.svg)

Death, taxes, and dilution. These are the inescapable realities in the life of a biotech investor.

Drug development is an expensive and (currently) inefficient activity. It often takes nearly a decade to design a drug candidate, nudge it through clinical trials, and go to regulators with hat in hand requesting approval.

Oh, and then companies have to figure out how to sell the thing. Drug developers often see worse operating losses in the first one to two years after launching their first approved drug product. That's because building commercial infrastructure to sell a drug product requires a significant investment, and the first time you build it there's a big lag before payoff.

But what if I told you that dilution can be properly managed. Entrance into the matrix not required.

Drug developers with shareholder-friendly management teams carefully manage cash runways between data readouts. If de-risking events are favorable, then a stock should become more valuable. If a stock is more valuable, then a business can raise more money with less dilution.

Let's explore the art of the biotech raise. That's followed by a review of eight recent de-risking events, a preview of six upcoming de-risking events, and a progress report on Finch Trades performance during the initialization period.

The Art of the Biotech Raise

Properly managing a cash runway is relatively straightforward for any business.

- Rule 1: Don't get cute.

- Rule 2: That's it.

In drug development, every company has key assets. When those key assets have important data readouts, then the stock has more to gain or lose.

Management cannot see results from ongoing studies, but it does have the results from meaningful milestones a week or so before sharing them publicly with investors. That's plenty of time to prepare a public stock offering the day after a data readout, especially if you know the results are positive or likely to be interpreted as such.

That's because the immediate share pop in all the excitement might prove less durable than you think, so better to "not get cute" expecting shares will keep rising. Just take the opportunity to favorably price an offering when you have the chance. This helps in periods when your company's shares are obviously overvalued and when broader market conditions are at heightened risk of deteriorating.

