.svg)

I always find it amusing when high-growth companies emphasize notching "record revenue" each quarter. Well, no shit. If a business is in growth mode, then each quarter should represent a new high watermark. It seems redundant.

Then along came AVITA Medical.

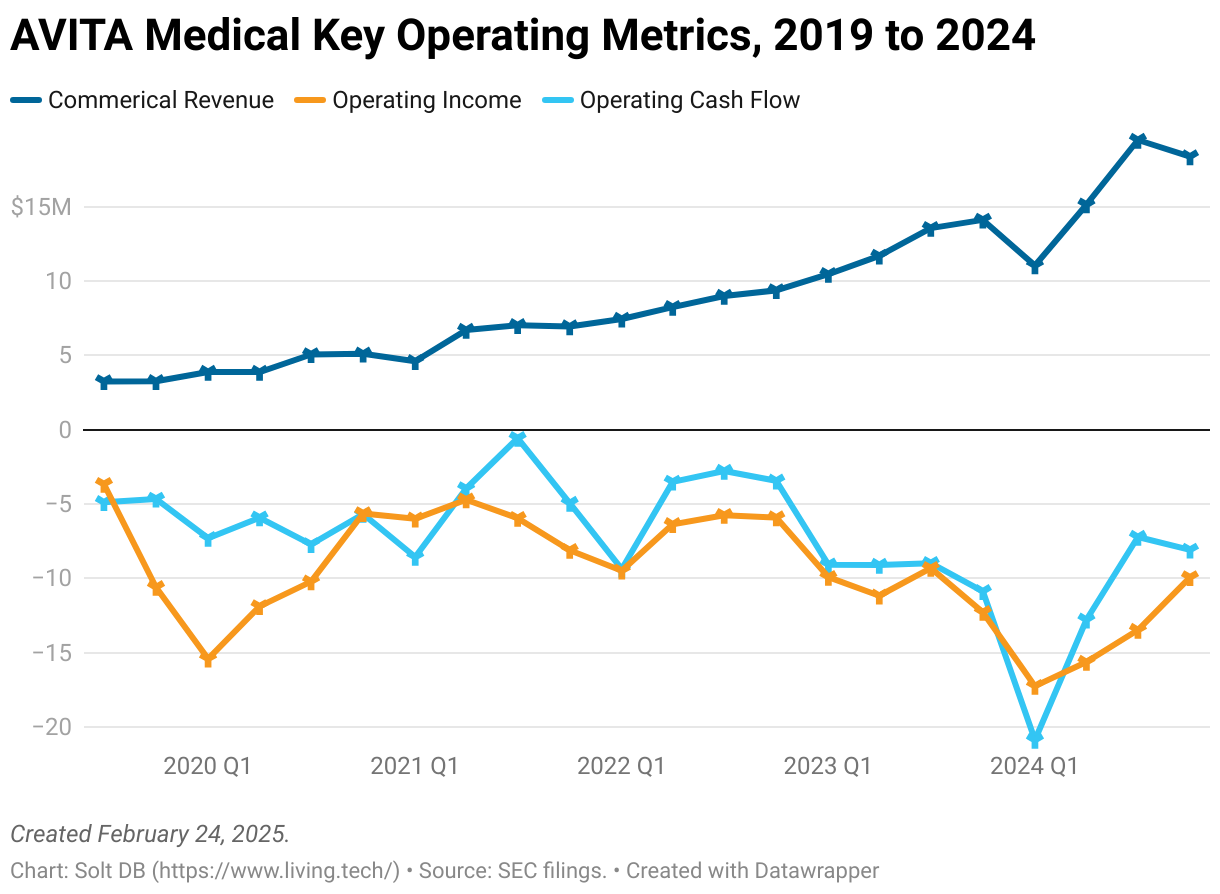

The company reported eight consecutive quarters of sequential revenue growth from Q4 2021 to Q4 2023 – each marking a record level of sales, of course. But a slower-than-expected rollout of its suddenly larger sales force and hospital red tape sabotaged that streak to start 2024. Although it returned to growth during the second and third quarters of last year, missing revenue guidance in the final frame of 2024 worsened the wobbly trust analysts and investors were beginning to rebuild in management.

AVITA Medical looks to recover in its 2025 campaign. To firmly regain the trust of market participants, the business needs to establish durable momentum that can carry into future years. To do that, management needs to meet annual revenue guidance by delivering revenue growth of 61% – easily a record.

This might be the last chance CEO Jim Corbett is given to turn his high-growth vision into reality. If the business stumbles again, then it could permanently damage the relationship with analysts. More concerning, a precariously short cash runway could cause more existential problems.

