"They Don't Make 'Em Like They Used To"

Illumina notched its first full-year operating profit in 2006 – eight years after being founded. For those of you keeping score at home, the company was founded in 1998 at the tail end of the Dot Com Bubble. It didn't bitch about interest rates or VCs that "didn't get it." It created an operating plan independent of interest rates and VCs based on operating efficiency and fiscal discipline.

Operating efficiency is a lost art in company formation.

What does operating efficiency mean? Think of operating efficiency as trickling down an income statement. A business needs to generate enough revenue at a high enough gross margin so that gross profit is greater than operating expenses. Revenue doesn't pay for shit. Gross profit is the key.

During the recent era of unusually low interest rates, many startups and businesses focused on generating revenue without focusing too much on the quality of the revenue. However, a business with $100 million in revenue at a 10% gross margin generates the same level of gross profit ($10 million) as a business with only $15 million in revenue at a 67% gross margin ($10 million). More revenue isn't always better, especially since the overhead needed to support a company generating $100 million in revenue will be significantly higher.

A business isn't sustainable or able to self-fund operations until it can consistently generate operating income, which is what's left over subtracting operating expenses from gross profit.

Illumina prioritized operating efficiency over growth from the beginning, which allowed it to become profitable just eight years after being founded. In 2006:

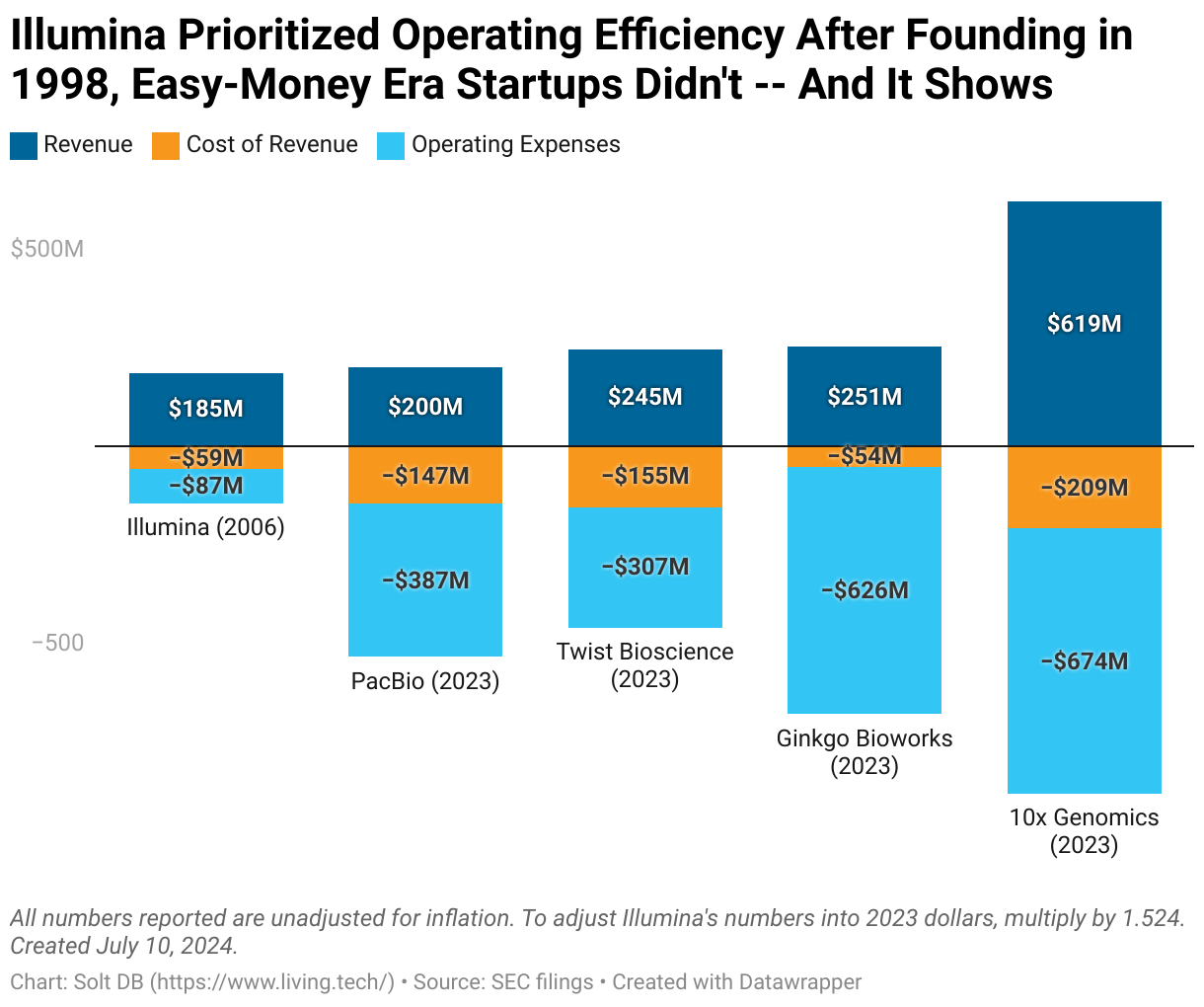

- The business had just $185 million in total revenue. That's equivalent to $282 million in inflation-adjusted 2024 dollars.

