.svg)

What does Ginkgo Bioworks want to be when it grows up? The company is still figuring that out.

I would argue the business was the single-biggest winner from the pandemic boom among all biotech companies – and perhaps all companies period. It launched onto the public markets through a special purpose acquisition company (SPAC), at a valuation that was more than double its last private fundraise, and added over $1 billion in cash to the balance sheet in the process. The founders perfectly timed the window to go public.

The financial runway was bolstered by leveraging its expansive laboratory space and political connections to provide COVID-19 testing for the Boston metro, then Massachusetts, and then significant swaths of the United States. Pathogen testing services raked in full-year 2021 revenue of $200 million and another $334 million the next year, which helped to offset losses from the core business.

Then again, the timing of the company's public debut and its impressive marketing machine masked some rather large deficiencies embedded in the business and shareholder structure. The core platform is challenged by both economics and a low probability of success for commercializing programs, while the number of shares outstanding increased 43% in the last two years.

More pressing for individual investors, few analysts seem to be paying attention to the very real risks surrounding the most important asset: data.

What Does Ginkgo Bioworks Do?

Ginkgo Bioworks has two operating segments:

- Cell Engineering ("the foundry") provides research services to companies across the bioeconomy. This segment operates as a contract research organization (CRO), which leverages large, automated laboratories to conduct biological research on behalf of customers.

- Biosecurity ("pathogen detection") provides large volume genetic testing services to public and private entities for the early detection of pathogens. For example, public school systems used this segment, called Concentric, for processing large volumes of COVID-19 test kits, while airports use the service for screening passengers and wastewater to get ahead of potential outbreaks for seasonal (or worse) pathogens.

Cell Engineering is the core business of Ginkgo Bioworks. An industrial biotech company looking to genetically engineer a microbe capable of producing an animal-free protein more efficiently might outsource the project to the foundry. An agricultural biotech company could tap Ginkgo's greenhouses in California to optimize a new crop trait before conducting field trials across thousands of acres. A drug developer could leverage the foundry for discovery programs (prior to preclinical testing) that might lead to drug candidates a couple years later.

