.svg)

This month I want to review a topic that's come up a lot recently on Discord: stock-based compensation (SBC).

Is it always a bad thing? Is there such a thing as too much? What's the proper way to interpret this metric?

This is one of the dozens of data points I track for each company in the coverage ecosystem. Although many investors interpret SBC as fat cats in the C-suite hooking themselves up with free money, the reality is that almost all SBC goes to employees. You know, the people actually building the company and doing the work.

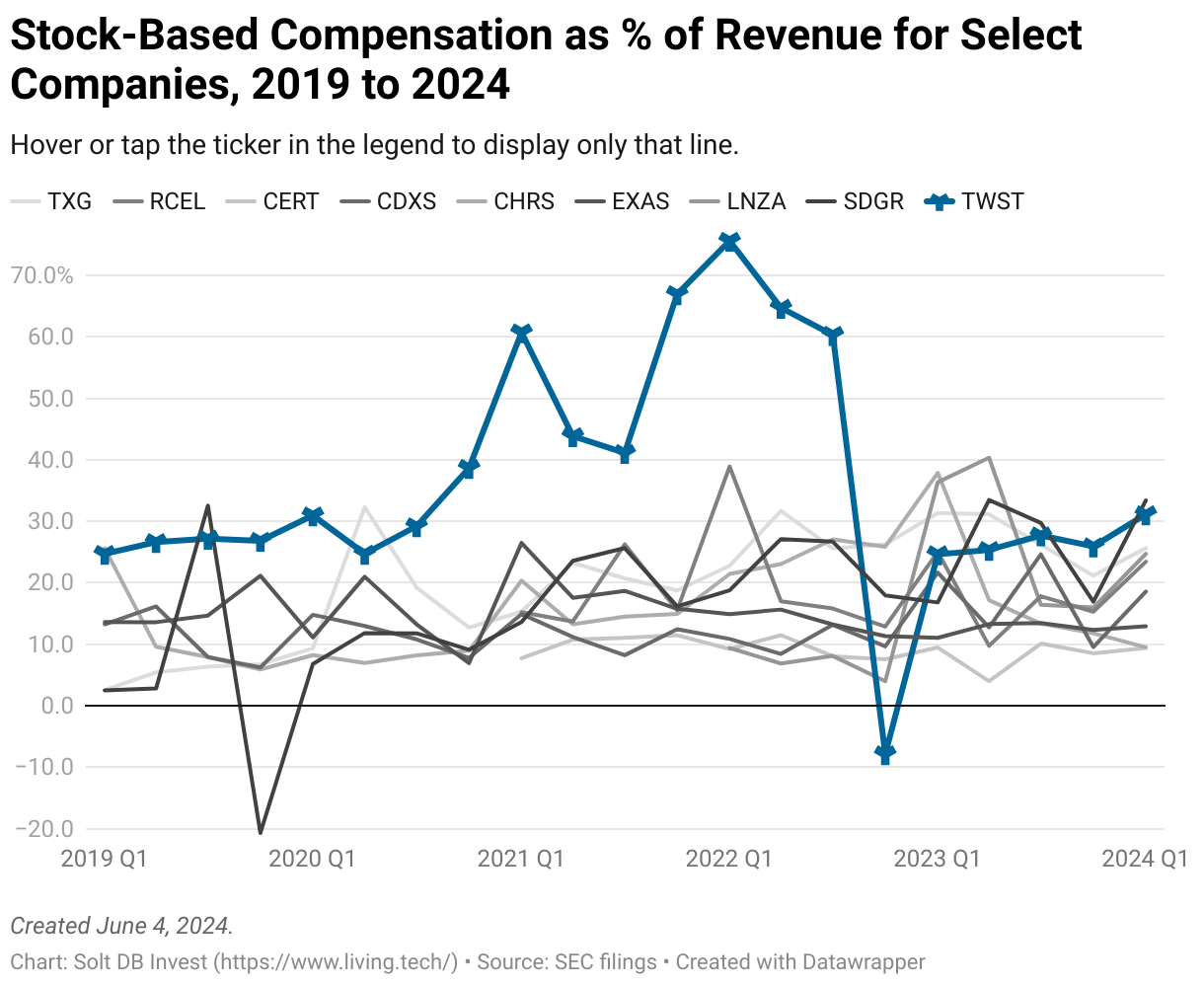

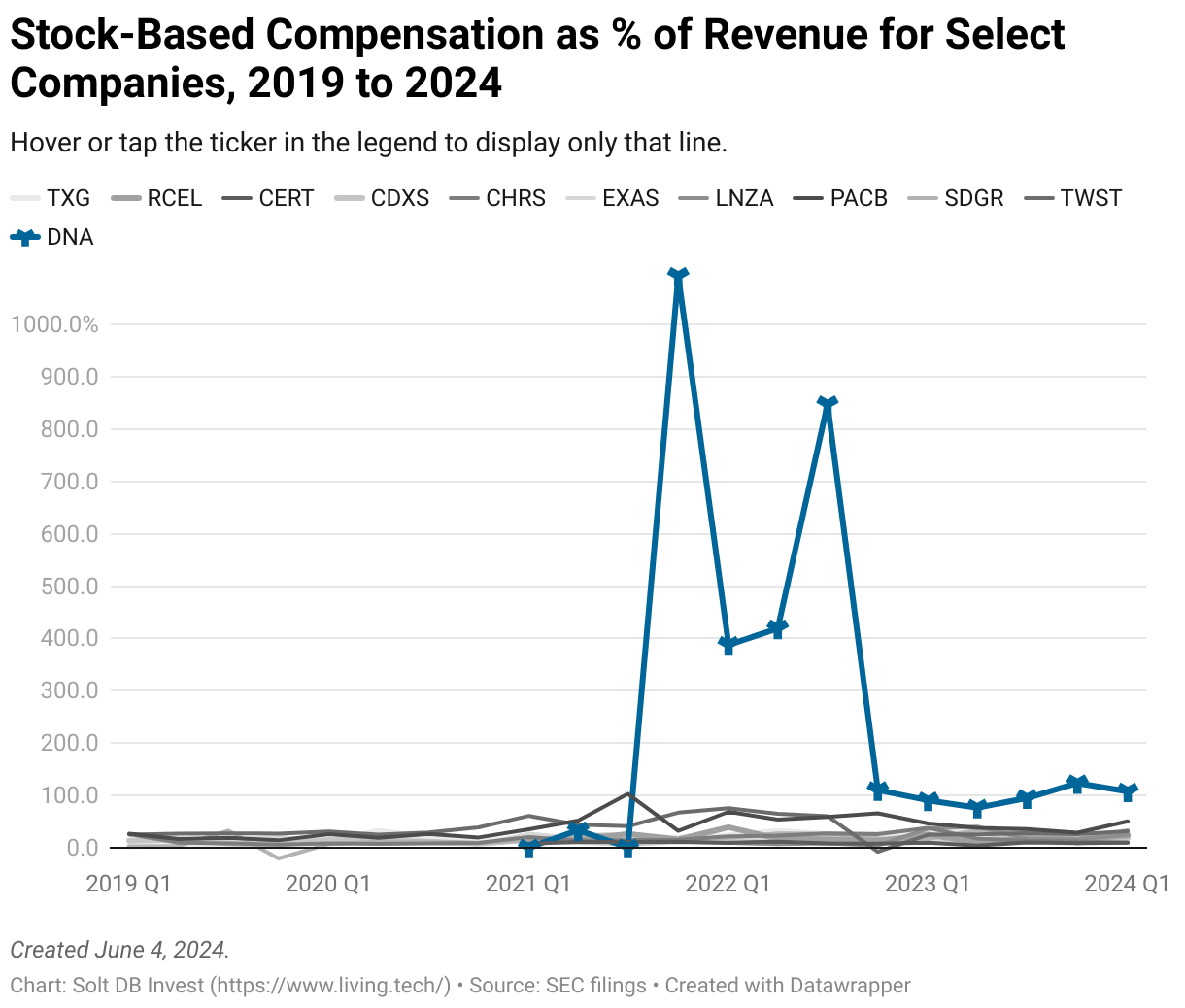

Let's look at groups of companies in the Solt DB Invest coverage ecosystem and how they rank on this metric.

