.svg)

The fast pace of innovation in living technology represents both an opportunity and a risk. Arrowhead Pharmaceuticals just got another reminder about the latter.

For the second time in six months, emerging therapeutics that look to correct the underlying genetic cause of alpha-1 antitrypsin (A1AT) liver disease teased preliminary data suggesting merit in each approach. Wave Life Sciences unveiled promising data for its RNA editor WVE-006 in October 2024. Beam Therapeutics followed in mid-March 2025 with an early look at its DNA editor BEAM-302.

Although the preliminary data readouts include just nine patients with evaluable mutant protein level data combined, correcting the mutation that causes A1AT liver and lung disease is closer to an ideal treatment than silencing the mutation. That doesn't bode well for the commercial longevity of fazirsiran, being jointly developed by Arrowhead Pharma and Takeda, which should be submitted for regulatory approval in 2028.

Fortunately, a deep pipeline means the RNA interference (RNAi) pioneer is never overwhelmingly dependent on any single program. The turbulent competitive dynamics in A1AT deficiency also highlight the importance of partnering lower priority or trickier-to-commercialize assets, which generates at least some financial benefit through upfront payments and cost-sharing – even if programs fail or get outcompeted.

The Fast-Changing A1AT Landscape Dynamics, Explained

A1AT deficiency is caused by mutations in the SERPINA1 gene, which encodes for the alpha-1 antitrypsin protein (AAT). Healthy copies of AAT float around the body and protect cells from inflammation. Mutated copies of AAT not only fail to guard against inflammation, but in severe cases can accumulate in the liver faster than the body can clear it.

As with all genes, individuals inherit one copy from each parent. But there are dozens of variants of the SERPINA1 gene. Some mutations have no impact on the function of the AAT protein, while others result in severe and life-threatening symptoms.

The disorder is a little unusual because it impacts two distinct major organs: the lungs and liver.

- Individuals with one faulty SERPINA1 gene usually produce enough AAT to remain healthy with no or mild symptoms.

- Individuals with one severe mutation can have impaired liver or lung function.

- Individuals with two mutations don't produce enough AAT to maintain healthy lung function, while the accumulation of faulty AAT proteins in the liver may require liver transplantation.

Arrowhead Pharmaceuticals designed fazirsiran to inhibit one type of severely mutated protein, called Z-AAT. Clinical trials have demonstrated that reducing production of the faulty protein allows the body to clear built-up accumulation in the liver, reducing scarring (fibrosis). If treated for long enough, then patients with severe fibrosis should see an improvement in liver function.

Although fazirsiran has the potential to treat A1AT liver disease by reducing production of Z-AAT, patients treated with the RNAi drug candidate are still at risk of A1AT lung disease. That's because silencing the mutated protein doesn't address the lack of functional AAT production, which is needed to protect the lungs.

