.svg)

First-ballot Hall of Fame spender Arrowhead Pharmaceuticals is suddenly flush with cash. That's good, because the company is about to spend even more money in the coming years.

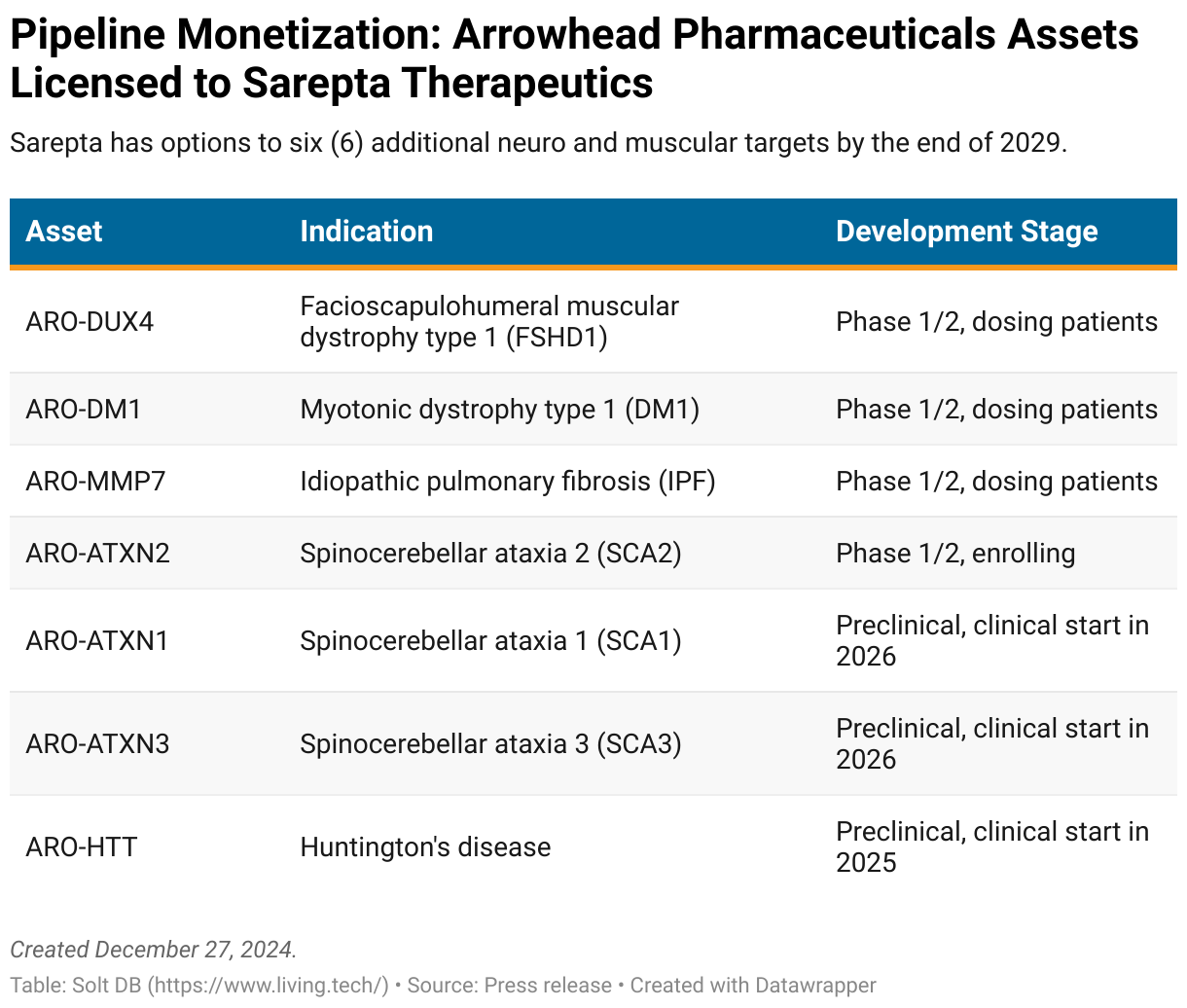

The RNA interference (RNAi) specialist delivered on its promise to monetize a productive R&D engine by inking a significant licensing deal with Sarepta Therapeutics. The agreement hands over rights to four (4) clinical-stage assets and three (3) preclinical assets in therapeutic areas spanning neuro, muscular, and lung diseases. The partner can direct Arrowhead to conduct discovery and preclinical work against up to six (6) additional neuro or muscular targets through 2029.

