.svg)

Certara might be the most complete business in the coverage ecosystem, but it may not offer great returns in the year ahead. Then again, keeping your head above water might be enough to outperform the market in 2025 and 2026.

Management saw no signs through February 2025 that customers are becoming less cautious. Although negative impacts from the Inflation Reduction Act (IRA) and a looming patent cliff suggest drug developers will need to increase biosimulation spending by 2026 at the latest, guidance for the year ahead expects another pedestrian performance for the business.

That doesn't necessarily mean investors should turn their attention elsewhere.

The biosimulation leader is making significant investments in its platform, including developing in-house tools, upgrading existing offerings, and augmenting capabilities with strategic acquisitions. Integrating the distinct parts of the technology platform will be a key focus again in 2025 – and the stakes are even higher now.

Certara's recent acquisition of Chemaxon will give customers access to leading AI drug discovery tools and services. That's not too noteworthy given the field's recent explosion. But integration is key. If every drug developer had access to bespoke predictive modeling tools to de-risk lead optimization in drug discovery, and could easily port data over to clinical biosimulation solutions on the same platform as a molecule advances, then that makes using the platform a competitive necessity.

Only Certara would have such a platform.

By the numbers

Cash is king in biotech right now. Certara is content generating consistent cash flow and leveraging it for internal projects and strategic software acquisitions. Although maximizing profits remains a distant concern, management's efforts to maximize software in the revenue mix will build significant operating leverage potential.

