By the numbers

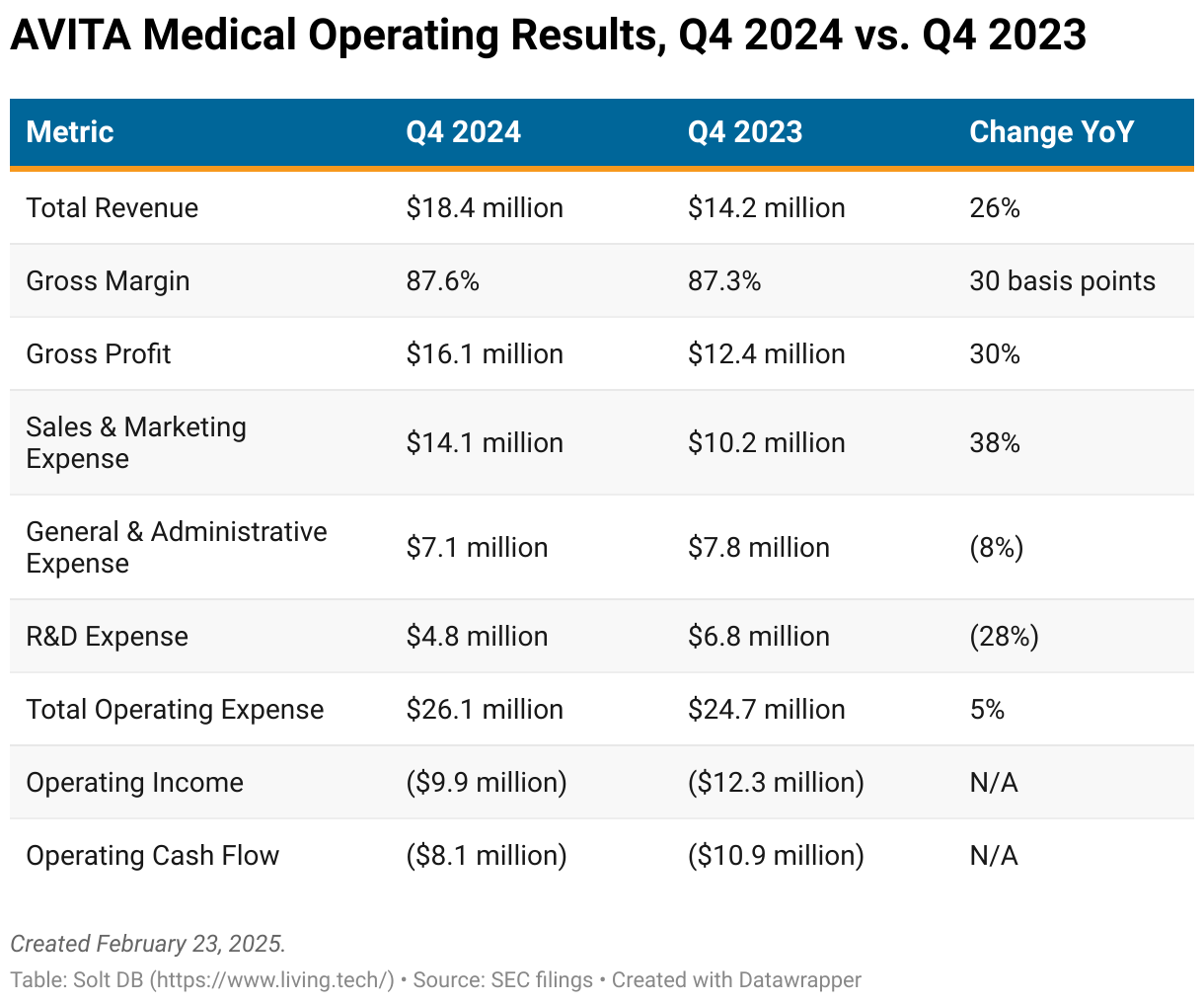

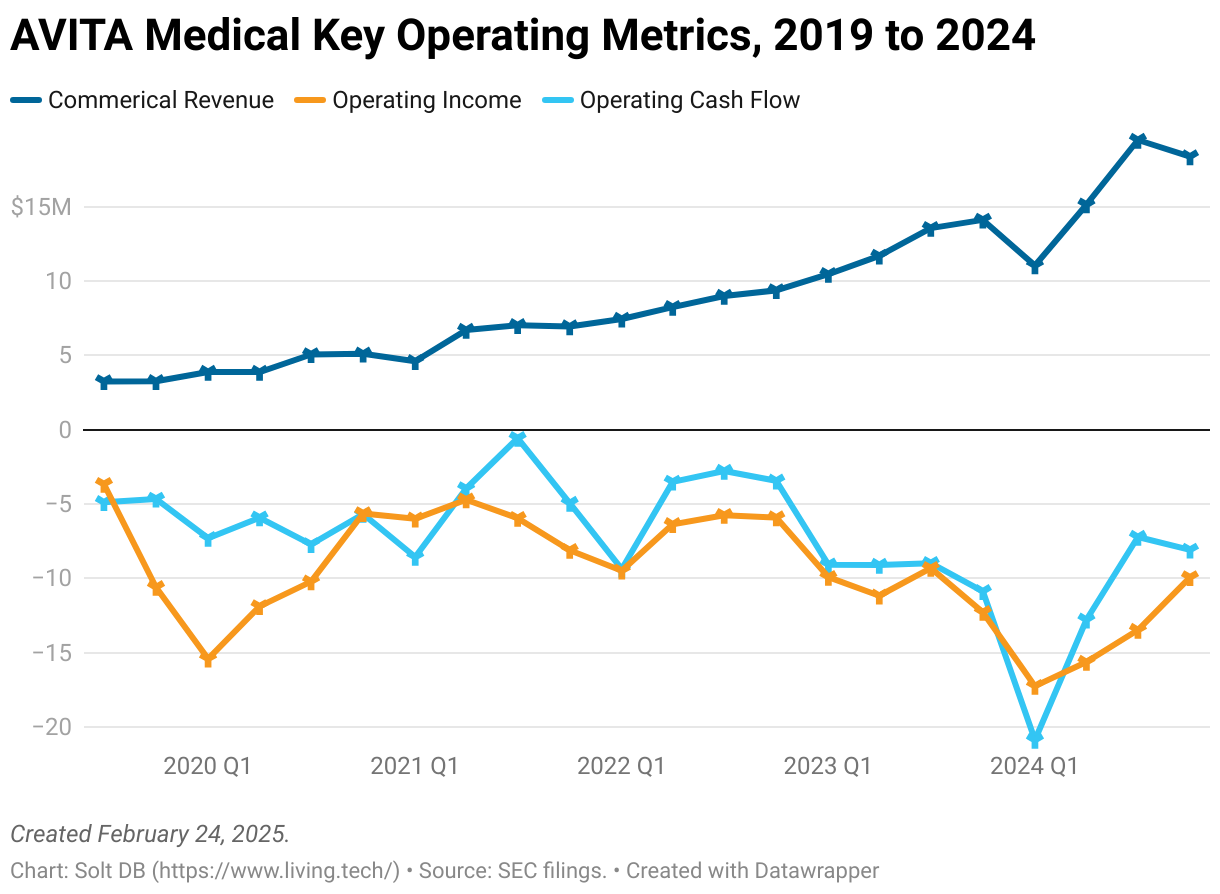

The wound-care specialist originally expected to achieve fourth-quarter 2024 revenue of $23.3 million at the midpoint. It ended up achieving just $18.4 million, which missed by 21%. The embarrassing performance was compounded by even simpler math: the business generated less revenue than the prior quarter. Again.

Not very "high-growth mode," eh?

Whiffing on revenue guidance for the second time in four quarters shouldn't be dismissed easily. Although the provided reasons are plausible, if it happens again, then investors will need to question why this management team is fit for the job.

It wasn't all bad news.

For the full year, AVITA Medical still achieved year-over-year revenue growth of 29% in 2024. That's strong. It only seems disappointing because management set expectations even higher.

The business demonstrated solid fiscal restraint during the fourth quarter, which could help create much-needed momentum in 2025. Total operating expenses of $26.1 million in Q4 were the lowest of 2024 and 18% lower than my model. Gross profit margin of 87.6% easily trounced my modeled value of roughly 80%, although the outperformance was driven by slower-than-expected traction for non-ReCell products, which have lower margins.

Higher margins and lower expenses are always a sweet combination. AVITA Medical's Q4 2024 operating loss of $9.9 million was 42% better than my model's expected outcome. If the business can keep it up – and delivers the promised growth trajectory – then it should turn cash flow positive in 2025.

Management expects to achieve full-year 2025 revenue of $103 million at the midpoint, free cash flow in the second half of the year, and GAAP profitability in the fourth quarter of the year. In a sign the team is learning from recent mistakes, it did not provide quarterly revenue guidance for Q1 2025.