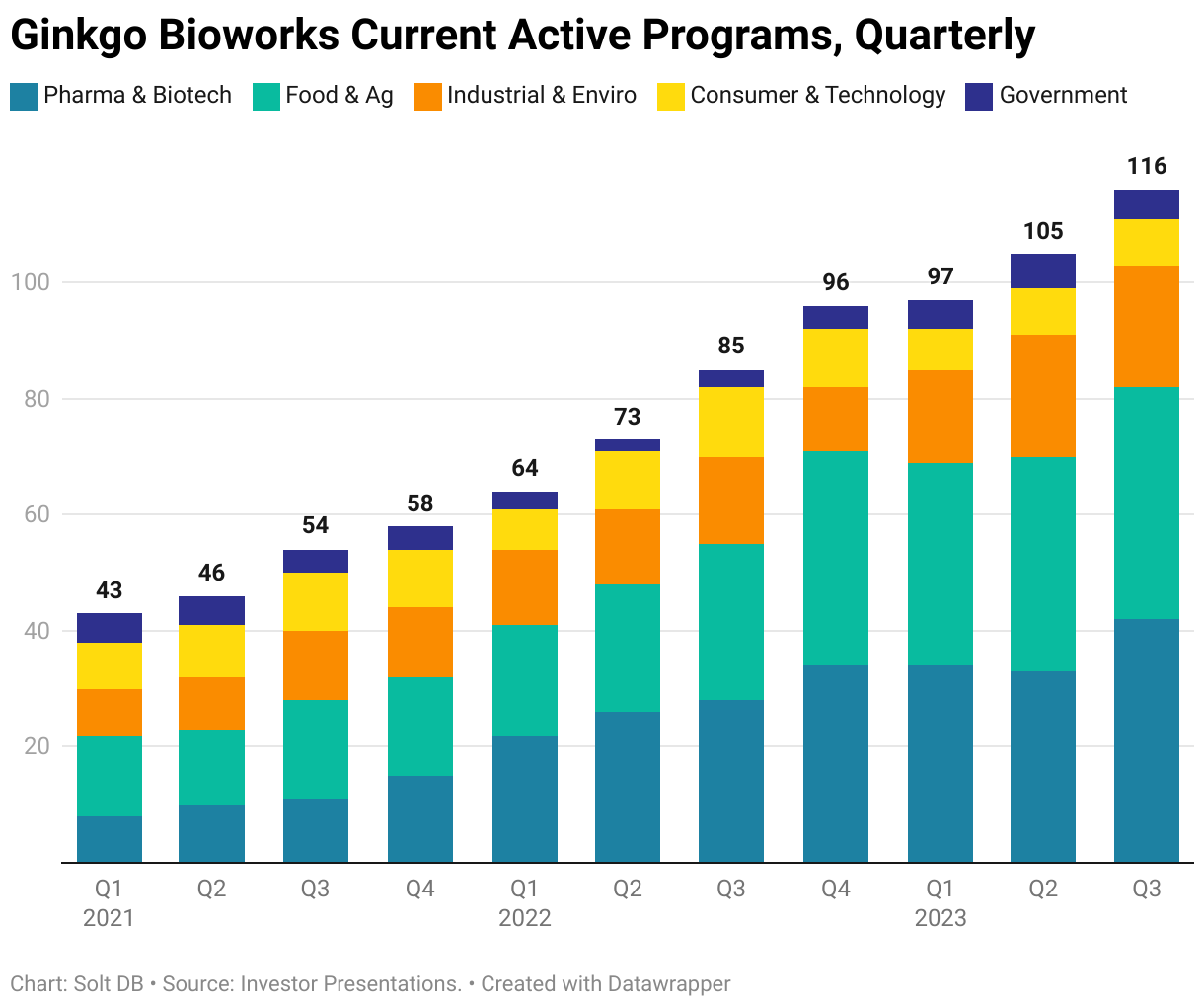

The business reports the number of current active programs at the end of each quarter, programs added during the quarter, and cumulative programs as of the end of each quarter. These are useful for gauging traction for Cell Engineering services, but provide much less analytical value than investors think. That's because programs are valued significantly differently across each industry and each customer. A lower number of high-value programs (such as in agricultural biologicals) would be better for long-term value creation than a higher number of low-value programs (such as in industrial enzymes).

For this segment, Ginkgo Bioworks generates services revenue when certain milestones are achieved within the scope of research programs. The business often structures contracts to also include downstream value potential, which can take a few forms:

- One-time payouts can be earned when products discovered at the foundry achieve certain development milestones. For a drug developer customer, this might be triggered when an asset enters clinical trials, doses the first patient in a late-stage clinical, and/or earns regulatory approval. These payouts will typically take two to six years to be realized from drug developer customers, but discovery-stage assets don't always advance into clinical trials.

- One-time payouts can be earned when products discovered at the foundry achieve certain commercial milestones. This might be triggered when a customer's asset achieves a certain annual sales level. For example, an industrial solvent produced by a microbe that originated in the foundry might one day achieve $50 million in annual revenue, which could trigger a one-time $5 million milestone payment to Ginkgo Bioworks.

- Recurring payouts structured as royalties when products discovered at the foundry generate revenue. Although modeled after drug development licenses, many industrial and agricultural biotech products have sharply lower economic realities. That means the royalty potential of these products is significantly lower than, say, a cell therapy product that originated at the foundry.

