.svg)

They say to never look a gift horse in the mouth. I'm not quite sure what that means, but I'm pretty confident Exact Sciences doesn't have any equestrian cavities.

The business encountered some turbulence in the third quarter of 2024. Similar to AVITA Medical, the company plowed ahead with a significant expansion of its sales team this year and failed to realize an immediate payoff. Similar to AVITA Medical, the unforced errors are completely within the company's control to correct.

Unlike AVITA Medical (which is on track to regain lost operating leverage), Exact Sciences has a multi-year track record of commercial execution and can now self-fund growth investments.

The precision oncology leader is the most efficient it's ever been. The business delivered record operating cash flow in the third quarter of 2024, while simultaneously holding operating expenses in check as a percentage of revenue. Although Q4 2024 revenue is expected to be worse, only impatient investors would overlook the many tailwinds arriving in 2025.

The next year will see the launch of Cologuard Plus, a higher selling price for Cologuard, the launch of the first molecular residual disease (MRD) products in the Oncodetect brand (a key growth driver), continued international expansion, more data for the blood-based screening tool that's already delivered better results than Guardant Health's Shield, and more data from the multi-cancer early detection (MCED) product candidate.

The recent plunge is overdone and represents a great opportunity for investors with a long-term mindset.

By the Numbers

Exact Sciences has given my models whiplash in 2024. The company, which is typically relatively predictable, has been anything but this year.

Despite Wall Street's sharply negative reaction and some speed bumps, the business is objectively moving in the right direction.