Is Stock-Based Compensation A Big Deal?

SBC usually doesn't directly impact models because, as we'll see, it usually represents an insignificant amount of dilution. It's also a non-cash expense, which means it doesn't factor into operating cash flow. In fact, when employees exercise stock options, the company receives cash.

That doesn't mean it's not important. It simply means you must understand the context behind the numbers. The problem is, that context isn't in financial statements.

Is a fast-growing business in a highly competitive industry and headquartered in a high-cost of living city? Then it might need to offer more generous share packages to attract and retain talent, especially if they're competing with the tech giants (Twist Bioscience).

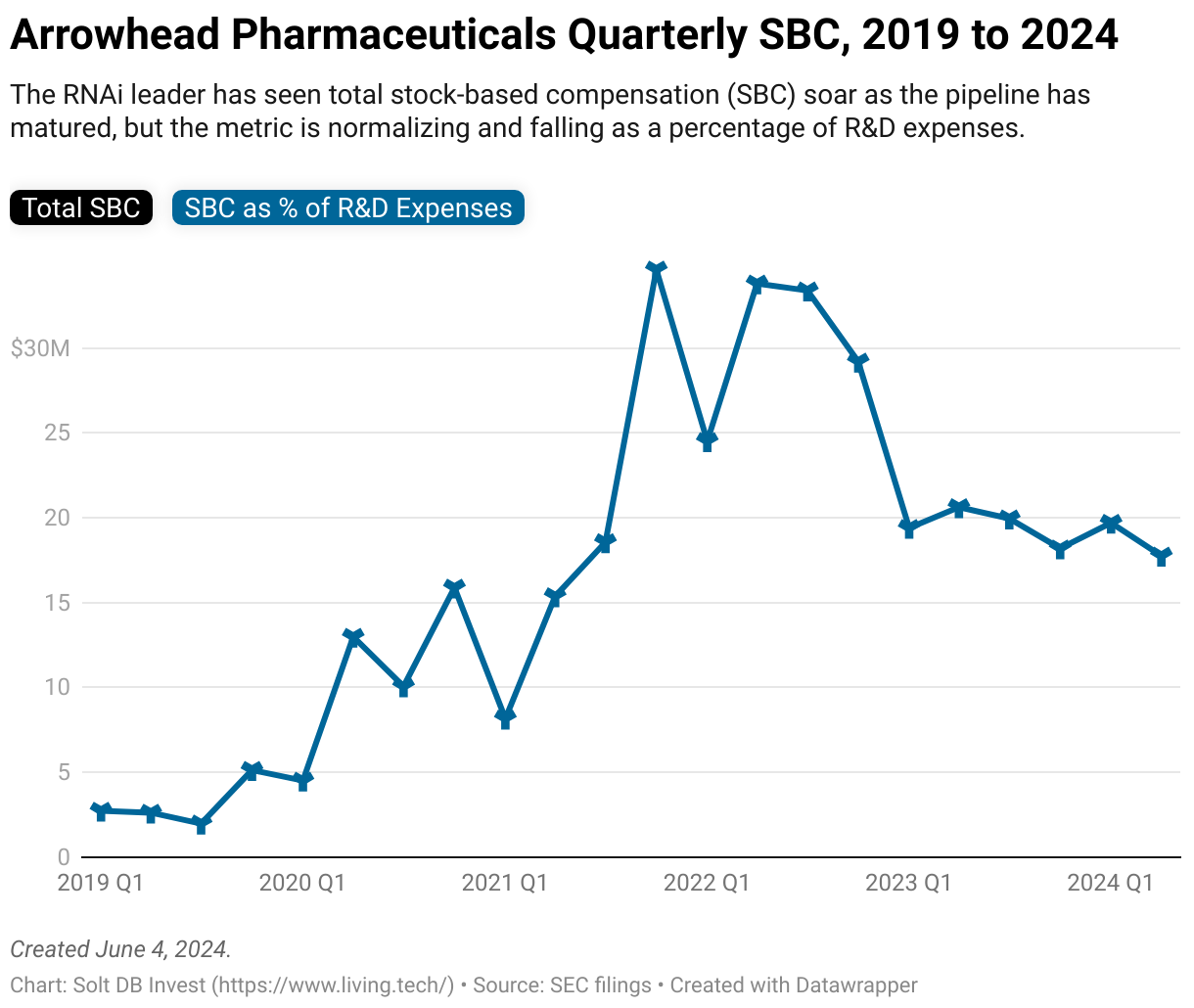

Is a drug developer rapidly expanding headcount as assets mature? Well, it's going to see a surge in total SBC, but it might remain steady or even decline as a percentage of R&D expenses (Arrowhead Pharmaceuticals).

