Living Tech Fails the iPhone Test

Let's discuss the scale of the iPhone and visualize the gap relative to the bestselling living tech products of all time.

For context, Solt DB organizes the bioeconomy into six biotech sectors including agricultural biotech, biopharma, education and art, environmental biotech, industrial biotech, and R&D Inputs. The most successful living tech brands all hail from drug development thanks to a near-complete lack of price regulations in the United States. Although this article focuses on drug products, readers are reminded that "biotech" and "biopharma" are two different things.

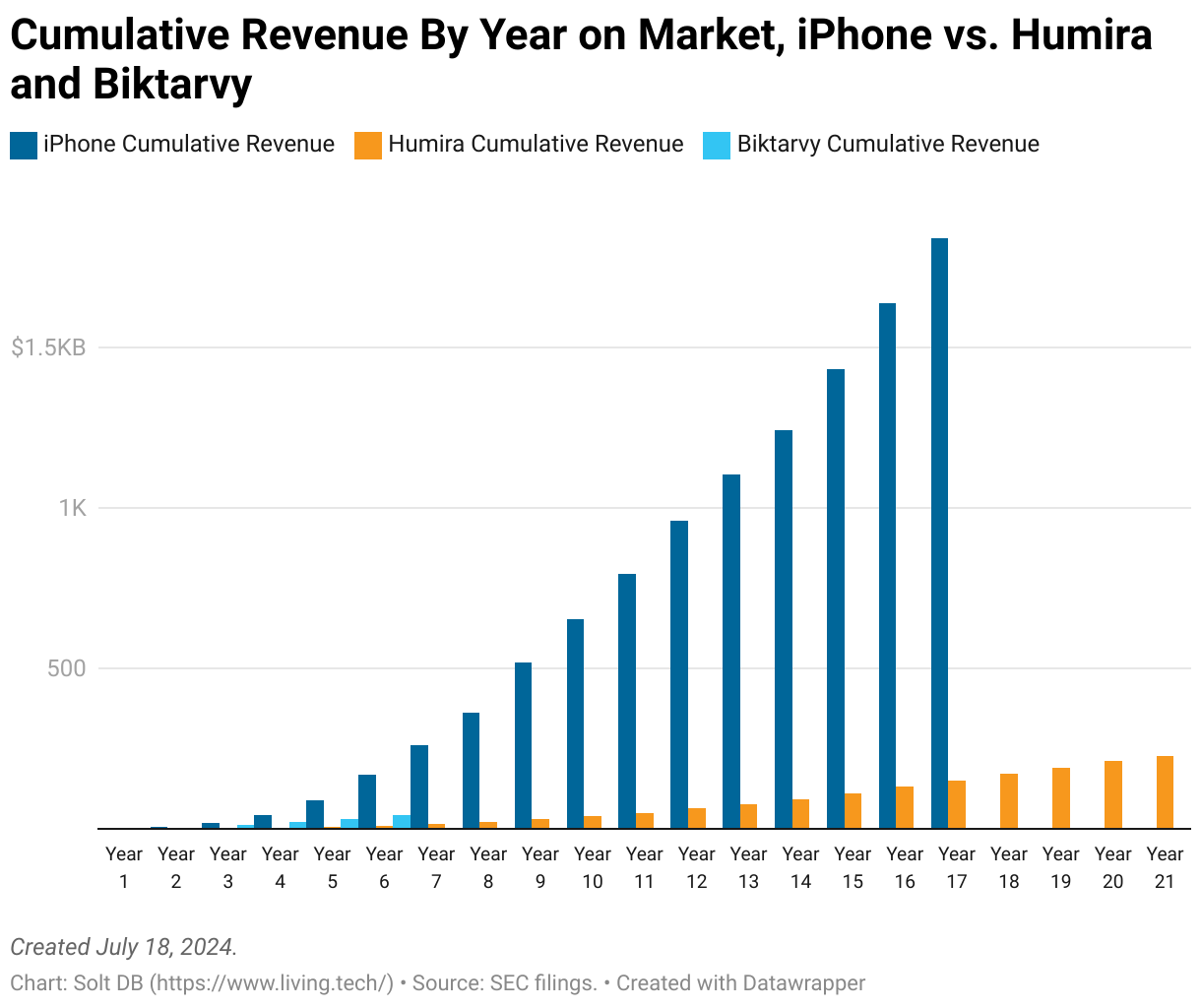

The bestselling drug brand of all time by cumulative sales is the autoimmune drug Humira from AbbVie, which generated $228 billion in revenue from market launch in 2003 through the end of 2023. The iPhone generated revenue of $200 billion in 2023 alone.

