.svg)

Warren Buffett has famously raised a record cash position of $325 billion as of September 2024, which represents 28% of Berkshire Hathaway's total asset value. That's the highest since at least 1990, according to The Financial Post.

The Oracle of Omaha argues the market is expensive. In fact, he won't even repurchase shares of his own Berkshire Hathaway at its current level. Almost every valuation gauge you can whip up loudly agrees. Investors can also worryingly see the sudden resurgence of FOMO and meme stocks, which is one of the best predictors of future broken hearts.

More broadly, Buffett argues valuations of great businesses in his sights are stretched, which is a bigger problem when you must deploy tens or hundreds of billions of dollars per acquisition.

Individual investors can always be nimbler than Berkshire. That's especially true when poking around the biotech sector right now, which remains one of the few left out of the U.S. stock market's furious rally.

Would biotech stocks decline further during a broad market downturn? I would expect so. At the same time, I don't see myself regretting buying shares of many companies in my sights near current prices. However, from past experience, I might regret not having more capital to deploy in a correction in the next 24 months.

That's why I've been building a strategic cash position. For every $1 I invest right now, I'm keeping $1 in cash on the sideline.

Navigating an Expensive Market

No single valuation gauge is the end-all, be-all telling investors to pack it up and go home until things cool off. There are always nuances.

For example, one of Buffett's favorite valuation gauge takes the value of the entire U.S. stock market as a percentage of U.S. gross domestic product (GDP). It's even called the "Buffett Indicator." The current value is 208%, which is 67% above the historical average dating back to 1950.

Nerds would also point out the indicator is two standard deviations above the average, which has happened only three times before. These periods ended in market plunges of 42%, 40%, and 19%.

There's no denying the market is expensive based on the Buffett Indicator. However, modern businesses generate more earnings from international operations than ever before. Perhaps comparing the value of the U.S. stock market to U.S. GDP is no longer as tight of a comparison.

While no single metric holds all the answers, almost every valuation gauge is giving the same answer: the U.S. stock market is really expensive.