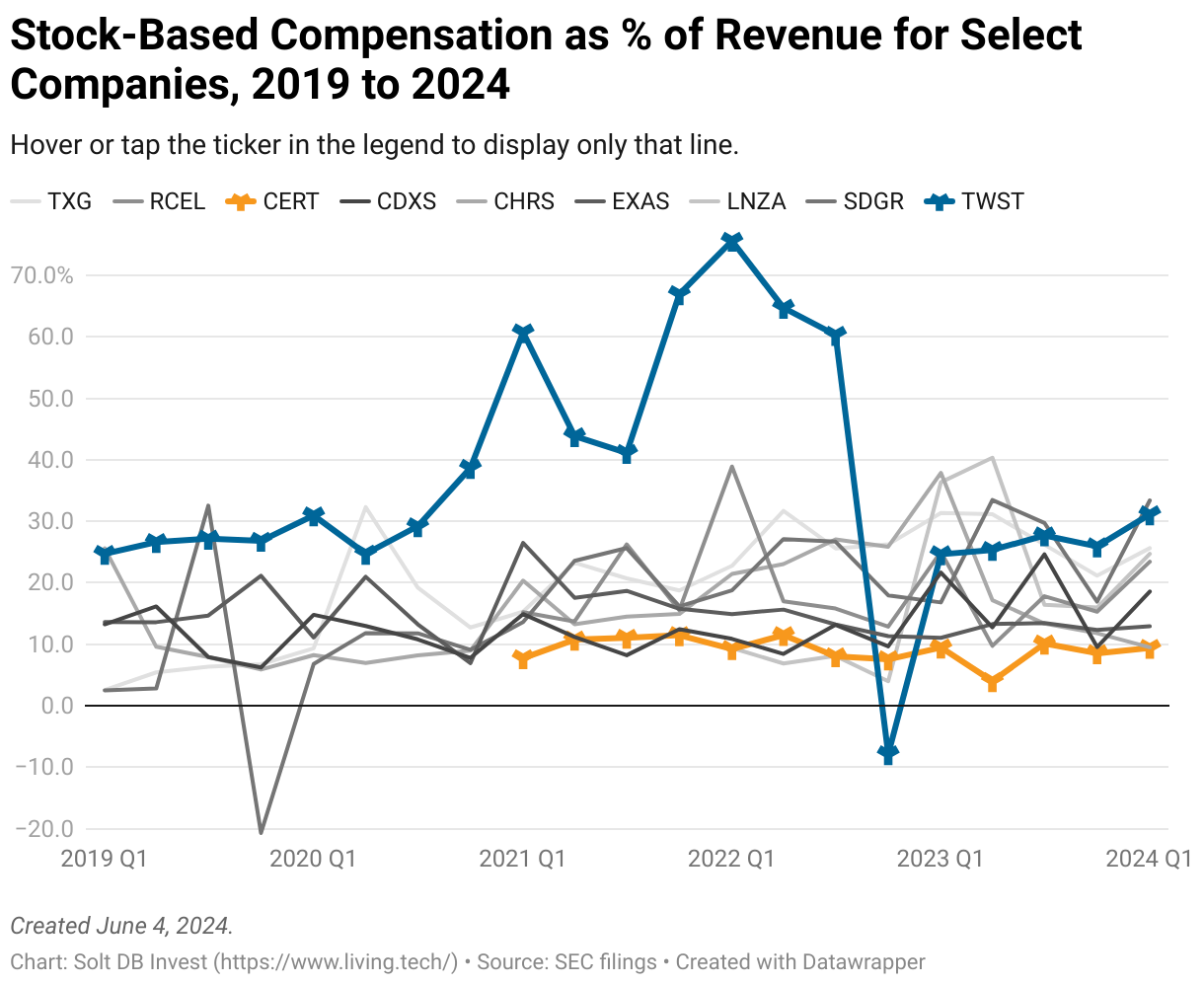

Is the company larger or profitable? It'll probably have a lower SBC as a percentage of revenue or operating expenses (Certara).