The bestselling drug brand of all time by cumulative sales through its sixth year on the market is the antiviral drug Biktarvy from Gilead Sciences, which generated $44 billion in revenue through the end of 2023. The iPhone generated $170 billion in cumulative sales through the same commercial checkpoint.

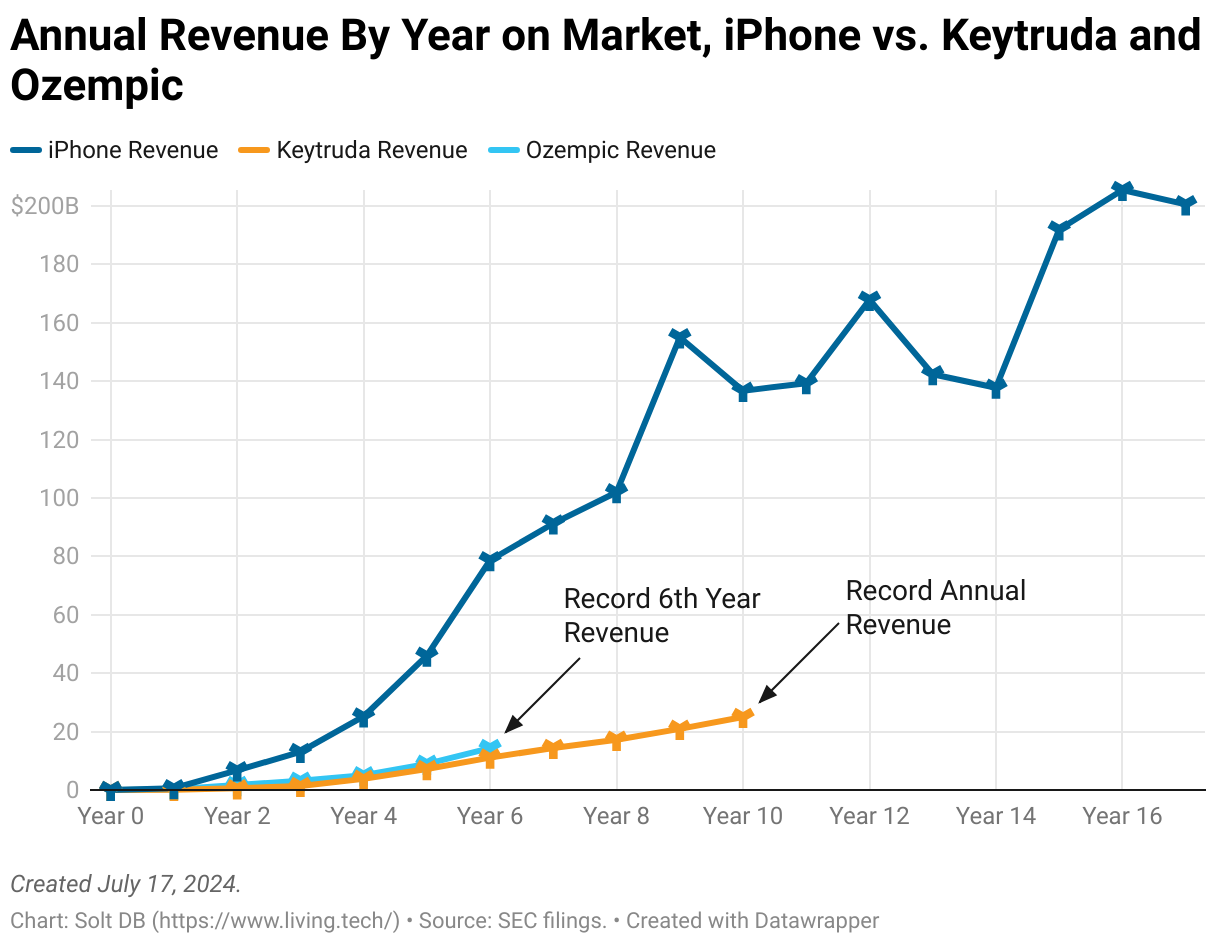

The bestselling drug brand of all time by one-year revenue (excluding hepatitis antivirals and pandemic vaccines) is the cancer drug Keytruda from Merck, which generated $25 billion in revenue in 2023. It took Keytruda 10 years to achieve that ramp. By contrast, the iPhone claimed that milestone in its fourth year on the market.