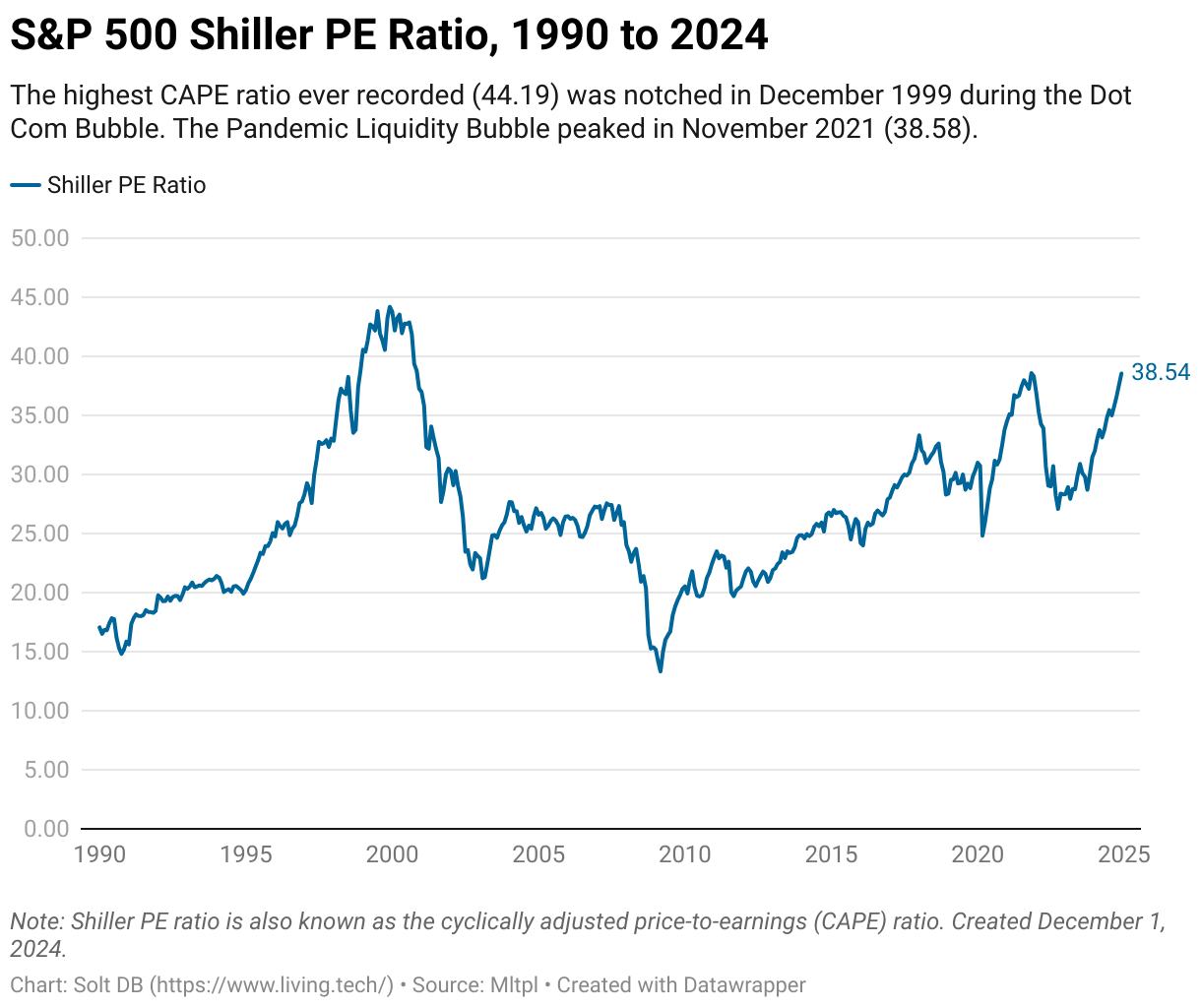

My favorite is the cyclically-adjusted price-to-earnings (CAPE) ratio, also known as the Shiller PE ratio. It compares the current price of a stock or index to the inflation-adjusted earnings over the past 10 years. Essentially, it smooths out booms and busts.

As of November 29, 2024, the S&P 500 has a CAPE ratio of 38.54. That's one of the most expensive ever, topped only by peaks of the Dot Com Bubble (44.19) and the Pandemic Liquidity Bubble (38.58).

The greatest irony to me is that the U.S. stock market corrected when the Federal Reserve began raising interest rates in 2022. All valuation gauges – from the Buffett Indicator to the Shiller PE ratio – began returning to more normal levels.

Then everyone lost their mind about artificial intelligence. Err, what we call artificial intelligence.

Does it contribute any measurable or meaningful economic value? Not in its current form. That's never stopped Wall Street before.

What's more likely is that the largest tech companies have more money than God and cannot risk sitting this one out. What if they don't invest and their competitors stumble upon a useful application? Or gobble up all the talent? Or have Wall Street analysts say nice things about them and not you? Can't have that!

The largest tech companies don't have very many useful ways to spend their enormous cash flows, so although the capital expenditures related to AI are mindboggling and beginning to worry some analysts, there's not much risk to Big Tech for being wrong. In that scenario, they reduce spending on AI and return cash to shareholders as buybacks or dividends.