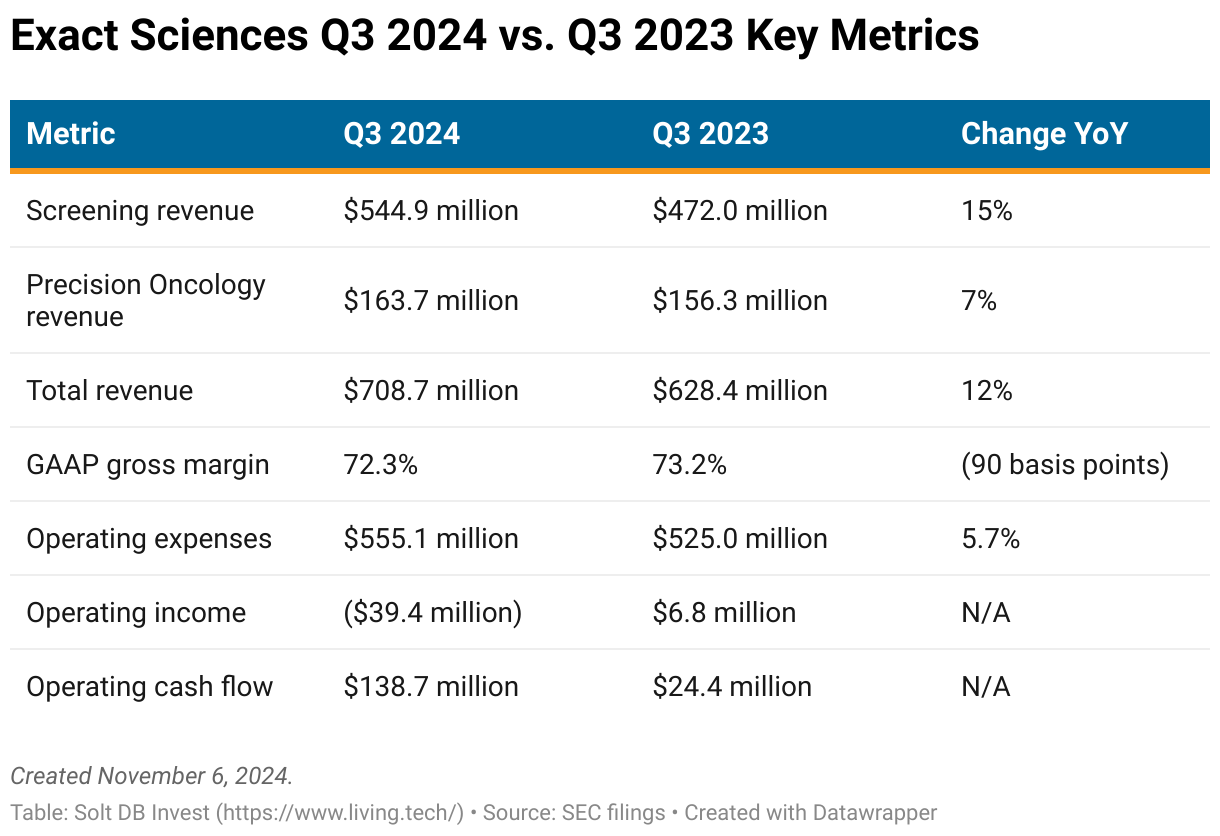

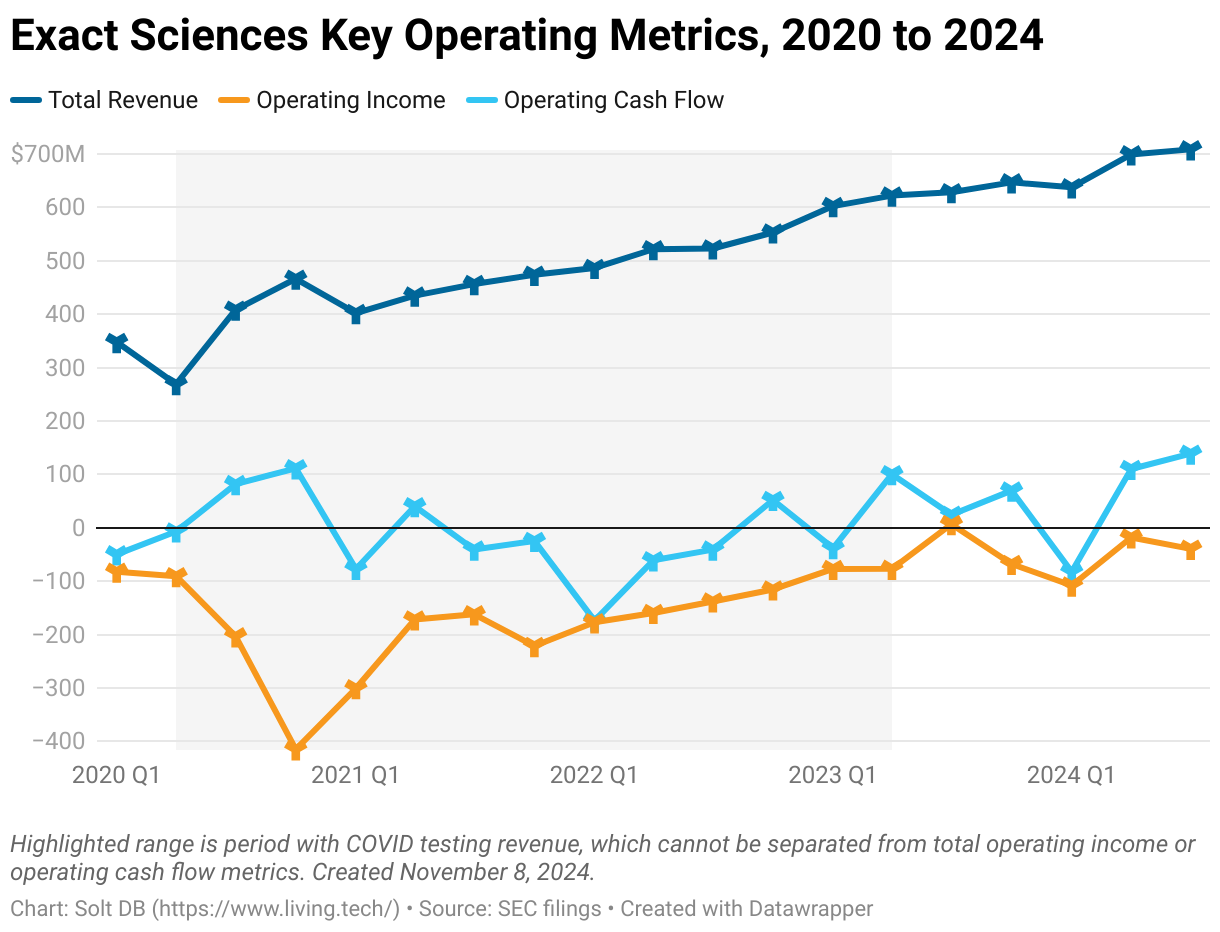

Third-quarter 2024 revenue of $709 million was easily a record, but less than expected. Sales were powered by record Screening segment revenue of $545 million and the second-highest ever Precision Oncology segment revenue of $164 million. Gross profit of $512 million was also a record. So was operating cash flow of $139 million. Operating margin of negative 5.6% was the third-best ever.

This is purely a case of missing expectations, not a deteriorating business or one that's in peril. There's no way to justify a 28% tumble that reduced the company's valuation by $3.7 billion due to slower-than-expected revenue, especially considering the factors can be easily addressed.

Management took full accountability for ho-hum operational execution during the quarter – a great sign in a world sorely lacking leadership. Exact Sciences explained that it whiffed on the key growth drivers outlined on the second-quarter 2024 earnings conference call in August due to things both within and outside of its control.

First, the back-to-back hurricanes that slammed the U.S. Southeast stung operations. An estimated 18% of all Cologuard orders occur in regions impacted by Helene and Isaac. The negative impact was most acutely felt in early October, which will weigh on Q4 2024 results.

Second, the company has been ramping its homemade software dashboard called ExactNexus, but had an embarrassing launch. A software glitch lost track of some orders, which means the company won't get paid for some tests from both its Screening and Precision Oncology. How. The. Fuck.

