By the Numbers

Twist Bioscience is objectively heading in the right direction.

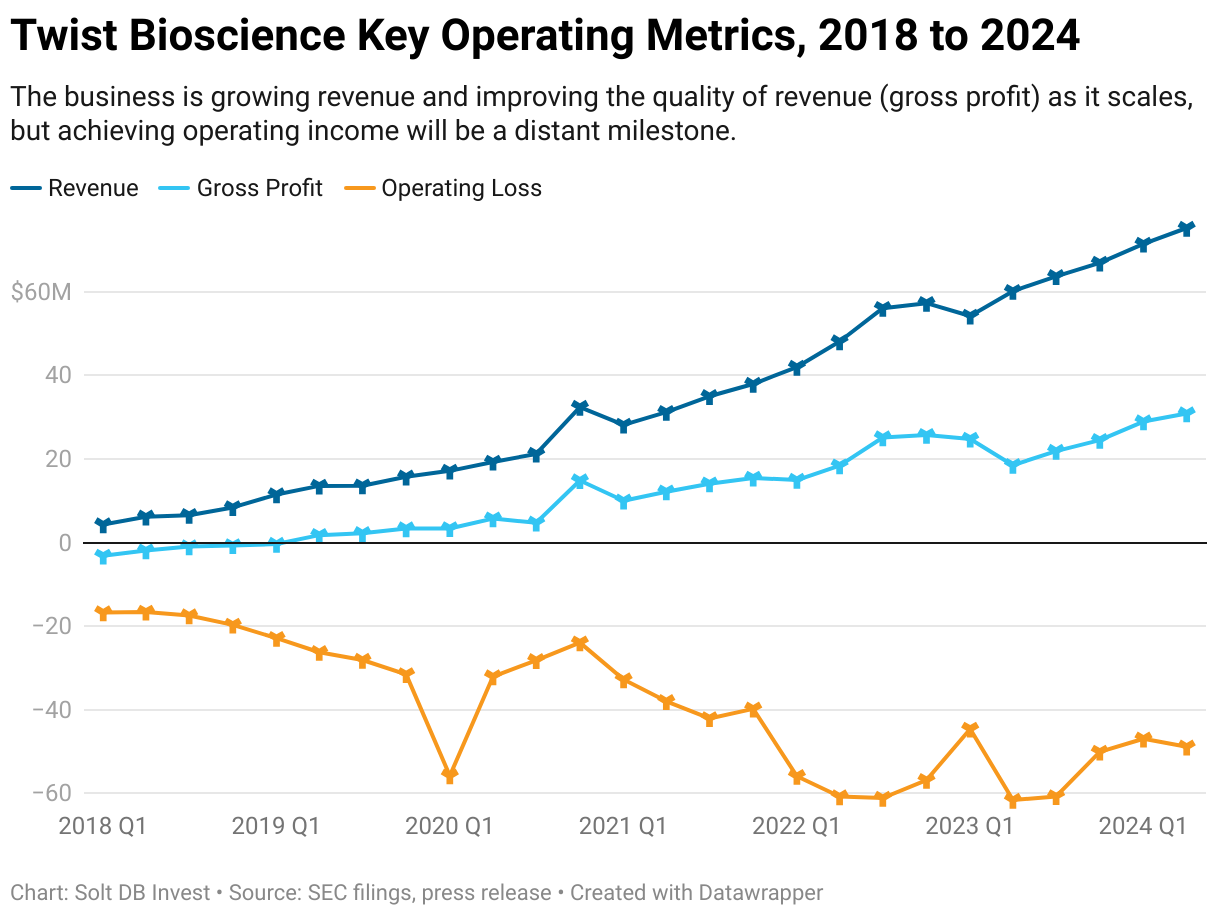

Revenue is growing at a healthy clip, gross margin is slowly improving, and operating expenses are growing at a manageable pace (although the business has a somewhat bloated level of overhead). A favorable trend for those key operating metrics is also driving a swift improvement in operating cash outflow, which was 58% lower in the first half of fiscal 2024 compared to the year-ago period.

