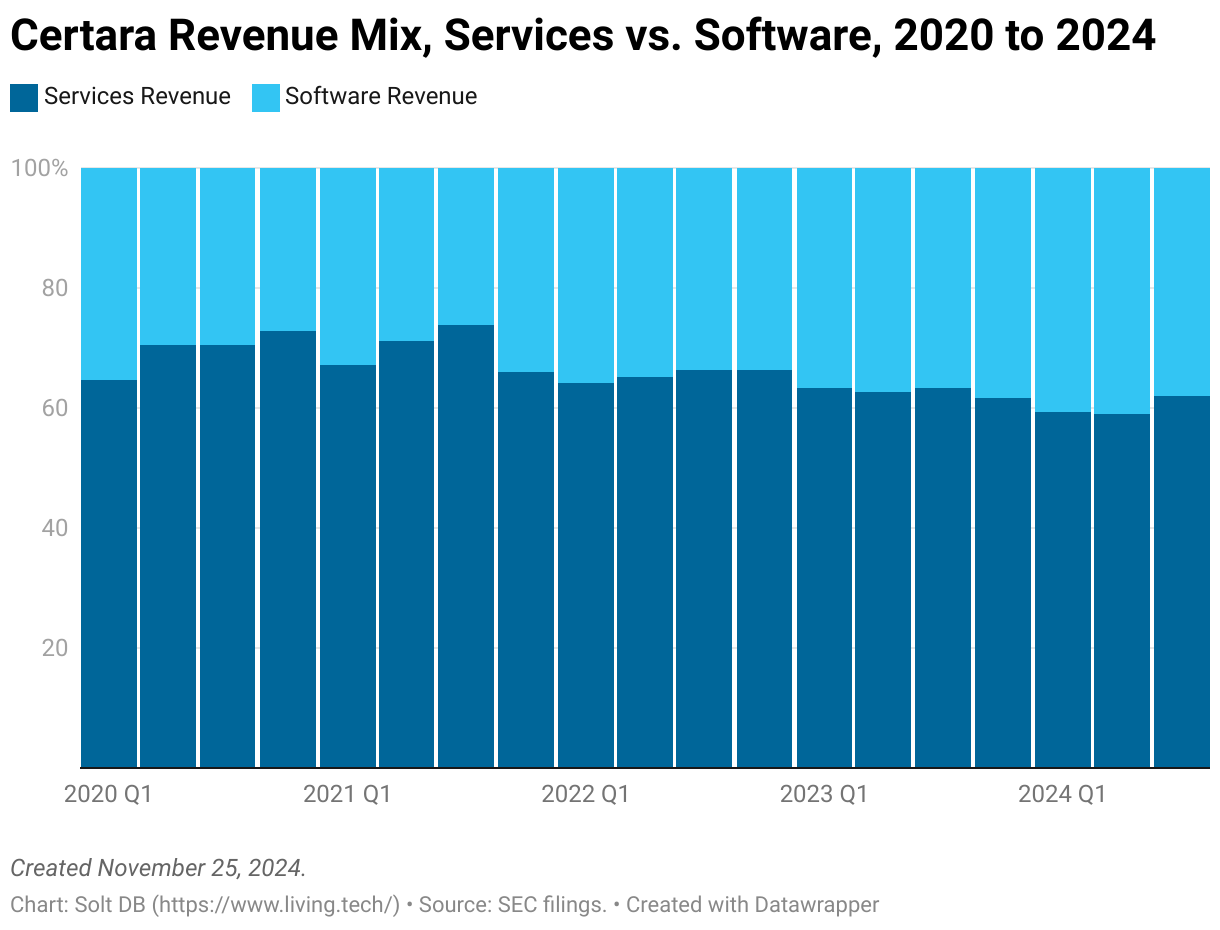

Wall Street seems somewhat conflicted about the company's large reliance on services, rather than software. Services have lower gross margins and require more overhead, which lowers operating margins too. But the "just focus on software" argument is much too simplistic.