New Launches Promise Growth, but Recent Launches Contribute Little

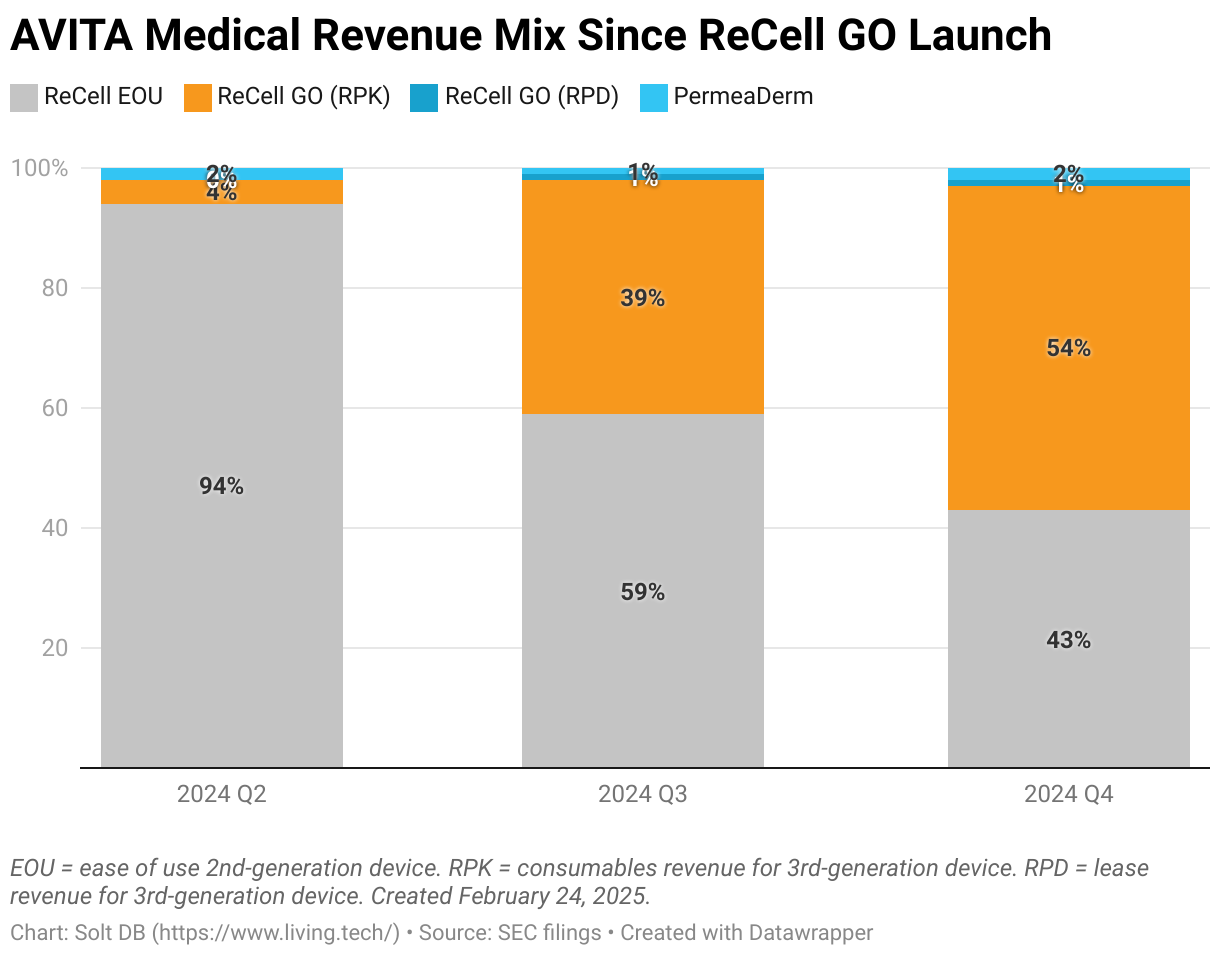

AVITA Medical has furiously added new products and geographic territories to fuel its growth push. But aside from ReCell GO and the United States, these efforts are contributing surprisingly little revenue.

The second-generation ReCell device, called "ease of use" (EOU), generated 43% of total Q4 2024 revenue. It will be phased out this year. The third-generation device, called ReCell GO, generated 54% of total revenue during the period. The transition to new devices is progressing as expected.

However, total revenue generated from ReCell devices stood at 97% in the final quarter of 2024. The branded wound dressing PermeaDerm – the first product brought in to capture more value from the full wound care spectrum– was responsible for just 2%.

Make no mistake: ReCell GO will be the dominant source of revenue for the rest of the decade. But investors want to see new products gain traction more quickly to provide meaningful diversification.

Consider a typical burn or wound covering 10% total body surface area (TBSA). PermeaDerm will generate an estimated $2,000 in revenue per patient procedure. That's less than the $6,500 for ReCell GO, and wound dressings aren't applied during every procedure, but PermeaDerm should be more than 2% of total revenue.

A slow start for the new dermal matrix product Cohealyx would be more challenging to overcome. Whereas PermeaDerm protects the surface of a treated wound and ReCell aims to replace the skin just below the dressing, dermal matrix products provide structural support for cells during the healing process. Cohealyx would be placed into a wound bed first, then skin cells from ReCell GO would be applied, and finally PermeaDerm on top.