- The DNA sequencing pioneer posted a gross margin of 67.9%. That left it with a gross profit of $127 million.

- Illumina recorded $54 million in sales, general, and administrative expenses ($83 million inflation-adjusted) and $33 million to R&D expenses ($51 million inflation-adjusted). Remarkably, the largest expense that year was the cost of revenue at $59 million ($91 million inflation-adjusted).

- That all trickled down the income statement as $38 million ($58 million adjusted) of operating income, representing an operating margin of 20.5%.

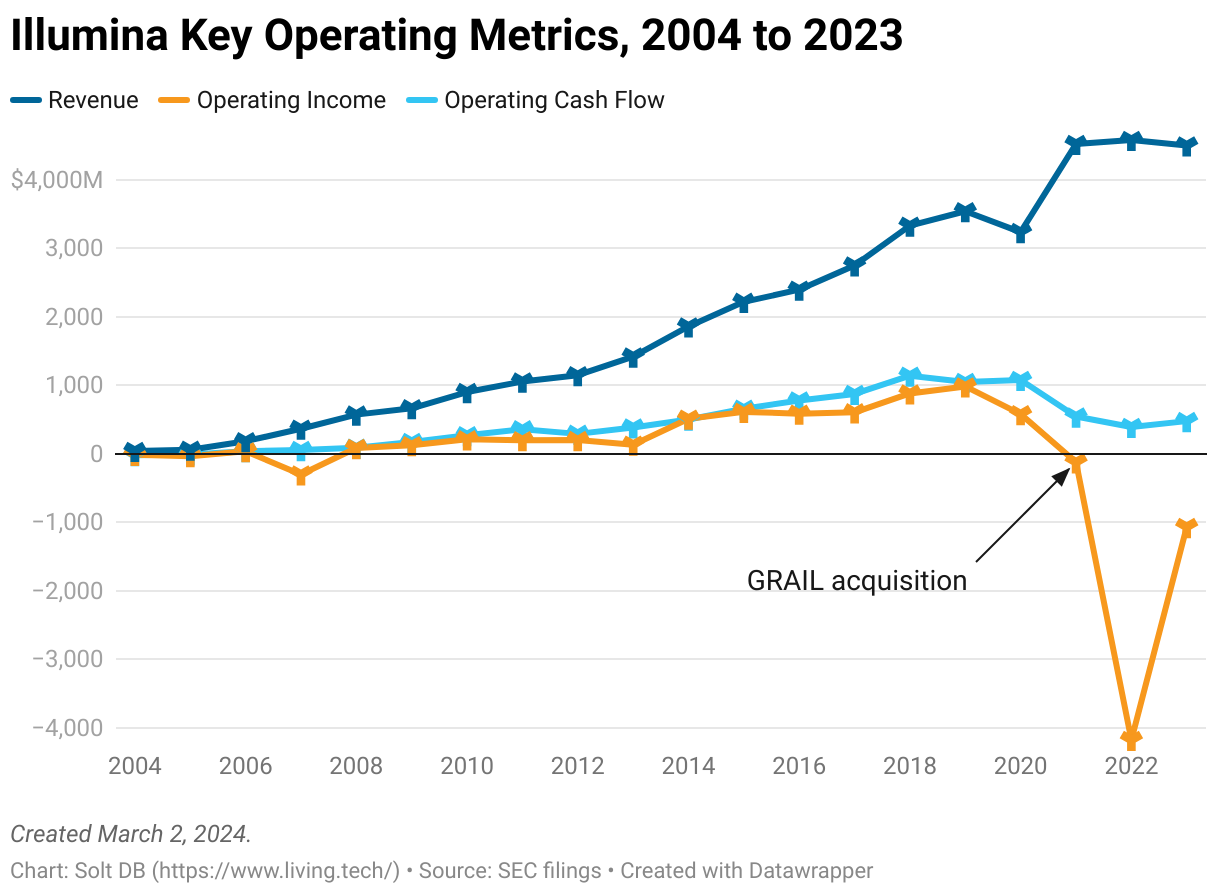

The business posted an operating loss the following year due solely to its acquisition of Solexa, but followed with 13 consecutive years of profitable operations until the disastrous GRAIL acquisition in 2021. It has never relinquished its streak of positive operating cash flow, which sits at 18 years and counting through 2023.