The bestselling drug brand of all time by its sixth year on the market is the cardiometabolic drug Ozempic by Novo Nordisk, which generated $14.3 billion in revenue in 2023. It launched the same year as Biktarvy. By its sixth year on the market the iPhone generated $78.7 billion in annual revenue.

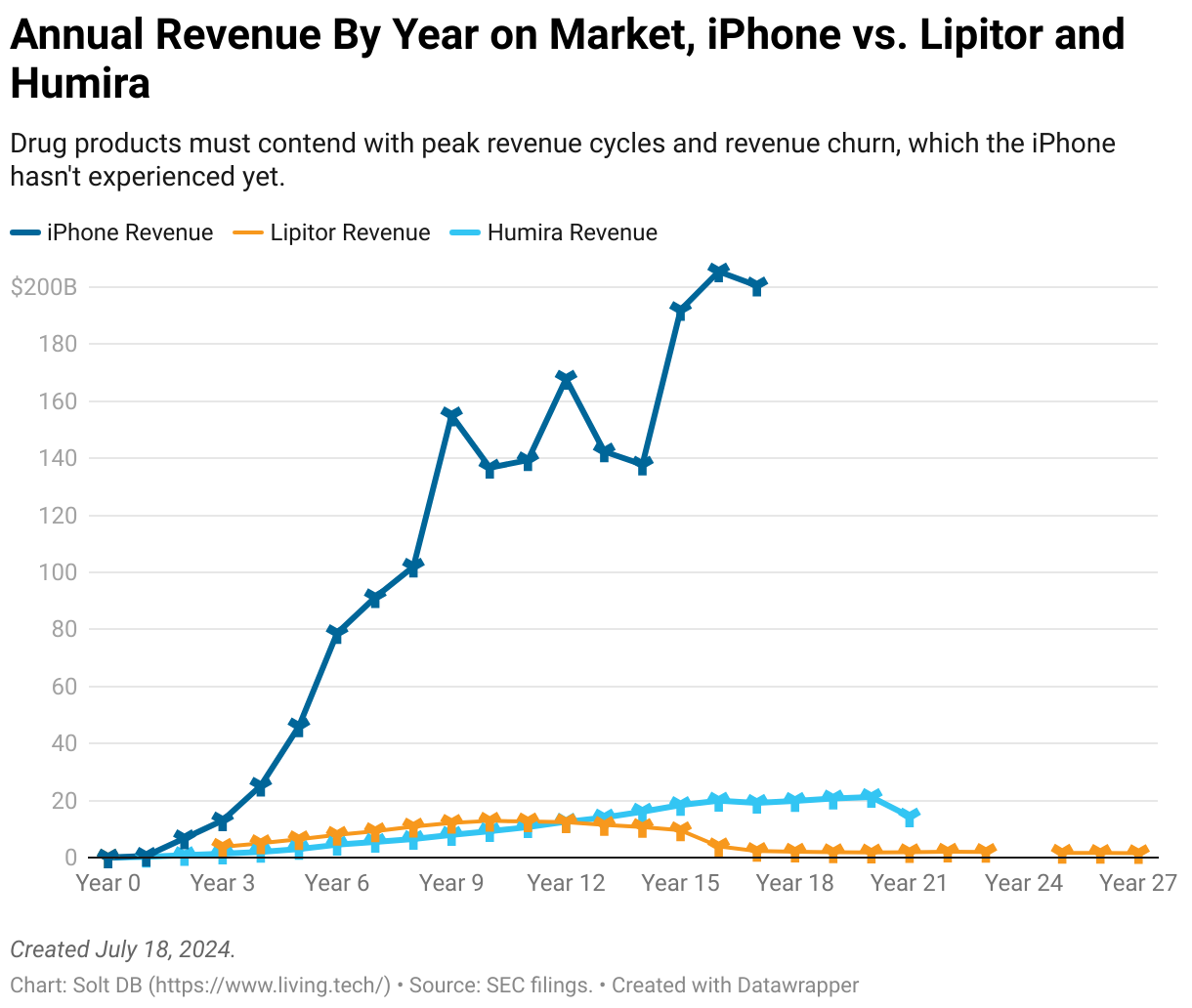

Although emerging blockbuster drugs (such as those treating obesity) will set new records for the sector, even they will eventually lose market exclusivity and face increasing competition as they mature. That's not to say the iPhone won't reach a revenue peak. Maybe it already has. But revenue peaks are expected and predictable in drug development. Apple doesn't need to completely replace its bestselling products every 10 to 15 years.