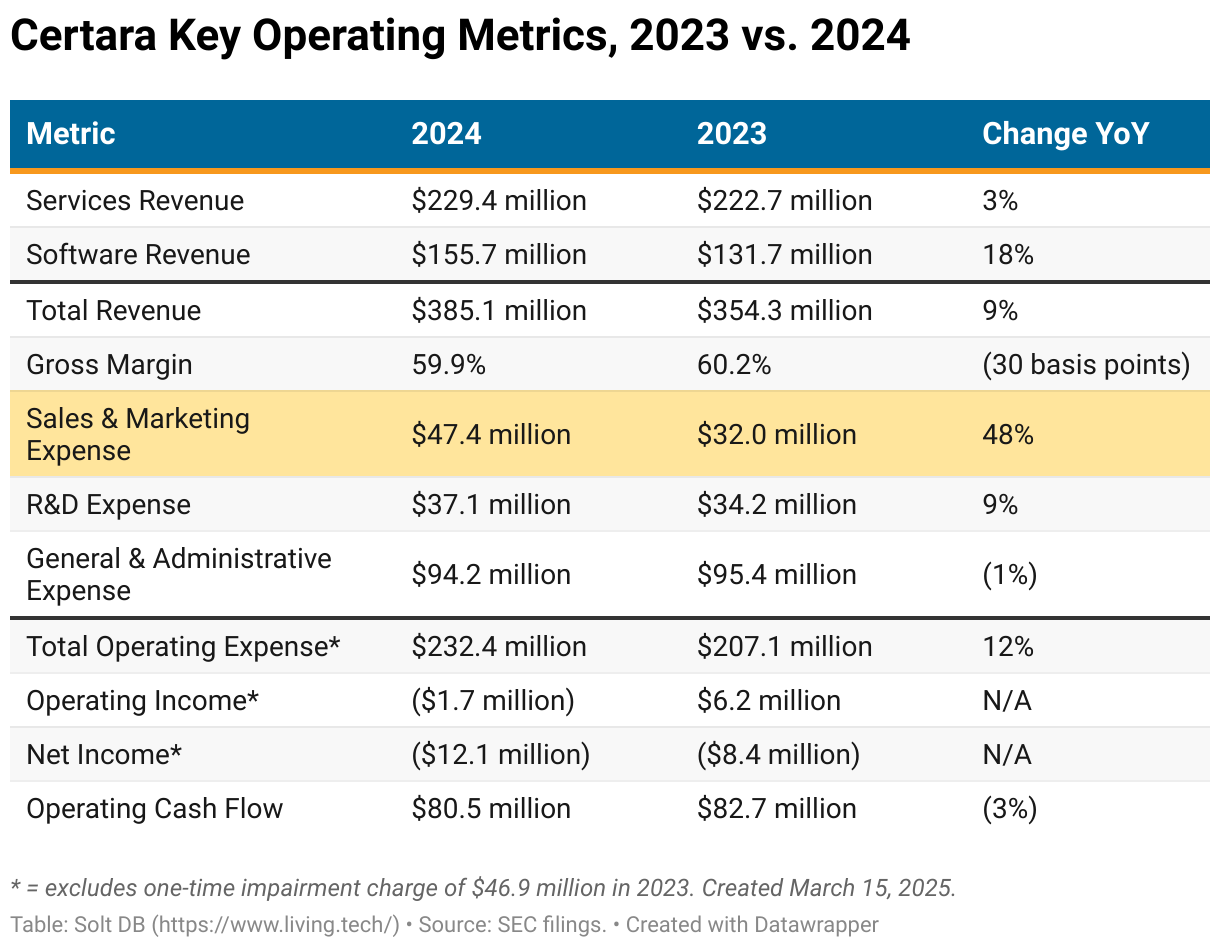

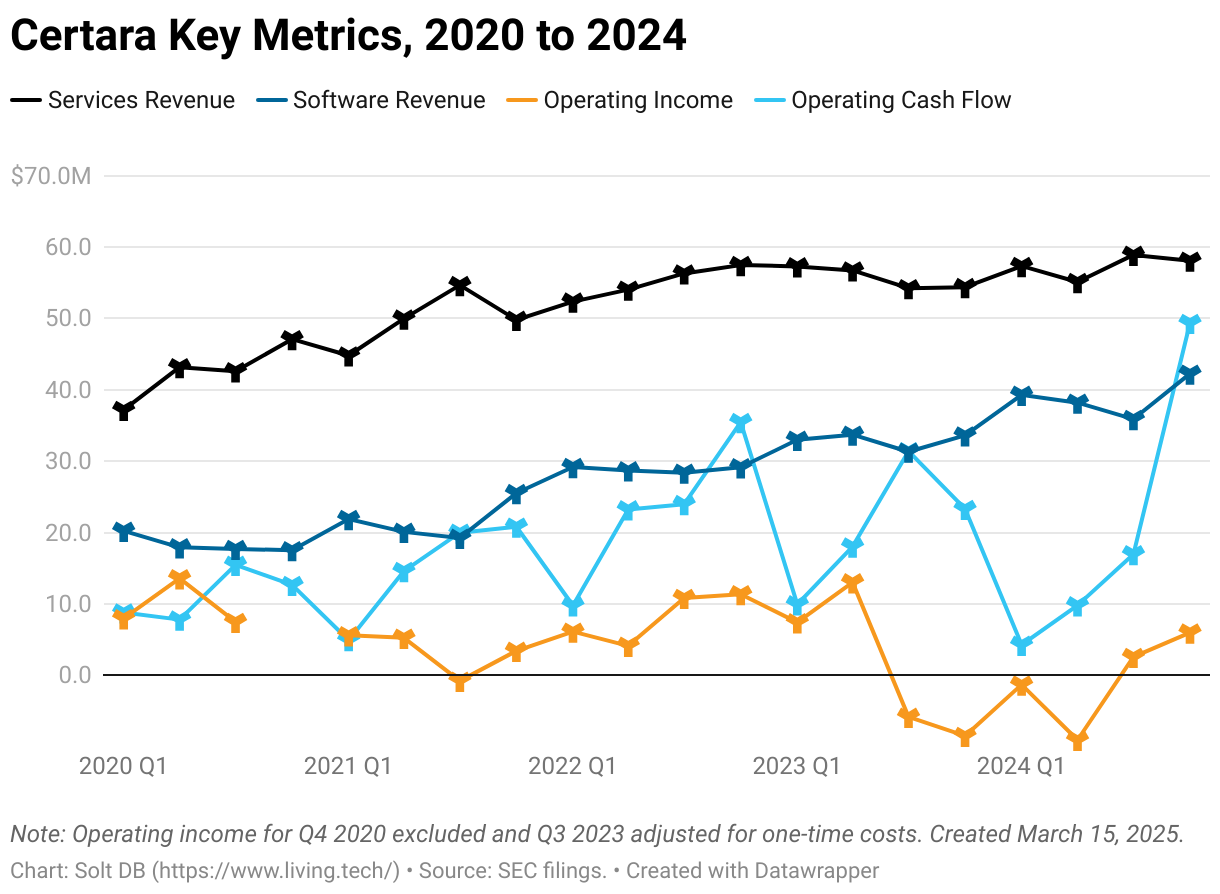

Fourth-quarter 2024 Software revenue jumped 26% from the prior year, lifted by contributions from Chemaxon. The segment eclipsed $40 million in quarterly revenue and represented 42.1% of the overall revenue mix, both firsts for the business. Services revenue grew 7% in the same span. Surprisingly, that included a positive contribution from the Regulatory Services unit, which still saw revenue decline by 10% on the full year.

Acquisitions made significant contributions to growth, but the underlying business remains strong. For the full year, Software revenue grew 18% (organic 10%, acquisitions 8%) and Services revenue grew 3% (organic negative 3%, acquisitions 6%).

Investors shouldn't be too focused on operating income and net income during this phase of the company's growth. The business operates near breakeven, balancing growth with growth investments, and reported losses primarily stem from non-cash charges and adjustments.

Certara has generated operating cash flow for at least 20 consecutive quarters (the oldest public data available). It's probably one of the healthiest businesses selling artificial intelligence solutions to the biopharma sector. Then again, the company's offerings existed before everything was rebranded as "AI."

