Krystal Biotech's R&D Spending, Visualized

To highlight the company's abnormally low R&D investments, it helps to compare it to the rest of the coverage ecosystem. This includes comparisons with precommercial drug developers, as well as commercial drug developers with similar levels of revenue.

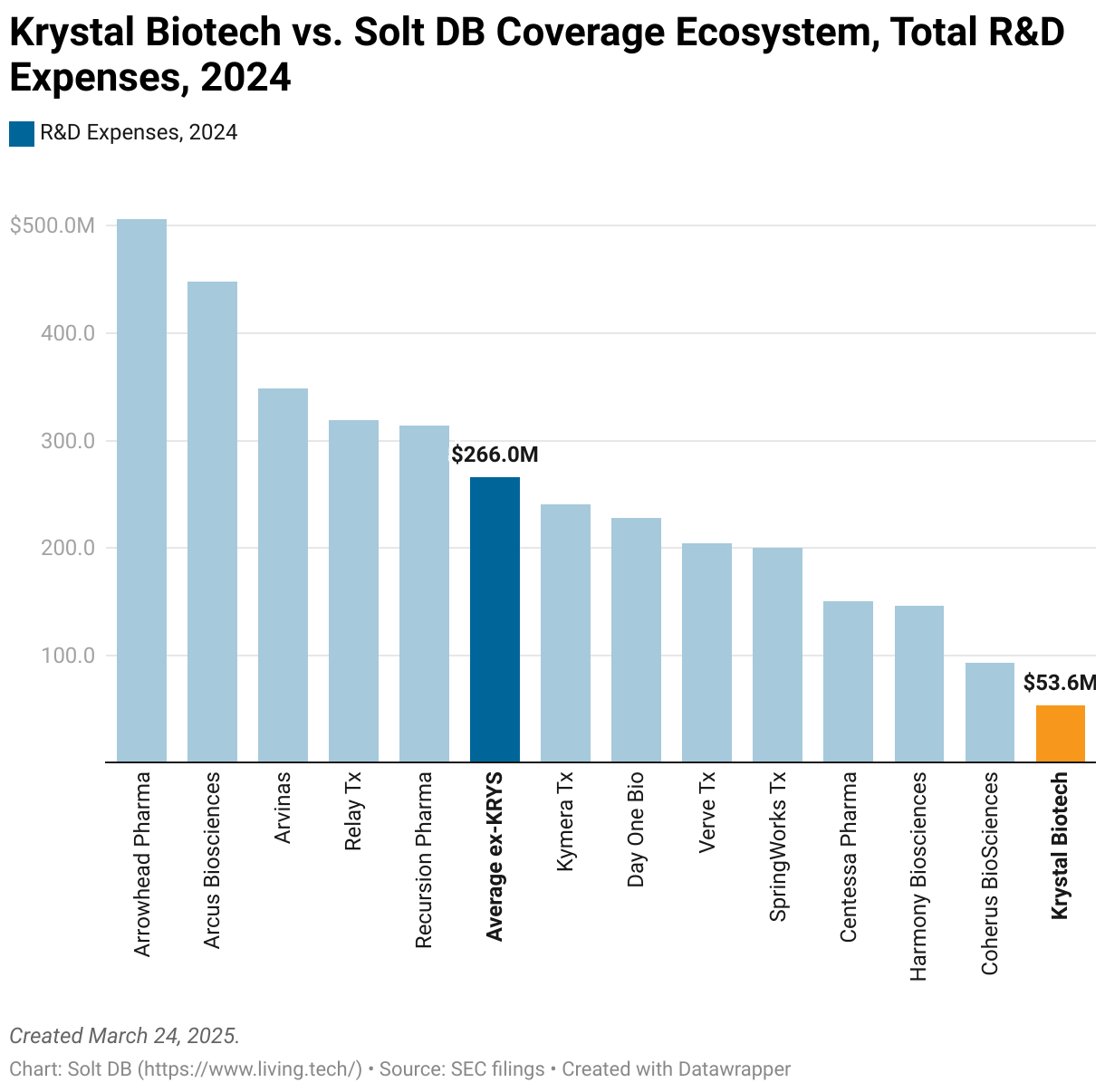

Krystal Biotech reported total R&D expenses of just $53.6 million in 2024. Only Coherus BioSciences spent less than $100 million last year, primarily because it was preparing its acquired pipeline for clinical starts in 2025.

Fellow commercial-stage drug developer SpringWorks Therapeutics spends that every four months. Relay Therapeutics invests that every quarter. It invested $92 million in clinical trials last year, which are just one component of R&D expenses and supported just two assets.

Harmony Biosciences, which doesn't even wield a congruent technology platform, spent 3x more than Krystal Biotech last year. Blueprint Medicines – which has the same level of revenue as Krystal Biotech – allocates roughly $50 million for nerds in lab coats on its payroll every two months.

