.svg)

I have sold my entire position in Krystal Biotech, which was 10% of my portfolio based on principal added.

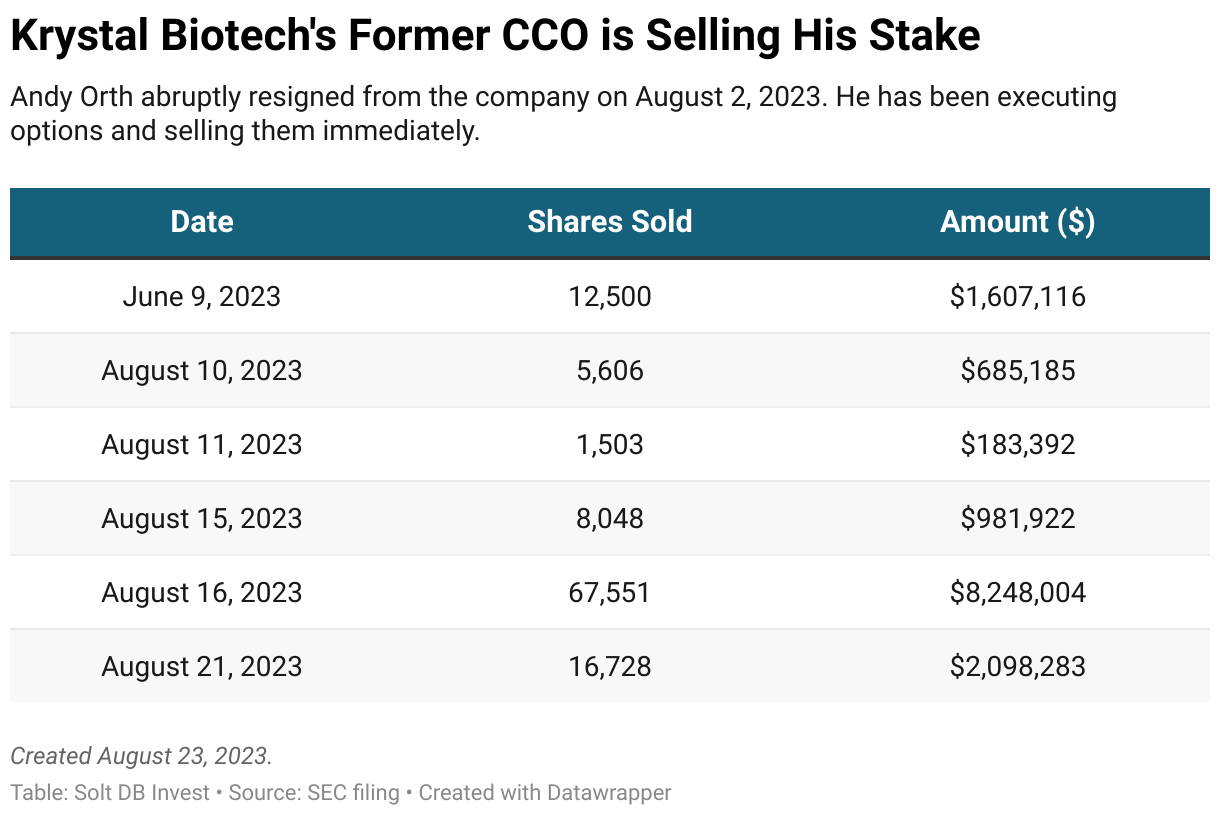

The now-former Chief Commercial Officer (CCO) Andy Orth appears to be selling his entire position in the company since departing. Although investors might find that easy to justify, the shares liquidated so far total over $12 million in five transactions from August 10, 2023, through August 21, 2023. These transactions are so new they don't yet appear within "insider activity" financial feeds.

According to his awarded options, he's probably not done.

The CCO's abrupt departure during the commercial launch and ramp of Vyjuvek already made me uneasy. When combined with additional information I might have been trying to ignore for too long, it's difficult to justify keeping Krystal Biotech in my portfolio.

Have I Been Biased Towards Krystal Biotech?

My position in Krystal Biotech has gained over 100%. That's solid for any investment in less than two years, more so when those two years stretch from 2021 to 2023 and include biotech. Although that might make it easier to neglect the position, I've become increasingly uneasy with recent developments, especially against the information I've perhaps neglected to fully price in.

Regulatory filings reveal Andy Orth, the former CCO who abruptly departed during Vyjuvek's commercial launch and ramp, has sold roughly 99,200 shares of Krystal Biotech in the 12-day period beginning August 10, 2023.

There's more to it than that. Gather 'round, it's story time.

In November 2017, I received a cease and desist letter from Intrexon. The company was a synthetic biology conglomerate unhappy with my critical reporting on its circular business model. The business had been buying large stakes in small and microcap companies, which then paid Intrexon for "R&D services." Complexity and obfuscation were key to the business model, although that only risked screwing over the little guy.

Intrexon was eventually investigated by the U.S. Securities and Exchange Commission (SEC) and left the public markets after a secretive agreement with regulators. Intrexon executives Krish Krishnan and Suma Krishnan, who had deep loyalties to Intrexon owner R.J. Kirk from the trio's days at New River Pharmaceuticals (acquired for $2.6 billion in 2007), had front row seats to it all.

That is, until they left to start Krystal Biotech in 2016. That association always made me uneasy. It's not the only information I've struggled with.

On the one hand, Krystal Biotech's technology platform has been validated in the real world. It's not a lab trick. It works. It has attractive potential.

On the other hand, Krystal Biotech has a history of questionable decisions. It stole technology for herpes simplex virus (HSV) gene therapy from PeriphaGen, a former neighbor, which led to a legal settlement that will cost up to $62.5 million. In my research and network through the Pittsburgh biotech scene, I've also heard the company is a complete shitshow internally. That's probably true of most companies, but multiple stories from multiple sources are difficult to ignore indefinitely.

Perhaps I've ignored those things for too long. Perhaps I've "looked the other way" because Krystal Biotech is based in my hometown of Pittsburgh, a place I desperately want to start delivering on its potential as an emerging biotech hub. Perhaps the only reason that hasn't stung yet is due to timing.

Shares of Krystal Biotech have performed well – and they still have upside potential if the company executes across the portfolio and pipeline. The business could be worth multiples of its current valuation if it executes with the commercial ramp of Vyjuvek, delivers promising results for KB407 in cystic fibrosis, and/or gets acquired.

But success doesn't change the process. My investing success has been derived from constantly reevaluating theses, removing emotions, and handling every opportunity objectively. Although the business could be worth more in the right circumstances, it could also be worth considerably less if various deficiencies begin to bite during a crucial stretch. I can identify other investment opportunities with similar or better upside and less risk.

Forecast & Modeling Insights

(Downgraded)

Krystal Biotech has been downgraded from a Growth (Speculative) to a Flyer position.

Solt DB Invest will still provide Base Research and timely research notes on the company. The only thing that changes is we will no longer model the fair valuation and the company will no longer have a Margin of Safety. A Flyer position is understood to be a very high risk investment.

Margin of Safety & Allocation

(Downgraded)

Krystal Biotech has been downgraded from a Growth (Speculative) to a Flyer position. As a result, all modeling has been suspended and there is no longer a suggested allocation.

Further Reading

- August 2023 regulatory filing (Form 144) describing transactions from Andy Orth in the preceding three months

- August 2023 research note analyzing the departure of CCO Andy Orth

.svg)

.svg)

.png)

.svg)

.svg)

.svg)