While regrettable, ExactNexus will be important for helping payers, providers, and sales reps quickly visualize and identify care gaps in 2025 and beyond. The colon cancer screening care gap spans an estimated 60 million Americans that are eligible for screening but fail to meet the requirement. There's a national program that incentivizes health care providers and payers to identify care gaps, but it's more aspirational than actionable. ExactNexus is a big step in addressing that for colon cancer screening – and it's backed by a treasure trove of data accumulated by Exact Sciences. No one else has that.

Cologuard is currently ordered with a roughly 22% efficiency rate within care gap programs. By contrast, Cologuard rescreens (an internal program) are now occurring at a roughly 67% efficiency rate. If Exact Sciences can merely double its ordering rate to just 44% within the care gap program, then it would represent a more than $1 billion growth opportunity. That would grow Cologuard revenue by nearly 50% from current levels and generate more than $500 million in additional annual operating cash flow. It'll get there.

Third, the significant expansion of the sales team in early 2024 has yet to drive immediate returns on investment. Sales are growing more slowly this year despite more reps, which means the sales team's productivity is significantly lower than expected. Management thinks it can address that with some low hanging fruit.

As one example, Exact Sciences knows that calling ordering physicians increases order rates. It knows that physicians added to the platform since 2020 order twice as frequently as physicians that were on the platform prior to the pandemic. However, the sales team is calling on the new segment of physicians half as much as the older segment of physicians. That's an easy thing to correct – and ExactNexus will be a key driver (when it's not losing track of payments…).