The business has had a stable geographic revenue mix since mid-2022. It still generates about 60% of revenue from the Americas, 30% from Europe and Middle East, and the remaining 10% from Asia. The geopolitical forces sweeping through the global economy will have an especially acute impact on the bioeconomy, but Twist Bioscience isn't too exposed – the higher the reliance on U.S. customers, the better.

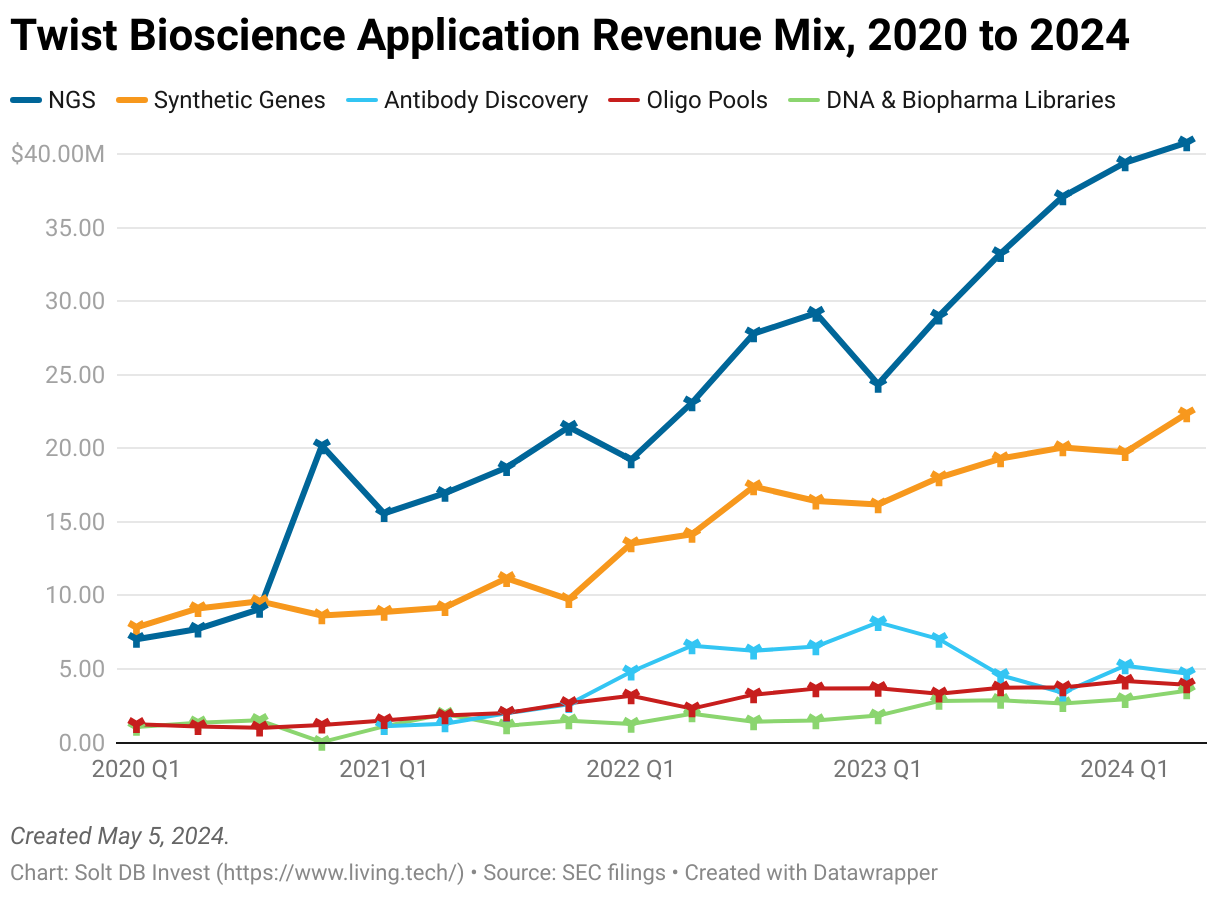

It's interesting to me that the application revenue mix and customer revenue mix have been stable in the span, too. The business generates about 55% of revenue from next-generation sequencing (NGS) applications, 30% from synthetic genes, and the remaining 15% from a hodgepodge of nerdy applications. Similarly, the business generates about 55% of revenue from customers in healthcare, 25% from industrial biotech, and 18% from academic groups.