For the same burn or wound procedure treating 10% TBSA, Cohealyx could generate $20,000 in revenue. It won't be used in every procedure, but it represents a meaningful opportunity to capture more value from each procedure. AVITA Medical's ambitions don't end with PermeaDerm or Cohealyx. Management is also exploring adding products to aid wound depth assessment, antimicrobials for protecting the wound bed, aiding blood clotting in the wound bed, and scar reduction.

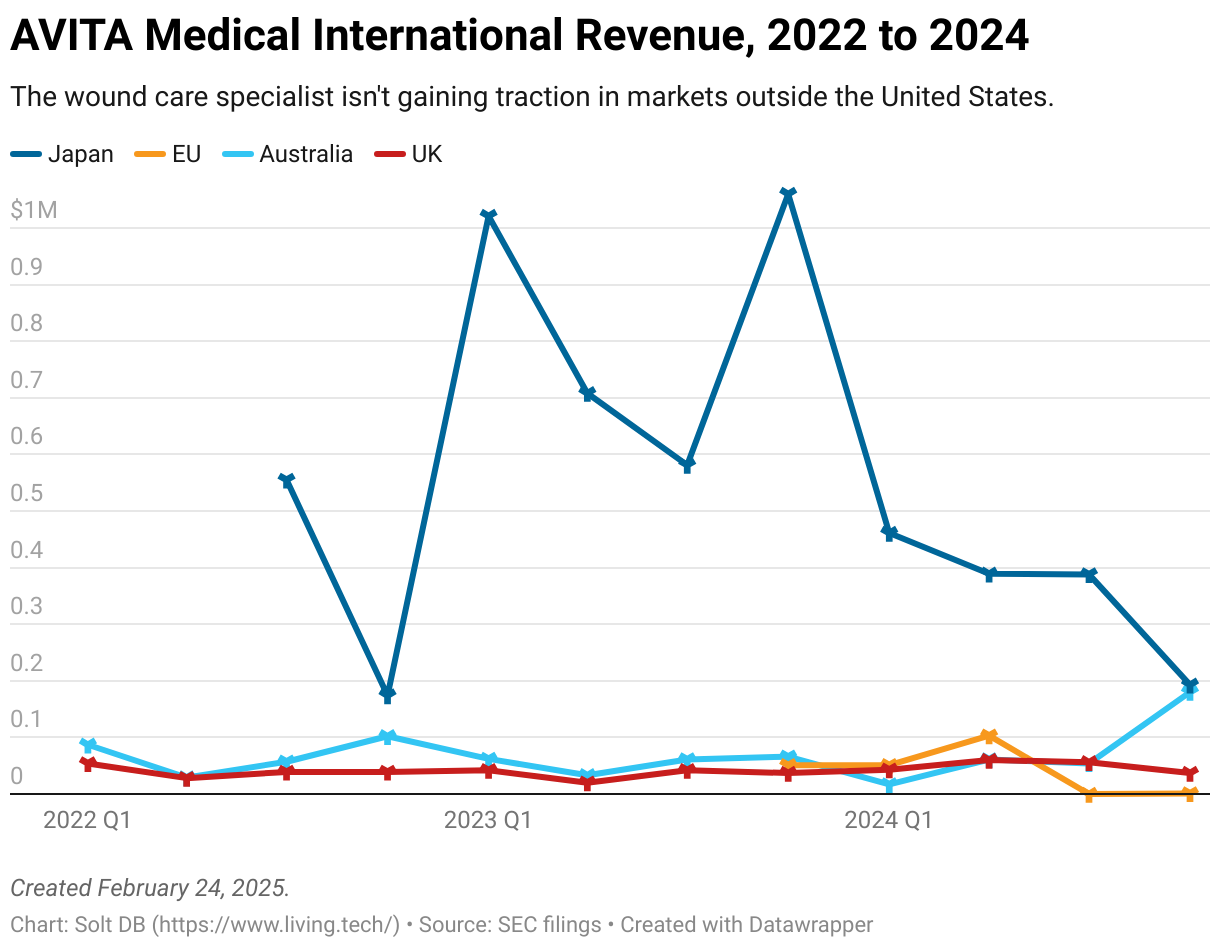

In addition to sluggish launches from new products, the company's international expansion into Japan and Europe isn't bearing fruit. AVITA Medical generated its second-worst quarterly revenue in Japan since launching 10 quarters ago and generated just $1,000 in Europe in the entire second half of 2024.

Forecast & Modeling Insights

Only Solt DB members have access to this information.

Margin of Safety & Allocation

Only Solt DB members have access to this information.

.svg)

.svg)

.svg)

-cropped.svg)