Consider the revenue arc of the two bestselling drugs of all time by cumulative revenue. AbbVie built a patent thicket and commercial pricing power so insurmountable that Humira's revenue didn't peak until its 20th year on the market – easily a record for biopharma. Lipitor, the world's first drug product to eclipse $10 billion in annual revenue and that was still somehow a blockbuster in 2023, more clearly shows the traditional revenue peak and decline of a drug brand. Neither comes close to the scale of the iPhone.

It's not just the iPhone, either.

Each of Apple's five business segments generated more revenue in 2023 than the world's all-time bestselling drug generated during its record-setting year. In addition to the iPhone ($200.6 billion), that included the Mac brand ($29.3 billion), the iPad brand ($28.3 billion), the wearables and home accessories portfolio ($39.8 billion), and services ($85.2 billion). Keytruda notched an industry record $25 billion in global revenue in 2023.

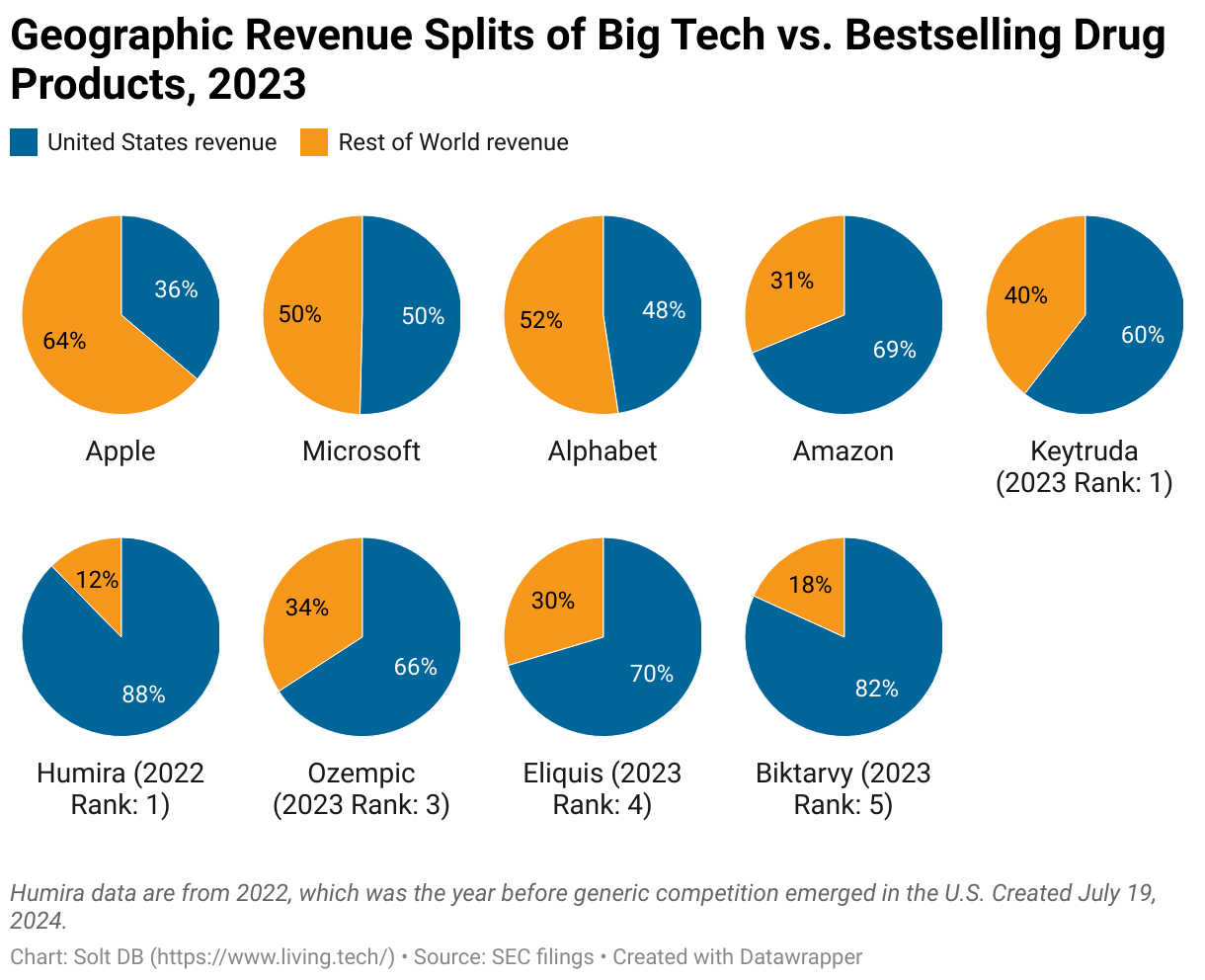

One reason drug brands fail to scale similarly to the iPhone or Air Pods or Amazon Web Services is that they don't scale globally. The global drug development industry is overwhelmingly dependent on patients in the United States for revenue and profits. As discussed in previous analysis from Solt DB, nearly 60% of blockbuster drug revenues were generated by American patients in 2023. The remaining 40% of sales from global bestsellers was generated by the other 96% of humanity.

That 60/40 geographic revenue split represents the average across all 152 blockbuster drug products in 2023. The top 20 or so drug brands are generally even more dependent on American patients. Information technology businesses don't have nearly the same geographic constraints.

It's not unusual for a business in any economic sector to be carried by its best products. But living tech products simply haven't scaled well enough to carry businesses to a $1 trillion market valuation.

Unfortunately, comparisons between information technology and living technology don't improve if we zoom out from products to focus on the overall profitability and efficiency of businesses.

