.svg)

Sharing is caring. Unless you're AVITA Medical. In that case, sharing more information just leads to more questions.

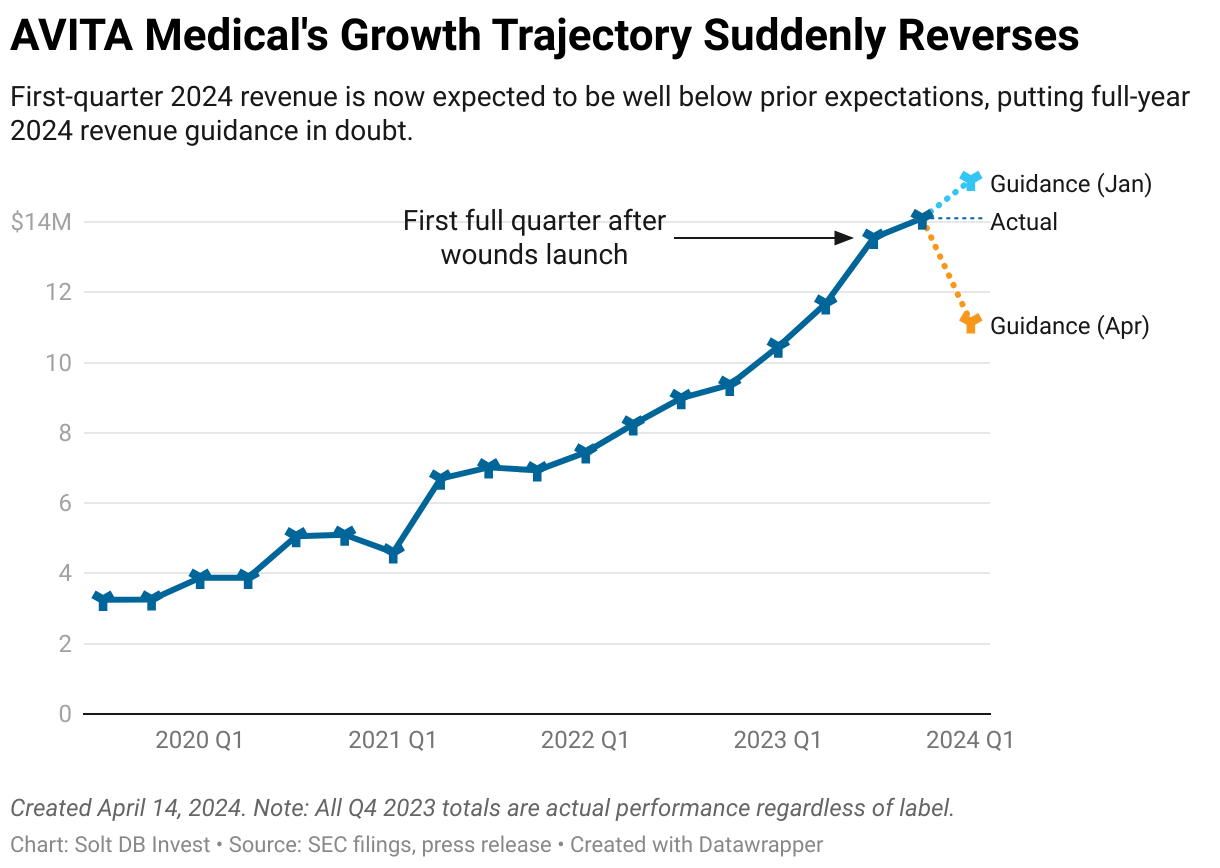

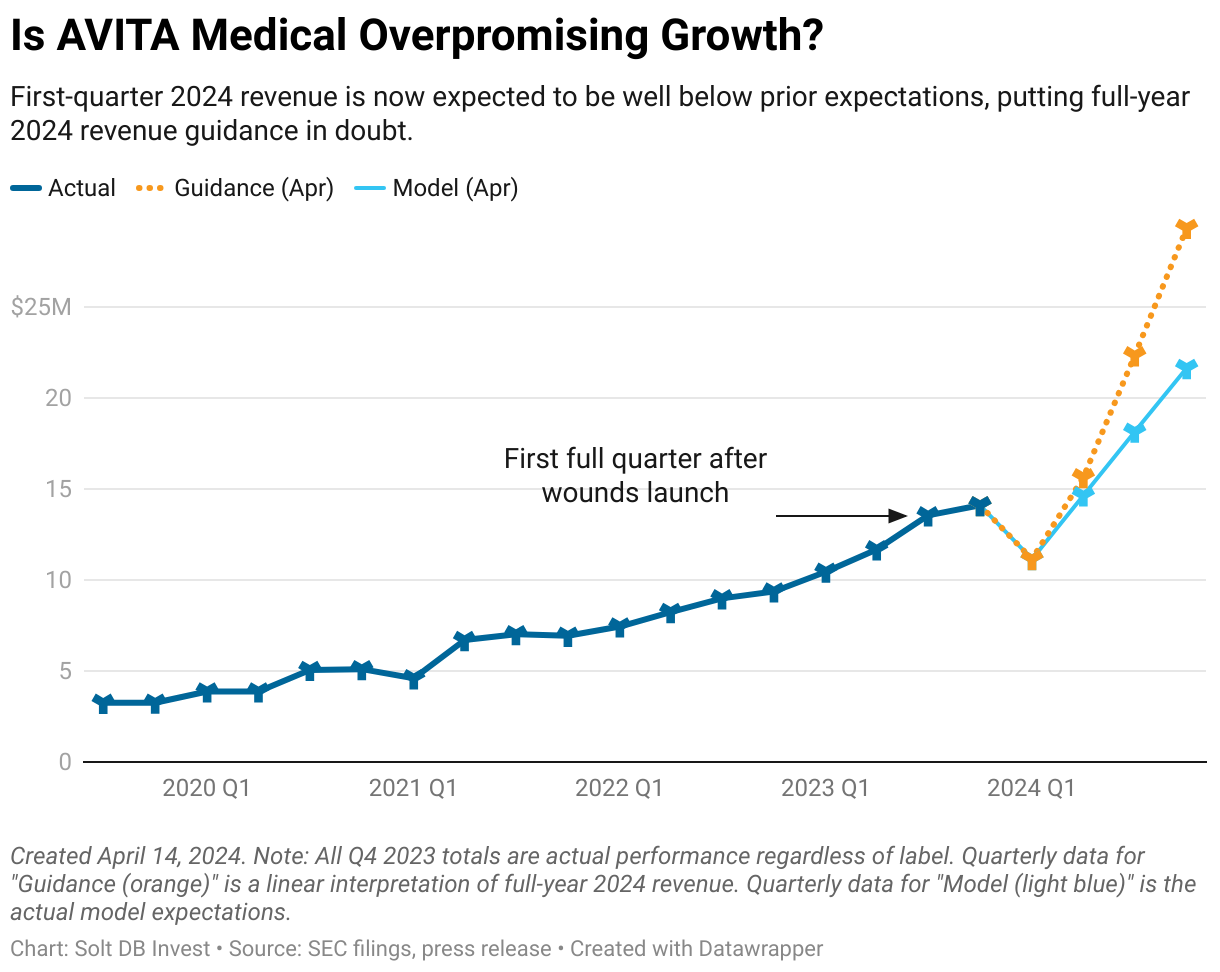

The medical device company announced it will come well short of first-quarter 2024 revenue expectations. In fact, revenue will be the lowest since the first quarter of 2023 and lower even than the quarter directly before ReCell System launched in wounds. That's a little odd, but it gets even weirder.

Management explained longer-than-expected value analysis committee (VAC) processes as the primary growth bottleneck, but shared numbers from the account pipeline suggesting the problem runs a little deeper than that. Those same numbers show AVITA Medical was well off its internal growth trajectory at the end of 2023, but didn't reset account goals before issuing 2024 guidance.

Essentially, the company set itself up for failure by assuming the growing gap could be made up in subsequent periods. That's a great way to quickly demoralize your sales team.

Most important, none of that explains why first-quarter 2024 revenue will be the lowest since ReCell System launched in wounds.

A Curious Math Problem

In February 2024, AVITA Medical told investors to expect first-quarter revenue of $15.2 million. That would mark the ninth consecutive quarter of growth and a quarterly record to boot. It would also suggest the company needed to execute very well in subsequent quarters to meet full-year guidance, but at least it was a reasonable number. The growth trajectory both to and from $15.2 million made sense.

Management now expects first-quarter revenue of just $11.2 million, which is 27% lower than initial guidance. It's also 5% lower than the sales achieved in the second quarter of 2023, which was the last full quarter before the launch in wounds.

Management explained the disappointing performance to start the year by stating, "The revision in guidance is attributable to a slower-than-expected conversion rate of new accounts for our expanded label of full-thickness skin defects." But the numbers it offered as an explanation create more questions than answers.

- A slowdown is one thing. But why is first-quarter 2024 revenue expected to be lower than pre-launch revenue?

- AVITA Medical says it added 73 new accounts since launching in wounds, including 22 during the first quarter of 2024. How is there meaningful account growth and declining revenue?

- Additionally, it's been nine months since launch, which suggests accounts aren't being added any faster now than immediately after launch. Nine months is three quarters. If 22 accounts were added in Q1 2024, then about 25 accounts were added in each Q4 2023 and Q3 2023.

Management then shared more detailed account metrics in an attempt for transparency, which only leads to more questions.