When Shares are Obviously Overvalued

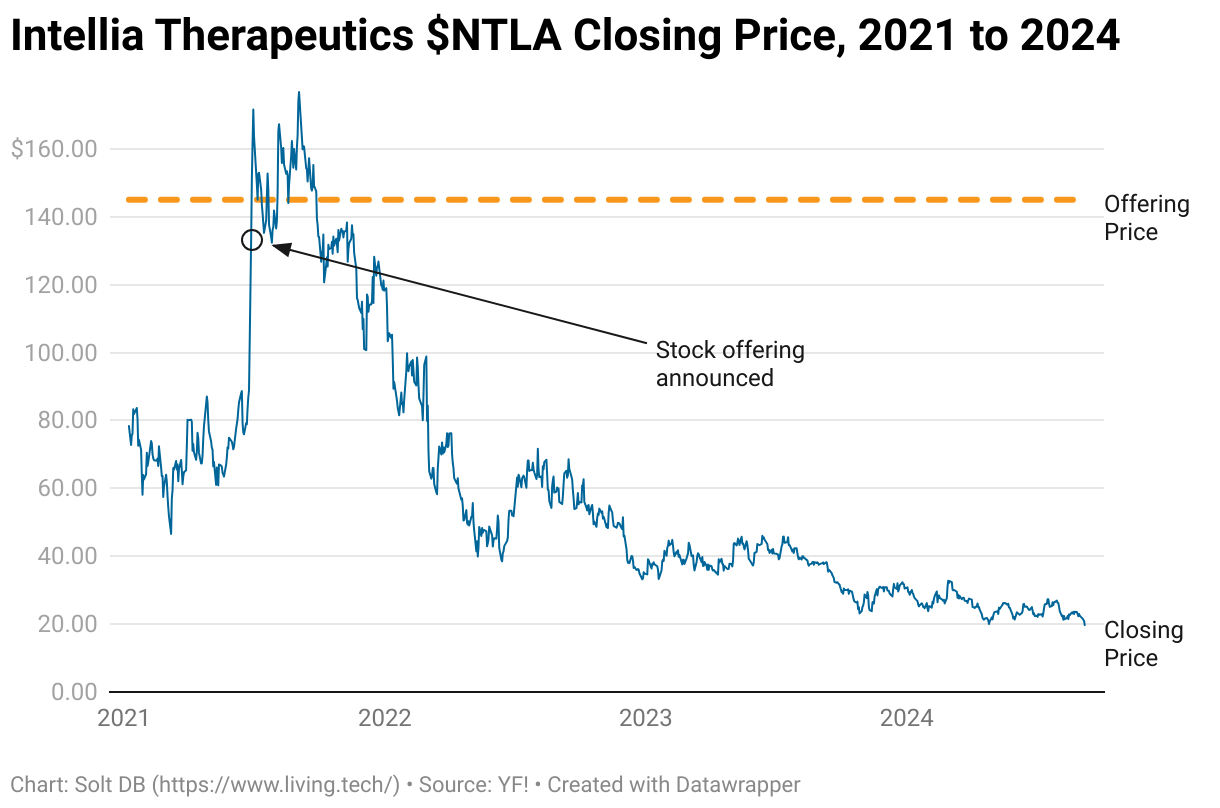

Intellia Therapeutics boasts one of the best-timed "Don't Get Cutes" of all time. In June 2021, a weekend data readout launched the stock into the stratosphere by valuing the business at $12 billion. Twelve. Fucking. Billion. Dollars. CEO John Leonard isn't dumb. The next day he ran those money printers full throttle and raised $690 million at $145 per share.

Legendary decision.

Shares dropped below $100 apiece seven months later and sit below $20 per share right now. By issuing obviously overvalued shares the day after a data readout, management needed to sell just 4.7 million shares to haul in $690 million in June 2021. The company would need to issue 46 million shares to raise that today. Forty-six. Fucking. Million. Shares. Told ya CEO John Leonard isn't dumb.

When Broader Market Conditions are at Heightened Risk of Deteriorating

Even when shares aren't obviously overvalued, the market might have other plans for you and that nice little biotech company you have there. Best to not get cute, take advantage of the immediate share pop in all the excitement, and extend your cash runway. You might need it more than you think.