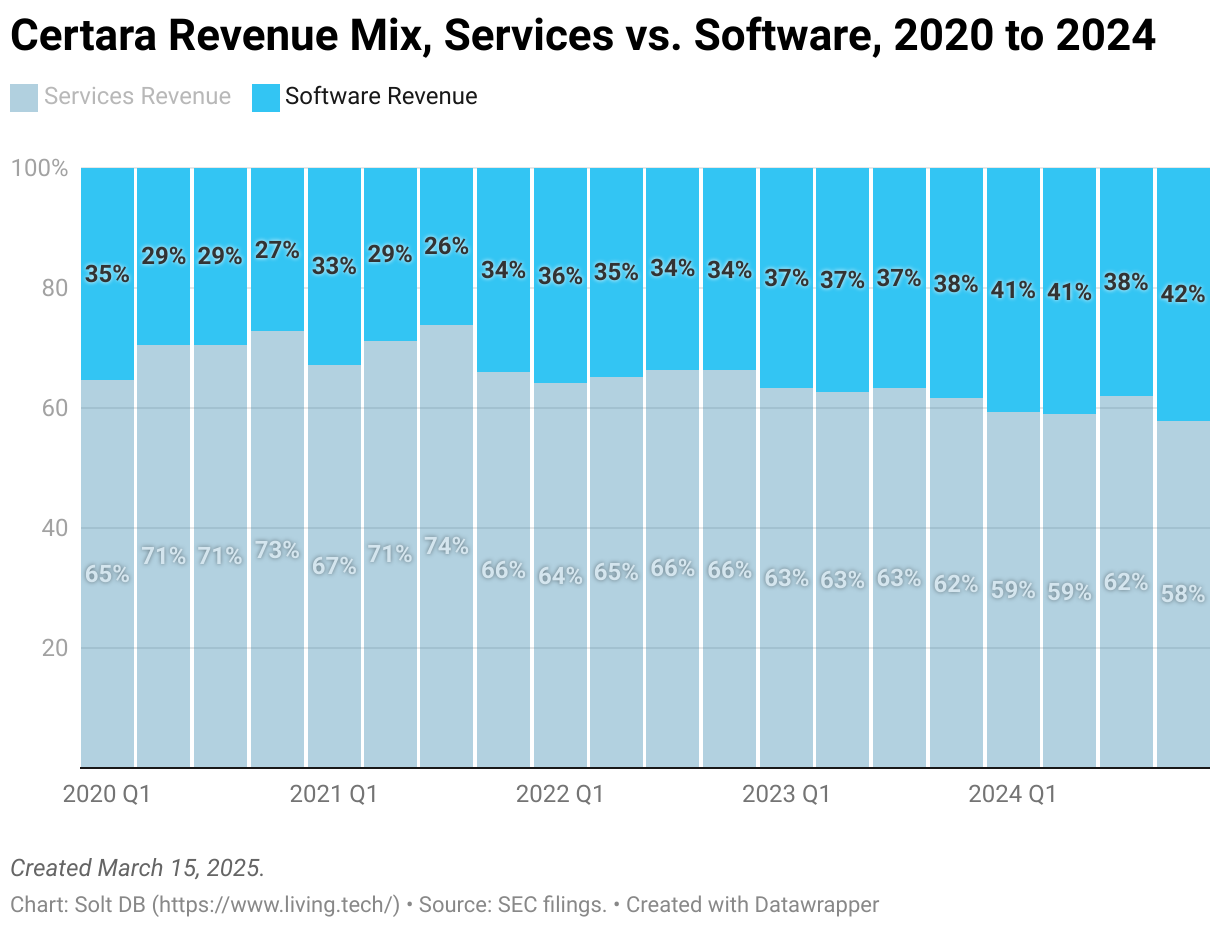

Meanwhile, efforts to maximize Software's share of overall revenue are progressing well. The segment's quarterly revenue has more than doubled since 2020. Software revenue has exceeded 40% of total revenue in three of the last four quarters. My model expects the segment to exit 2025 generating 44.9% of total revenue for the business and average 43.9% for the full year.

If management continues to execute, then it will create considerable operating leverage – the classic goal of a scaled software business.

