.svg)

If IPOs and SPACs were cool during the liquidity bubble of 2020 and 2021, then the reverse merger might be how the end of 2023 is remembered. Unfortunately, they're a sign of the continued unwinding of the liquidity bubble -- not quite as cool as a SPAC or flashy IPO, and certainly not as lucrative for existing shareholders.

The concentration of reverse mergers in the gene therapy and gene editing space in particular signals the difficult funding environment for these specific ventures.

CRISPR gene-editing hopeful Graphite Bio merged with Lenz Therapeutics, which develops drug candidates for eye diseases. Former gene therapy powerhouse Homology Medicines merged with Q32 Bio, which develops drug candidates for autoimmune and inflammatory diseases. Immune tolerance leader Selecta Biosciences merged with Cartesian Therapeutics, which develops RNA-based cell therapy for rare diseases.

For the latter, RNA-based cell therapy is a relatively promising approach on paper, but this is an entirely different company now. Considering that and some not-so-favorable financial realities, Solt DB Invest is closing coverage of Selecta Biosciences. The economic potential of the former pipeline remains intact through contingent value rights granted to previous shareholders, while closing coverage gives us the opportunity to introduce research of a more investable company (we recently announced MoonLake Immunotherapeutics and Schrodinger were added to our coverage ecosystem). Here are some closing thoughts on the merger and the path forward for Cartesian Therapeutics.

A Lack of Execution and Meaningful Traction

A confluence of two powerful forces led to the company's fateful decision: A lack of execution and declining interest in gene therapy.