Meanwhile, Arrowhead Pharmaceuticals spends roughly $50 million on R&D expenses every month. The RNAi specialist spent heavily to prepare assets for out licensing, culminating in a deal with Sarepta Therapeutics that will allow it to recoup $1.125 billion in the first year.

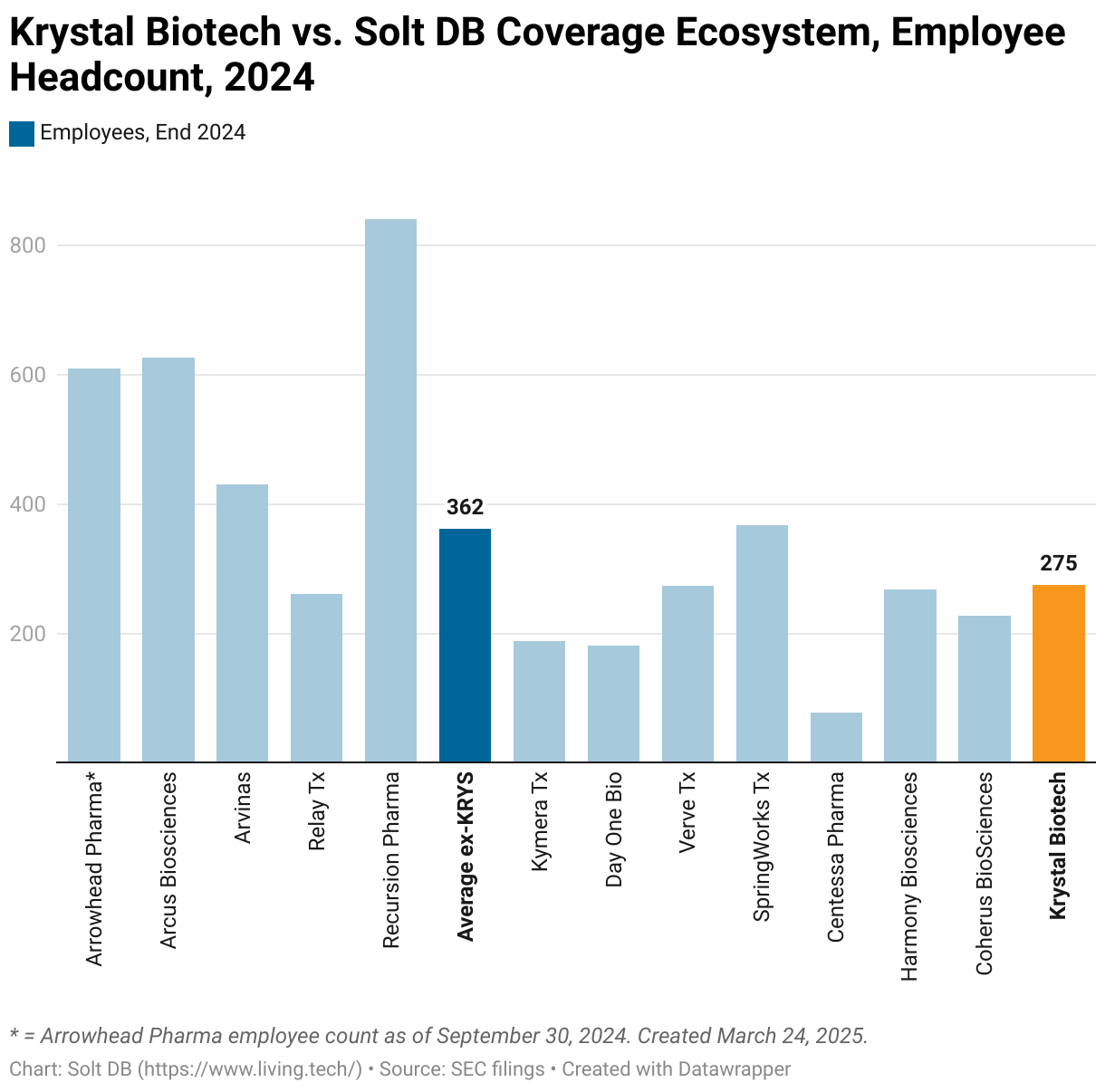

Krystal Biotech's unusually low R&D spending isn't a function of a small team size. The company entered 2025 with 275 full-time employees. That's exactly the median of the coverage ecosystem's drug developers. It's less than the average of 362 employees excluding Pittsburgh's premier gene therapy company, but far from the smallest team.