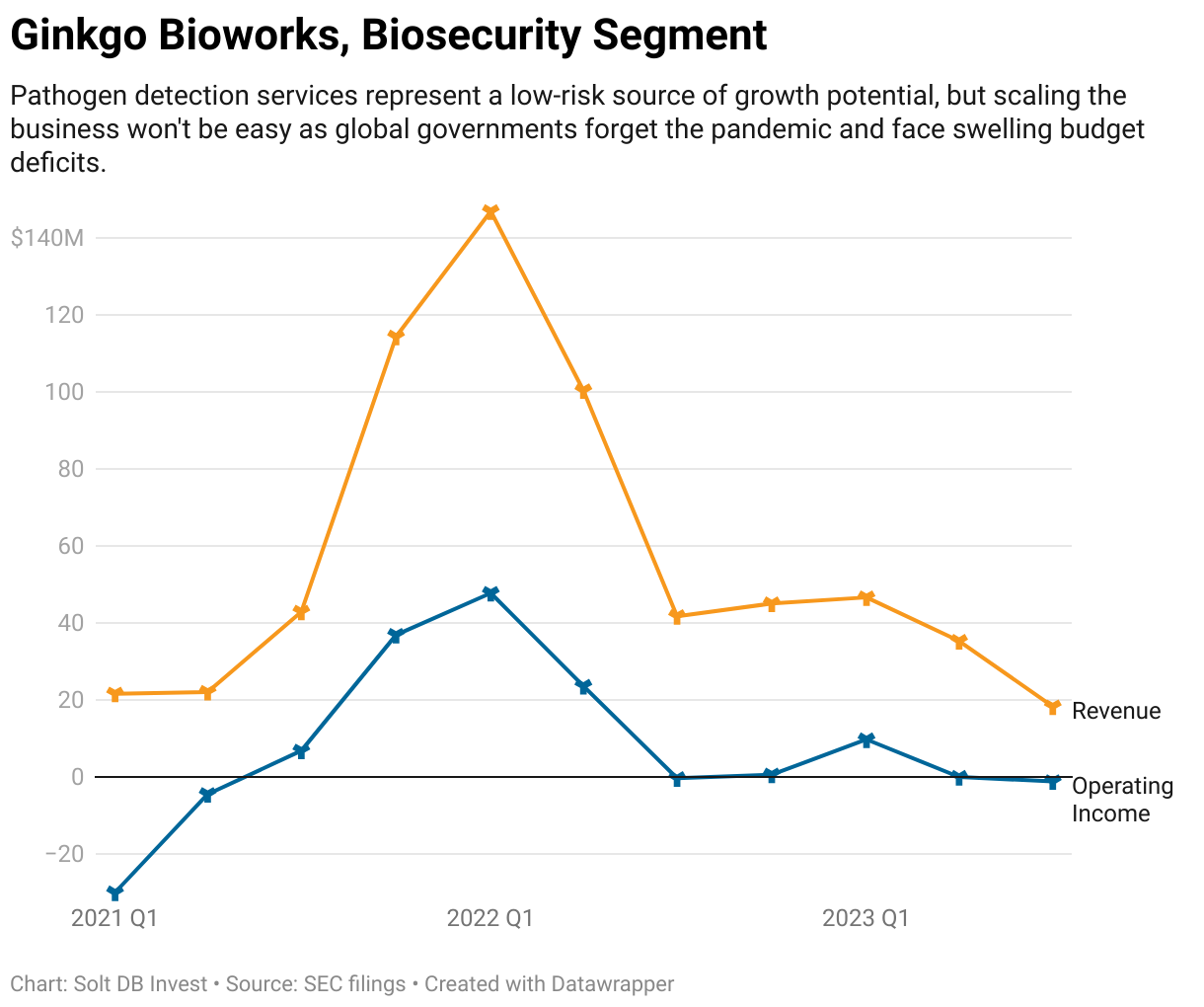

As for the Biosecurity segment, the pandemic boom might be over, but pathogen detection services boast attractive margins and are a low-risk source of growth potential. Ginkgo Bioworks generated only $18.2 million in third-quarter 2023 revenue from Biosecurity, but the segment sported an operating loss of only $1.1 million. It's not a distraction or a waste of resources. If scaled, then it could be a reliable source of cash flows and help to offset woeful operating margins from Cell Engineering.

However, the business will face an uphill climb in its attempt to scale the Biosecurity segment. Pathogen detection services might be a great idea and a much-needed type of surveillance for modern society, but it's not an expense public or private entities are used to paying for even as we enter 2024. Swelling budget deficits from Western nations make austerity measures a very real possibility in the near future, and it's difficult to see biosecurity services surviving austerity budgets.

By the Numbers

Ginkgo Bioworks has had a challenging year.

