.svg)

I don't know if "A-B-C" is as easy as "1-2-3," but I do know the fragmented multi-omics diagnostic landscape is coalescing around a handful of leaders. Each is scaling well – and this year it really is as easy as "1-2-3."

Tempus AI will crack $1 billion in revenue in 2025 thanks to its acquisition of Ambry Genetics. Natera's almost twice as large. Led by Signatera, the company expects 2025 revenue to fall a whisker shy of $2 billion, but that seems conservative. Exact Sciences is larger still. This year it will be the first in the landscape to eclipse $3 billion in annual revenue.

The revenue leader isn't too surprising here. If Cologuard was a standalone company, then it would deliver $2.3 billion in full-year 2025 revenue.

Exact Sciences will continue to lean on its flagship brand for growth and cash flow. The launch of Cologuard Plus in 2025 will boost revenue thanks to market share growth and a higher selling price, while a lower cost of goods sold relative to its predecessor will bump margins.

But the business is also looking to diversify revenue and find new sources of growth. That makes the launches of Oncodetect, the company's first molecular residual disease (MRD) product, and Cancerguard, the company's in-development multi-cancer early detection (MCED) product, important events to watch this year.

By the numbers

Exact Sciences delivered a solid year of operations. The biggest headwind was growing pains from an expanded sales team, which tripped up the company in Q1 2024 and Q3 2024. A software glitch (self-inflicted) and the impact from hurricanes (out of the company's control) didn't help. In the grand scheme of things, if those easily-corrected factors are the biggest issues facing a business, then things are going pretty well.