Biotech Isn't Close to Earning a $1 Trillion Valuation

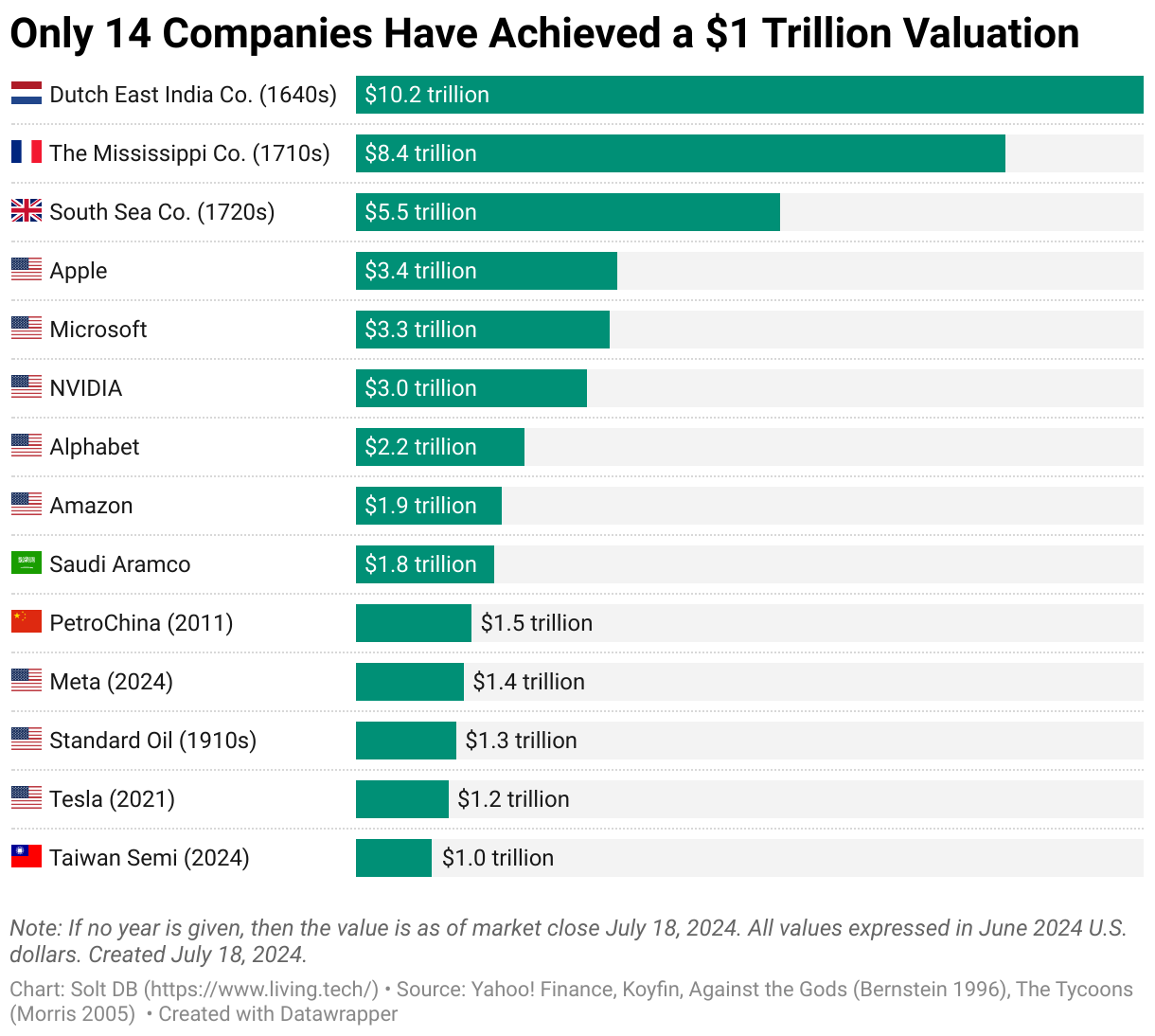

Only 14 companies have ever achieved a $1 trillion valuation. None have been biotech companies.

The three largest companies in history, The Dutch East India Company in the 1640s and The Mississippi Company and South Sea Company in the early 1700s, literally were the distribution infrastructure for trade in their time. The pride of the Netherlands eventually succumbed to an inefficient cost structure, while the others represented two early examples of devastating and eponymously-named stock bubbles. We never learn, do we?

Another trio of trillion-dollar companies have hailed from the energy sector, specifically focused on petroleum and refined products. All three were monopolies in their respective region or time. A future living technology company could find parallels. Go invent and commercialize the mitochondrial battery, or ambient chromatography, or cellular water desalination. You might have a chance to make this list.

All remaining companies in the group are modern American information technology giants, and whatever sector Tesla's from this quarter. How do biotech companies stack up?

