.svg)

.svg)

Business is simple, but not easy. Get customers, make them happy, and ensure as many of them as possible keep coming back.

It's all those fickle humans – customers, vendors, employees, and that micromanaging asshole who just became your boss – that make business so difficult.

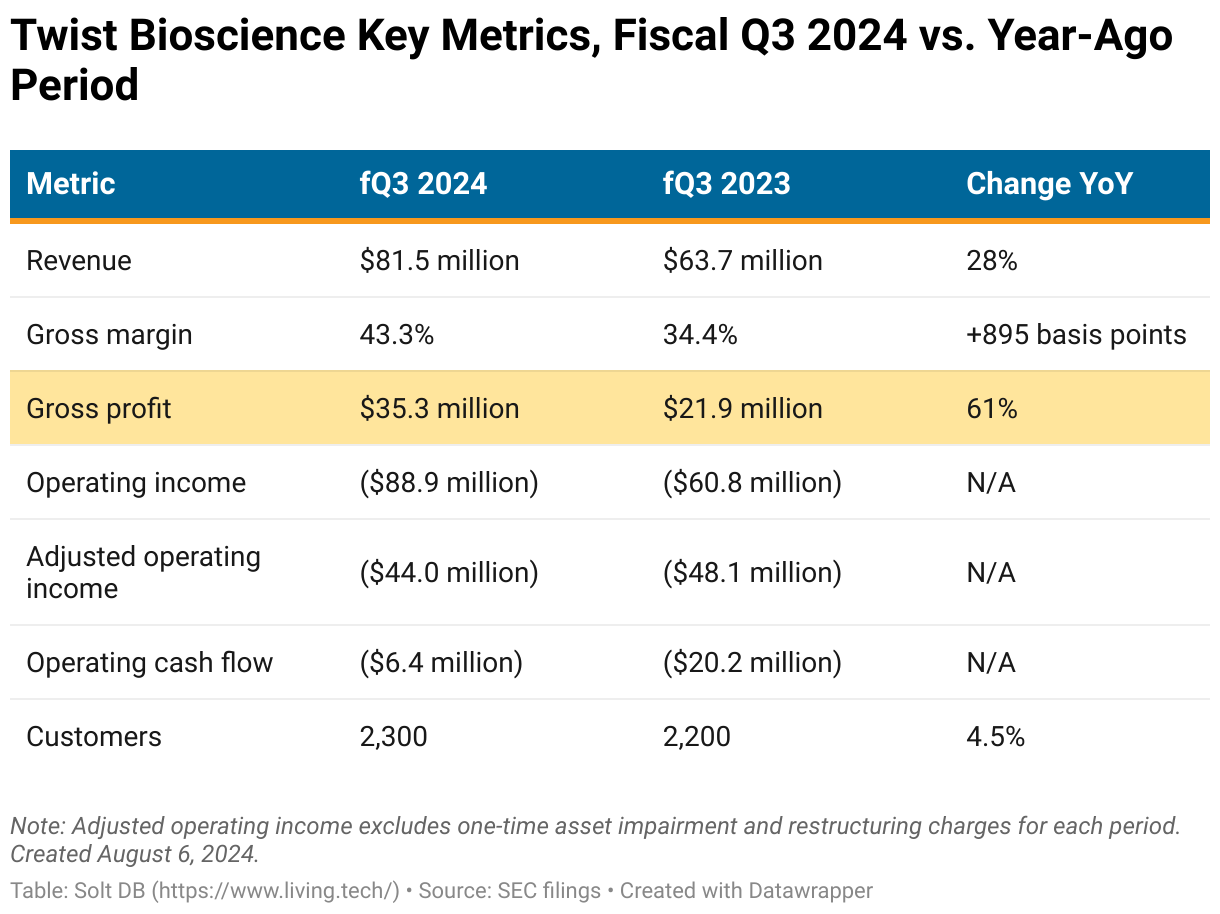

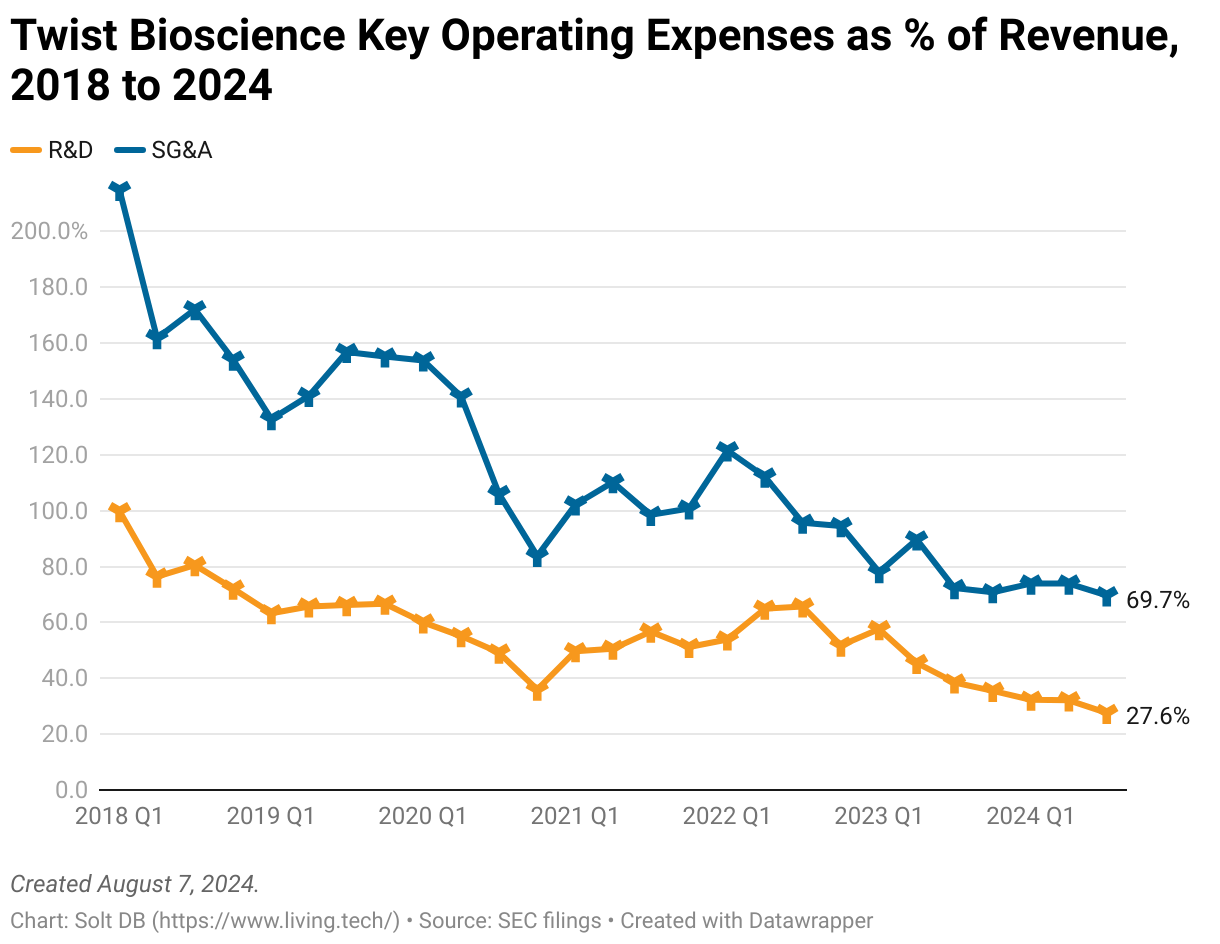

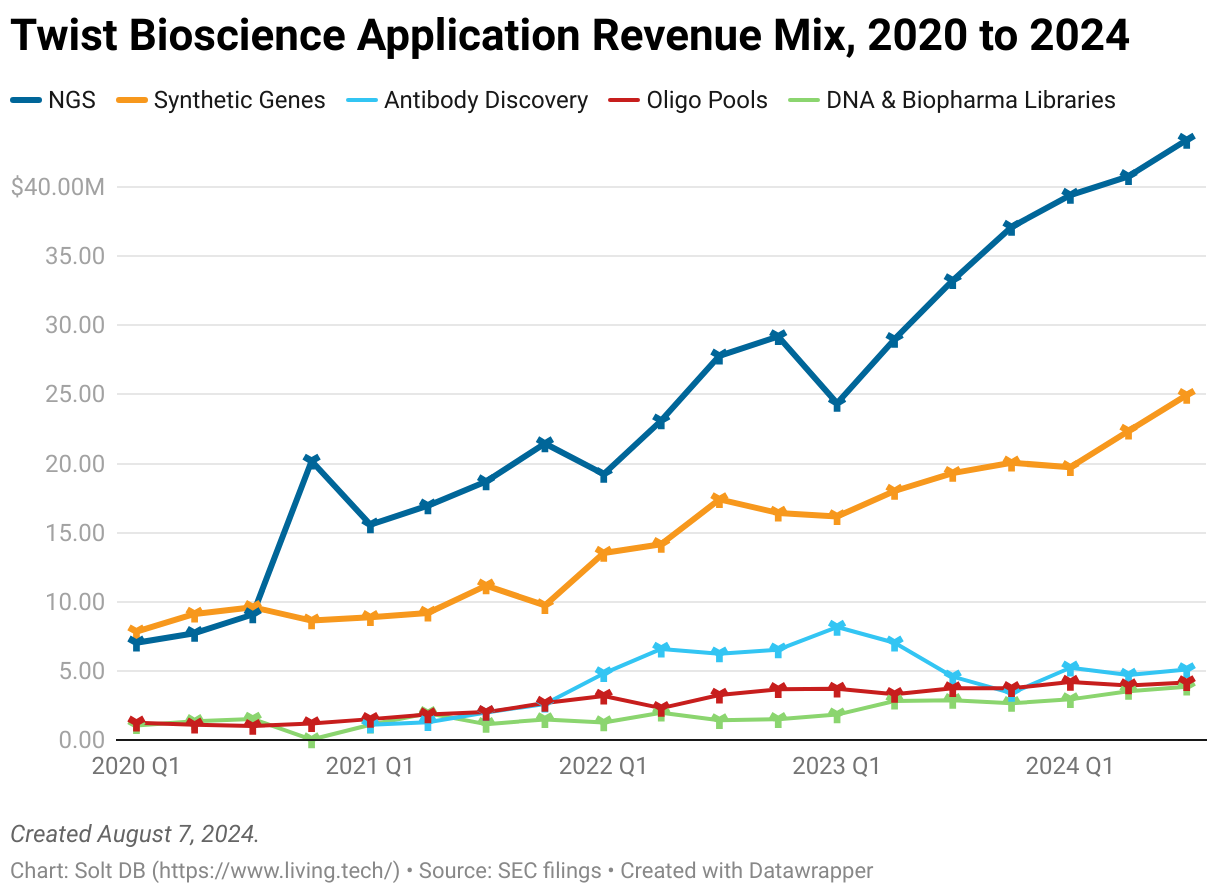

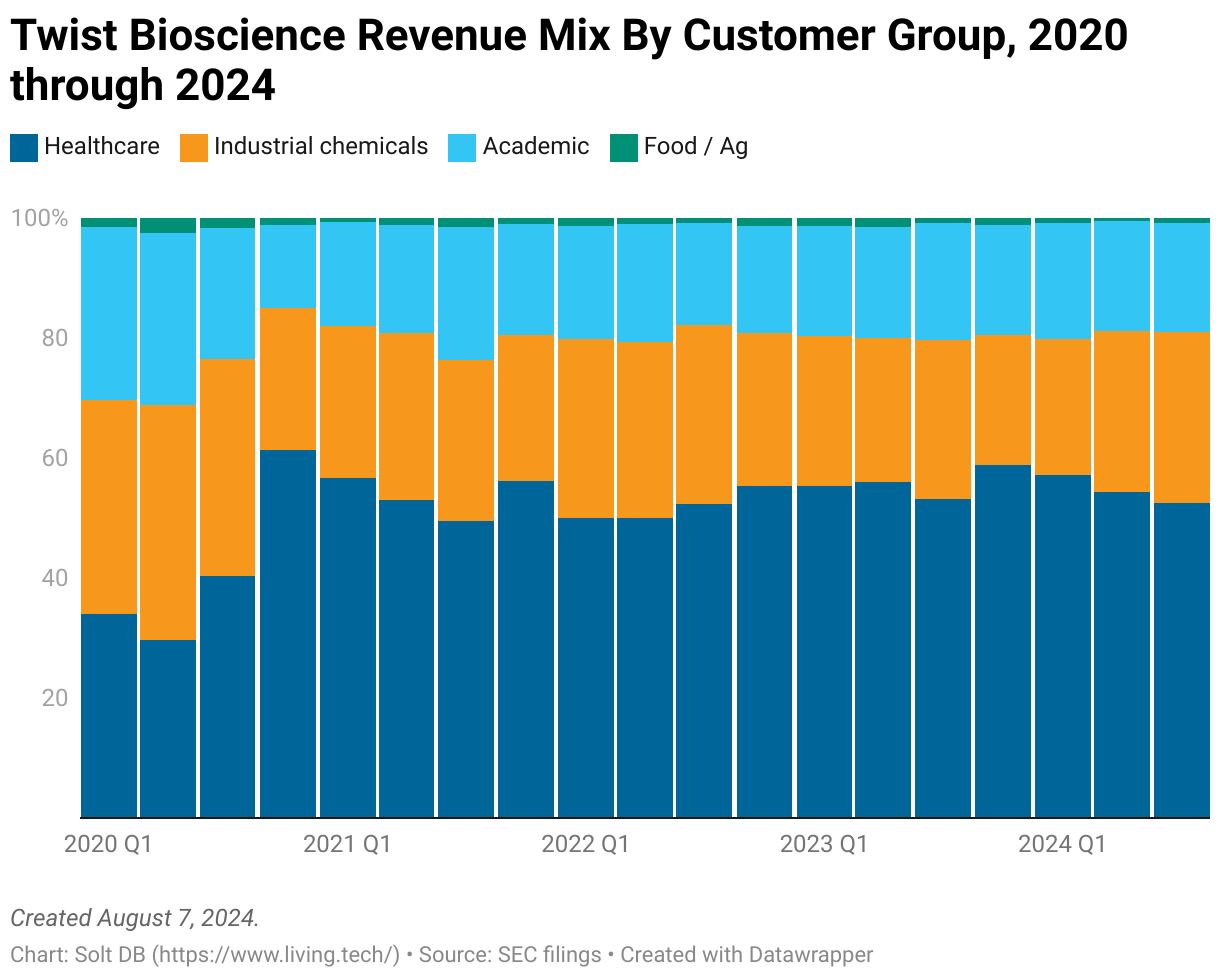

Twist Bioscience is doing an excellent job navigating financial markets, an increasingly competitive landscape, and making customers happy. The business is becoming more efficient (more revenue and fewer costs) and more diverse (more product offerings in disparate applications and industries). It's well positioned from a geopolitical perspective, too, with over 60% of revenue generated from the United States.

If investors wanted to nitpick, then the valuation is an easy place to start. Investors are forced to pay for future growth stretching years into the future, which introduces a valuation premium that can quickly unwind.