Despite having a blueprint for over two decades, no other biotech company serving the R&D inputs sector has come close to replicating Illumina's success. Actually, not many companies in any biotech sector have replicated Illumina's success.

Why not?

It's important to acknowledge there aren't any apples-to-apples comparisons across time or industries. Different lab instruments have different margins, utilization rates, competitive landscapes, and value-added benefits. The same can be said for comparisons to other R&D inputs used across major biotech sectors, such as reagent kits or synthetic DNA.

Nonetheless, the absence of profitable businesses at similar levels of revenue in the broader peer group is striking. Consider how other businesses fared with revenue totals comparable to Illumina's 2006 campaign ($185 million in 2006 dollars is $282 million in 2024 dollars).

Ginkgo Bioworks (founded 2008), 10x Genomics (2012), and Twist Bioscience (2013) were born into an era of easy money. They were built like it, too. PacBio (2004) is spiraling toward bankruptcy, whether investors realize it or not, primarily because it never prioritized operating efficiency in its two-decade history. It shows, too.

How the F*nch Did Illumina Pull It Off?

Illumina was ultra-efficient because it had to be. It wasn't just the DNA sequencing leader. Netflix was founded in 1997. Google was founded in 1998. Facebook was founded in 2004. That timing isn't a fluke.

That’s the good news in all these data.

If adversity breeds resilience, and resilience breeds profitable operations, then some of the world's most efficient businesses ever created are forming right now during biotech's current funding crunch. We just can't appreciate it yet. We don't even know the names of many of these companies. Some primordial teams are meeting right now, reading this, and about to launch a motherfucker of a business. Good. The bioeconomy (and planet) needs it.