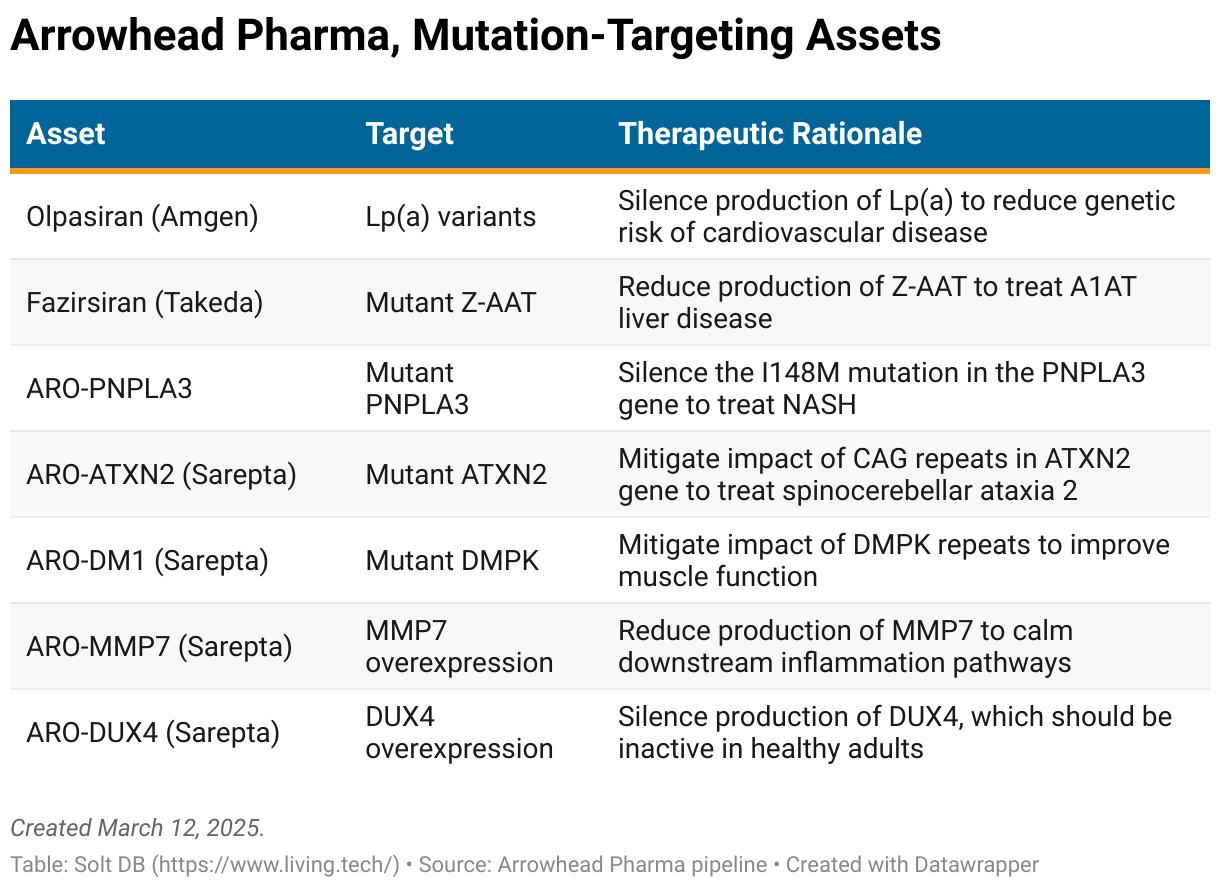

Using RNAi to silence mutated genes results in a riskier commercial strategy, as safely fixing mutated genes will always be an ideal treatment. This is why the company has partnered all but one of its mutation-targeting assets, such as fazirsiran or olpasiran. In this specific case, Arrowhead Pharma chose to partner with Takeda because it's the second-largest provider of augmentation therapy for A1AT lung disease. Augmentation therapy provides AAT proteins to individuals who cannot produce enough on their own.

The complementary partnership – fazirsiran treats A1AT liver disease, augmentation therapy treats A1AT lung disease – de-risks the commercial strategy and promised to offer patients the first complete solution for severe A1AT deficiency.

But the emergence of RNA editing and DNA editing drug candidates weakens the value proposition of an Arrowhead Pharma and Takeda tie-up. If mutated Z-AAT proteins can be corrected into functioning AAT proteins, then both liver and lung manifestations of A1AT deficiency could be treated with a single drug product.

- In October 2024, Wave Life Sciences announced early data from the first two patients ever treated with an RNA editing drug candidate. WVE-006 demonstrated the ability to correct mutated RNA encoding the Z-AAT, converting it into a functioning version called M-AAT. With a little dose optimization it seems like an ideal treatment for A1AT deficiency.