Certara is careful to define its largest segment as "software-enabled services." That's because many customers aren't equipped to utilize biosimulation software without help. These may include smaller companies with limited resources, or even the largest drug developers when exploring a new therapeutic modality.

It's also important to remember drug developers spend hundreds of millions of dollars developing a single drug candidate. Services are seen as insurance for their massive investments, not an added cost.

That said, although services will remain a large part of the business indefinitely, Certara is keen to increase contributions from its higher-margin software segment. After all, the biosimulation total addressable market is evenly split between software and services at $2 billion apiece.

The recent acquisition of Chemaxon (closed October 2024) is expected to add roughly $21.6 million in software revenue in 2025. That should nudge the company's software segment to at least 43% of total revenue, up from less than 30% in 2020.

Forecast & Modeling Insights

(Introducing 2025 model.)

Will the biotech winter turn into spring in 2025? I'm not sure about that, but I think investors can expect Certara's services segment to begin thawing at the very least.

When coupled with the second-consecutive year of contributions from a software acquisition (Applied BioMath in 2024, Chemaxon in 2025), Certara can achieve revenue growth of 9.4% compared to 2024. That's far below the historical rate of 15% to 18%, but better than the 5.6% in 2023 and 7.9% in 2024.

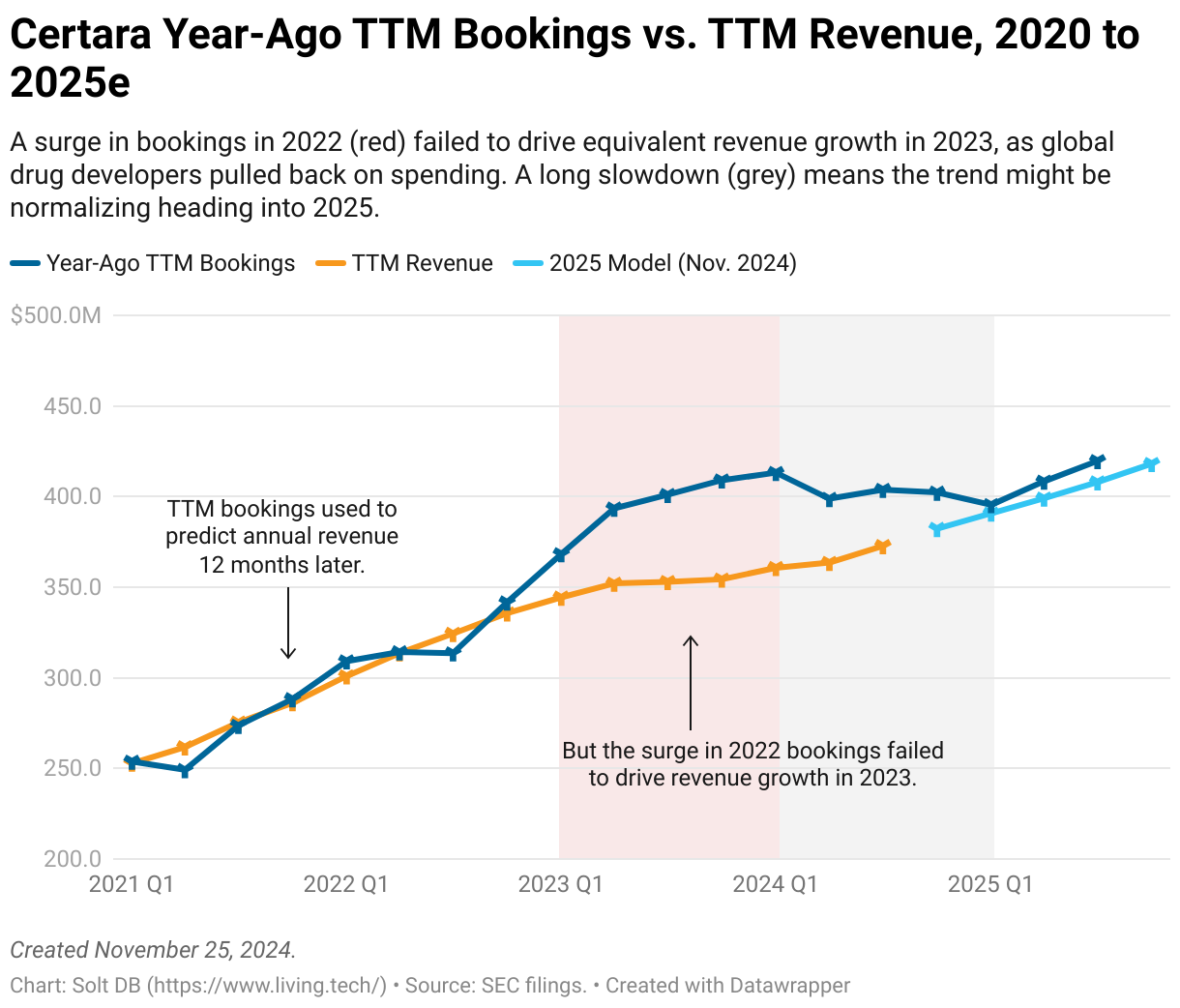

The key here is to understand the relationship between bookings and revenue. Or more accurately, year-ago trailing twelve month (TTM) bookings and TTM revenue.

Certara records bookings for revenue that's reasonable to be achieved in the next 12 months. It's generally predictive of revenue for the next year because customers must sign contracts for software and services. Makes sense.

Except that relationship broke down during the biotech winter. Bookings recorded in 2022 were still reflecting the pandemic boom, not the nails-on-a-chalkboard reality right around the corner. When capital markets turned more viscous, so too, did the willingness of customers to part with their cash.