AVITA Medical says it ended March 2024 with 71 submissions in the evaluation or decision stage of the VAC process. That's a healthy amount – converting most would roughly double the number of accounts added since launch in wounds. Converting most would also mean the company has penetrated over one-third of the 800 targeted accounts across both burns and wounds.

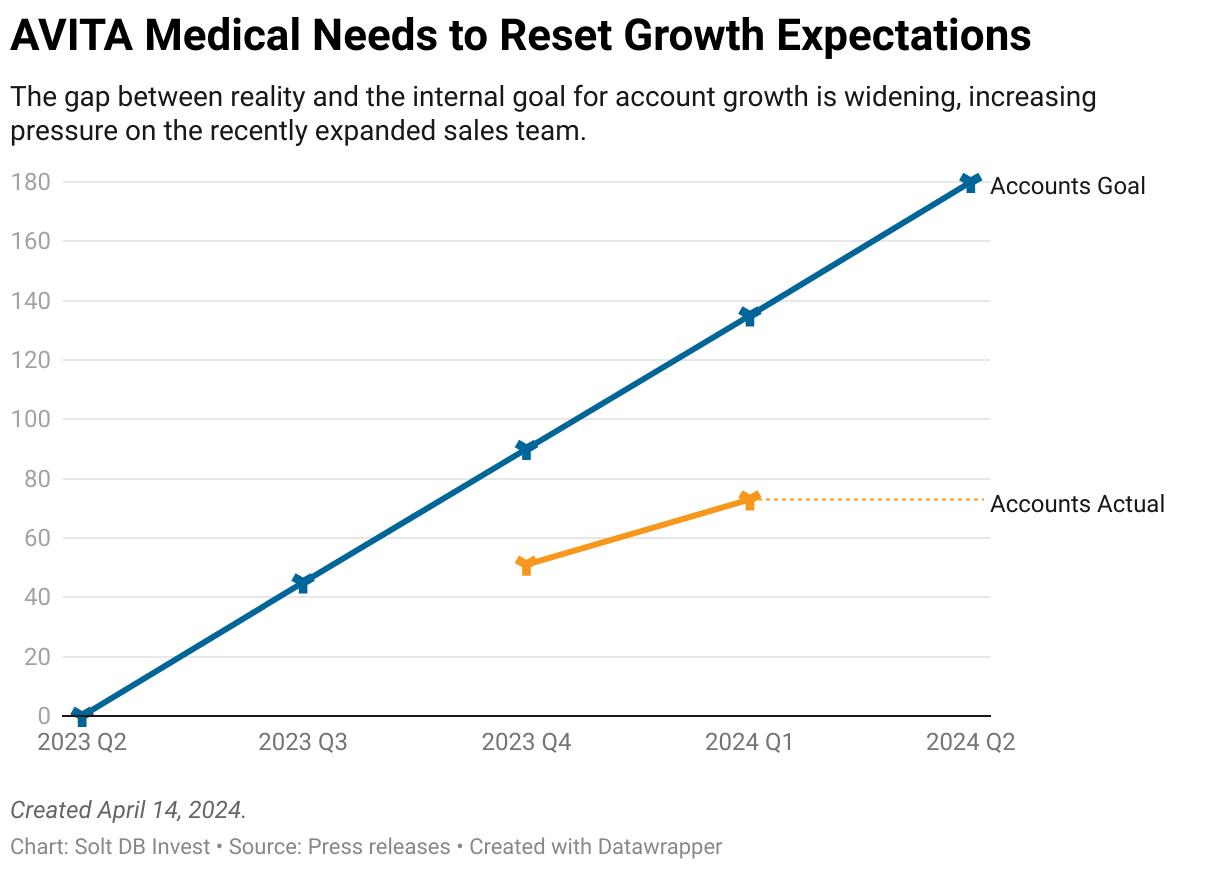

But management followed that by stating it expected to add 15 accounts per month from launch, adding it expected to end March 2024 with about 135 new accounts total. This was a dumb thing to admit.

Not only was the company well off its goal for the end of March (73 new accounts actual vs. 135 new accounts expected), but it wasn't very close to its goal for the end of 2023 either (51 new accounts actual vs. 90 new accounts expected). Why didn't the company reset its growth expectations before setting full-year 2024 revenue guidance?

On the third-quarter 2023 conference call in November 2023, management stated it had over 100 prospective accounts at various stages within the adoption process. The most recent figure (71 submissions) specifically refers to account prospects in the final two stages of the adoption process, so it's unclear if these two metrics can be directly compared.

Investors will certainly need more of an explanation on the upcoming first-quarter 2024 conference call in May. Until then, we can put some pieces together.