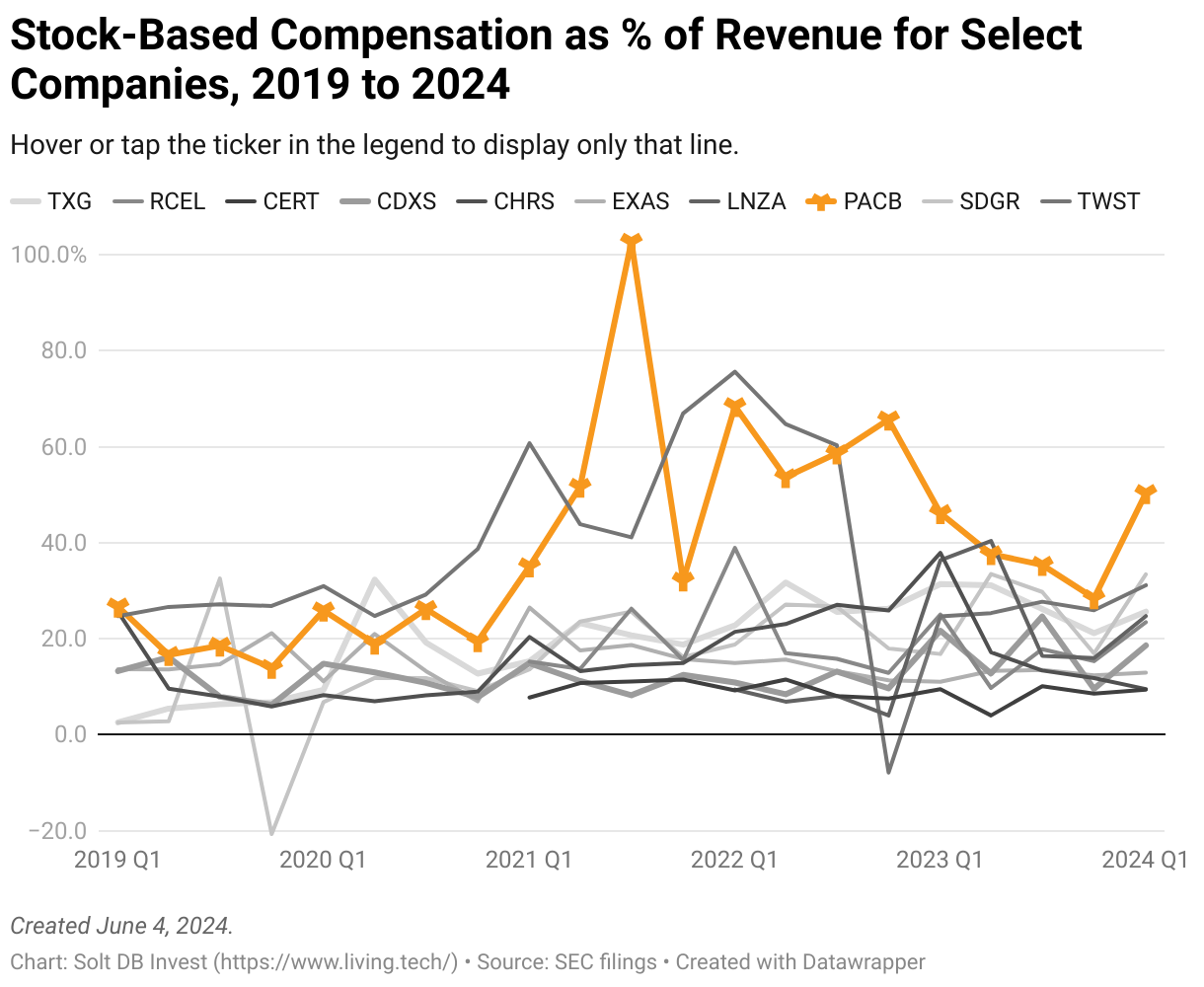

Context isn't just for making excuses. If the SBC surge from a sudden increase in headcount doesn't normalize quickly (or decline) as a percentage of revenue, then that could be an early signal those extra employees aren't driving revenue growth (PacBio).

But some of the most important context to acknowledge is that SBC usually isn't a big deal. It's insignificant as a percentage of a company's entire market cap. It's easy to find outliers, because they're relatively rare. It's a core and expected part of compensation for lab employees (not greedy executives)(I mean, they're still greedy)(you get what I'm saying).

If you view all these companies on the same chart as shown above, then they just paint lines across the graph – but generally within a reasonable bounds.

And the outliers are, well, easy to spot.

De-Risking Events to Watch

Here's what I'm watching during June:

Arrowhead Pharmaceuticals' R&D Day

The RNAi specialist has committed to one R&D Day each month through the end of the summer. That's the burden of having so many separate pipelines I suppose.

The May presentation focused on muscular programs. Despite being perfectly and coincidentally timed with an industry-moving muscular update from Dyne Therapeutics, shares didn't respond. It's an early-stage pipeline and a disease group that's proven tricky to adequately target.

The June presentation should be a little different. It'll focus on Arrowhead's cardiometabolic programs, including plozasiran and zodasiran. The two lead drug candidates are coming off three separate data readouts in two different diseases since the fiscal Q2 2024 earnings call just a few weeks ago.

It'll be a great opportunity to drum up excitement for approvals on the horizon. Meanwhile, an R&D Day in August will hype up an important cardiometabolic program: a next-generation obesity drug candidate targeting INHBE – a novel obesity gene that doesn't appear to be associated with muscle loss when inhibited.

Relay Therapeutics' New Pipeline

The company's ambitious strategy in breast cancer will take a backseat this week when management publicly reveals new, unrelated pipeline programs on Thursday, June 6. Investors have long been teased about two additional oncology programs and two genetic disease programs, all in preclinical development. The wait will finally be over.