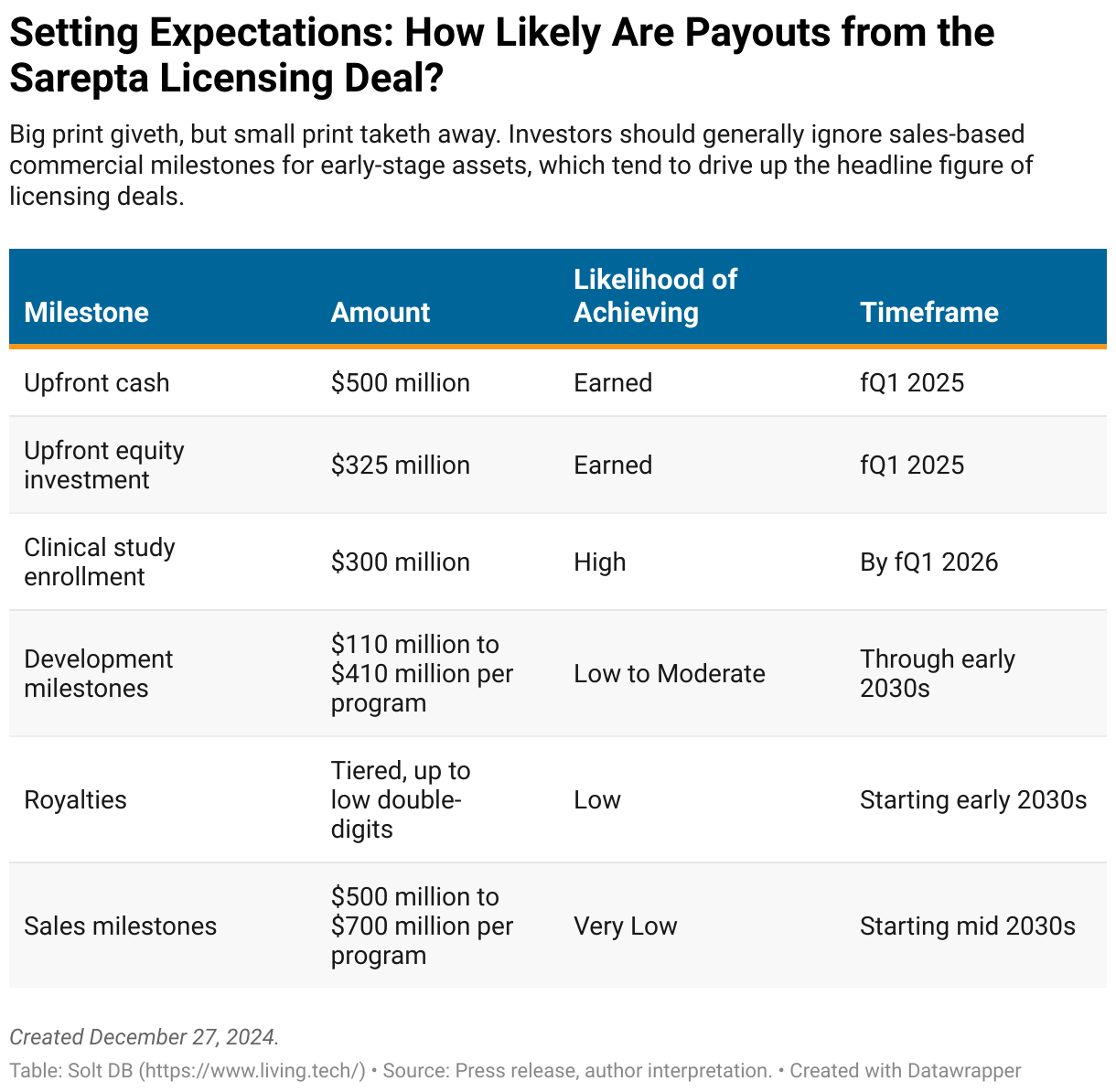

The transaction provides meaningful upfront, near-term, mid-term, and long-term economics. Arrowhead will receive $825 million upfront and can earn an additional $300 million by Thanksgiving 2025 for achieving certain patient enrollment milestones in ongoing clinical trials. That's a healthy $1.125 billion in cash in 12 months – a very significant haul, especially given the current state of corporate capital markets.

Sarepta will commit an additional $250 million total over the next five years ($50 million per year), which will offset expenses incurred for the up to six neuro or muscular target nominations.

In the mid- to long-term, Arrowhead is eligible to receive development milestones of $110 million to $410 million per program. The high probability of success of RNAi assets suggests a meaningful portion of these milestones could be achieved, albeit back-weighted to later stages of clinical development many years from now.

Finally, the company can earn sales milestones of $500 million to $700 million per program, plus low double-digit royalties on sales. Although commercial milestones drive up the headline figures of licensing deals in drug development (this one has "up to $10 billion in total future milestones"), the revenue levels required to trigger payments are almost never achieved. That inconvenient detail, combined with the fact revenue won't be generated for another 7 to 10 years, means investors can and should ignore these figures.

Did Arrowhead give up too much? Does the cash haul matter given its cash burn? Let's jump in and visualize the impact.

Is It Concerning Arrowhead Keeps Selling Off Assets?

The ability to continuously monetize R&D is a strength, not a weakness, of an RNAi platform. Besides, Arrowhead owns full rights to at least seven drug candidates across cardiometabolic, lung, and complement-mediated diseases; plus full rights to additional discovery-stage assets.