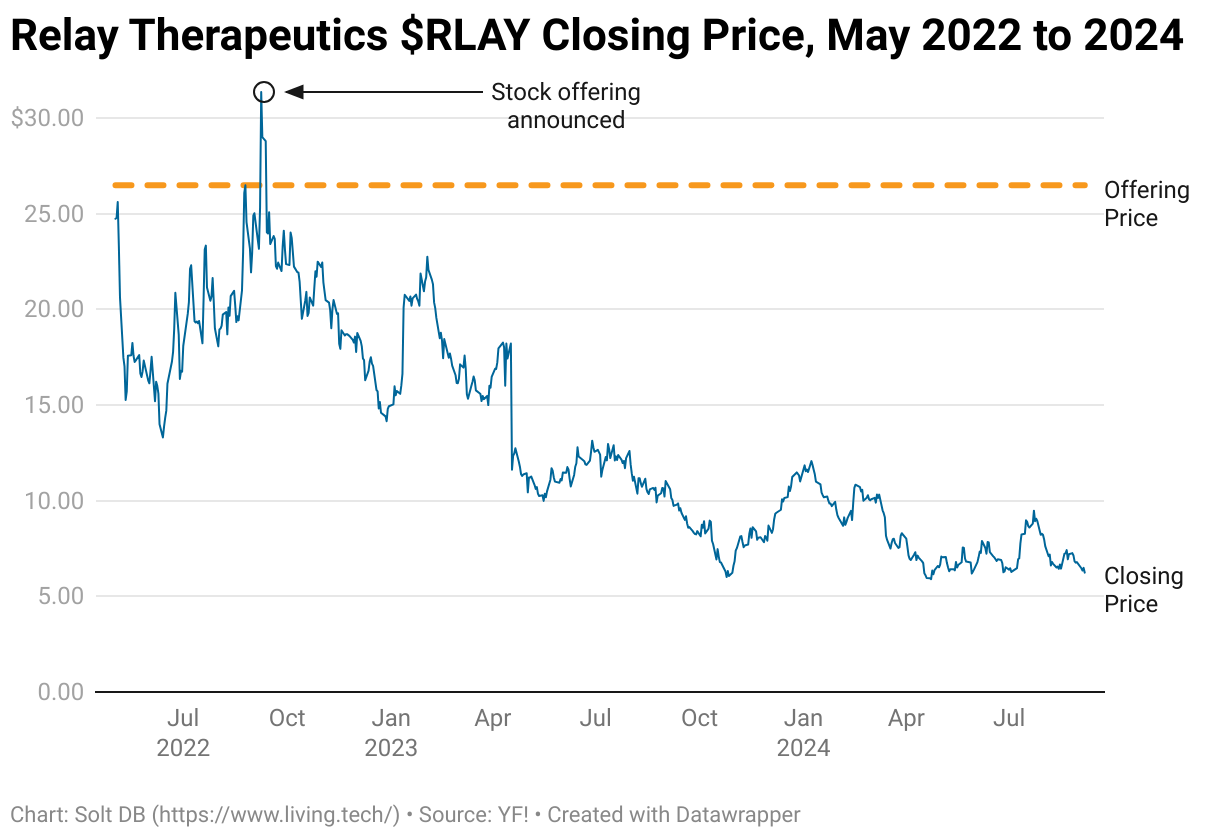

In September 2022, Relay Therapeutics delivered a knockout blow to the competitive landscape with data for its FGFR2 inhibitor lirafugratinib. Shares rose to $31 apiece leading up to the conference that management had teased as the forum for the data readout. That level sure sounds marvelous right now, but it was also a year-to-date high in late 2022. That was a very volatile year as the sector began the long come down from frothy bubble peaks. It was so long of a trek down that some might argue we're still walking today!

By issuing shares the day after a data readout during a period of broader market turbulence, management needed to sell just 13 million shares to haul in $345 million in September 2022. The company would need to issue 76.7 million shares to raise that today.

How Do More Recent Examples Stack Up?

Recent trends hint that companies are starting to be rewarded for extending their cash runways following data readouts. That's a nice reprieve from the relentless decline in biotech stocks in recent years.