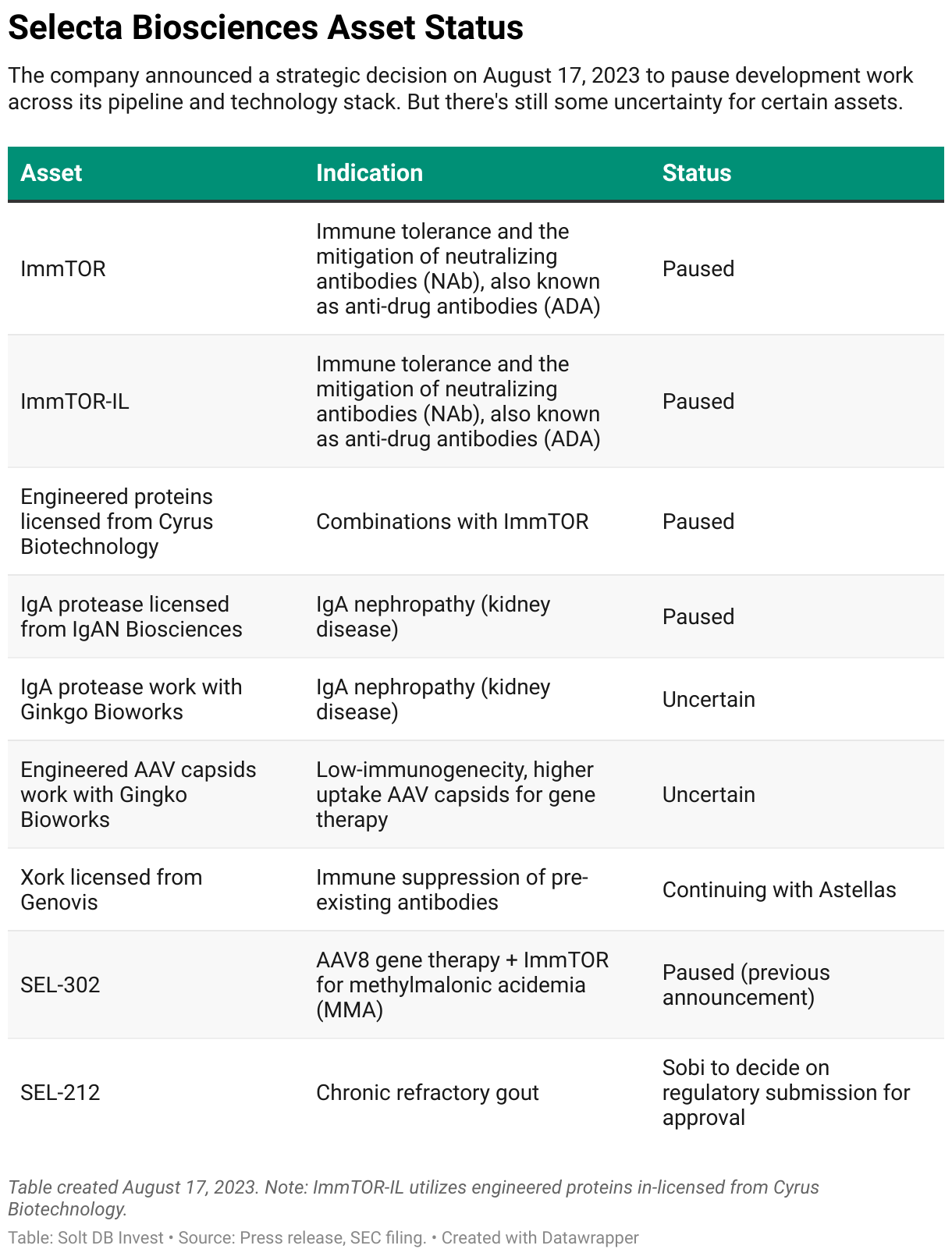

Selecta Biosciences at various times had licensing deals and partnerships with Takeda, Spark Therapeutics, Sarepta Therapeutics, Ginkgo Bioworks, and Astellas. The lead drug candidate licensed to Sobi is on track to earn regulatory approval by early 2025, then offer strong competition to Horizon Therapeutics' workhouse Krystexxa in chronic refractory gout. Krystexxa had $716 million in full-year 2022 revenue. Solt DB Invest expects SEL-212 to generate peak annual revenue of over $500 million (the company expects up to $700 million).

Despite multiple major licensing agreements, there wasn't enough meaningful commercial traction. Takeda disbanded its gene therapy unit. Sarepta Therapeutics and Spark Therapeutics decided not to pursue the company's ImmTOR immune tolerance tool in clinical trials. The next-generation tools with legitimate potential -– Xork and ImmTOR-IL – were too early to make a difference. Meanwhile, Selecta Biosciences frustrated investors with a lack of progression within its wholly-owned pipeline, a grievance the finch has noted multiple times in our research.

It's difficult to build a business – or find enough willing investors – on hopium alone.

The merger with Cartesian Therapeutics is a slightly better outcome than bankruptcy. Previous investors of Selecta Biosciences will receive contingent value rights (CVRs) allowing them to benefit from the future commercial success, if any, of the company's immune tolerance pipeline. That could be somewhat worthwhile given the market potential of SEL-212, which is why I'm keeping my CVRs. There's not much risk to letting it ride at this point.

But make no mistake: The immune tolerance pipeline of Selecta Biosciences will no longer be actively developed. This is a completely different company now.

Cartesian Therapeutics Has Potential, But It's a Mess

The new company has adopted the public listing of Selecta Biosciences and the drug pipeline of Cartesian Therapeutics. The stock ticker has changed from $SELB to $RNAC.

Cartesian Therapeutics is developing RNA-based chimeric antigen receptor T cell (CAR-T) therapies. Whereas existing CAR-T cell therapies utilize gene editing techniques to engineer desired characteristics (DNA based), the company's technology platform utilizes RNA tools to do the same (RNA based). There are meaningful benefits and drawbacks to the approach.

- No Lymphodepletion: The company's rCAR-T cell therapies don't require patients to undergo complicated lymphodepletion (chemotherapy) treatment before being administered cell therapy, which significantly reduces risks and side effects.

- Controllable Therapeutic Window: Cartesian Therapeutics can provide multiple doses of its rCAR-T to drive a therapeutic response. Although each dose packs a smaller punch, the overall response can be finely tuned over multiple doses while maintaining an acceptable tolerability profile. Traditional CAR-T cell therapies often must be dosed in a single administration, which can provide meaningful benefit but with greater toxicity.