Relay Therapeutics' Dynamo technology platform can be applied to drug discovery and drug development in any therapeutic area, not just cancer. That represents the potential to have multiple unrelated pipelines and diversify opportunities. The company seems to be mentioning protein degraders more often in recent months, which could suggest a push into neuroscience or rare diseases.

Similarly, it makes sense for any emerging company to focus on a specific area. The new programs represent partnership opportunities, which could raise non-dilutive cash.

The timing might work out pretty well. If data readouts in late 2024 are favorable and management wisely raises money to take advantage of a rising share price, and the company licenses emerging programs, then Relay Therapeutics could enter 2025 with over $1 billion in cash. That (and positive data with RLY-2608) would justify resuming development of the paused programs in breast cancer.

Ideas of the Month for June 2024

There are many ways to be active in the stock market. Solt DB Invest takes a strategy-agnostic approach to biotech investing, which requires valuation discipline and a more active style (even for long-term positions). Here's an update on recent ideas of the month and several timely ideas for members.

May 2024 Ideas

- One swing trade idea was PacBio $PACB. I thought it could be purchased and quickly exited for a 10% to 20% gain. The stock closed at $1.76 per share the date the monthly digest published and reached a high of $2.23 per share (a gain of up to 26%). The stock's most recent close: back down to $1.80 per share.

- The other swing idea last month was 10x Genomics $TXG. It was a swing and a miss. The stock went from $26.29 to $21.51 per share (a loss of up to 18%). I've not been enthusiastic about the business for a couple years now, but thought it would bounce back more quickly. Instead, shares have set a new all-time low.

Long-Term Stock

Arvinas $ARVN

Shares of Arvinas closed at less than a $2 billion market cap on Tuesday, June 4. That's a little low. Then again, the company was valued at just $1 billion as recently as October 2023.