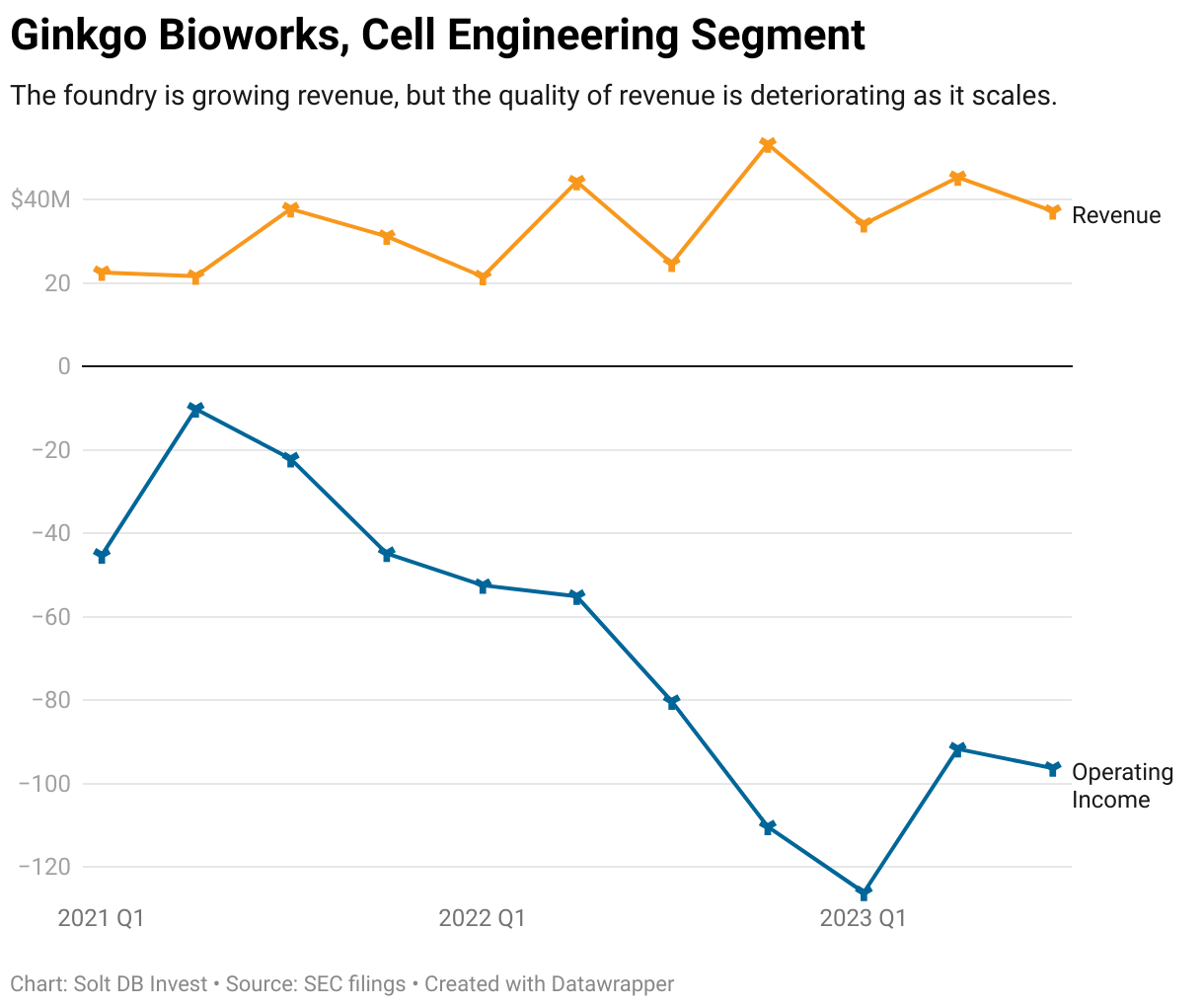

The company expects Cell Engineering revenue growth to stagnate in 2023 despite growing the number of current active programs by over 20%. Segment operating losses in the first nine months of 2023 have already exceeded the full-year 2022 total, driven by increasing expenses. A deteriorating quality of revenue will blunt the value of revenue growth. As the market moves on from "growth-at-all-costs" business models, higher revenue from the foundry won't necessarily drive the share price higher.

The foundry, much like biology and the bioeconomy, is complex. That makes it difficult for Ginkgo Bioworks to accurately forecast its own performance. For example, the company has recently focused more of its bandwidth on drug development partners, which have large resources and are familiar with licensing and royalty contracts. However, those contracts, especially with larger pharma companies, are less lucrative upfront. That can lead to less revenue even as program count grows -- at least initially.