By the numbers

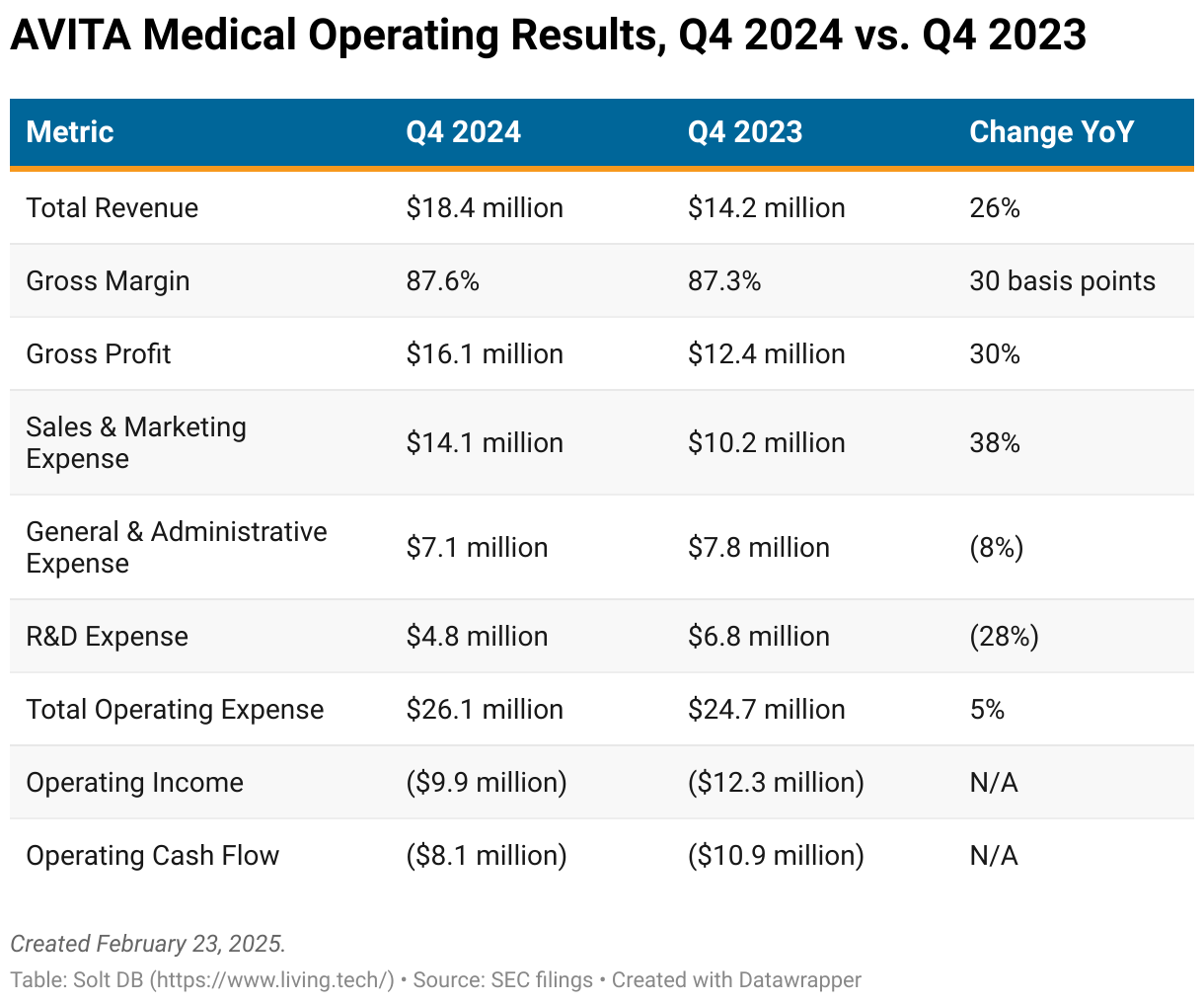

The wound-care specialist originally expected to achieve fourth-quarter 2024 revenue of $23.3 million at the midpoint. It ended up achieving just $18.4 million, which missed by 21%. The embarrassing performance was compounded by even simpler math: the business generated less revenue than the prior quarter. Again.

Not very "high-growth mode," eh?

Whiffing on revenue guidance for the second time in four quarters shouldn't be dismissed easily. Although the provided reasons are plausible, if it happens again, then investors will need to question why this management team is fit for the job.

It wasn't all bad news.

For the full year, AVITA Medical still achieved year-over-year revenue growth of 29% in 2024. That's strong. It only seems disappointing because management set expectations even higher.