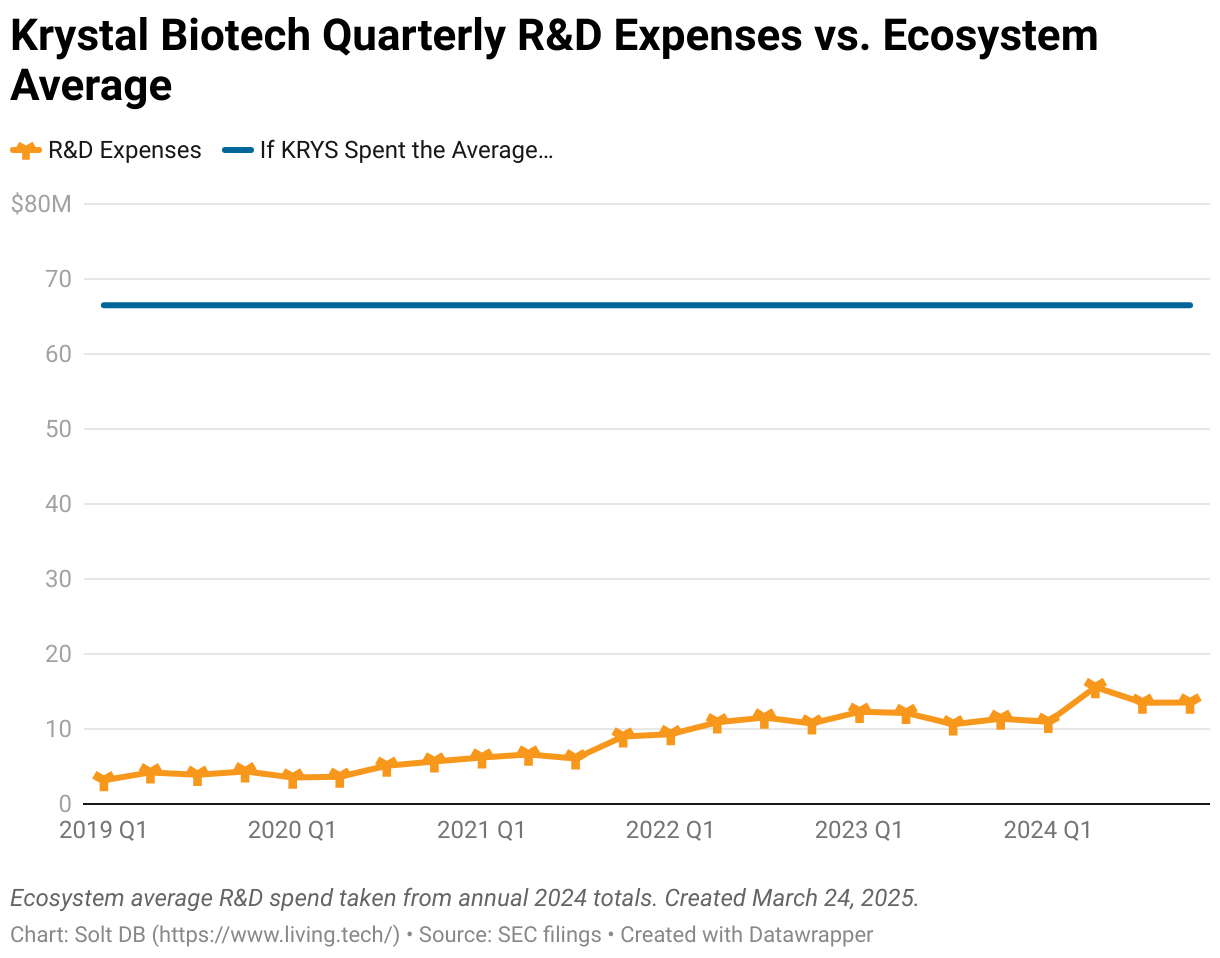

If Krystal Biotech invested the average R&D expenses of the coverage ecosystem, then it would spend $66.5 million per quarter and $266 million per year. That would increase annual research expenses by $212 million, plus additional costs for a larger team, more vendors, and so on.

Considering the business reported full-year 2024 earnings before income taxes (EBIT) of $95 million and operating cash flow of $123 million, a normal level of investment in the technology platform and pipeline would result in an unprofitable and cash-burning business.