Consider how unique it is for a drug developer to reproducibly generate and sell assets across therapeutic areas.

Know-how in single domains is difficult to extend

Most drug developers develop assets in a single therapeutic area, such as liver disease or blood cancers. It's difficult to translate that expertise to completely unrelated areas because the technology stack and know-how is rarely relevant across domains.

RNAi doesn't have that problem because it works at the genetic level. If you can design a short-interfering RNA (siRNA) molecule to disable gene expression, then the therapeutic area is irrelevant. Genetic diseases? Lung diseases? Brain diseases? Cardiometabolic diseases? Have a field day.

Of course, you still need to deliver the payload to the proper tissues in the body to realize the potential, but RNAi drug developers have demonstrated promising progress with next-generation targeting ligands.

Most therapeutic modalities are limited by intellectual property

Similarly, expertise and know-how in many therapeutic modalities doesn't offer extensive intellectual property protection in unique domains. Do you have a kick ass technology platform for developing small molecule tyrosine kinase inhibitors or monoclonal antibodies? Sweet, but so do dozens of other companies.

This forces drug developers to go deep in a single focus area (Revolution Medicines is all-in on pan-RAS inhibitors) or broad in a single therapeutic area (AbCellera generates hundreds of monoclonal antibodies for partners but retains little economics for individual assets).

Depth or breadth can each be valuable, but RNAi platforms don't have to choose. They're not limited by intellectual property. Alnylam Pharmaceuticals, Novo Nordisk, Arrowhead Pharmaceuticals, Wave Life Sciences, and one or two others own substantially all the proprietary ways to design clinically-meaningful siRNA molecules. They invented the ways to modify siRNA structures regardless of therapeutic area, which is unique to this therapeutic modality.