- In March 2024, Beam Therapeutics announced preliminary phase 1 data from the first nine patients ever treated with an in vivo CRISPR base editing drug candidate. BEAM-302 demonstrated the ability to correct the mutation that causes Z-AAT proteins and produce functioning M-AAT proteins. It needs a little more dose optimization than WVE-006, but it's another promising therapeutic approach.

RNA editing is likely to have similar dosing schedules as RNAi, or roughly once per three to six months. DNA editing is permanent with current tools, meaning only one or several doses need to be given in a patient's lifetime. Either beats the snot out of dosing patients with RNAi to address A1AT liver disease, then providing weekly augmentation therapy via intravenous infusions in special medical centers to address A1AT lung disease.

What's Next for Fazirsiran?

The emergence of promising corrective therapeutic modalities significantly reduces the value of fazirsiran. I've removed it from my model.

Arrowhead Pharma entered into a co-development agreement with Takeda in 2020. The RNAi pioneer snagged $300 million upfront, another $40 million at the start of the first phase 3 study, and stands to receive an additional $527.5 million in milestones. The two agreed to a 50/50 profit share in the United States, while Takeda will pay 20% to 25% royalties on international sales.

The pharma giant expects to complete multiple ongoing studies in the next few years and submit a regulatory filing in 2028. That could potentially be moved up to 2027 depending on study results in the interim. Takeda estimates fazirsiran has peak global sales potential of $1 billion to $3 billion.

Although the shared asset could enjoy no competition for several years, RNA editors and DNA editors might not be too far behind. If WVE-006 and BEAM-302 deliver promising results in larger studies, then regulators may be open to accelerated development timelines and approvals. That's more likely for Wave Life Sciences than Beam Therapeutics, as RNA editing is reversible. The U.S. Food and Drug Administration (FDA) may want longer-term safety data from DNA editing tools.

I certainly wouldn't expect fazirsiran to become a blockbuster drug product unless a technical or safety surprise derails emerging drug candidates (I don't expect that either). The asset could have more longevity in international markets thanks to convenient subcutaneous administration, but the revenue opportunity is almost immaterial and, once again, RNA editing would have the edge. It's also administered subcutaneously.

Why Arrowhead Pharma Partners Mutant-Targeting RNAi Assets

Don't worry, I wasn't going to leave yinz hanging.

The fact that Arrowhead Pharma deprioritizes mutant-targeting RNAi drug candidates – and partners those it does conjure up – is a profound insight for investors. This alone can give you confidence if the market overreacts to perceived competitive threats from corrective therapeutic modalities.

(To be clear, the market reaction to fazirsiran's competitive positioning wasn't an overreaction per se, but the business was already relatively undervalued.)

Arrowhead Pharma has adopted a development strategy that accounts for the commercial realities of RNAi. The ability to safely and selectively silence genes is very valuable, but that isn't enough to treat every disease. As is the case with A1AT deficiency, an ideal treatment requires both reducing production of faulty proteins and restoring production of functional copies. RNAi can only do the former. While the approach can still provide value in certain indications, these assets will always be exposed to next-generation competition that can both silence and restore.

This explains why the company has outlicensed all but one asset that takes aim at mutant protein production.

So, what the hell makes the other pipeline assets different?