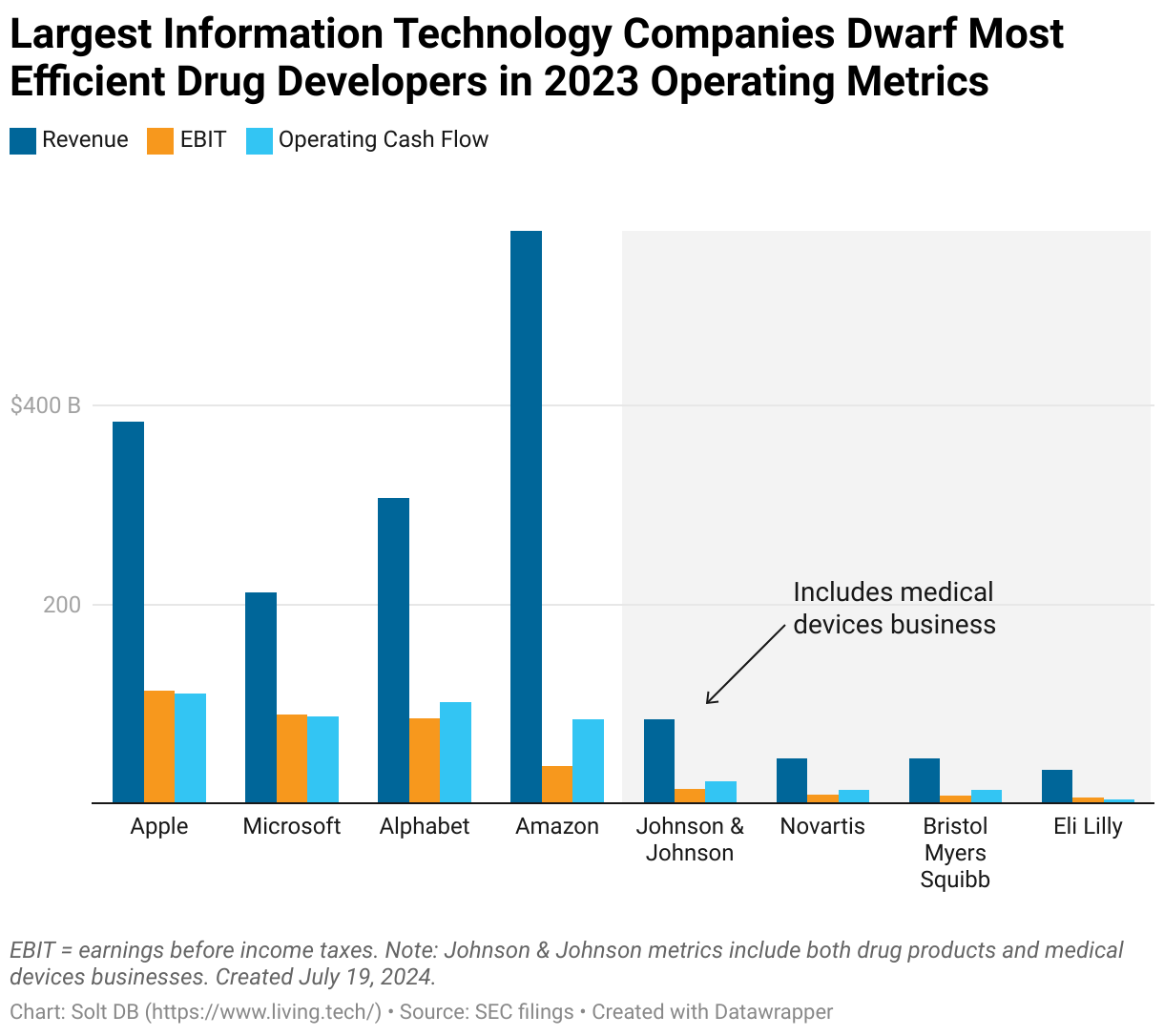

The three most-profitable drug developers in 2023 were Johnson & Johnson, Novartis, and Bristol Myers Squibb. The largest drug developer as of this writing is Eli Lilly, which is riding a wave of momentum from big wins across its cardiometabolic (obesity), neuroscience (Alzheimer's), and oncology portfolios.

They might be the Fab Four of pharma, but they're dwarfed by the four largest information technology companies when it comes to the key operating metrics of revenue, earnings before income taxes (EBIT), and operating cash flow.