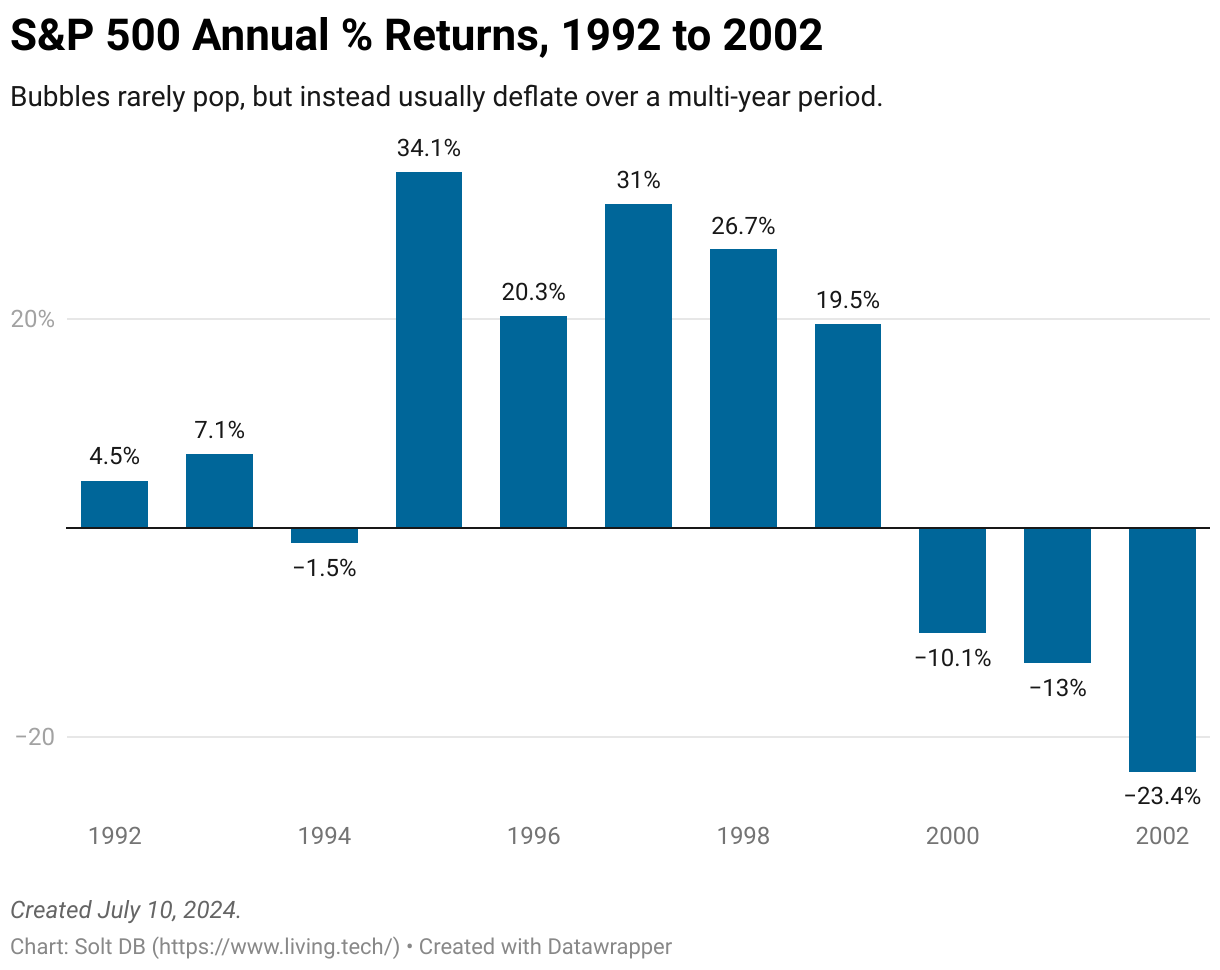

That doesn't mean current valuations are justified. The market will correct eventually, just like it always has when valuation gauges are flashing red. Most importantly, every time the S&P 500 has become too detached from fundamentals in the past, investors have earned lower annual returns from passive investing. Heck, consumer staples outperformed tech for over a decade after the peak of the Dot Com Bubble. Consumer. Staples. It doesn't help that investors had to endure three consecutive years of double-digit declines in its aftermath.

I'm taking the wisdom gained from experience to position my portfolio for outperformance.

The last time I was concerned about frothy market valuations was in 2021. The smartest things I did were manage allocations appropriately and continue plowing money into a stock I couldn't believe was so undervalued. That company, Dicerna Pharmaceuticals, delivered a mixed phase 3 study in August 2021 which tanked the stock. I kept buying.

Now, to be honest, I was a little nervous about making it "such a large position" – eventually topping out at 21% of my portfolio. Gasp! That seemed to go against the conventional wisdom of diversification.

Dicerna Pharmaceuticals was acquired by Novo Nordisk in December 2021, serendipitously occurring just two weeks before the then all-time market peak. I did "the smart thing" and redeployed the capital over the next six months, which seemed great as biotech stocks corrected. The S&P 500 lost 19% in 2022.

If only I knew the biotech winter would drag on for 36 months (and counting), then perhaps I would've adopted an even slower pace.