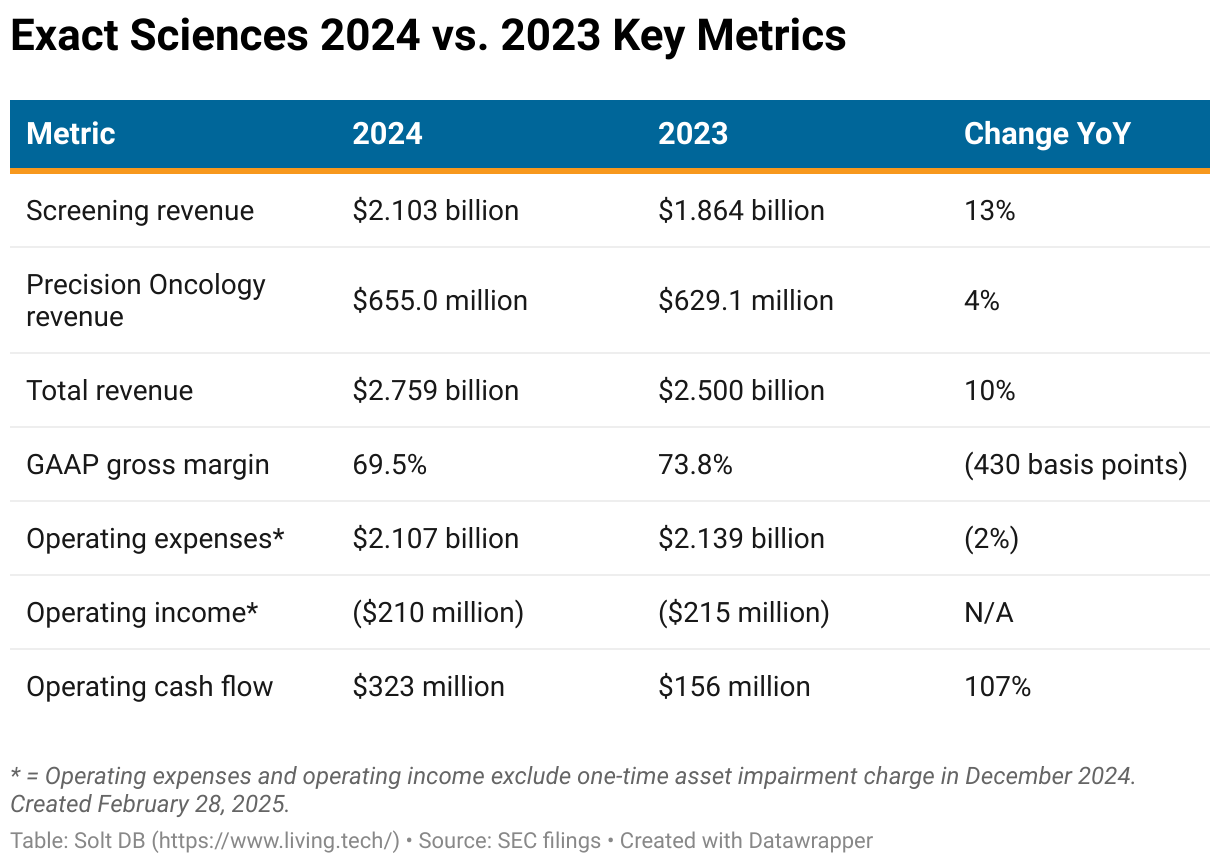

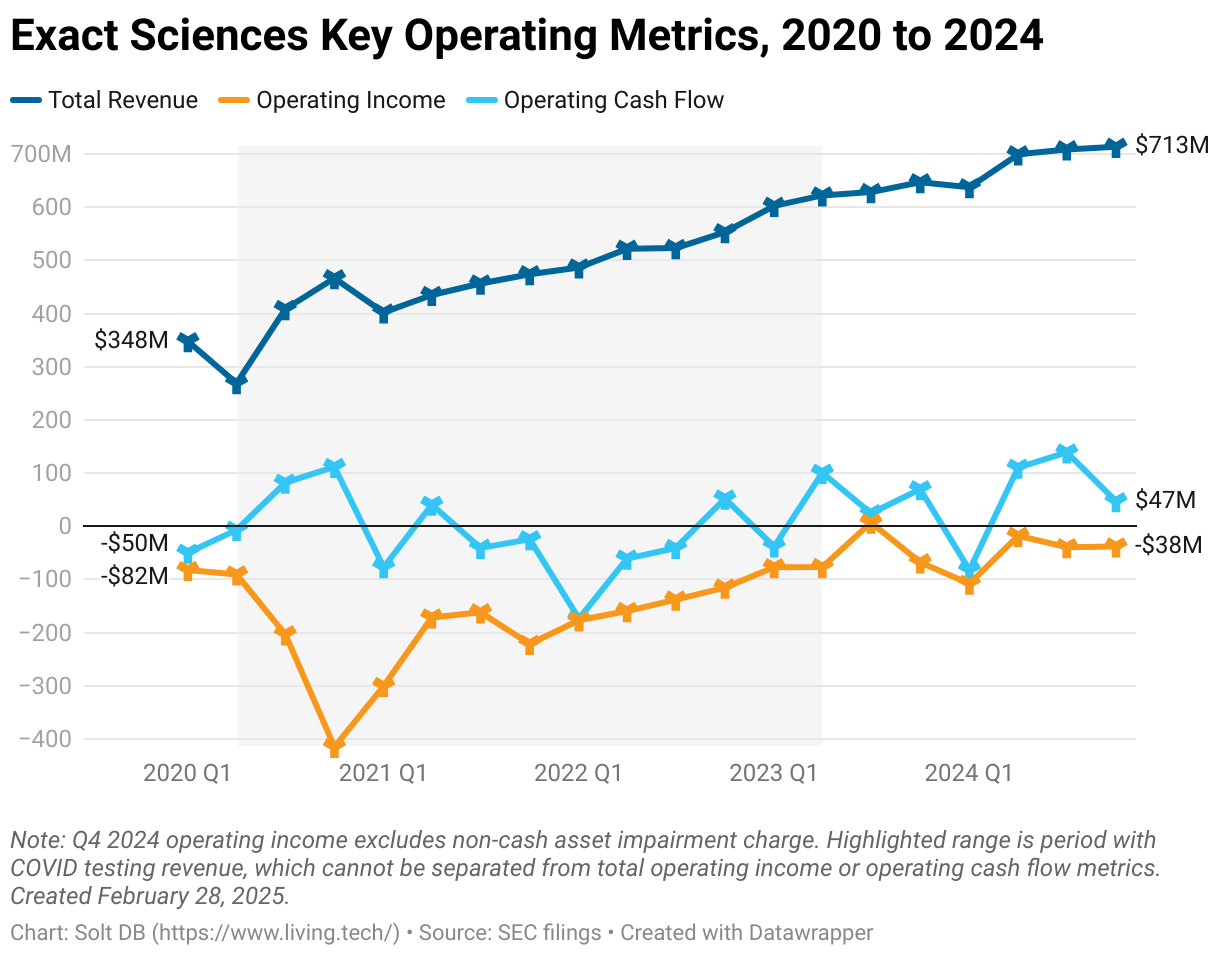

The business managed to grow revenue 10.4% compared to 2023. Although respectable, it was the slowest annual growth rate for the business since Cologuard launched in 2024. Total revenue grew 18.5% in 2021, 17.9% in 2022, and 19.9% in 2023.