The business demonstrated solid fiscal restraint during the fourth quarter, which could help create much-needed momentum in 2025. Total operating expenses of $26.1 million in Q4 were the lowest of 2024 and 18% lower than my model. Gross profit margin of 87.6% easily trounced my modeled value of roughly 80%, although the outperformance was driven by slower-than-expected traction for non-ReCell products, which have lower margins.

Higher margins and lower expenses are always a sweet combination. AVITA Medical's Q4 2024 operating loss of $9.9 million was 42% better than my model's expected outcome. If the business can keep it up – and delivers the promised growth trajectory – then it should turn cash flow positive in 2025.

Management expects to achieve full-year 2025 revenue of $103 million at the midpoint, free cash flow in the second half of the year, and GAAP profitability in the fourth quarter of the year. In a sign the team is learning from recent mistakes, it did not provide quarterly revenue guidance for Q1 2025.

New Launches Promise Growth, but Recent Launches Contribute Little

AVITA Medical has furiously added new products and geographic territories to fuel its growth push. But aside from ReCell GO and the United States, these efforts are contributing surprisingly little revenue.

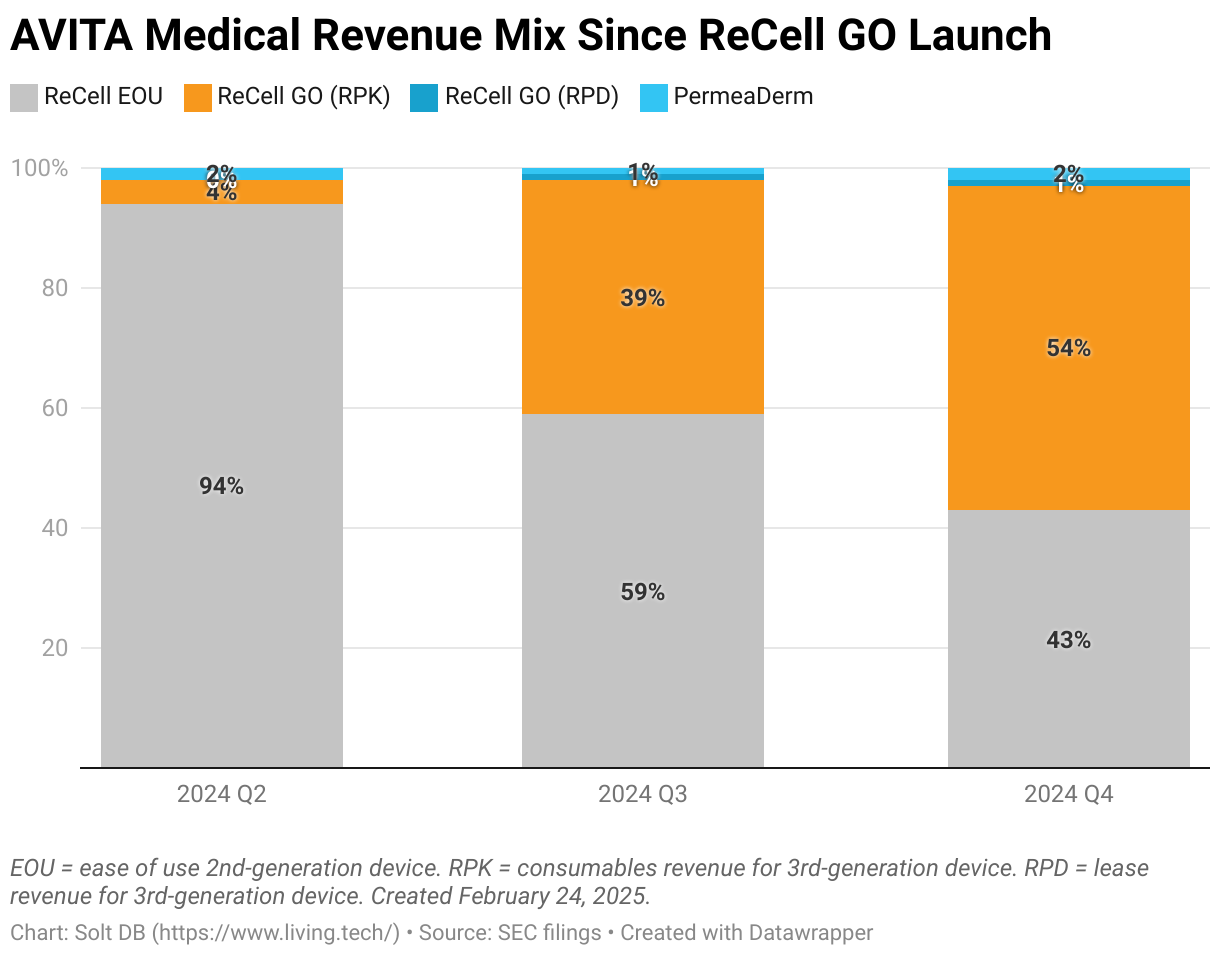

The second-generation ReCell device, called "ease of use" (EOU), generated 43% of total Q4 2024 revenue. It will be phased out this year. The third-generation device, called ReCell GO, generated 54% of total revenue during the period. The transition to new devices is progressing as expected.