But Arvinas is doing a great Arrowhead Pharmaceuticals impression.

The company's lead drug candidate, vepdegestrant (ER degrader), is co-owned with Pfizer. Arvinas can earn up to $400 million in milestone payments upon earning regulatory approvals, which could arrive relatively soon considering the first of several phase 3 studies has already begun.

The company's next-most advanced asset, ARV-766 (AR degrader), was just licensed to Novartis. Arvinas will realize a $150 million upfront cash payment during Q2 and can earn hundreds of millions more from development milestones in the next seven years.

Oh, and the company already ended March 2024 with $1.16 billion in cash. That war chest will be deployed to strategically develop preclinical oncology assets before monetizing them, while focusing on a wholly-owned neuroscience pipeline. If meaningful data readouts are now even further away with ARV-766 shipped off to Novartis, then why should you care about a hopeful neuroscience pipeline?

Arvinas' protein degraders can cross the blood-brain barrier, which means they can be administered orally and potentially treat things like Parkinson's, Huntington's, and Alzheimer's diseases at the genetic level. That's wild. In a world where everything gets hyped as a disruptive game-changing super-magical galactic event, the company's neuroscience pipeline could legitimately disrupt the global industry. If it works.

Short-Term Stock

Recursion Pharmaceuticals $RXRX

Recursion Pharmaceuticals has the opposite problem of Arvinas: It needs a lot more cash relatively soon. The business ended March 2024 with about $300 million in cash and is burning about $100 million per quarter. Luckily, it might have a sneaky and non-dilutive fix.

The company's expansive neuroscience partnership with Roche has a unique structure. While Recursion can earn traditional milestone payments as its partner develops up to 40 unique molecules, the company can also earn up to $500 million for just selling data generated from its technology platform. Roche kinda needs the data (see: the "up to 40 unique programs" part).

The math gets a bit tricky because there are up to 28 datasets involved, and not all have to be acquired at the same time. Nonetheless, Roche seems likely to acquire at least the first 16 datasets, which could greatly increase the efficiency of drug discovery within the scope of the collaboration. That decision would trigger a payment of $250 million.

The other $250 million is tied up to the remaining 12 datasets. The catch here, though, is these could be used outside of the collaboration with Recursion. If Roche sees enough potential to commit to its emerging neuroscience pipeline – a suddenly-hot field in the global industry – then it could buy these datasets, too. Even better, it has to make a decision soon after exercising the first purchase option.

I recently chatted with CEO Chris Gibson about these data payments. He just smiled, laughed, and said, "Someone's been reading SEC filings."

Whether or not Roche buys datasets soon, I can see Recursion licensing most of its seven (7) first-generation pipeline programs. There are three rare disease programs and an oncology program in phase 2 studies, while a C. difficile treatment candidate is ready for a phase 2 study. These don't fit neatly into the company's new strategy and it doesn't make sense to build commercial infrastructure for them.

All I know is the business needs to raise capital before the end of 2024, but that counterintuitively could turn into a positive event for the stock. There are simply too many options for monetizing existing assets without dilution.

Swing Trade

Ginkgo Bioworks $DNA

Poor Ginkgo Bioworks is struggling to keep its head above water. You could easily argue the company's market valuation will dip far below the $1 billion mark. That probably makes more sense given the recent pivot.

But… if you're a crazy prepper who thinks bird flu is a legitimate threat (hey, I don't know), then Ginkgo Bioworks would absolutely shred higher on that oh-shit-here-we-go-again health calamity. Or even a short-term scare about bird flu. Investors would rightly or wrongly think the company's biosecurity infrastructure would be tapped for surveillance and response activities (and likely by the federal government).

The timing is uncertain and the trigger might not occur, but if you pinky promise your future self to lock in gains and not get greedy, then a small position near current prices could pay off handsomely under the right circumstances.

Finch Trades

I recently purchased:

- $1,000 of Relay Therapeutics at $6.275 per share

- $1,000 of Exact Sciences at $44.98 per share

.svg)

.svg)

.svg)

.png)

.svg)

.svg)

.svg)