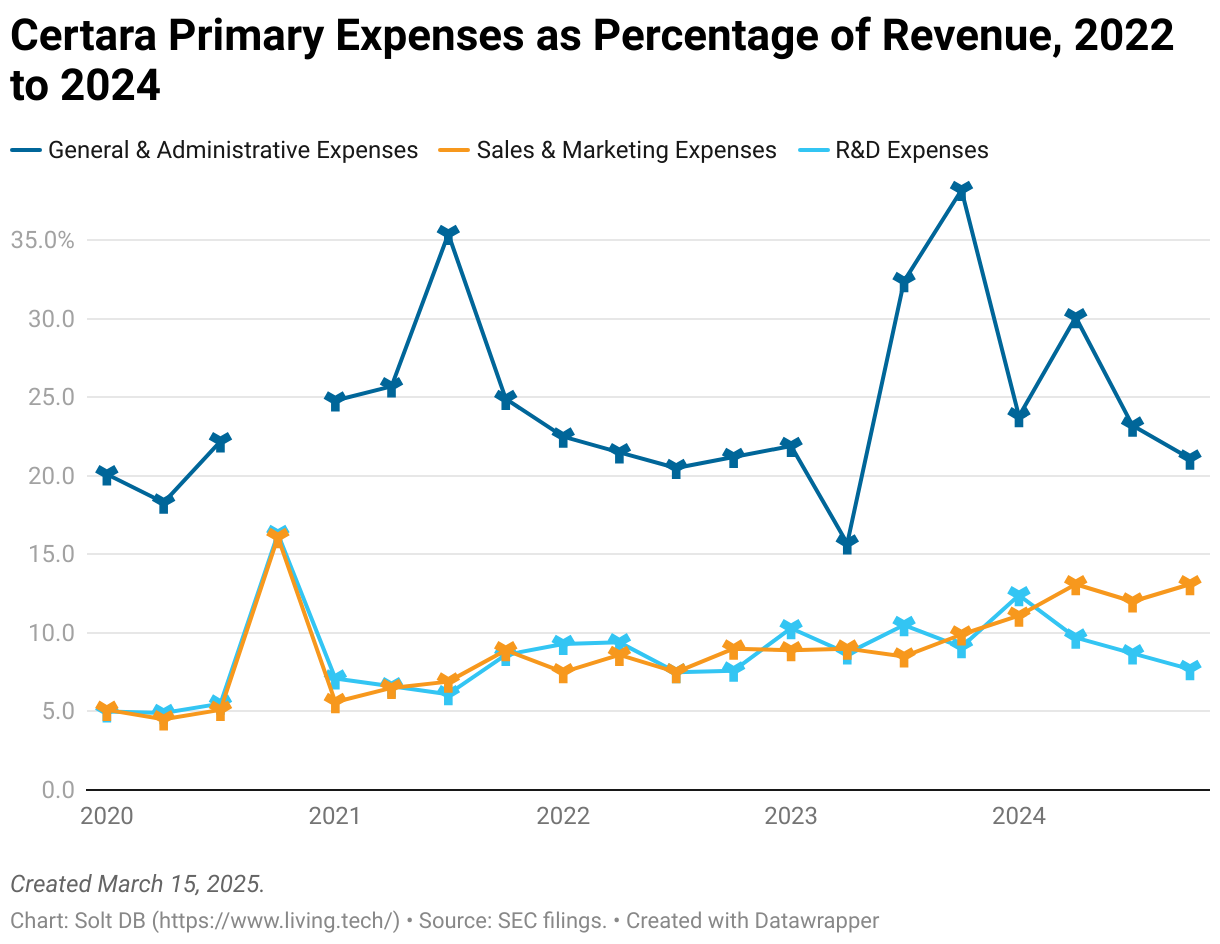

Despite the health of the business, operating efficiency has room for improvement. That's not too surprising given its appetite for acquisitions.

Sales and marketing (S&M) expenses surged 48% year over year. This line item increased by $27.3 million from 2021 to 2024 (growing 136%), compared to a $22.5 million increase in general and administrative (G&A) expenses in that span (growing 18%).

As a percentage of revenue during the same three-year period, S&M expenses have climbed from 7% to 12% on an annual basis, compared to a decline from 28% to 24% for G&A expenses. The more recent acquisitions of Applied BioMath and Chemaxon added new or significant capabilities to the platform, which explains the upward trend. But investors want to see S&M expenses as a percentage of revenue level off or decline eventually.

2025 guidance

Certara issued initial full-year 2025 guidance as follows:

- Revenue of $415 million to $425 million (midpoint of $420 million)

- Adjusted diluted earnings per share (EPS) of $0.42 to $0.46 (midpoint of $0.44 per share)

- Shares outstanding of 162 million to 164 million, representing dilution of just over 1%

Around the Horn

Investors should keep an eye on several developments in 2025. Here's how I'm thinking about them.

Strategic review of Regulatory Services business unit

Certara is conducting a strategic review of its Regulatory Services business, which has singlehandedly tanked the performance of the overall Services segment since 2023. This unit helps customers submit paperwork for new drug applications, biologics license applications, label extensions, responding to regulatory requests, and so on.

Regulatory Services generated full-year 2023 revenue of $60.5 million (17% of total revenue and 27% of Services revenue). That declined nearly 10% in 2024 to just $54.7 million (14% of total revenue and 24% of Services revenue).

If this part of the business is excluded, then Services revenue would have grown 8% in 2024 – more than double the reported growth rate of 3%.

Management is evaluating various scenarios, which may include keeping the unit. The recent weakness was driven by reduced demand from Certara's largest customers, although Regulatory Services returned to revenue and bookings growth in Q4 2024. It's difficult to predict the unit's valuation without knowing profitability metrics, but an asset sale could be worth roughly $50 million.