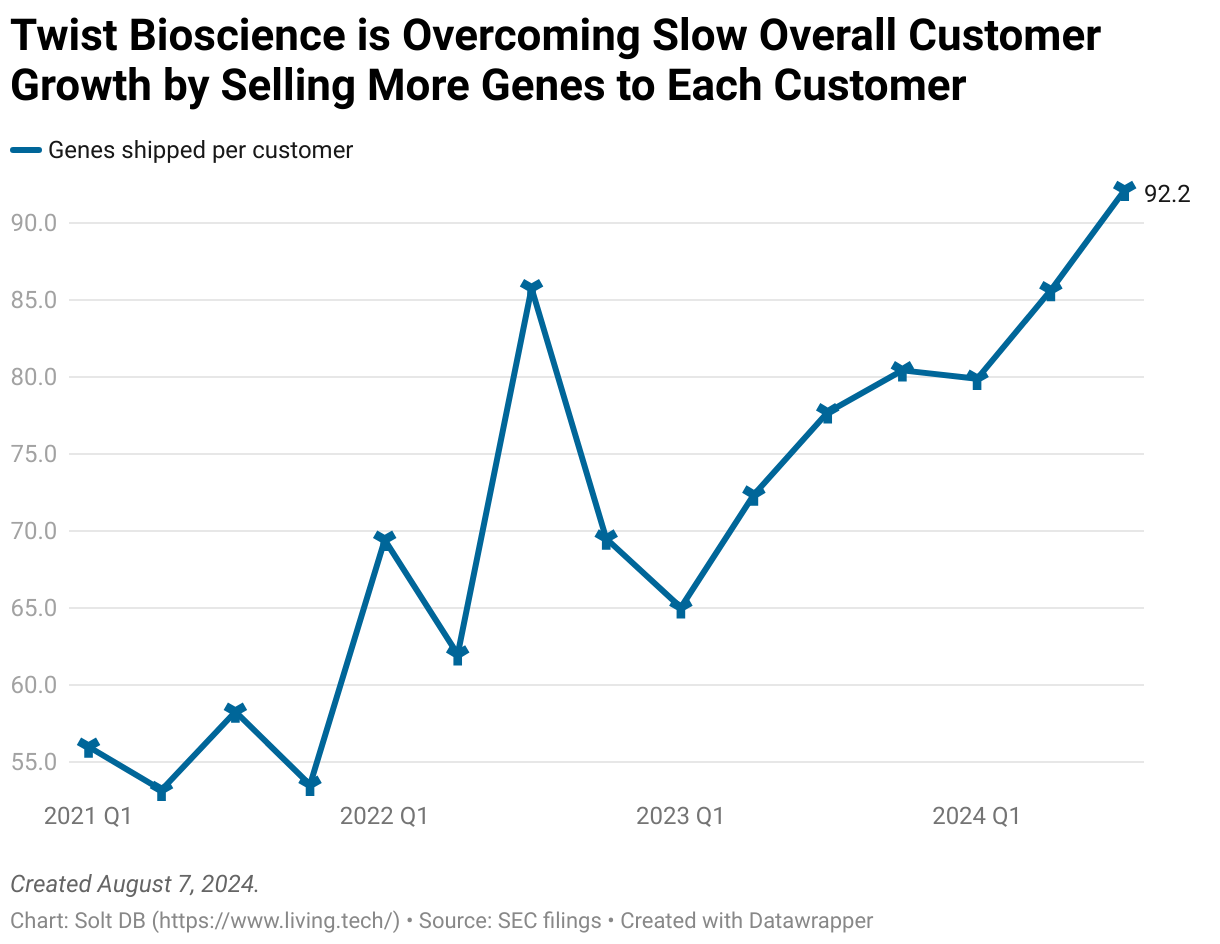

Dig a little deeper and the DNA synthesis pioneer is struggling to grow its customer base. That makes me a little uneasy given the competitive dynamics, especially considering DNA synthesis can become significantly cheaper – and many companies are trying. How many customers would flee if a competitor offered similar quality at lower prices?

For now, at least, shipment data suggest existing customers are becoming increasingly comfortable leveraging the platform. Twist Bioscience shipped 92 genes per customer during fiscal Q3 2024, up from an average of 55 throughout fiscal 2021.

That's just one of a handful of favorable long-term trends, which bodes well for the business heading into fiscal 2025.

.svg)

-cropped.svg)