In other words, any drug developer can develop a monoclonal antibody to treat a brain disease. But if you want to treat a brain disease by silencing gene expression using RNAi, then you have to partner with one of a handful of companies. That allows RNAi specialists to extract significant economics for relatively immature assets.

.avif)

More asset sales are coming in 2025

"We are already in a situation where the number of opportunities we're considering far outstrips the number of programs that we can plausibly prosecute." -- Dr. Douglas Fambrough, CEO of Dicerna Pharmaceuticals (May 2021)

Arrowhead isn't done monetizing assets. Why should it be? RNAi platforms are drowning in opportunities.

Depending on the terms of the Sarepta pact, the company could still generate neuro and muscular assets with the intent to outlicense them to new partners. For example, Arrowhead has teased next-generation assets in Huntington's disease (prior-gen ARO-HTT included in Sarepta deal) and Alzheimer's disease.

The company has also teased the development of an emerging eye platform. Coincidentally, these disclosures have been timed with teasing from Krystal Biotech about the potential to package RNAi inside its herpes-simplex virus (HSV) vectors to deliver genetic medicines in eye drops, rather than risky injections.

The lowest-hanging fruit is zodasiran. The phase 3-ready asset was being developed side-by-side with plozasiran in cardiometabolic disorders, but was deprioritized due to the totality of data favoring plozasiran in broader use cases. Don't mistake that for being worthless.

Zodasiran handily outperformed plozasiran on an emerging biomarker: remnant cholesterol. In fact, zodasiran has by far the best clinical data of any global asset in reducing remnant cholesterol, which is increasingly viewed as the key to reducing long-term cardiovascular risks in specific patient populations. The late-stage asset could be valuable to the right drug developer, or perhaps even a newly-formed company based on the asset.

An asset sale is also baked into the recent loan agreement with Sixth Street – more so with a post-Sarepta amendment. In August 2024, Arrowhead snagged $400 million in cash to help pad the balance sheet and support the upcoming commercial launch of plozasiran. Although the loan isn't due until 2029, the company agreed to make prepayments under certain scenarios, including specific percentages of:

- Plozasiran revenue

- Upfront payments related to pipeline monetization transactions

- Zodasiran licensing payments

The RNAi specialist amended the prepayment covenant after the Sarepta licensing transaction, but the details won't be known until the next quarterly report is filed in February 2025. It's unclear if it completely nixed prepayment requirements due from the Sarepta licensing deal or reduced them. Nonetheless, it's plausible the business could repay the loan in full if it sells zodasiran.

Do the Assets Have a High Probability of Success?

The licensed assets target gene expression in three tissue types – muscle, lung, and neuro – that are relatively new for RNAi, which has proven itself by delivering therapeutic payloads to the liver. Each tissue type requires a unique delivery technology, but next-generation tools are broadly referred to as "extrahepatic," meaning "outside the liver."

Extrahepatic delivery tools don't have much clinical data, so it's difficult to say much about the probability of success (POS) of these assets. But the competitive landscape confirms large market opportunities, significant unmet need, and the potential for Arrowhead's delivery platforms to enjoy unique advantages.

Muscle (ARO-DUX4, ARO-DM1)

RNA medicines are uniquely positioned to treat rare muscle diseases.

- Antisense oligonucleotide (ASO) and peptide nucleic acid (PNA) candidates seek to treat disease by repairing or skipping mis-spliced mRNA.

- RNAi candidates seek to treat disease primarily by tagging mutated mRNA for destruction.

Arrowhead's first muscular drug candidates target two diseases with no treatment and debilitating quality of life.

- ARO-DM1 takes aim at myotonic dystrophy type 1 (DM1) by silencing the DMPK gene, which encodes a protein critical for smooth muscle cell structure.

- ARO-DUX4 takes aim at facioscapulohumeral muscular dystrophy type 1 (FSHD1) by silencing the DUX4 gene, which is usually inactive in healthy adults.