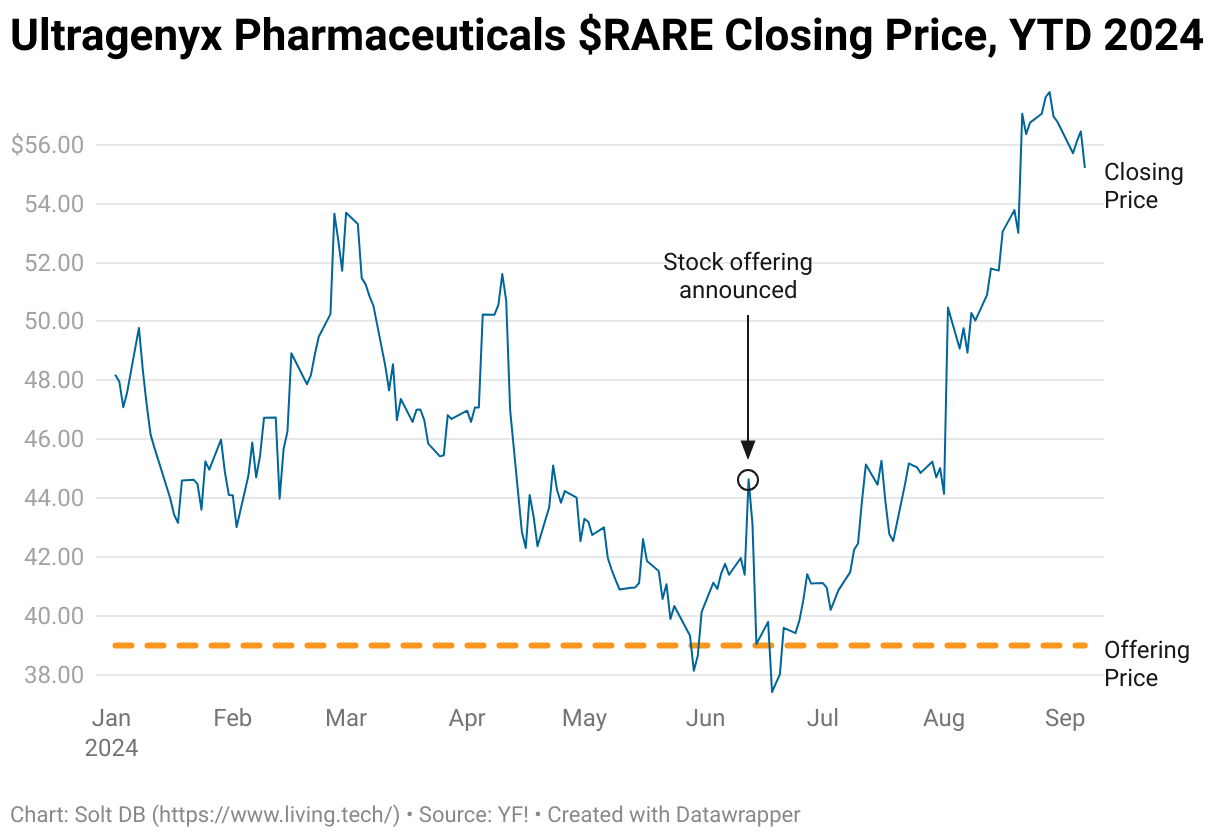

In June 2024, Ultragenyx Pharmaceuticals followed the Don't Get Cute Rule when shares popped after an important data readout. Management hauled in $393 million by selling 10 million shares at $39 each. That looked like a brilliant move when shares nosedived below the offering price soon after.

But then things abruptly changed. Ultragenyx reported a best-case scenario regulatory update in July and faster-than-expected product growth in August, which pushed shares above $55 each. That level has held through the broader market's recent stumble, so far.

Does that suggest management misfired by offering shares near multiyear lows in June? Not quite. It might have actually lit the match.

Shares have been re-rated higher largely because faster growth means cash flow should improve more quickly than previously expected. That means the $393 million raised in June suddenly represents an additional 18 months of runway, which makes the business much more interesting.

It's tempting to think the company could've waited and enjoyed an even more favorable offering price, but there's value to getting dilution out of the way, rather than having it hang over the stock. As two other recent examples show.

- In July, Kymera Therapeutics announced Sanofi peeked at interim data for KT-474 in autoimmune diseases and decided to immediately accelerate development. But the business already had a cash runway into the first half of 2027, so it didn't raise money. When shares remained elevated a month later, management said "screw it" and raised another $258 million for the hell of it. Shares are now 10% higher than the offering price.

- In September, Vaxcyte raised a mindboggling $1.5 billion in cash after a favorable data readout. The offering price of $103 per share was by far the highest stock price of all time. Well, at the time. Shares are almost 10% higher right now.

Relay Therapeutics might rejoin the stock offering club this week if Monday's data readout for RLY-2608 is favorable. Management didn't give investors a chance to hype up the stock beforehand, but that also catches Wall Street off guard. Analysts will have to quickly adjust models without days or weeks of planning. That would play to management's advantage if results are favorable.

A reasonable cash haul could easily extend its runway into 2027 or even 2028. If it follows with a favorable lirafugratinib regulatory update later this year, and/or solid safety data for a triple combination of RLY-2608, then the stock may find reasons to keep climbing higher. And why not? There could be at least four years of runway.

First things first, of course.

Recent De-Risking Events Roundup

It's been a little bit since the last Monthly Digest, so there's a longer list of developments to review. Here's a review of de-risking events since the last Monthly Digest, recapped in alphabetical order:

Arrowhead Pharmaceuticals $ARWR

The RNA interference (RNAi) developer announced its decision to advance plozasiran, instead of zodasiran, into an important cardiovascular outcomes study. The company was developing both assets simultaneously in sometimes overlapping cardiometabolic indications. It had previously communicated only one would be studied in broader patient populations as a potentially mass-market treatment for lowering cholesterol.

The first and only RNAi drug product marketed for a mass-market cardiometabolic indication is Leqvio, which was the primary reason Novartis acquired The Medicines Company for $9.7 billion. The asset also lowers cholesterol (albeit through a different genetic target) and has been shown to improve cardiovascular outcomes. Leqvio is on pace to generate over $700 million in full-year 2024 revenue.