My biggest takeaways from that experience:

- Concentration isn't automatically bad or risky. In fact, the best investors of all time have very concentrated portfolios, not diversified ones. A lot of investing advice is akin to nutritional advice. Does everyone need 2,000 calories and 275 grams of carbohydrates every day? No, but the government has to communicate that information in a way that can be followed by 340 million mouth-breathing Americans. My ideal portfolio size has shrunk from 15 positions at the time to just my five or six highest-conviction stocks today.

- Don't race your cash position. It was common to hear that cash sitting in your brokerage loses value to inflation, especially in 2021 and 2022. What goes unsaid is that your invested cash also loses value to inflation. It's the same exact exchange of value. But do you know what can never lose 80% of its value in 365 days? The U.S. dollar. Do you know what can easily lose 80% of its value in that span? Biotech stocks. A cash position isn't a wasted position, especially when you primarily invest in volatile growth stocks.

To navigate the current frothy valuations of the U.S. stock market, I'm concentrating into my highest conviction stocks and keeping $1 in cash for every $1 invested. I'll be able to make large purchases during the next inevitable correction, whether that occurs in 2025 or 2026.

A Quick Word on the Margin of Safety

The Margin of Safety (MOS) helps provide an objective sense of what price you should be comfortable paying right now for a given company.

- The MOS is based on the current model.

- The current model is based on what can be responsibly modeled with the information available.

The MOS is an important metric, but it inherently isn't very forward looking. Just because a company has a MOS of "only" X% or XX% and not XXX% doesn't mean it's a worse opportunity in the long run. You also have to consider position sizing and the overall risk profile.

This recently came up with Arrowhead Pharmaceuticals, which I plan to make one of my core portfolio positions of 20% to 25%. Don't dismiss it because it has a Margin of Safety of "only" XX% right now. This should easily ascend to a market valuation in excess of $10 billion by the end of the decade.

A month prior it came up with AVITA Medical. The 2024 model was reduced because the company's growth trajectory was delayed within the current timeframe. That means the price you should feel comfortable paying right now was reduced. But that doesn't necessarily mean the business is flawed or the opportunity is reduced. It was just delayed into the future.

Upcoming De-Risking Events Roundup

Here's a preview of de-risking events to keep an eye on, in order of nearest to furthest:

Arvinas $ARVN

Arvinas will announce preliminary phase 1/2 data for a combination of vepdegestrant (lead drug candidate) and Eli Lilly's Verzenio (abemaciclib) at the San Antonio Breast Cancer Symposium (SABCS) in mid-December. Verzenio is a CDK4/6 inhibitor.

The company is positioning its lead drug candidate as a better selective estrogen receptor degrader (SERD) than fulvestrant, which is the current standard of care. However, Arvinas has monetized the asset by handing the rights to Pfizer. It will use development, regulatory, and sales milestones, as well as royalties, to develop a pipeline of protein degraders in neuroscience indications.

The all-important, head-to-head phase 3 study comparing vepdegestrant to fulvestrant will have a data readout at the end of December or early January.

Relay Therapeutics $RLAY

Relay Therapeutics is advancing its own SERD to a status of investigational new drug (IND) application ready, but it may be waiting to see how the competitive landscape develops. There's value to owning each slice of the treatment paradigm, but RLY-2608 could be valuable as the foundation for the industry's breast cancer combinations, too. That would have the added benefit of saving R&D expenses for more diverse bets.

The company's SABCS presentation is expected to announce the preliminary phase 1/2 data for the initial RLY-2608 triplet. In September 2024, data presented for the RLY-2608 doublet with fulvestrant set a high bar for the competitive landscape. The triplet adds a CDK4/6 inhibitor into the mix, which will be important for earning approvals in the large first-line treatment setting.

The opportunity is large. Roche recently earned approval for its own PI3K-alpha inhibitor, Itovebi, as part of a similar triplet with a SERD and CDK4/6 inhibitor. The company's own management estimates Itovebi has a $2 billion peak sales opportunity in that treatment setting alone.

Investors already know RLY-2608 is likely to be more effective and safer than Itovebi, which could create compounding advantages when paired with CDK4/6 inhibitors. This month's data readout will offer the first test of that hypothesis.

Keep in mind that CDK4/6 inhibitors have their own toxicity issues, so realizing the true potential of a PI3K-alpha and CDK combination might require next-generation assets. Relay Therapeutics expects to initiate a new study cohort evaluating RLY-2608 in a new triplet with fulvestrant and Pfizer's atirmociclib, a novel CDK2 inhibitor with greatly improved tolerability, before the end of 2024. It will be the first time the asset is studied in a triple combo regimen.