A few thoughts.

First, the business will grow more slowly as the numbers get larger. Exact Sciences added $259 million in revenue in 2024; not notably different from the $276 million added in 2021. But the growth rates those years – 10.4% vs. 18.5% – make the difference seem more dramatic.

Second, that doesn't mean management gets to wiggle off the hook that easily. Revenue grew slower than expected in 2024. The headwinds mentioned above contributed, but so did stagnation in the Precision Oncology segment. The unit grew only 4.1% last year and has grown just 17% since 2021. By comparison, the Screening segment grew 13% last year and 98% since 2021. That suggests Oncotype Dx, the standard of diagnostic care for HR+ / HER2- breast cancer recurrence risks, has reached its peak.

Third, growth should accelerate this year and next. Management's initial revenue guidance expects 13.4% this year, while my 2025 model expects the Screening segment to grow nearly 16.5%. Both improvements are driven by moving past last year's headwinds and initial contributions from Cologuard Plus. The next-generation screening tool should provide an even bigger boost in 2026.

Delivering in 2025 will be key to alleviating any concerns among analysts that, just maybe, Cologuard is petering out years earlier than expected. (I don't see signs of that.)

Importantly, the business remains healthy and on track for profitable operations in 2026.

Exact Sciences grew revenue by double digits and achieved a 2% decline in operating expenses, which helped to drive improvements in both operating income and operating cash flow. Unexpectedly higher product costs last year dropkicked gross margin below 70% for the first time since 2016. If gross margin matched its 2021 to 2023 average, then the business would've reported an operating loss of only $92 million and operating cash flow of $441 million.

The launch and ramp of Cologuard Plus should help. It boasts a cost of goods sold at least 10% lower than its predecessor.