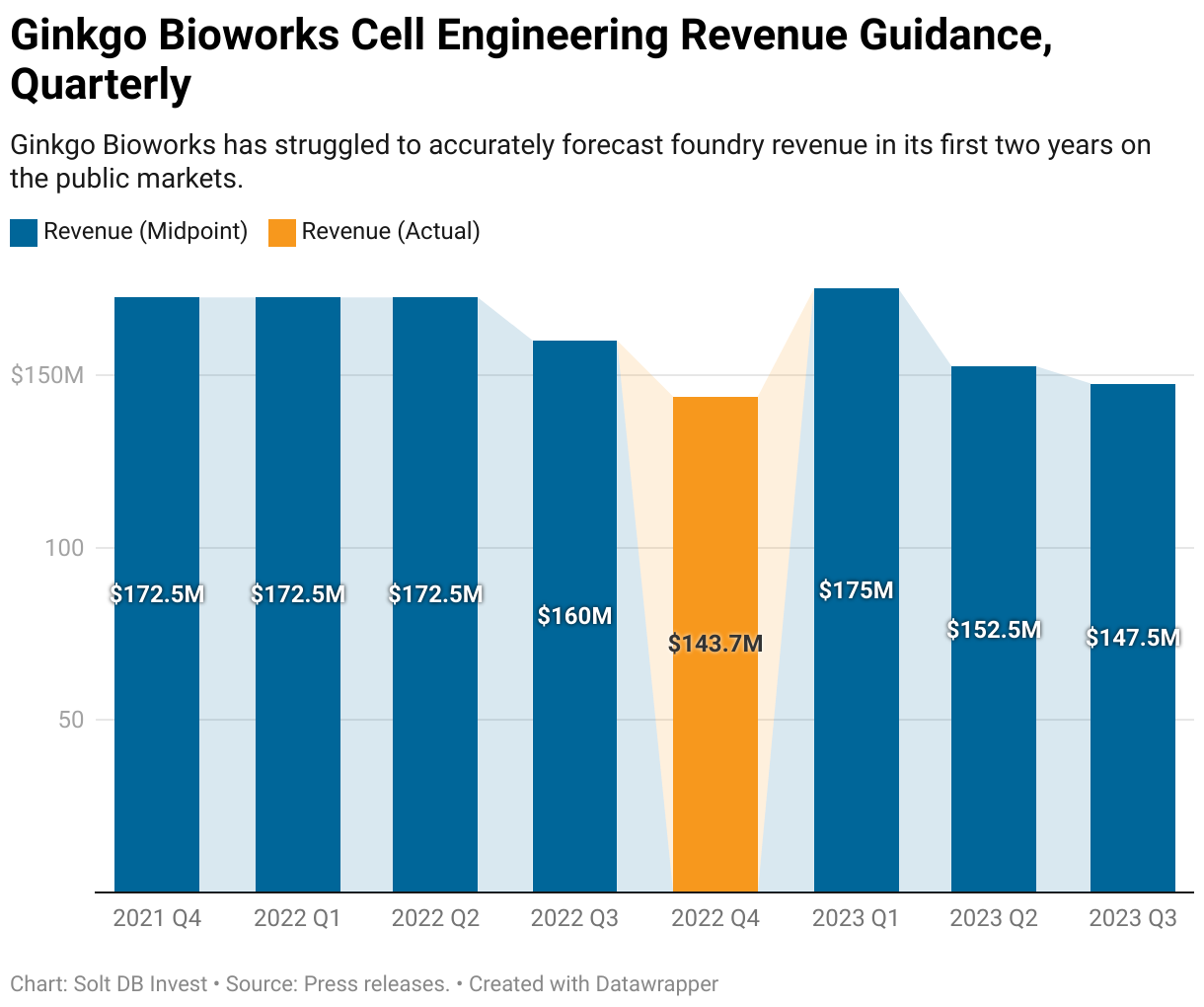

Regardless of the factors driving the company's forecasting challenges, Ginkgo Bioworks needs to do a better job setting expectations for investors. The business has whiffed on its initial guidance in each of its first two full years on the market.