Arrowhead Pharma $ARWR

Given the breadth of Arrowhead's technology platform, I suppose it'll be listed in the "upcoming de-risking events" section for every Members Digest.

Fresh off a licensing deal with Sarepta that will earn the RNAi specialist $1.125 billion in the next 12 months, the company should soon begin its first phase 1 study in obesity for ARO-INHBE.

Investors shouldn't think the company is done monetizing assets, either. Although plozasiran won the battle against zodasiran for advancing into a large-scale cardiovascular disease clinical trial (that's the approval that will launch Leqvio to blockbuster status, the first RNAi drug product to achieve that level), zodasiran still has value.

That's especially true since zodasiran is significantly better than plozasiran at reducing remnant cholesterol, which is an emerging biomarker for several rare and common cardiometabolic diseases. The right partner – or even a newly-formed company built around the asset – could find it valuable.

AVITA Medical $RCEL

AVITA Medical expects to earn 501(k) clearance for Cohealyx, a collagen-based dermal matrix that can be used in larger burns and wounds together with the ReCell platform, by the end of 2024. The product would launch in early January 2025 and represents another arrow in the quiver to provide a full spectrum of wound care products.

Then again, the business generated just $0.7 million in revenue from other wound care products in the first nine months of 2024. There's a ways to go.

Coherus BioSciences $CHRS

Coherus has a relatively rich slate of de-risking events in the next six months thanks to pipeline developments.

The company expects to begin a new phase 2 study for a casdozo triplet with toripalimab and an anti-VEGF therapy in a type of liver cancer, report phase 2 data for the pre-toripalimab triplet in the same type of liver cancer, initiate a phase 1 combination study with CHS-114 (CCR8 inhibitor) and toripalimab in Q1 2025, and report phase 1/2 data for the casdozo and toripalimab combination in non-small cell lung cancer by mid-2025.

I'll be patiently awaiting the preliminary phase 1 data readout for CHS-114 expected by the end of 2025.

Verve Therapeutics $VERV

The CRISPR base editing pioneer expects to announce preliminary phase 1b data for VERVE-102 in the first half of 2025.

Finch Trades Review

Finch Trades are how I share my real-world investing transactions in real time with members.

- Each transaction confirmation is shared on Discord as soon as the transaction closes, so I cannot cherry-pick my track record. Follow-up research notes are published soon after.

- The all-time returns of Finch Trades will be reported vs. what would've happened if I invested in the S&P 500 instead. I want to demonstrate biotech investing can outperform a passive investing approach when used in conjunction with my modeling and the Margin of Safety Dashboard.

- The all-time returns of Finch Trades are dollar-weighted. This differs from a stock recommendation service where each "pick" is equally weighted. I think Finch Trades better reflects real-world investing.

As of market close on Friday, November 29, 2024, Finch Trades are underperforming the S&P 500 by 28%.

Finch Trades has deployed $18,721 of capital since initiation in April 2024. That principal has declined 16% to $15,676 in that span. It would've grown to $20,985 (+12%) if I invested in the S&P 500 instead.

This is the initialization period. As poor as it looks, the comparison is impacted by two things.

First, the S&P 500 is up 20% since the first Finch Trade on April 25 – just 220 days ago. The index is up 10% since a Finch Trade on September 5 – just 87 days ago. In fact, 64% of deployed capital is being compared to double-digit gains for the index. This will not matter once the invested positions have more time to reach important inflection points.

Second, 84% of deployed capital sits in Coherus BioSciences (cost basis $1.84 per share) and Relay Therapeutics (cost basis $5.80 per share). I'm not complaining because these positions will drive outperformance in future periods. For example, if Coherus BioSciences rises to $2.45 per share (a market cap of $282 million), then Finch Trades overall will match the S&P 500's performance.

As previously communicated, I plan to deploy my 2025 IRA contribution of $7,000 into Coherus BioSciences in early January.

I plan to publish a dashboard tracking Finch Trades in real time, similar to the current Margin of Safety Dashboard, in the first half of 2025.

.svg)

.png)

-cropped.svg)