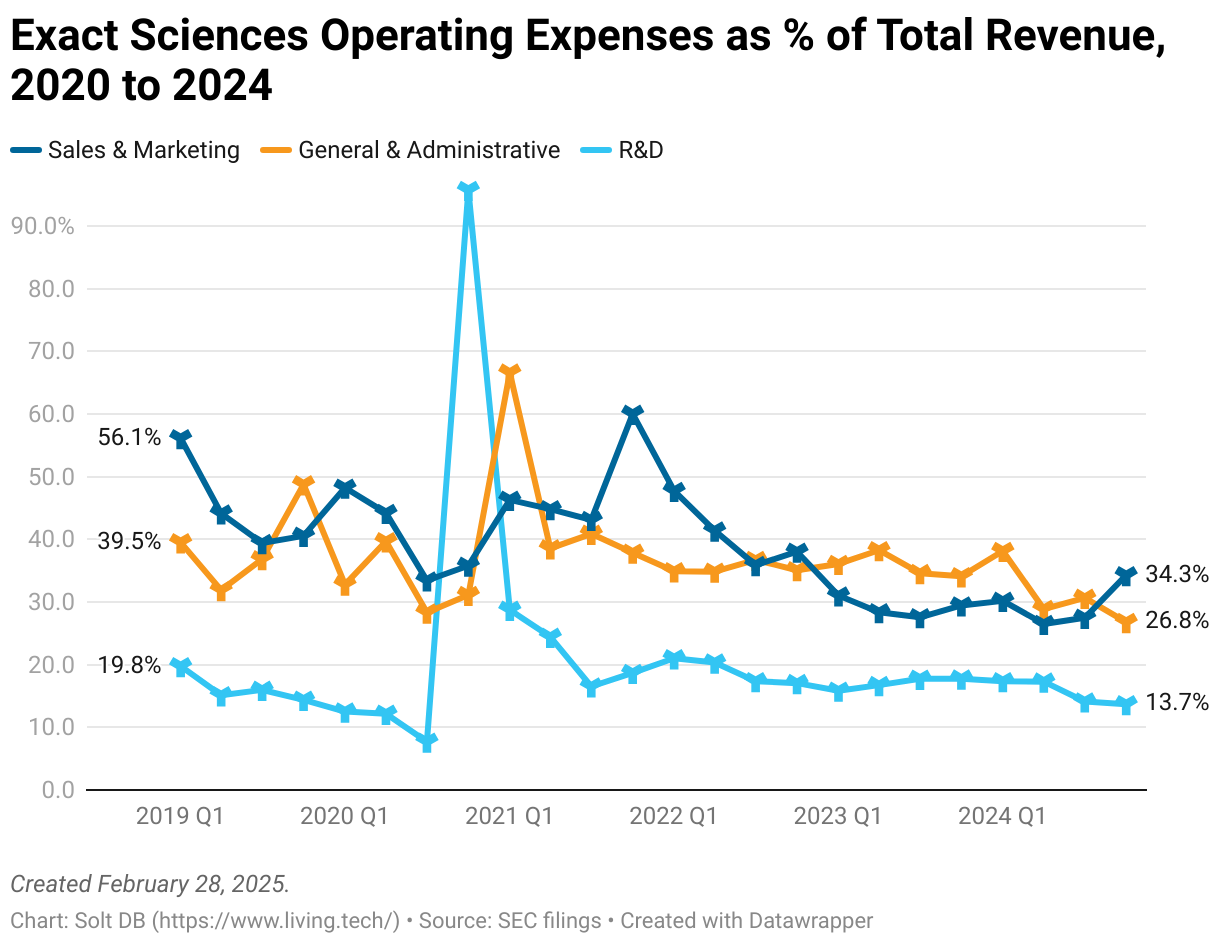

Delivering revenue growth and margin improvement will nudge the business closer to profitability. Keeping operating expenses in check will help, too.

During Q4 2024, R&D expenses reached their lowest level as a percentage of revenue since before the coronavirus pandemic. (Don't worry, the business isn't neglecting its future: Exact Sciences spent a record amount on internal R&D in 2024.) Selling, general, and administrative (SG&A) expenses reached their lowest level ever on the same basis.

Sales and marketing expenses bucked the improving trend. That's because this line item grew faster than revenue from Q3 to Q4 last year. The business spent $24 million more on sales and marketing in that sequential span, but added only $5 million in revenue.

The business is objectively healthy and improving, leaving investors with no major causes for concern. So, let's wrap up with two final items.