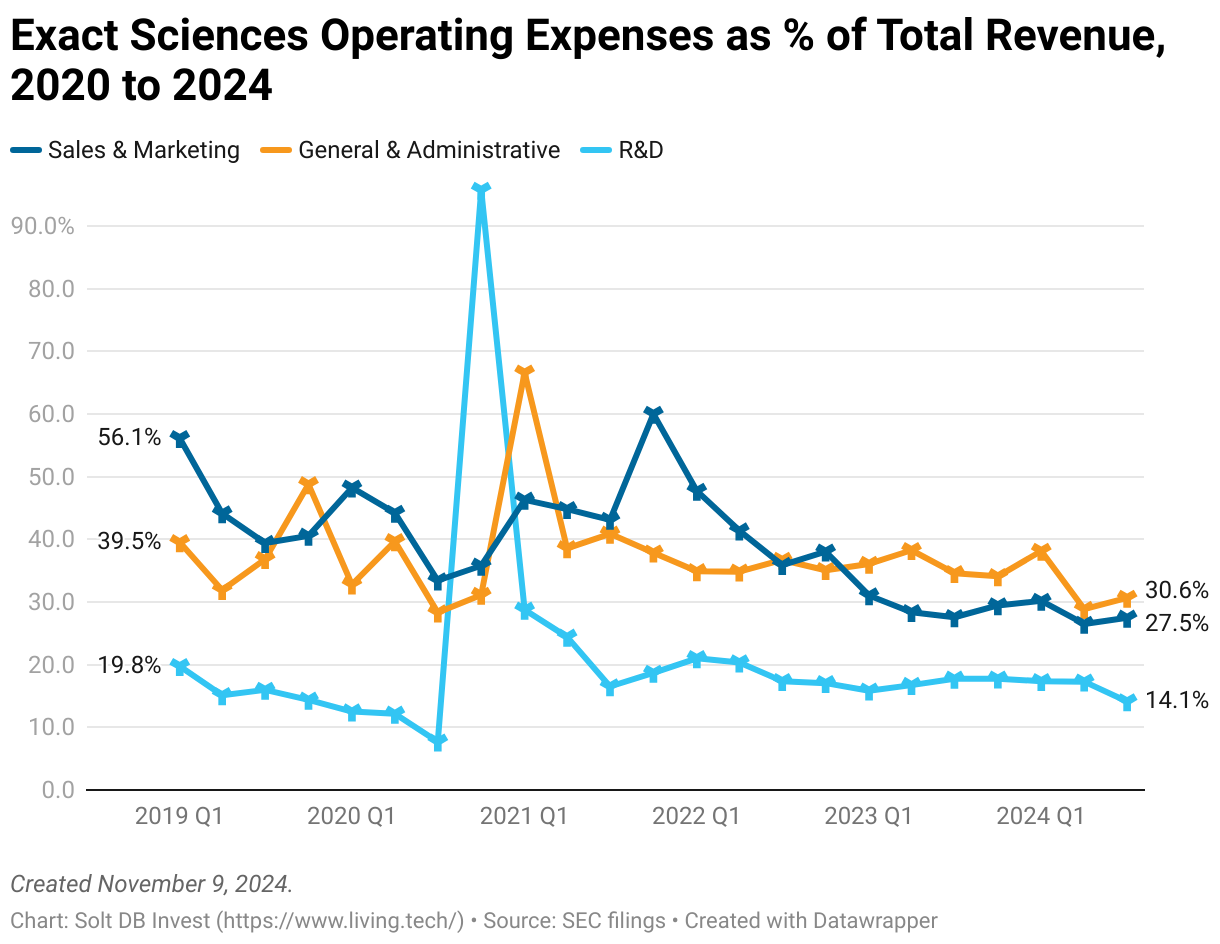

Despite the speed bumps encountered in 2024, Exact Sciences hasn't flinched on improving operating efficiency and leverage. Operating expenses as a percentage of revenue are still trending lower over time. This is called operating leverage – investors want to see companies grow revenue, but also benefit from higher revenue. Growth-at-all-costs business models might be exciting to own, but tend to not create shareholder value in the long run.