However, total revenue generated from ReCell devices stood at 97% in the final quarter of 2024. The branded wound dressing PermeaDerm – the first product brought in to capture more value from the full wound care spectrum– was responsible for just 2%.

Make no mistake: ReCell GO will be the dominant source of revenue for the rest of the decade. But investors want to see new products gain traction more quickly to provide meaningful diversification.

Consider a typical burn or wound covering 10% total body surface area (TBSA). PermeaDerm will generate an estimated $2,000 in revenue per patient procedure. That's less than the $6,500 for ReCell GO, and wound dressings aren't applied during every procedure, but PermeaDerm should be more than 2% of total revenue.

A slow start for the new dermal matrix product Cohealyx would be more challenging to overcome. Whereas PermeaDerm protects the surface of a treated wound and ReCell aims to replace the skin just below the dressing, dermal matrix products provide structural support for cells during the healing process. Cohealyx would be placed into a wound bed first, then skin cells from ReCell GO would be applied, and finally PermeaDerm on top.

For the same burn or wound procedure treating 10% TBSA, Cohealyx could generate $20,000 in revenue. It won't be used in every procedure, but it represents a meaningful opportunity to capture more value from each procedure. AVITA Medical's ambitions don't end with PermeaDerm or Cohealyx. Management is also exploring adding products to aid wound depth assessment, antimicrobials for protecting the wound bed, aiding blood clotting in the wound bed, and scar reduction.