If you think Arrowhead is late to the party, then don't worry. The patient population is estimated at 20 million, compared to only 1,000 for the initial plozasiran indication expected to be submitted to regulators before the end of 2024.

AVITA Medical $RCEL

The recent FDA approval of ReCell GO marks an important milestone for AVITA Medical and will be an important growth driver. The third-generation device is the first to fully automate cell harvesting and preparation. Importantly, it changes the company's business model.

Whereas ReCell used to be sold as one-time-use kits, ReCell GO is a durable device that requires one-time-use consumables to operate. However, each device needs to be replaced eventually, which means investors have a sneaky way to track customer adoption (early on) and the number of procedures performed each quarter (over time). If you dig through SEC filings, then you'll see:

- ReCell GO preparation kits (RPK) represent the sale of a consumable required to perform a single procedure

- ReCell GO progressing device (RPD) represents a depreciable asset

AVITA Medical doesn't sell ReCell GO devices. It leases them due to a limited lifetime of 200 uses. As a result, it tracks the number of ReCell GO devices in the hands of customers as an asset on its balance sheet. Each sale of an RPK (representing a single procedure) triggers a 1/200 reduction to the value of this asset line.

Each ReCell GO device costs about $3,500 to manufacture. If it can be used 200 times, then the RPD value is depreciated by $17.50 for each RPK sold.

If investors find the accumulated depreciation line item associated with ReCell GO and divide by $17.50, then they'll get a pretty accurate estimate of customer adoption. During Q2 2024, customers ordered enough RPKs to perform approximately 685 procedures on the new ReCell GO devices. That's enough to almost completely replace prior-generation devices, or roughly double revenue – and not all customers have ordered the new devices yet.

Given that nerdy math and context, management's seemingly wild revenue guidance makes more sense. Execution in the coming quarters will be key though.

I have a half-written research note I'll try to get out soon to walk through this math and Q2 2024 results.

Certara $CERT

In June 2024, the FDA upgraded its model-informed drug development (MIDD) program into a pilot. This is the regulatory body's biosimulation program. Together with industry – and Certara – the FDA is working to understand how biosimulation can and cannot be used to improve the efficiency of drug development.

Everything is on the table.

The FDA has, in specific cases, allowed Certara's biosimulation data to be used instead of animal studies. In at least one example, biosimulation data alone was used to completely avoid a phase 3 clinical trial and earn a supplemental approval for an acne drug.

Importantly, the FDA Modernization Act 2.0 signed into law in December 2022 no longer requires animal studies, but the agency has taken shit for the general inaccuracy of organ-on-a-chip methods currently used as a replacement. The FDA is eager to address that criticism with a better replacement. Hint: It's biosimulation.

The MIDD pilot will take a few years to complete, but it has the potential to mark a significant turning point for Certara, especially given the industrywide focus on conducting more meaningful R&D for significantly less investment. Read more and discuss this on our Discord server.

Coherus BioSciences $CHRS

Coherus BioSciences needs to focus on commercial execution during 2024. It delivered solid second-quarter results that showed promising ramps for both Loqtorzi and Udenyca Onbody. Read the recent research note.

Day One Bio $DAWN

Well, well, well. Day One was an attractive biotech stock with a lower valuation ceiling, but recent moves might significantly raise that ceiling.

In the span of two months the business raised a total of $394 million in three separate transactions (including $219 million in non-dilutive funds) and in-licensed an asset with intriguing potential.

Day One thinks the asset, an antibody drug conjugate (ADC) that targets PTK7 in solid tumors, can succeed where others have failed. The high-value target has proven too toxic to adequately whack, leading Pfizer and AbbVie to abandon a closely-watched drug candidate. If DAY301 shows early promise with a cleaner safety profile in 2025, then it could be a significant value driver for the company.

Exscientia $EXAI

Recursion Pharmaceuticals announced it will absorb Exscientia. The combined technology-enabled drug development platform will be a little sloppy initially, suggesting Recursion will need to terminate, deprioritize, or divest multiple non-core assets. The merger removes a more meaningful long-term opportunity for Exscientia as a standalone business, but there are paths to success after the dust settles. Read the recent research note.