What Likely Happened

For starters, management was obviously too aggressive with expectations for account growth. A hospital VAC process typically takes three to six months. It's only been nine months since the launch in wounds, so it's too soon to say whether the process is taking longer than six months or if management expected the process to take less than six months. Perhaps a combination of both.

One thing that's likely complicating the VAC process for ReCell System is the advantageously broad approval covering full-thickness skin defects. It covers surgical wounds for cancer patients, gunshot wounds, bacterial infections, industrial accidents, and many more acute injuries. That's awesome for growth, but a nightmare for committee deliberations.

A VAC brings together stakeholders from across the clinical spectrum and supply chain, including physicians, nurses, risk analysts, administrators, and others. The goal is to confirm clear clinical and economic benefits from using a product.

Although AVITA Medical's clinical trial clearly demonstrated a clinical benefit, it didn't specifically conduct an economic analysis study for ReCell System in wounds. It did so for burns and is doing so for stable vitiligo. This could be holding up VAC decisions.

This could also explain the surprisingly low revenue for the first three months of the year. To grease the wheels of bureaucracy, AVITA Medical might be giving free product to hospitals bogged down in the VAC process for real-world trials on site. This is a common practice for medical equipment sales, but it sacrifices revenue generation during the conversion process in a bid to convert customers.

Forecast & Modeling Insights

(Reduced 2024 model.)

AVITA Medical reiterated its initial full-year 2024 revenue guidance range of $78.5 million to $84.5 million, specifically stating it believes it can still meet the lower end of the range.

My previous 2024 model expected annual revenue of $77.59 million. Given the slow start to the year, I'm revising that to $65.60 million. That still represents 32% growth from 2023 – and it excludes any contribution from ReCell Go or PermeaDerm matrix products.

As of this writing, I'm not willing to assume slower-than-expected VAC processes can be corrected quickly enough to get the business back on its previously expected growth trajectory. I see no reasons to believe the overall growth opportunity is diminished, but it will take longer to achieve.

Here's my current thinking.

How AVITA Medical Can Get Back on Track

The sales process for ReCell System in full-thickness skin defects is more complex than burns – management isn't lying about that. Investors simply need to see the most realistic growth projections for the road ahead.

If there's no hope of returning to a 15 account per month trajectory, then management needs to admit it was wrong and reset sooner than later. I'm not sure investors or Wall Street would be disappointed with 30% revenue growth in 2024 – it's only disappointing when compared to the lofty expectations set by management.

I don't think the total growth opportunity has changed, I just think it will take longer to achieve.

AVITA Medical remains on solid footing. It has a great product for treating acute wounds (both burns and skin defects) with gross margins of over 84%. A slower-than-expected growth trajectory could scramble the timeline for achieving positive cash flow and profitability, but both milestones appear to be a question of when and not if.

Other sources of revenue growth and margin expansion remain in place. Expanded approvals in Japan, new distribution deals in Europe, the upcoming launch of ReCell Go, and launch of PermeaDerm matrix products will all contribute to revenue growth in 2024.

How AVITA Medical Can Go Off the Rails

Investors probably won't receive more detailed information about the sales pipeline, such as how the company defines prospective accounts, the number of accounts at different stages of conversion, and whether VAC deliberations are requesting additional information. If AVITA Medical is struggling to build a sales pipeline, then that might lead to lingering challenges for growth.

The business expanded its commercial sales team from 30 to 70 reps in the second quarter of 2023, right ahead of the launch in wounds. That appeared to have been paying dividends until the surprising first-quarter 2024 revenue expectation was dropped on investors. The company was so confident in the growth opportunity it even planned to expand to 100 sales reps in the first half of the year. Is that still the plan? Does it still make sense to be so aggressive?

If AVITA Medical is struggling to build a sales pipeline and still expands the sales team, then that will likely lead to another implosion in the future. There are only so many trauma centers and hospitals in each geographic area, so adding more sales reps won't necessarily lead to more growth, especially if VAC processes are bogging down account conversions.

If, for some reason, the growth opportunity in full-thickness skin defects isn't as large as expected, then that would complicate the path forward for the business. The stock price was beginning to factor in important future milestones, like reduced cash burn and profitability, that were to be driven by high-margin revenue growth. Remove that and there's bound to be a bumpy road ahead.

Margin of Safety & Allocation

AVITA Medical is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close April 12: $9.88 per share

- Modeled Fair Valuation: $13.60 per share

- Allocation Range: Up to 15%

AVITA Medical reported 25.707 million shares outstanding as of February 7, 2024. The modeled fair valuation above assumes 29.563 million shares outstanding, which is equivalent to 15% dilution.

Further Reading

- April 2024 press release resetting first-quarter revenue expectations

- February 2024 research note discussing full-year 2023 operating results and initial 2024 guidance

- January 2024 research note discussing initial 2024 guidance

.svg)

-cropped.svg)