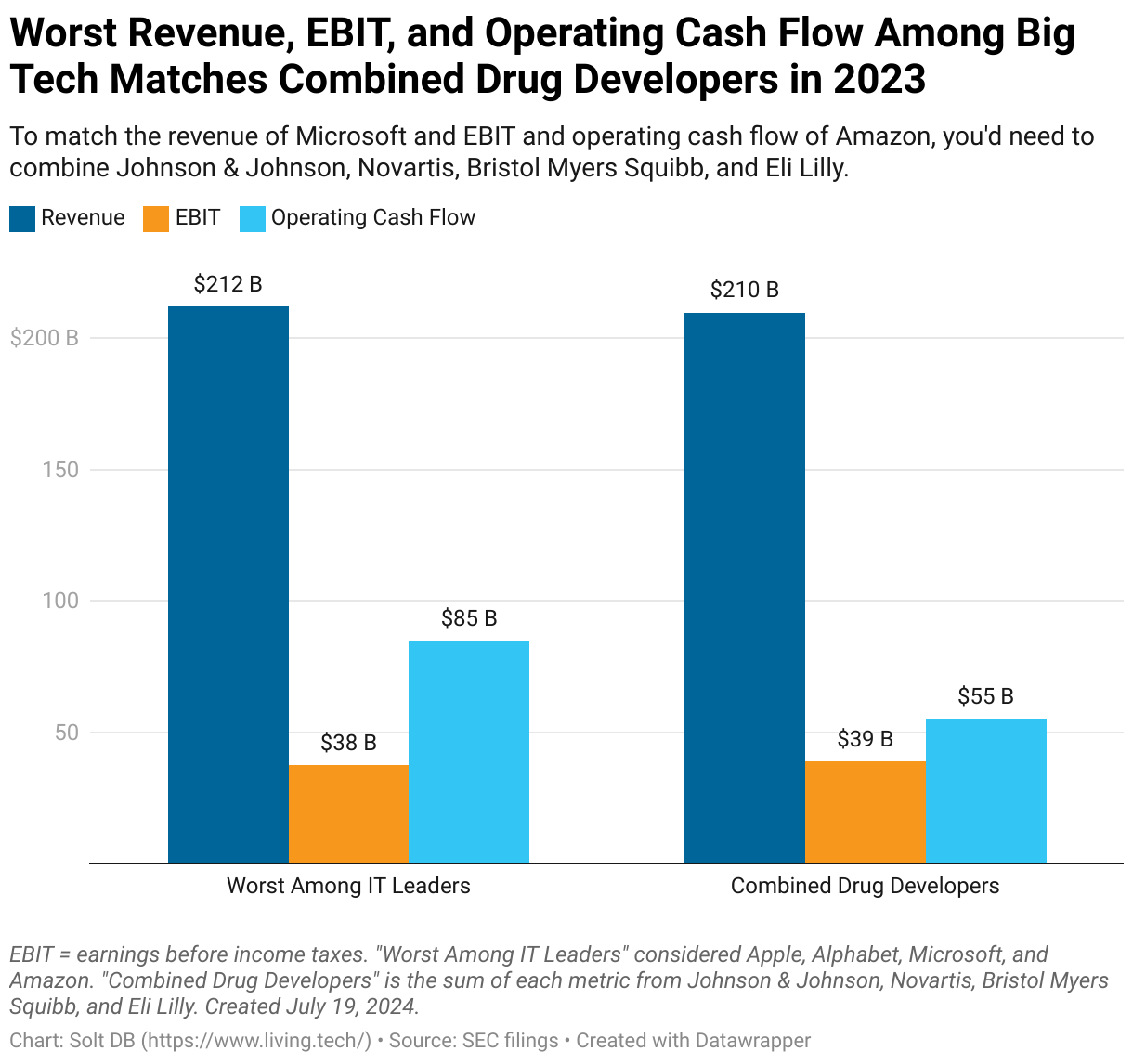

These four drug developers had combined revenue of $209.7 billion, EBIT of $39.2 billion, and operating cash flow of $55.1 billion in 2023. That roughly matches the revenue of Microsoft ($211.9 billion) and the EBIT of Amazon ($37.6 billion) – each the worst values among the four Big Tech companies above.

The comparison falls apart on operating cash flow, as the worst value among IT leaders (Amazon's $84.9 billion) easily outpaces the combined performance of pharma's Fab Four.

Oh, and you'd have to include Johnson & Johnson's medical devices business segment in the data visualizations above and below to make the comparisons work.

Information technology companies aren't just larger than living technology companies. They're also significantly more efficient at converting revenue to earnings.

Alphabet (28%), Apple (30%), and Microsoft (42%) easily outpaced the EBIT margins of Johnson & Johnson (18%), Bristol Myers Squibb (19%), Novartis (20%), and Eli Lilly (19%). Amazon's low-margin business isn't as efficient on this metric (7%), but it makes up for it with sheer size. It generates 16.8x more revenue than Eli Lilly and 2.7x more than Microsoft.

Amazon might be a harbinger for non-biopharma businesses that will presumably have lower margins, such as those in agricultural biotech, industrial biotech, environmental biotech, and R&D inputs. Growables will need truly staggering global scale in humanity-altering applications, such as climate tech or energy storage, to drag a company across the $1 trillion valuation threshold.

There are exactly zero self-sustaining living tech businesses in these applications today.

The Best is Yet to Come

Despite present-day limitations I'm confident living technology will eclipse information technology as the key economic driver in my lifetime. I'm not sure it'll be close.