Meanwhile, the Biosecurity segment was expected to see a significant reduction in revenue from 2022. The declining performance has not been a surprise. It just stings a little more against the backdrop of swelling Cell Engineering losses. The pathogen detection segment generated operating income of $71.3 million in the first half of 2022, but only $8.7 million total in the five quarters since. The next few years are likely to be characterized by a long, difficult slog of scaling a new and unfamiliar service.

The overall business will continue to be buoyed by the significant cash balance, which stood at $1.05 billion at the end of September 2023. Ginkgo Bioworks has a handful of factors within its control which can be leveraged to manage cash burn in the next few years. The business can fund operations into 2026 near current levels of cash burn.

However, Wall Street will start to become more anxious with each passing quarter starting in 2024. Individual investors should be prepared for increased volatility, a potential reverse stock split, and a potentially much lower valuation by the end of 2024.

The Importance of Properly Set Expectations

Many biotech stocks have experienced significant declines since the pandemic boom. Investors are still struggling to sort out which are justified and which represent an opportunity. That's kind of the point of Solt DB Invest, which encourages investors to think in objective terms and think of the margin of safety for an investment, ranked dynamically against other available investments.

A biotech stock that's down 80% isn't necessarily a great opportunity. What valuation has the stock descended 80% from? How much of the decline was driven by dilution? Individual investors must be careful not to blindly anchor expectations to the glory days of 2020 and 2021.