Kymera Therapeutics $KYMR

The newest addition to the coverage ecosystem (a model has yet to be introduced) took advantage of its premium valuation and raised $225 million through a stock offering. That follows a July 2024 decision by Sanofi to accelerate and expand its use of the company's protein degraders in certain autoimmune disorder indications. I disagree with the company's valuation, but it's great to see a management team wisely take advantage of an opportunity to raise more capital.

LanzaTech $LNZA

Multiple major commitments to carbon capture and sequestration projects may bode well for LanzaTech's technology platform, which feeds carbon emissions from industrial processes to engineered microbes that convert it into ethanol. LanzaTech has a secondary technology platform that can convert ethanol into jet fuel.

Bank of America recently agreed to pay $205 million for a 10-year carbon capture program in North Dakota, while Exxon Mobil said it expects to start carbon capture projects on the Gulf Coast in 2025. Read more and discuss on our Discord server.

Upcoming De-Risking Events Roundup

Here's a preview of de-risking events to keep an eye on, in order of nearest to furthest:

Relay Therapeutics $RLAY

The company scheduled its most important data readout for RLY-2608 for Monday, September 9 before the market opens. I'll publish a research note this weekend providing a cheat sheet for how to interpret the results.

Arrowhead Pharmaceuticals $ARWR

The company remains on track to submit a regulatory application for plozasiran in familial chylomicronemia syndrome (FCS) before the end of 2024. This will be the first approval request in the company's history.

Centessa Pharmaceuticals $CNTA

The company expects to report initial data from its pivotal study of SerpinPC in hemophilia B before the end of 2024. This is the most overvalued stock in the coverage ecosystem, but the current model only reflects the bispecific antibody platform (LockBody). I'll need to add the emerging opportunity for its OX2R agonist in neuro indications and revisit my sour outlook for SerpinPC (the primary driver of the valuation).

Codexis $CDXS

The company expects to enter its first technical collaboration for the ECO Synthesis platform (enzymatic RNAi manufacturing) before the end of 2024. It teased a proof-of-concept at a major conference using molecules from Alnylam Pharmaceuticals, but there are only so many RNAi developers to choose from. Novo Nordisk (formerly Dicerna), Novartis (formerly The Medicines Company), and Arrowhead Pharmaceuticals round out the remaining big fish.

Exact Sciences $EXAS

The company might have BLUE-C data for its blood-based colon cancer screening tool before the end of 2024. This will be meticulously compared to Guardant Health's recently-approved Shield product. No matter how favorable or unfavorable, these diagnostics face a difficult road to earning meaningful reimbursement coverage.

Arvinas $ARVN

The company expects to report a topline data readout for a phase 3 study involving its lead drug candidate before the end 2024 or in early 2025. The asset is licensed to Pfizer, but it would be meaningful if investors can pencil in milestones and royalties to help fund development of the in-house neuro pipeline.

Finch Trades Review

Finch Trades are how I share my real-money investing moves in real time with members.

- Each transaction confirmation is shared on Discord as soon as the transaction closes, so I cannot cherry-pick my track record. Follow-up research notes are published soon after.

- The all-time returns of Finch Trades will be reported vs. what would've happened if I invested in the S&P 500 instead. I want to demonstrate biotech investing can outperform a passive investing approach when used in conjunction with my modeling and the Margin of Safety Dashboard.

- The all-time returns of Finch Trades are dollar-weighted. This differs from a stock recommendation service where each "pick" is equally weighted. I think Finch Trades better reflects real-world investing.

As of market close on Friday, September 6, 2024, Finch Trades are underperforming the S&P 500 by 23%. I would consider this an initialization period, especially since 92% of the funds invested to date are allocated to Coherus BioSciences and Relay Therapeutics, which have near-term de-risking events.

Finch Trades will eventually have a real-time performance dashboard on the website similar to the Margin of Safety Dashboard.

.svg)

.svg)

.svg)

.png)

.svg)

.svg)

.svg)