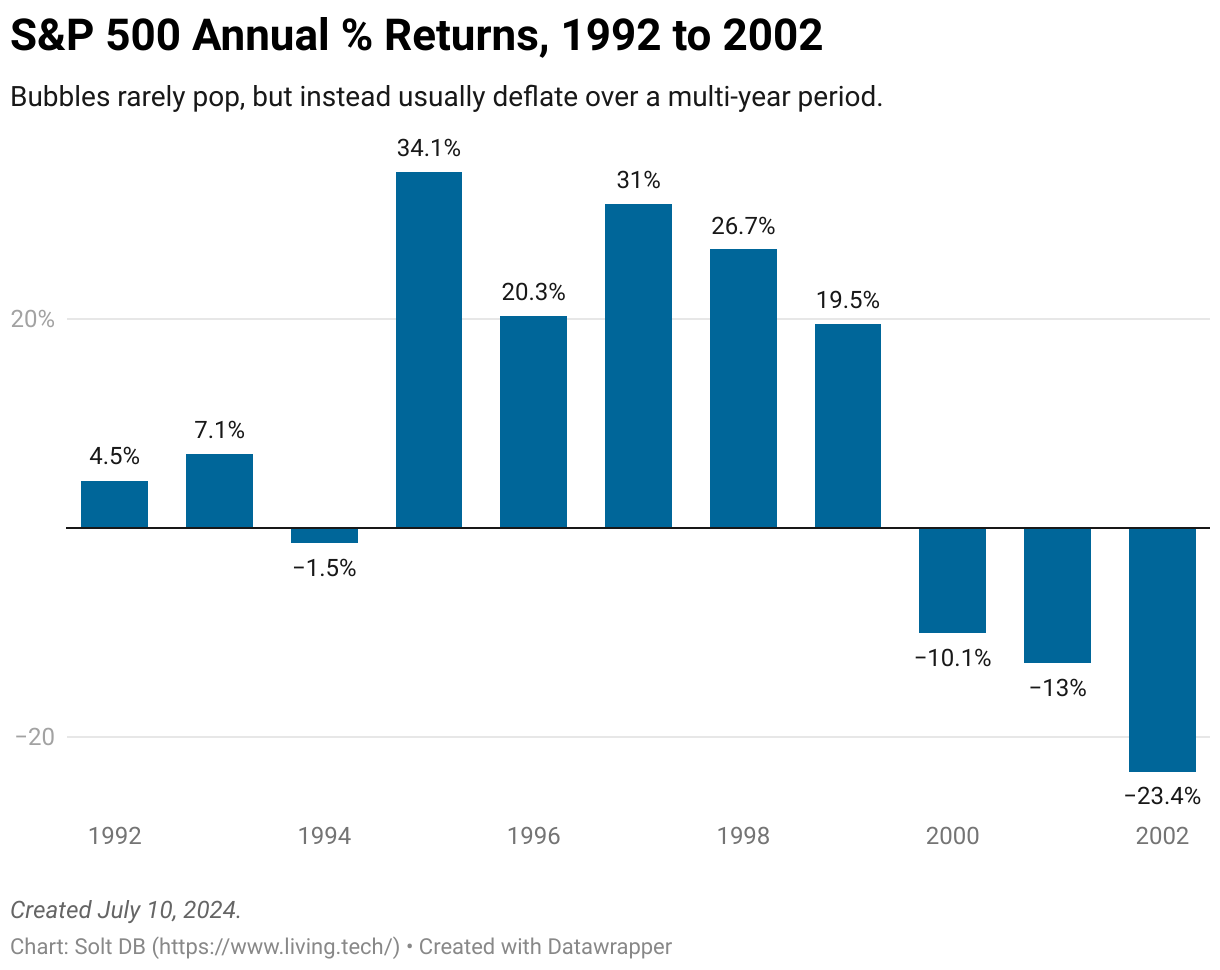

Consider that Illumina was founded in 1998 – near the very end of the Dot Com Bubble. For context, most bubbles don't violently pop, but slowly and painfully deflate over years. The S&P 500 delivered five consecutive years of double-digit percentage gains from 1995 to 1999. It followed with an equally unusual three consecutive years of double-digit percentage losses.

Advice to blindly keep pouring money into the S&P 500 at currently bubbly levels catalyzed by artificial intelligence because "you can't time the market" misses this key historical context. Money invested in the S&P 500 in January 2000 returned 4.9% annually through June 2024 after accounting for inflation. Money invested in January 2003 returned 8.1% per year on the same basis.

Still want to trot out hollow bullshit like "time in the market beats timing the market"? Okay.

If you had invested $10,000 in the S&P 500 at the beginning of each year from 2000, 2001, and 2002, then you'd have $108,051 in June 2024. If you had instead parked that money in cash and then dumped it all into the S&P 500 at the beginning of 2003, then you'd have $153,979 right now. That's a difference of 43%. Would you like your net worth to be 43% higher? I thought so.

Timing absolutely does matter in investing, especially in biotech investing. You just have to acknowledge that retirement is as much an industry as it is a modern stage of life.

Wait until investors read a paper from an economist at the U.S. Federal Reserve who found that, from 1989 to 2019, an estimated 40% of growth in corporate profits was explained solely by lower tax rates and lower interest rates. Fully 100% of the expansion in valuation multiples in that span was explained by the same factors.

Illumina embraced the subdued funding environment it was born into. Interest rates were 5.84% the year the company was founded. They're 5.33% today. Interest rates were 5.17% eight years later when the company turned profitable. Emerging startups today might not be in much worse shape in 2032, although interest rates could be permanently higher as demographics deteriorate.

The DNA sequencing leader succeeded by mastering the "little things." It didn't overspend on marketing, or building a giant sales force, or R&D for lab tricks with little commercial viability. It built, acquired, and developed technologies customers needed.

You might argue things weren't so simple. I concede a point or two.

For example, Illumina operated with little meaningful competition. It acquired what little technological threats it faced.

And although a gang of newcomers such as PacBio, Oxford Nanopore, and Element Bio are now promising years of double-digit growth ahead, they'll combine for full-year 2024 revenue of about $500 million and an operating loss of at least $400 million.

The titan of sequencing won't grow at all this year. It'll generate only $4.4 billion in revenue.

The End of the Expansion Bias

This longitudinal analysis of Illumina highlights what John Bogle, the founder of Vanguard and inventor of passive investing, described as a world awash in "management, not leadership." Jay Flatley was a leader. We don't have too many of those in living tech today.

Rather than wait for interest rates to decline, investors and entrepreneurs should acknowledge that for most of history companies needed to be more fiscally responsible to survive. The brief 14-year period from 2009 to 2022 is the historical anomaly, not representative of normal market conditions, for building businesses.

There are companies caught on both sides of the divide of the expansion bias. Whereas some startups used "growth-at-all-costs" business models to scale and eventually achieve profitable and positive cash flow operations, many others left themselves no room to pivot.

Ironically, chasing shiny objects backfired on Illumina. If only it had stuck to its roots.

The recent return to historically normal interest rates is a warning, not a temporary blip. While Wall Street hinges on every word from Jerome Powell, investors and entrepreneurs would be better served understanding the future impacts of deficits and demographics. You can always choose operating efficiency as a strategy. Build accordingly.

.svg)

.jpg)

.svg)

-cropped.svg)