The average age of death for individuals with DM1 is 48 years old, while individuals with FSHD1 are often required to use a wheelchair within 20 years of diagnosis. Given the seriousness of these specific diseases and the importance of the genes involved, an ideal treatment would correct the mutated gene or correct a meaningful level of mis-spliced mRNA. RNAi candidates don't check both boxes, but they could greatly improve quality of life and buy time for functional cures to be developed.

Investors already have proof-of-concept for RNAi candidates in both DM1 and FSHD1 courtesy of Avidity Biosciences. Partially due to the restrictive IP landscape, the company has taken a unique approach to deliver RNAi payloads to muscle cells: it links siRNA molecules to an antibody. These antibody oligonucleotide conjugates (AOC) have demonstrated encouraging phase 1/2 results. In fact, del-desiran has earned FDA Breakthrough Therapy designation.

But AOCs have drawbacks. Antibodies are relatively large, which can limit potency. Less potency means they also require relatively high doses, which can cause more side effects and reduce efficacy over time, especially if antibodies are neutralized by the immune system. Importantly, Avidity Biosciences delivers cargo by targeting the transferrin receptor on muscle cells, which can muck up iron uptake and transport ("transferrin" is Latin for "across" and "iron").

Arrowhead took advantage of its favorable IP position to engineer siRNA-peptide conjugates, rather than siRNA-antibody conjugates. That enables ARO-DUX4 to deliver its payload via integrin receptors on muscle cells, rather than transferrin receptors. Chemistry modifications improved stability and persistence, allowing lower doses to be much more potent.

The company conducted head-to-head preclinical testing to gauge its competitive positioning before advancing to the clinic.

- In non-human primates, Arrowhead found AOCs reduced DUX4 expression by roughly 50% (exactly what Avidity Biosciences has observed in clinical trials).

- The company's unique siRNA-peptide conjugates reduced DUX4 expression by over 80% for over three months.

- Avidity Biosciences administers del-desiran every two months, while Arrowhead is targeting a quarterly dosing schedule.

That bodes well for competitive positioning and earning milestones from Sarepta in the next few years.

Neuro (ARO-ATXN1, ARO-ATXN2, ARO-ATXN3, ARO-HTT)

There's much less information available to weigh the competitive dynamics in RNAi assets delivered to the central nervous system.

The current crop of assets licensed to Sarepta Therapeutics all utilize intrathecal (IT) administration, meaning injected into a space between the spine and spinal cord, which allows a therapeutic to enter the cerebrospinal fluid that surrounds the brain. It's not the most convenient route. An ideal neuro drug would be administered intravenously (IV) or subcutaneously (SC, "a simple shot") and cross the blood-brain barrier. But patients have no treatment options, and twice-yearly or once-yearly dosing is possible.

Arrowhead is developing a next-generation siRNA-peptide conjugate platform that can deliver RNAi across the blood-brain barrier with SC administration. In fact, it appears to be better at penetrating deep brain regions, which makes sense considering IT administration is "limited" to the cerebrospinal fluid. In other words, it could be more convenient, more effective, and safer than current-generation assets.

It's unclear if the up to six (6) preclinical assets included in the Sarepta deal include the next-generation platform, but I think that's a safe assumption. Imagine if we could treat debilitating diseases like Huntington's or Alzheimer's at the genetic level with a simple shot four times a year. Investors will likely see preliminary data in humans before the end of the decade.

Lung (ARO-MMP7)

A genetic medicine for idiopathic pulmonary fibrosis (IPF) will need to clear the high bar set by existing and emerging assets in the global industry pipeline. There are generic drugs available (pirfenidone, the active pharmaceutical ingredient in Roche's Esbriet) and Boehringer Ingelheim's Ofev. Meanwhile, United Therapeutics expects topline results for its pivotal TETON studies, which are evaluating its blockbuster product Tyvaso in the new indication.