It's no mistake Twist Bioscience has leaned into NGS tools during its recent prioritization of operating efficiency – it's the largest and most profitable segment for the business. That has come at the expense of biopharma applications, which were held up as a key growth area not too long ago. The longer lead times for these customers and applications mean the company is better off waiting for milestones and royalties to kick in years from now than going all-in.

Overall, the business is off to a great start in the first half of fiscal 2024. But some additional context is helpful.

Twist Bioscience is on pace to report an operating loss of approximately $183.4 million in fiscal 2024, according to the current model. That's a meaningful improvement from the $217 million operating loss in fiscal 2023. The operating margin of negative 58% is also markedly better than negative 89% last year and negative 115% in the two previous years.

That means the business might only burn $91 million in cash during fiscal 2024, allowing it to exit September with approximately $245 million in cash. If gross margin steadily improves to 60% and revenue grows at 25% for the next several years, then that's probably a long enough cash runway to reach cash flow positive operations and profitability. The question becomes: Is 25% revenue growth realistic? It's certainly plausible.

Does Express Genes Mark Another Hit for Twist Bioscience?

One of the most attractive things about Twist Bioscience as an investment opportunity is the diversity of the business. The company can serve customers across multiple independent industries and applications. A slowdown in synthetic biology applications might not necessarily predict a slowdown among DNA sequencing applications, and vice versa.

Choosing a new application area, then launching and ramping into it, isn't guaranteed to succeed. The company has executed very well within the NGS tools market, which now provides most revenue and gross profit. But it whiffed when eyeing the opportunity in biopharma and antibody discovery applications, which haven't delivered revenue growth in two years.

That makes the early success of Express Genes more soothing to anxious investors. Express Genes is a premium product offering allowing customers across biopharma, industrial biotech, and genetic testing to realize 30% to 55% reductions in shipping times compared to the company's standard offering.

It's still early. The full launch only occurred on January 24 and mapping order backlogs onto future revenue growth is more art than science for a new product offering. But the launch was aligned with a best-case scenario.

- Express Genes appears to be a hit – so far, at least. The business reported fiscal second-quarter 2024 revenue of $29.8 million vs. an order backlog of $44.9 million for its unofficial synthetic biology segment. That compares to $26.8 million in revenue and orders of $29.2 million in the last full quarter prior to launch.

- For the first time ever, the order backlog for synthetic genes (which represents 30% of total revenue) exceeded the order backlog for NGS tools (which represents 54% of total revenue).

This is a great start. Can the momentum keep up? Investors will feel more confident in their answer after seeing fiscal third-quarter 2024 results reported in August. Two things I'll be watching.