As a result, the surge in bookings recorded in 2022 failed to drive an equivalent surge in revenue in 2023. It stung more because bookings growth in 2022 was already well above the historical trend.

The good news is that bookings didn't grow at all in 2023. In fact, they declined slightly. That reflected cautious customer spending. Makes sense.

The better news is that pain has already been absorbed by the business and shareholders. Revenue grew in 2024, which allowed TTM revenue to "catch up" to the TTM bookings from the year-ago period.

In other words, bookings appear likely to once again be predictive of revenue in 2025.

There's still some statistical fog clouding the 2025 model of Certara, but I'm confident enough to release this new model. Remember, the goal of modeling is to provide an objective answer to the question, "what's a fair price to pay for this business?"

- Full-year 2025 revenue of $418.144 million, up 9.4% from 2024. Services revenue increases roughly 3% to $234.182 million. Software revenue grows 7.8% from existing business, plus an estimated $21.6 million boost from Chemaxon, to $183.962 million total.

- Revenue mix settles near 56.0% for services and 44.0% for software. That compares to a 59.5% / 40.5% split in 2024 and 71.4% / 28.6% split in 2018 (the oldest data available).

- Adjusted net income of $84.5 million, up 19.2% from $70.9 million in 2024

- Diluted earnings per share (EPS) of $0.52, up from $0.44 in 2024

Margin of Safety & Allocation

Certara is considered an Anchor position. The current modeled fair valuation for the company based on my 2025 model is below:

- Market close November 27: $11.27 per share

- Modeled Fair Valuation: $13.13 per share ($12.63 per share previously)

- Allocation Range: Up to 5%

Certara reported 160.975 million shares outstanding as of November 1, 2024. The modeled fair valuation above assumes 162.585 million shares outstanding, which is equivalent to 1% dilution.

Further Reading

- November 2024 press release announcing Q3 2024 operating results

- November 2024 regulatory filing (10-Q) detailing Q3 2024 operating results

- September 2024 press release describing an example of using biosimulation to optimize dosing for a novel trispecific antibody before it was tested in humans

- June 2024 website update from the U.S. Food and Drug Administration detailing the Model-Informed Drug Development (MIDD) Program

- December 2023 research note analyzing the acquisition of Applied BioMath

-cropped.svg)