- Community Friendly: CAR-T cell therapies might grab headlines, but higher toxicity risk means they have to be administered in facilities equipped to deal with cytokine release syndrome (CRS) and neurotoxicity. rCAR-T cell therapies can potentially be administered in community facilities – where roughly 80% of cancer patients are treated.

- All-In-One Platform: Cartesian Therapeutics is currently pursuing autologous cell therapies (cells derived from patients), but is developing tools for allogeneic (off the shelf) and in vivo (editing cells inside patients) approaches.

Despite the potential of rCAR-T cell therapy, there are some drawbacks. The likely need for multiple doses – up to six – requires multiple administrations over months. For rare diseases with no or few treatment options, that can be an acceptable inconvenience. But the competitive landscape for many autoimmune diseases is increasingly crowded with more convenient options, such as bispecific antibodies or novel small molecules. Cartesian Therapeutics' lead indication, myasthenia gravis (MG), is a solid target. The rest of the pipeline might find competition creeping up sooner than expected.

This is important to highlight in the context of Selecta Biosciences' immune tolerance platform. As noted previously, the intravenous administration requirement for ImmTOR-IL was a significant drawback. That likely meant it would be boxed up in the rarest of rare diseases and fall behind in, say, Type 1 diabetes. Convenience almost always trounces efficacy.

The lead drug candidate from Cartesian Therapeutics, Descartes-08, will next have a data readout from a phase 2b clinical trial in MG. The primary endpoint is the percentage of patients who achieve a six (6) point improvement on the self-reported MG-ADL scale at 12 weeks compared to those receiving placebo. Although possible with optimized doses, a previous trial failed to reach that mark. Descartes-08 appeared to be safe and effective with deepening responses through week 36 (beyond a six-point improvement on the MG-ADL scale), but the ongoing study's endpoint might lead to disappointment on Wall Street.

Outside the clinic, there's also the messy new reality of the outstanding share base. Reverse mergers are rarely straightforward. For Cartesian Therapeutics, there are a whopping 696.2 million shares outstanding. That almost guarantees shares won't trade above the $1 per share mark – and essentially necessitates a reverse stock split (20-to-1 or 15-to-1 is my guess) to maintain standing on the Nasdaq.

Ol' Maxxie's Path Forward

Solt DB Invest isn't a stock recommendation platform. We provide research for stocks that are very risky – and those that are significantly less so. As such, the finch also provides suggested allocations for each stock in its coverage ecosystem based on a portfolio of 10 to 15 holdings total.

There's a big difference between a stock like Relay Therapeutics, where we think investors can comfortably have an allocation of up to 15%, and a stock like NeuBase Therapeutics, where we thought allocations should've maxed out at 0.5%. Stock recommendation services treat all stocks equally – and only tell you to buy stocks. We learned individual investors are frustrated with that approach. That's why we focus on providing objective research whether stocks are overvalued, fairly valued, or undervalued.

For Selecta Biosciences, we thought allocations should've maxed out near 2.5% after the company paused development of its pipeline in August 2023. Those shares have since been sold and/or converted into shares of Cartesian Therapeutics, plus CVRs. Individual investors might still find long-term value in the CVRs, especially if Sobi continues with the regulatory filing and potential commercial development of SEL-212.

Owning a CVR is essentially like owning a share of a business, but it provides rights to "share" in the future economic potential of an asset or business unit. In this scenario, CVRs granted for Selecta Biosciences allow investors to enjoy any financial benefits from SEL-212 (owned by Sobi), Xork (being developed by Astellas), and ImmTOR-IL (on the shelf). The significant economic potential of SEL-212 makes the CVRs worth hanging onto – there's not much risk at this point – but be prepared to wait for several years for a meaningful payout.

Further Reading

- "It's Acquisition or Bust for Selecta Biosciences" research note from November 2023 prior to the merger announcement with Cartesian Therapeutics

- "Selecta Biosciences Pauses Most Development, Seeks Licensing" research note from August 2023 evaluating the company's decision to halt development and seek alternative paths forward

- "Selecta Biosciences Navigates Shifting Gene Therapy Landscape" research note from May 2023 evaluating the deteriorating landscape for gene therapy tools and drug developers

.svg)

.svg)

.png)

.svg)

.svg)

.svg)