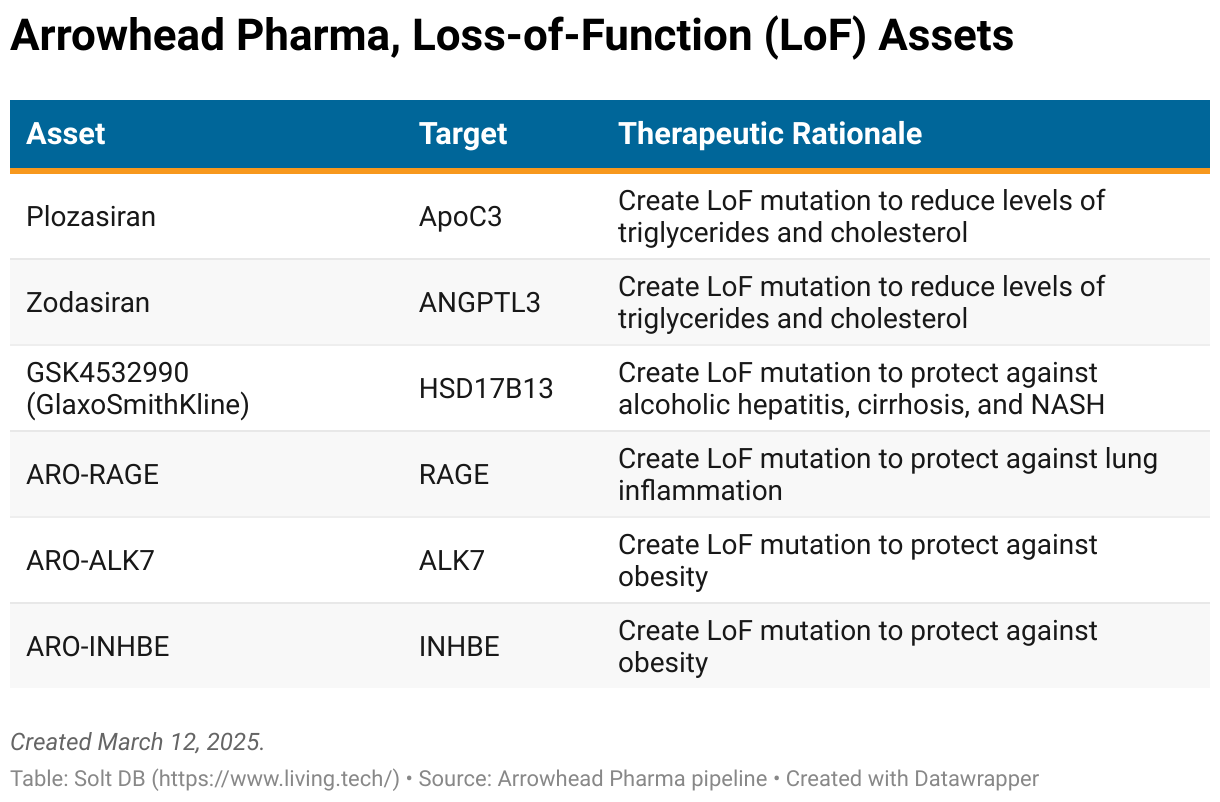

Rather than block the production of faulty proteins to silence disease-causing mutations, Arrowhead Pharma prioritizes assets that give patients protective mutations. The goal is to create a specific genetic makeup ("genotype") known to guard against diseases – and it's typically accomplished by silencing genes that aren't actively implicated in diseases at all.

Consider plozasiran. The RNAi drug candidate silences the ApoC3 gene to significantly reduce levels of triglycerides and cholesterol. The ApoC3 gene isn't mutated and doesn't cause high cholesterol in these patients, but loss-of-function mutations that disable the gene protect against it.

Or take ARO-INHBE. The INHBE gene isn't mutated and doesn't cause obesity, but scientists have discovered individuals with rare loss-of-function mutations that disable the gene are protected against obesity, type 2 diabetes, and cardiovascular risks.

RNAi drug candidates that engineer protective genotypes with loss-of-function mutations have much lower competitive threats. If Arrowhead Pharma can reduce ApoC3 or INHBE or RAGE levels enough to treat high cholesterol, obesity, or asthma; then there's little to no room for improvement – patients either have a protective genotype or they don't. The best competitors can do is match the performance of RNAi and try to compete for market share.

The company may deviate from this approach on a case-by-case basis if it has other core advantages. For example, a next-generation delivery platform might allow RNAi drug candidates to cross the blood brain barrier with subcutaneous administration – something emerging therapeutic modalities cannot always match. But these opportunities will be rare and, in the long run, the fast pace of innovation in living technology will catch up to RNAi's delivery advantages.