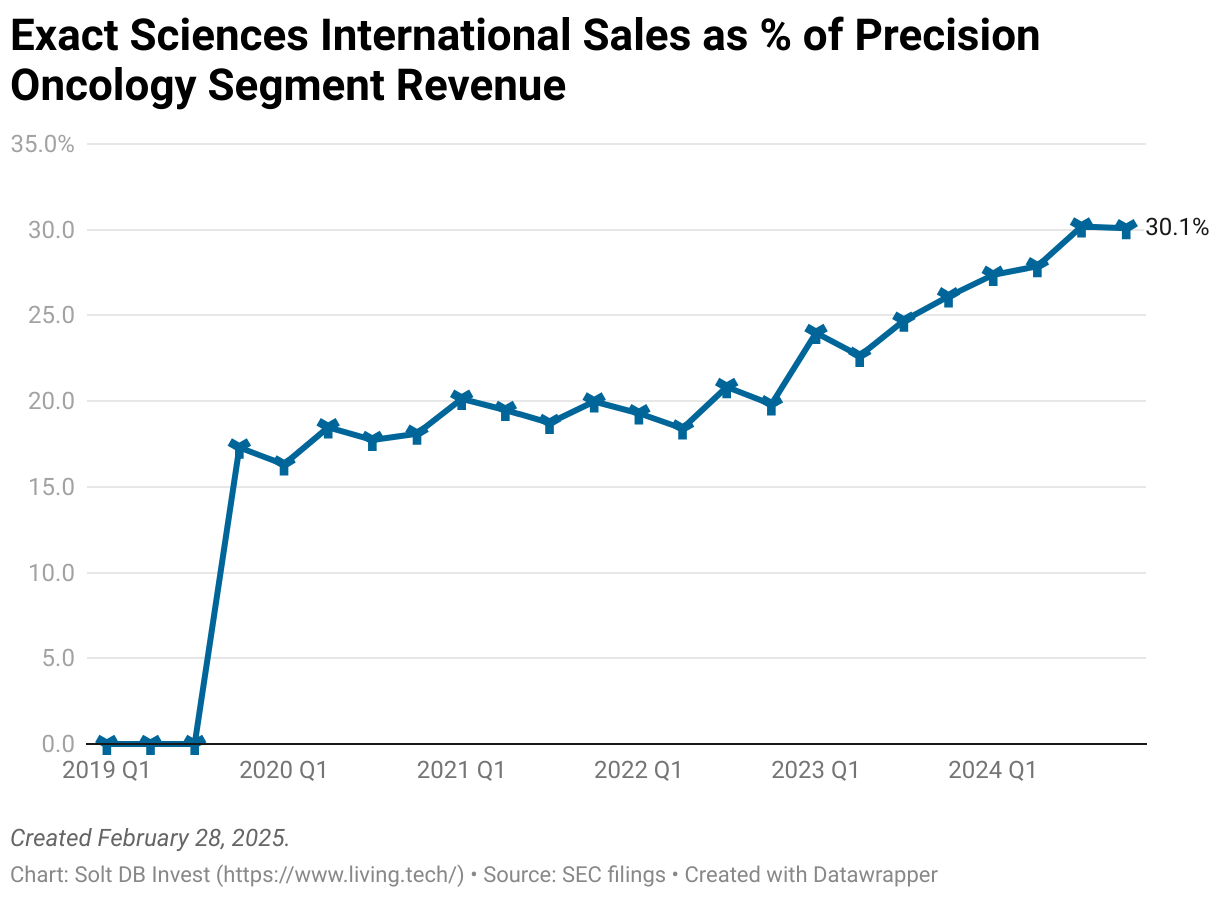

I've communicated the international contributions of the Precision Oncology segment in recent quarters. For consistency, ex-U.S. revenue represented 30% of total unit sales in Q4 2024 – same as the record set in the prior quarter. Although investors want to see this segment grow faster, it's almost perfectly diversified right now with Medicare, commercial, and international sources each accounting for about 30% of total revenue. "Other" revenue comprised the remaining 12%.