What makes the Chemaxon acquisition important?

Certara has historically been focused on providing biosimulation software and services for clinical development activities. What's the optimal dose of a drug candidate? How long does it take the body to excrete it? Is a drug candidate likely to have drug-drug interactions or other systemic toxicity issues? Modeling and data are used to inform clinical trial design, labeling of new drug products, and the potential of new formulations.

The acquisition of Chemaxon is focused on discovery-stage development activities. The chemoinformatics platform augments Certara's minimal offerings in this segment of the market with a simple goal: give all customers access to AI drug discovery tools so they don't have to build their own.

It's a large opportunity that's bound to grow quickly. In 2024, biosimulation solutions for clinical-stage molecules represented a $1.4 billion opportunity. Finding and optimizing those molecules with discovery-stage biosimulation tools was valued at $2.04 billion.

There will always be drug developers with specific technical specialties, like Recursion Pharma's mission to map biology and Relay Therapeutics' motion-based drug development. But Certara wants to put powerful predictive analytics tools in the hands of all drug developers to optimize lead discovery.

Integrating platform remains key focus through 2026

To be blunt, the company's software and services offerings are relatively fragmented. Certain tools are siloed. Data from one tool cannot always be accessed in another.

Certara is making progress integrating the overall platform, which would help unlock a few percentage points of growth. Seamless connections between all tools will also reduce the sales and marketing expenses required during a molecule's lifetime.

The vision is to enable customers to discover molecules with promising pharmacological properties (ex: a chemical that might become a drug candidate), then continue using biosimulation software and services during preclinical, clinical, and regulatory stages of development.

Forecast & Modeling Insights

(Reduced.)

Certara is a relatively easy business to model. The company's full-year 2025 guidance is in line with the model introduced in November 2024. However, my expectations for earnings growth were a bit too ambitious, likely due to higher-than-expected S&M expenses.

The current model has been refined with the release of full-year operating results and guidance for the year ahead.

- Full-year 2025 revenue of $421.142 million (vs. $418.144 million previously), up 9.3% from 2024. Company guidance expects a midpoint of $420 million. Services revenue increases roughly 3% to $236.373 million. Software revenue grows 18.7% to $184.769 million total.

- Revenue mix (services / software) settles near 56.1% / 43.9%. That compares to a 59.6% / 40.4% split in 2024 and 71.4% / 28.6% in 2018 (the oldest data available).

- Adjusted net income of $74.5 million (vs. $84.5 million previously), up 2% from $72.9 million in 2024

- Diluted earnings per share (EPS) of $0.46 (vs. $0.52 previously), up one penny from $0.45 in 2024. Company guidance expects a range of $0.42 to $0.46 per share in diluted EPS.

The current model excludes any impact from acquisitions or asset sales.