Forecast & Modeling Insights

(Reduced.)

To be conservative, I have removed fazirsiran from the current model due to the emergence of corrective therapeutic modalities such as RNA editing and DNA editing. Although WVE-006 and BEAM-302 are in the earliest stages of development, each represents a more ideal potential treatment for A1AT deficiency. The fact that two distinct therapeutic modalities have achieved similar promising results de-risks the approach of correcting Z-AAT and suggests neither is a fluke.

The real-world impact is a reduction in the commercial longevity of fazirsiran. Modeling that can get sloppy, especially considering it may not launch on the market until late 2028 at the earliest and competitors have treated just nine patients. Fazirsiran likely has some value, but the pipeline is deep enough where investors can safely exclude it from consideration. If I'm wrong, then it'll only be to the upside.

The impact to the current model is a $787 million reduction in Arrowhead Pharma's estimated fair value ($3.871 billion now vs. $4.658 billion prior).

The most significant events that will impact the model, ranked by earliest expected, are below:

- Lung pipeline: The phase 1/2a study of ARO-RAGE in asthma is expected to be completed in March 2025. That means investors can expect a data readout by mid-2025. My current model doesn't include an asset-specific contribution from ARO-RAGE, but it will be updated with positive results.

- Complement-mediated diseases pipeline: The company reported positive results in the phase 1 study of ARO-C3 in kidney disease in March 2025. Investors can expect to learn of mid-stage development plans for both ARO-C3 and ARO-CFB in the next quarter or two.

- Commercial transition: Plozasiran approval (regulatory), launch and ramp (commercialization), and competitive dynamics against Ionis Pharmaceuticals' Tryngolza (approved in familial chylomicronemia (FCS) on December 19, 2024). The regulatory decision date is November 18, 2025.

- Obesity pipeline: Arrowhead Pharma is likely to present preliminary phase 1 results for ARO-INHBE (liver) and ARO-ALK7 (adipose) by the end of 2025.

- Amgen license: Preliminary phase 3 data readouts for olpasiran in cardiovascular disease. The study is expected to be completed by the end of 2026. Arrowhead sold all rights and royalties to the asset, but can still capture $485 million in milestone payments.

- SHASTA studies: Preliminary data readouts from the SHASTA studies, which are phase 3 clinical trials evaluating plozasiran in severe hypertriglyceridemia. SHASTA-3 and SHASTA-4 are expected to be completed by late 2026, with supplemental approvals possible by late 2027. An upcoming SHASTA-5 study will evaluate plozasiran's ability to reduce acute pancreatitis in patients with severe hypertriglyceridemia, an important label expansion opportunity.

- CAPITAN study: Preliminary data readouts from the CAPITAN study, which is the phase 3 clinical trial evaluating plozasiran in cardiovascular disease. The CAPITAN study is one of the most important long-term de-risking events for Arrowhead, but will not be completed until 2030 or later (my estimate).

Margin of Safety & Allocation

Arrowhead Pharmaceuticals is considered a Growth (Quality) position. The current fair valuation for the company based on my 2025 model is below:

- Market close March 12: $15.77 per share

- Modeled Fair Valuation: $27.77 per share

- Allocation Range: Up to 15%

Arrowhead Pharmaceuticals reported 126.098 million shares outstanding as of February 3, 2025. It sold 11.926 million shares to Sarepta Therapeutics on February 7, 2025. The modeled fair valuation above assumes 139.405 million shares outstanding, which is equivalent to 1% dilution.

Further Reading

- March 2025 press release from Beam Therapeutics announcing early results for BEAM-302

- February 2025 regulatory filing (10-Q) detailing fiscal Q1 2025 operating results

- December 2024 research note evaluating Sarepta Therapeutics licensing transaction

- October 2024 press release from Wave Life Sciences announcing early results for WVE-006

.svg)

-cropped.svg)