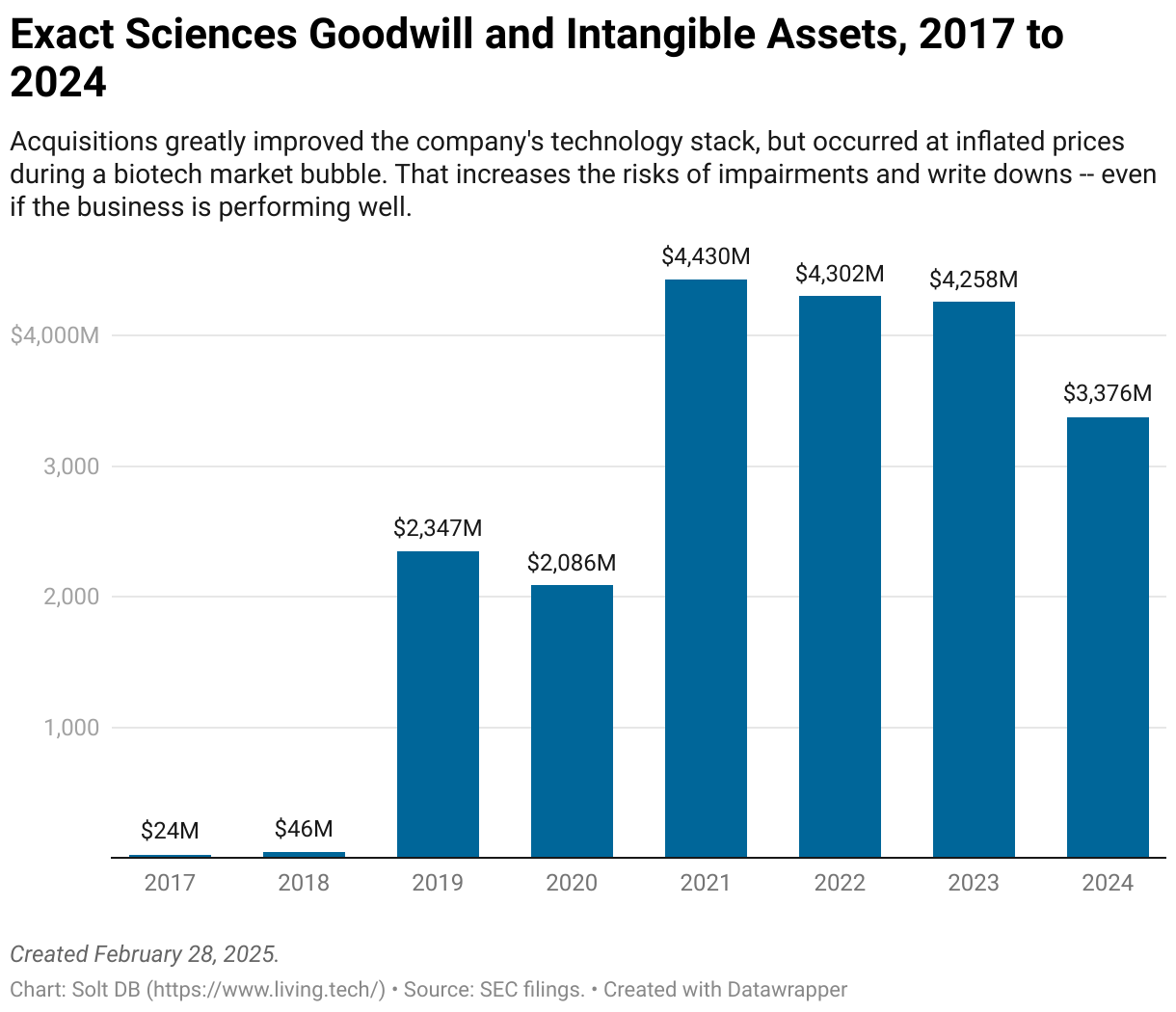

Exact Sciences also took the opportunity to write off $838 million of intangible assets in Q4 2024. This non-cash charge tanked profitability metrics, but had no impact on cash flow.

Goodwill and intangible assets are often used to account for acquisitions. Goodwill is the amount of the acquisition minus the actual value of the acquired business. Think of it as the "premium." Intangible assets include things like know-how, brand value, and so on.

After over one dozen acquisitions, the company has a massive amount of goodwill and intangible assets on its balance sheet. It doesn't help that many buyouts occurred during the more buoyant times of 2020 and 2021, which inflated valuations. These two line items totaled over $4 billion before the impairment.

That's simply the price Exact Sciences had to pay to acquire a technology stack. By contrast, Guardant Health has never had more than $19 million in goodwill and intangibles. Natera's balance since 2017: zero.

Forecast & Modeling Insights

(Refined.)

Management issued full-year 2025 revenue guidance that aligned well with my 2025 model communicated last November, but I'm taking the opportunity to refine a couple items.

I now expect Screening revenue to be higher than previously expected, although Precision Oncology will be lower than previously expected. The net change from the prior model is just $2 million – a rounding error.

My current 2025 model for Exact Sciences assumes:

- Full-year 2025 revenue of $3.128 billion, representing year-over-year growth of 13.4%. The company's guidance expects $3.065 billion at the midpoint.

- Screening revenue of $2.444 billion, representing year-over-year growth of 15.9%. The company's guidance expects $2.370 billion at the midpoint.

- Precision Oncology revenue of $684 million, representing year-over-year growth of 4.5%. The company's guidance expects $685 million at the midpoint.

- Gross margin of 70.5%, marking an improvement from 69.5% in 2024.

I had originally expected the Precision Oncology segment to grow faster in 2025, especially with the launch of Oncodetect. Management's guidance seems too conservative, but given the sluggish growth in recent years I've decided to let execution drag my model higher, if needed.

Meanwhile, Cologuard Plus received a slightly higher reimbursement price than my previous model. Revenue growth from the transition to the next-generation product is difficult to predict and depends on the pace of launch, uptake, and inventory management decisions at thousands of providers nationwide. But investors can expect to begin seeing positive contributions in both revenue and margins by the end of 2025.

Finally, I don't expect the launch of Cancerguard to make a material contribution. It doesn't have reimbursement coverage (and won't for many years) and there's not a defined market for it today. Exact Sciences is launching now to build brand awareness, collect early feedback and data, and position itself for an MCED opportunity estimated to be nearly 40% larger than Cologuard's.

Margin of Safety & Allocation

Exact Sciences is considered an Anchor position. The current fair valuation for the company based on my 2025 model is below:

- Market close February 28: $47.41 per share

- Modeled Fair Valuation: $87.88 per share

- Allocation Range: Up to 15%

Exact Sciences reported 185.755 million shares outstanding as of February 18, 2025. The modeled fair valuation above assumes 187.613 million shares outstanding, which is equivalent to 1% dilution.

Further Reading

- February 2025 press release announcing 2024 operating results

- February 2025 regulatory filing (10-K) detailing 2024 operating results

- November 2024 research note

.svg)

.png)

-cropped.svg)