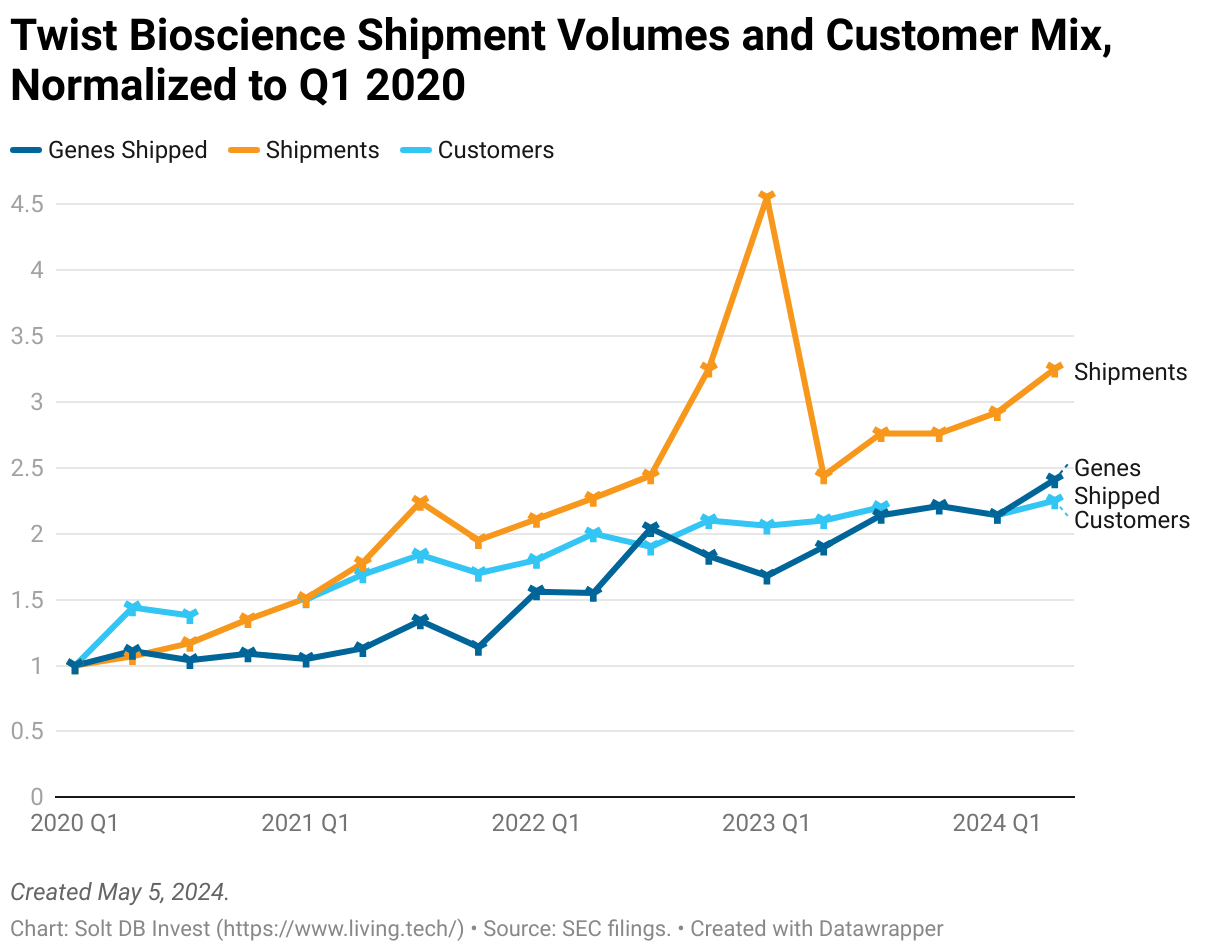

First, investors want to see if the numbers of customers and orders are increasing with the order backlog. The ambitious vision of Express Genes is that by offering high-quality synthetic DNA with fast turnaround times, Twist Bioscience can convert stubborn "DNA Makers" – labs that find it easier to create their own genes and just eat the labor costs – into customers. Faster shipping also makes the brand more attractive in a jampacked competitive landscape.

The too-early-to-tell signs are encouraging, but not conclusive. Twist Bioscience shipped a record number of genes, reported the highest number of shipments in five quarters, and saw a slight uptick in customers. The business has been struggling to grow the number of customers for the last eight quarters. Will these numbers pop in the fiscal third quarter?

Second, Express Genes is a new offering, but it has some cannibalization risk. There are customers who were previously purchasing synthetic DNA from Twist Bioscience who are happy to pay a premium price for faster turnaround times. These customers result in only marginal revenue and gross profit growth. Signing up brand new customers and accounts will be a much bigger growth driver, but it's too soon to say how many new customers come knocking. It's likely that Express Genes has reset the level of quarterly customers higher, but how much higher?

Keep in mind the launch of NGS tools had no cannibalization risk, which helps to explain the portfolio's ongoing success. Express Genes are different. This is certainly something to watch as the quarterly periods tick by, as cannibalization risks have eaten shareholders alive for other companies in the Solt DB Invest coverage ecosystem – namely PacBio and 10x Genomics. Wall Street tends to only pay attention to this risk when it's too late for individual investors to course correct.

Scenario Analysis

Only Solt DB members have access to this information.

Margin of Safety & Allocation

Only Solt DB members have access to this information.

.svg)

.svg)

.svg)

-cropped.svg)