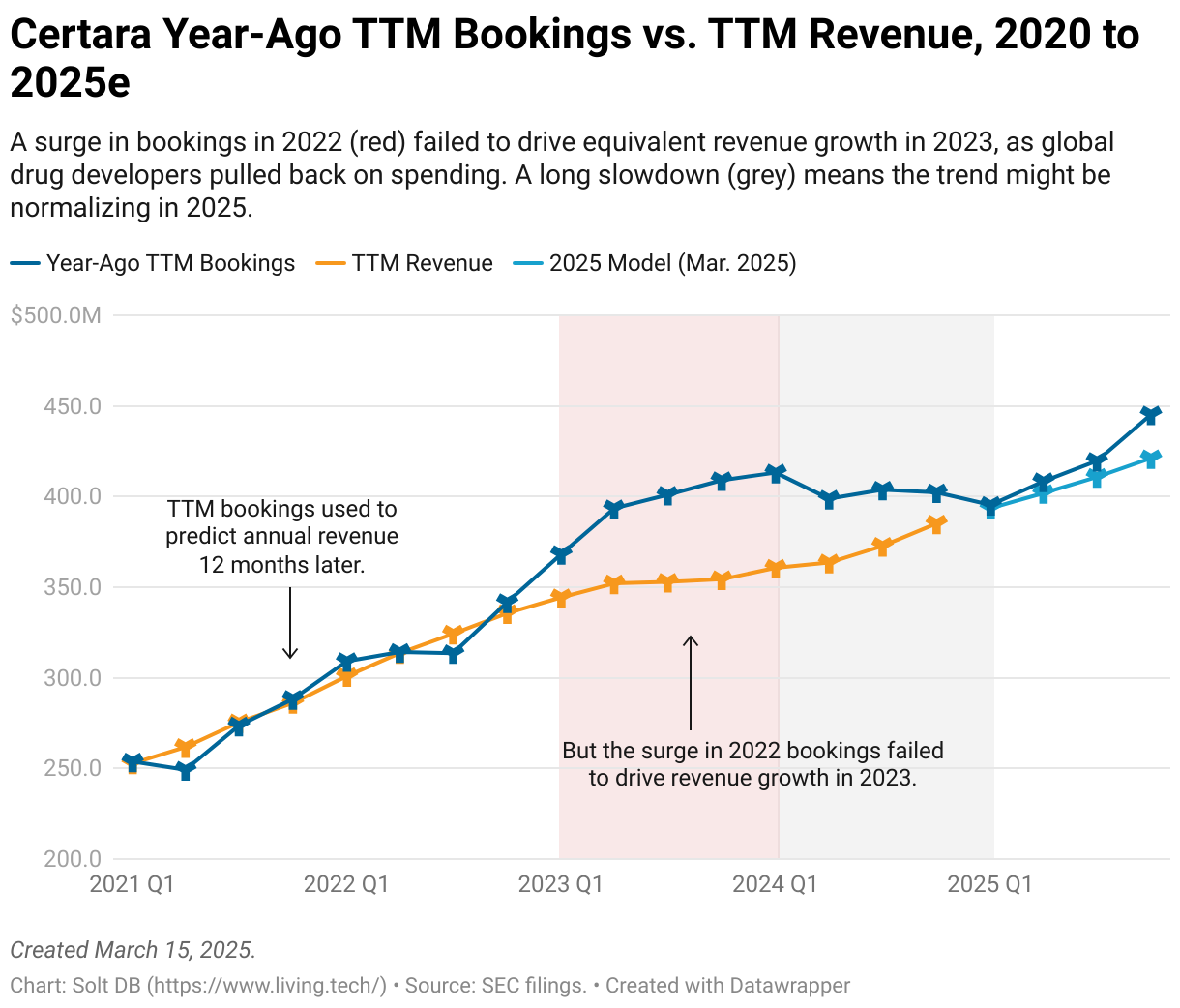

The model aligns well with full-year 2025 guidance and, importantly, the relationship between trailing twelve-month (TTM) revenue and bookings. If bookings once again become predictive of revenue similar to pre-2022, then it'll be a sign the biotech sector is recovering – or the business has repositioned itself for the new reality, at least.

I walked through the relationship between year-ago TTM bookings and TTM revenue in the same section of a previous research note. The chart below has been updated with the most recent numbers through Q4 2024.

Margin of Safety & Allocation

Certara is considered an Anchor position. The current fair valuation for the company based on my 2025 model is below:

- Market close March 14: $10.92 per share

- Modeled Fair Valuation: $11.62 per share

- Allocation Range: Up to 10%

Certara reported 161.017 million shares outstanding as of February 17, 2025. The modeled fair valuation above assumes 162.628 million shares outstanding, which is equivalent to 1% dilution.

Further Reading

- February 2025 press release announcing Q4 2024 operating results

- February 2025 regulatory filing (10-K) detailing 2024 operating results

- November 2024 research note evaluating Q3 2024 operating results and introducing the initial 2025 model for the business

-cropped.svg)