It might seem a bit odd Sarepta Therapeutics is interested in this singular lung program considering the company's focus is on neuromuscular disorders, but IPF is technically a musculoskeletal disease.

Forecast & Modeling Insights

(Increased.)

The updated model is based on the estimated fair value of Arrowhead Pharmaceuticals in the next 12 months. The valuation remains the same, but reduced expectations for dilution increase the estimated fair value on a per-share basis. A longer cash runway also de-risks an investment, which increases the suggested allocation range to up to 15%.

A summary of changes to the forecast and model for Arrowhead Pharmaceuticals:

- Valuation (Market Cap): The assets included in the Sarepta licensing deal weren't included in the prior model. Arrowhead continues to have an estimated fair valuation of $4.658 billion.

- Valuation (Per Share): The prior model assumed share dilution of 15%, or 143.096 million shares outstanding by the end of calendar 2025. The updated model reduces expectations for dilution to 1% by the end of calendar 2025. After including the Sarepta equity investment, the updated model assumes 137.615 million shares outstanding.

- Allocation Range: Although the model doesn't materially change, a solidified cash runway into 2028 significantly reduces the risk of investing in Arrowhead Pharmaceuticals, especially with shares now trading near pre-announcement levels. The allocation range has been increased to up to 15%.

The most significant events that will impact the model remain the same:

- Plozasiran approval (regulatory), launch and ramp (commercialization), and competitive dynamics against Ionis Pharmaceuticals' Tryngolza (approved in familial chylomicronemia (FCS) on December 19, 2024).

- Maturation of wholly-owned programs, including advancing ARO-RAGE (inflammatory lung diseases like asthma) into phase 2 studies and complement-mediated disease assets ARO-C3 and ARO-CFB into phase 1b. Mid-stage assets will contribute to my model.

- Preliminary phase 3 data readouts for olpasiran in treating cardiovascular disease. The study is expected to be completed by the end of 2026.

- Preliminary phase 3 data readouts for fazirsiran (Takeda and Arrowhead) in alpha-1 antitrypsin (A1AT) liver disease. There are three phase 3 studies ongoing. The first is an open-label study with a follow up period of 2.5 years, which is expected to be completed in 2H 2026. The second is in patients with low fibrosis scores, which is expected to be completed in 2H 2028. The third is in patients with moderate to severe fibrosis scores, which is expected to be completed in 1H 2029. Full data from the phase 1/2 study is expected in mid-2025.

- Preliminary data readouts from the SHASTA studies, which are phase 3 clinical trials evaluating plozasiran in severe hypertriglyceridemia. SHASTA-3 and SHASTA-4 are expected to be completed by late 2026, with supplemental approvals possible by late 2027. An upcoming SHASTA-5 study will evaluate plozasiran's ability to reduce acute pancreatitis in patients with severe hypertriglyceridemia, an important label expansion opportunity.

- Preliminary data readouts from the CAPITAN study, which is the phase 3 clinical trial evaluating plozasiran in cardiovascular disease. The CAPITAN study is one of the most important long-term de-risking events for Arrowhead, but will not be completed until 2030 or later (my estimate).

Margin of Safety & Allocation

Arrowhead Pharmaceuticals is considered a Growth (Quality) position. The current modeled fair valuation for the company based on my current model is below:

- Market close December 26: $19.53 per share

- Modeled Fair Valuation: $32.56 per share

- Allocation Range: Up to 15%

Arrowhead Pharmaceuticals reported 124.434 million shares outstanding as of November 20, 2024. The modeled fair valuation above assumes 137.615 million shares outstanding, which accounts for the Sarepta equity investment ($325 million invested at roughly $27.50 per share) and an additional 1% dilution.

Further Reading

- December 2024 press release announcing the Sarepta licensing deal

- December 2024 regulatory filing (10-K) detailing fiscal full-year 2024 operating results

- May 2024 research note analyzing the high R&D costs of Arrowhead Pharmaceuticals

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)