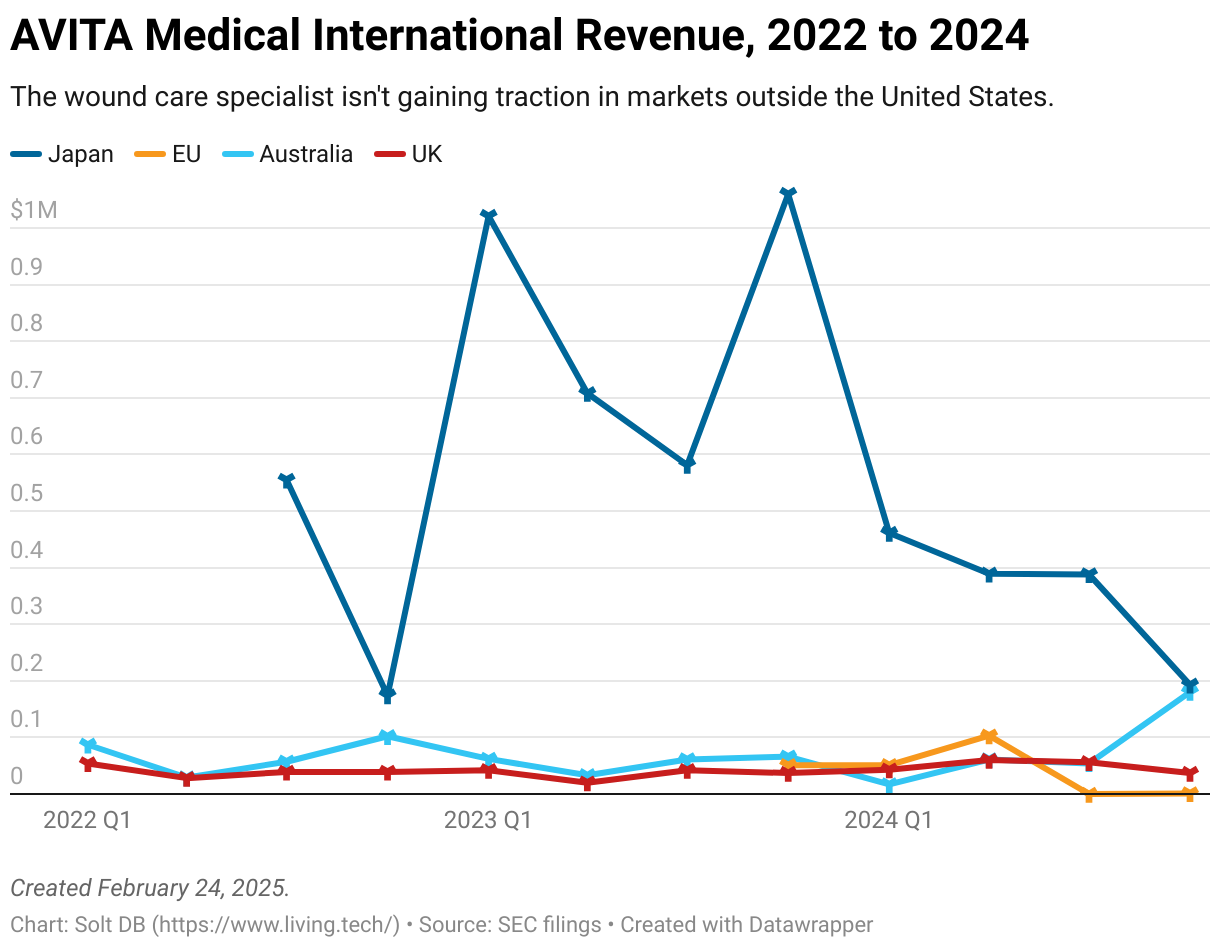

In addition to sluggish launches from new products, the company's international expansion into Japan and Europe isn't bearing fruit. AVITA Medical generated its second-worst quarterly revenue in Japan since launching 10 quarters ago and generated just $1,000 in Europe in the entire second half of 2024.

Forecast & Modeling Insights

(Unchanged from January 2025.)

My original 2025 model introduced last November expected at least $145 million in annual revenue. I wasn't even close!

The current model was introduced (without a research note) in January when AVITA Medical ripped off the Band-Aid for missing its own guidance. The current model remains unchanged after full-year 2024 results were officially reported in February.

My 2025 model expects:

- Full-year 2025 revenue of $110 million, representing year-over-year growth of 70%. The business exits the year with roughly $35 million in quarterly revenue.

- Full-year 2025 gross profit of roughly $88 million. Gross margin of roughly 82% is lower than 2024 as lower margin products generate more revenue, partially offset by higher margins for ReCell GO.

- Full-year 2025 operating loss of $18.6 million. The business generates roughly $1.5 million in operating income in Q4 2025.

To reiterate, investors shouldn't dismiss missed guidance. But instead of looking at revenue guidance ($103 million at the midpoint) as a sign management hasn't learned its lesson with past overpromising and underdelivering, I think guidance is an attempt to underpromise.

If the business comes close to breakeven in Q4 2025 as guided, then it'll need at least $35 million in revenue that quarter. That assumes a conservative 80% gross margin and $27.5 million in quarterly operating expenses.

The ramp of ReCell GO – and the high-margin consumables each device generates – will drive revenue growth in 2025. The business generated only 54% of revenue from the new device in the final frame of last year, which means there's plenty of untapped optimization remaining.

The launch of ReCell GO Mini, designed to be used for wounds one-quarter the size of typical ReCell GO procedures, should add meaningful uplift. Unlike PermeaDerm or Cohealyx, investors shouldn't have much doubt the product can ramp quickly. Meanwhile, if Cohealyx launches as expected in Q2 2025, then it should generate at least $5 million in quarterly revenue by the end of the year, given current procedure volumes that would require a dermal matrix.

How might my 2025 model or management's guidance fall apart?

Hospitals continue to reel from a pandemic hangover, which has kneecapped budgets and resulted in severe staffing shortages. Although ReCell GO is designed to enable hands-free operation in the operating room, a lack of skilled nurses poses a headwind. Myself and management could be underweighting this factor.

It's also possible for Cohealyx to encounter a delay in commercial uptake or reimbursement. An ongoing study intends to generate real-world data from human patients (the product was cleared using animal studies only), but results may not live up to expectations or convince surgeons to use the product.

Margin of Safety & Allocation

AVITA Medical is considered a Growth (Quality) position. The current modeled fair valuation for the company based on my 2025 model is below:

- Market close February 25: $9.41 per share

- Modeled Fair Valuation: $18.83 per share

- Allocation Range: Up to 15%

AVITA Medical reported 26.358 million shares outstanding as of February 7, 2025. The modeled fair valuation above assumes 30.311 million shares outstanding, which is equivalent to 15% dilution.

Further Reading

- February 2025 press release announcing Q4 2024 operating results

- February 2025 regulatory filing (10-Q) detailing Q4 2024 operating results

- November 2024 research note discussing the importance of ReCell GO

.svg)

.svg)

-cropped.svg)