We just haven't built the proper infrastructure, sensors, and tools yet. We're also limited by our thinking. The iPhone, Google Search, and Amazon Web Services combine existing technologies in a unique way to create compounding value. Living technology has yet to do the same.

For example, who said antibodies and proteins can only be used in healthcare applications? Biology has handed us the ultimate tool for filtering air and water, or for real-time non-destructive detection of any chemical signature. We too often focus limited resources on wishy washy efforts that sound cool but lack direction, like the Cancer Moonshot. Where's the moonshot effort to reduce antibody manufacturing costs 100x so we can embed them on ambient filters and sensors?

Why are our most powerful sequencing instruments the size of a refrigerator? The iPhone fits in your pocket. Why does sequencing require special sample preparation steps? If everyone needed to write code to use Microsoft Word or Google Docs, then I'm not sure many people would've seen the point. Things don't get interesting until sequencing tech arrives at your family doctor, local pharmacy, or Walmart.

Think of it this way: If you could build the ultimate self-aware and autonomous robot, then it would probably be an organism.

Biology programs itself, converts and stores its own energy, harvests its own resources, copies itself, forks its code in response to dynamic surroundings, repairs itself, only uses on-device compute for the ultimate speed and security, and retains information for billions of years. It can do this without any human input after an initial engineering phase.

It'll take another two to three decades, but entirely new products, services, consumer gadgets, and household appliances await once we adequately reverse engineer 3 billion years of evolutionary R&D from Mother Nature. Until then, we might not see many living technology businesses reach a $1 trillion valuation.

.svg)

%20(squoosh).jpg)

.svg)

-cropped.svg)