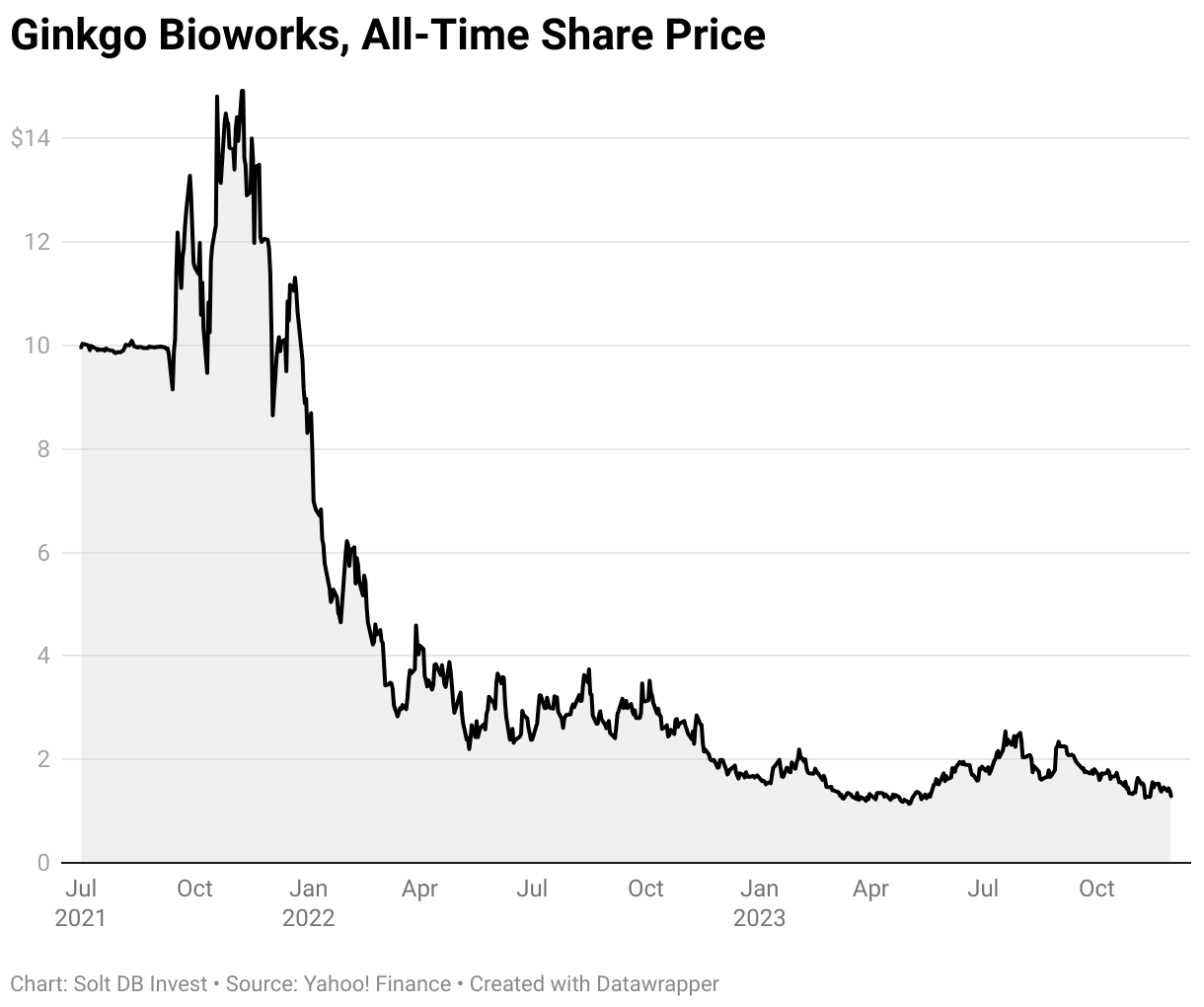

Unfortunately for Ginkgo Bioworks, the math isn't very favorable and certainly doesn't point to a speedy recovery to the SPAC price. If shares climbed back to $10 apiece, then the business would be valued at $21.2 billion. If shares reclaimed their all-time high of $15.86 apiece, then the business would boast a valuation of $33.6 billion. There is absolutely no scenario where either valuation is realistic in the next five years. It might not even be possible by 2030.

Why is it unlikely for Ginkgo Bioworks to reclaim its SPAC price or all-time high in the foreseeable future? Even before considering our model, it's important to understand two structural components that impact the company's valuation.

Dilution is a Permanent Value Reducer

Consider that shares are down 86% from the SPAC price. However, the number of shares outstanding has increased by 43% since November 2021. That alone is responsible for half of the share price decline – and that cannot be clawed back. There's also a decent amount of dilution still on the horizon.

Expectations Have Materially Declined

Another factor to consider is how expectations that drove the SPAC valuation have changed in the last two years.

At the time of the SPAC, Ginkgo Bioworks projected full-year 2023 revenue of $341 million from Cell Engineering alone. The core segment was expected to scale annual revenue to $628 million in 2024 and $1.1 billion in 2025. The business now expects the segment to have full-year 2023 revenue of just $147.5 million.

The reasons for reduced expectations aren't important in this context. The reality is significantly less growth than previously expected equates to a significantly lower valuation.

Next: An Individual Investor's Cheat Sheet for Ginkgo Bioworks

The headline figures of Cell Engineering programs and revenue will garner the most attention from investors and analysts, but they're not so important at this stage in the business' trajectory.

Solt DB Invest will provide preliminary forecasting insights in an upcoming article, including headwinds and challenges such as:

- Scenarios for scaling the Biosecurity segment.

- Structural changes in how research is conducted in the life sciences can provide a tailwind for Cell Engineering.

- Why the data generated by Ginkgo Bioworks, formerly known as Codebase, might be less valuable than analysts expect.

- A segment-by-segment look at program valuations and modeling.

- Evaluating near-term value creation potential from the Cell Engineering segment, with a focus on agricultural biologicals instead of drug development.

- Using the upcoming public debut of Bolt Threads for details about the pace of progress in industrial biotech programs in the foundry.

If subscribers have pointed questions about Ginkgo Bioworks, then share them in Discord and I'll be sure to share those insights in the upcoming article.

Margin of Safety & Allocation

Ginkgo Bioworks is considered a Growth (Speculative) position. Solt DB Invest will introduce a multi-year financial model for the business and add the stock to the Margin of Safety Dashboard in early 2024.

Further Reading

- Late 2022 article evaluating the low success rate from Ginkgo Bioworks' foundry (Ginkgo Bioworks and Amyris Whiffed on Commercial Promises)

- Late 2022 article evaluating the company's focus on a horizontal platform and the risks of shunning manufacturing assets (Ginkgo Bioworks' Original Sin)

- Late 2022 article including interviews with one dozen founders, executives, and elite academics in synthetic biology (How to Win in Synthetic Biology)

-cropped.svg)