Investors Can Expect Increased R&D Spending Ahead

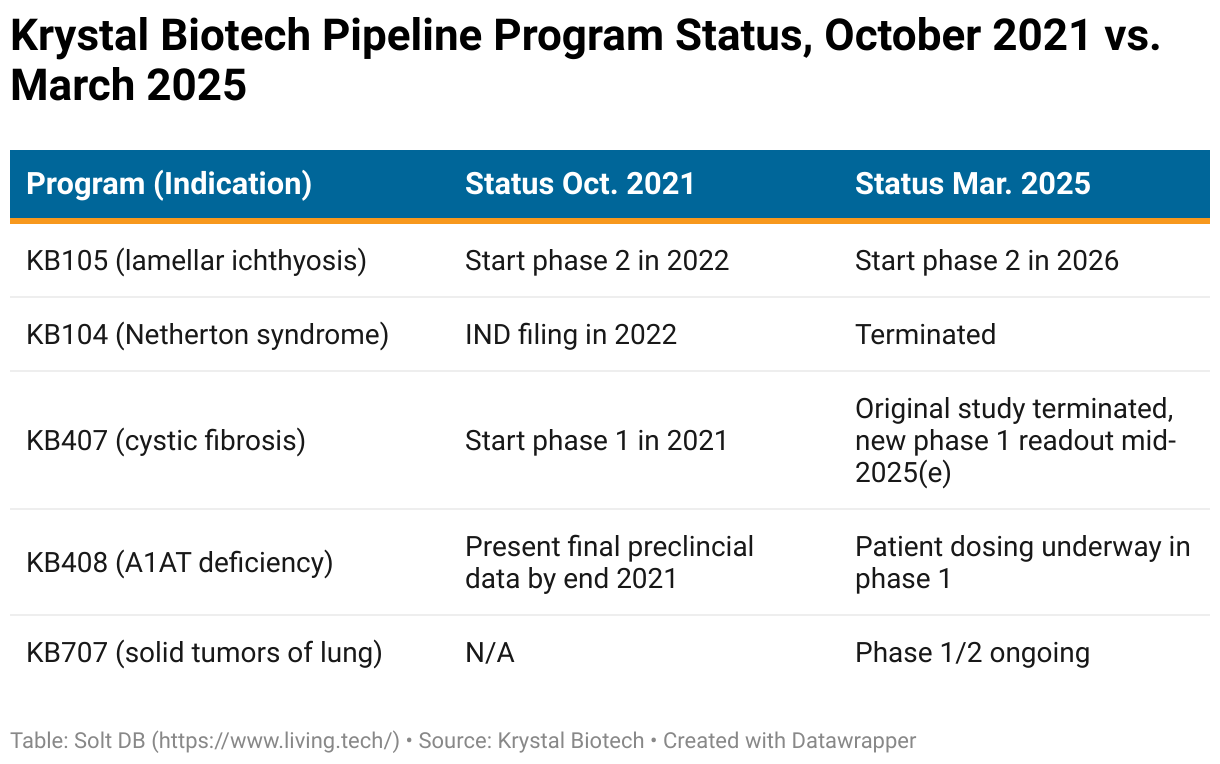

The risks of chronically low R&D spending can be severe. Investors should be careful not to extrapolate Vyjuvek's development to the remaining pipeline. The asset benefitted from a unique combination of characteristics that led to the ridiculously efficient development, but those conditions will be impossible to replicate for core pipeline programs now making their way through clinical trials.

The asset enrolled only 30 patients in its pivotal study. That's possible when targeting a rare disease like dystrophic epidermolysis bullosa (DEB) with no competing treatment options or development candidates, but it won't work for larger indications in the pipeline such as alpha-1 antitrypsin (A1AT) deficiency, cystic fibrosis, or lung cancer. Krystal Biotech simply cannot continue as an independent company without significantly higher R&D investments.

Consider how little the pipeline has advanced in the last three-and-a-half years.

To be fair, portfolio optimization isn't a bad thing. Investors want to see mindful investments rather than reckless spending with no payoff, which many drug developers continue to do (for some reason…). Many drug developers wish they were in a similar position to control their own destiny. The gene therapy specialist can fund itself and go as fast or slow as it wants with pipeline programs.

But Krystal Biotech is really pushing the limits of operational efficiency. As pipeline programs advance it'll need to significantly increase investment.

The phase 1 study of KB407 in cystic fibrosis is enrolling only 12 patients, same as the phase 1 study of KB408 in A1AT deficiency. By contrast, the phase 3 studies for fazirsiran in A1AT deficiency being conducted by Takeda Pharmaceuticals and Arrowhead Pharmaceuticals will enroll over 250 patients.

Meanwhile, the phase 1/2 program for KB707 in lung tumors is designed to enroll 240 patients – several times more patients than the company has enrolled in clinical trials across its entire pipeline since it was founded. As the asset advances to the phase 2 portion, investors can expect a significant increase in R&D expenses.

The strange thing is the business ended 2024 with $750 million in cash. That should provide a comfortable runway even under scenarios where it invests a "normal" amount in research each quarter.

Forecast & Modeling Insights

Only Solt DB members have access to this information.

Margin of Safety & Allocation

Only Solt DB members have access to this information.

.svg)

.svg)

.svg)

-cropped.svg)