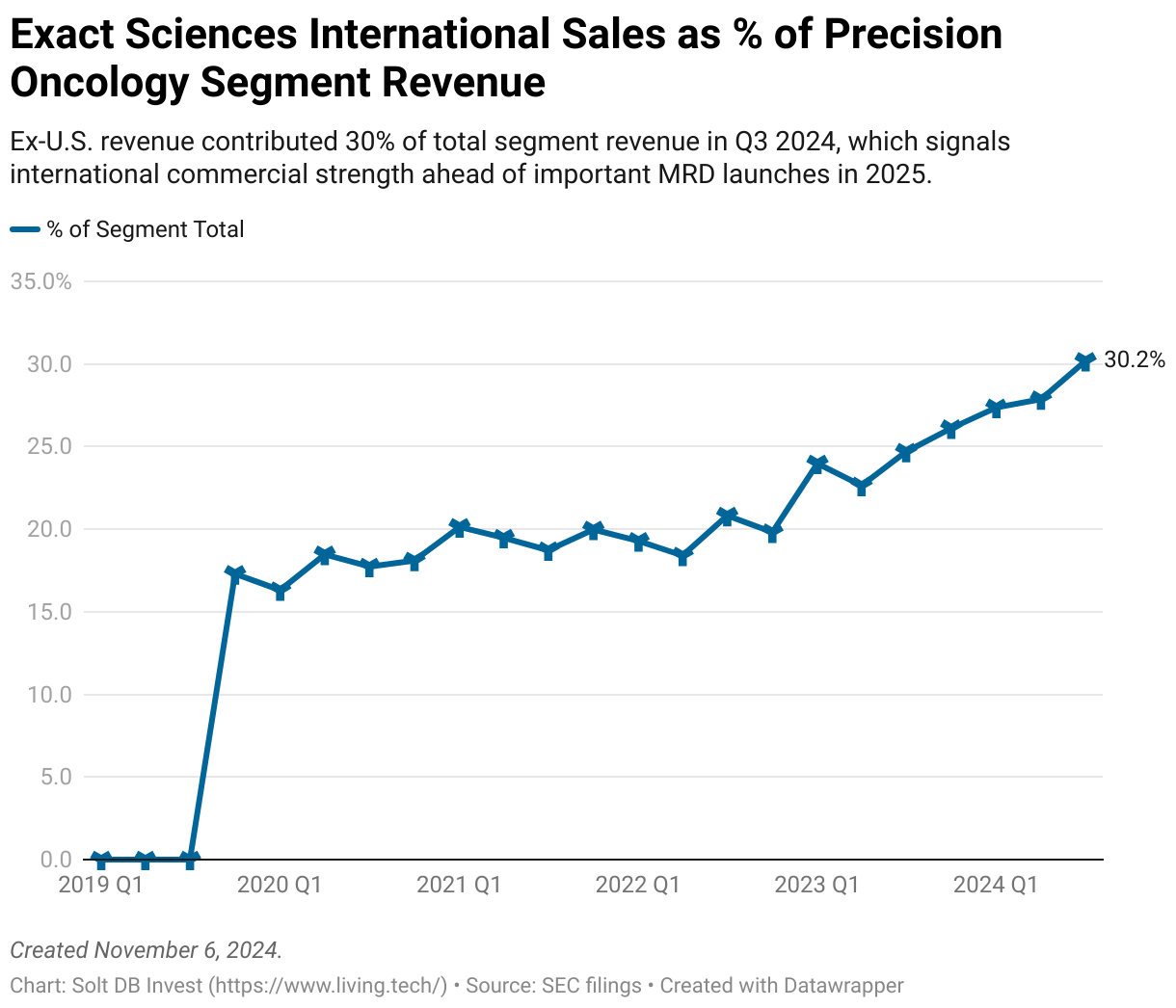

Importantly, the same favorable trends continued to drive the Precision Oncology segment. International revenue was the single-largest source of revenue in Q3 2024 for the first time ever.

This tailwind could provide a significant long-term advantage for Exact Sciences when it launches and ramps Oncodetect products. This brand of diagnostics, aimed at molecular residual disease (MRD) (sometimes the "m" stands for "minimal"), are important for monitoring cancer patients both during and after they've received treatment. MRD products promise to detect molecular signatures at the very first signs of recurrence (allowing treatment to restart sooner) and gauge if patients are responding to current treatment (potentially allowing doctors to change course sooner). Both can save costs and lives. Both can be used across virtually any type of cancer – feeding a large market opportunity.

MRD tests are one of the most important innovations in cancer diagnostics ever. The competitive landscape will be dominated by companies with large commercial footprints, including Roche, Exact Sciences, Guardant Health, NeoGenomics, and Natera. Only Roche and Exact Sciences have meaningful international footprints as of late 2024.

Importantly, a steady cadence of product launches in the Oncodetect portfolio (approvals and launches will occur for specific types of cancer) in the next few years will help the Precision Oncology segment return to growth within the lucrative U.S. market, where it's been relatively stagnant since the beginning of 2021.

Commercial Updates

Exact Sciences has a diverse slate of tailwinds that promise to power growth in 2025 and beyond.

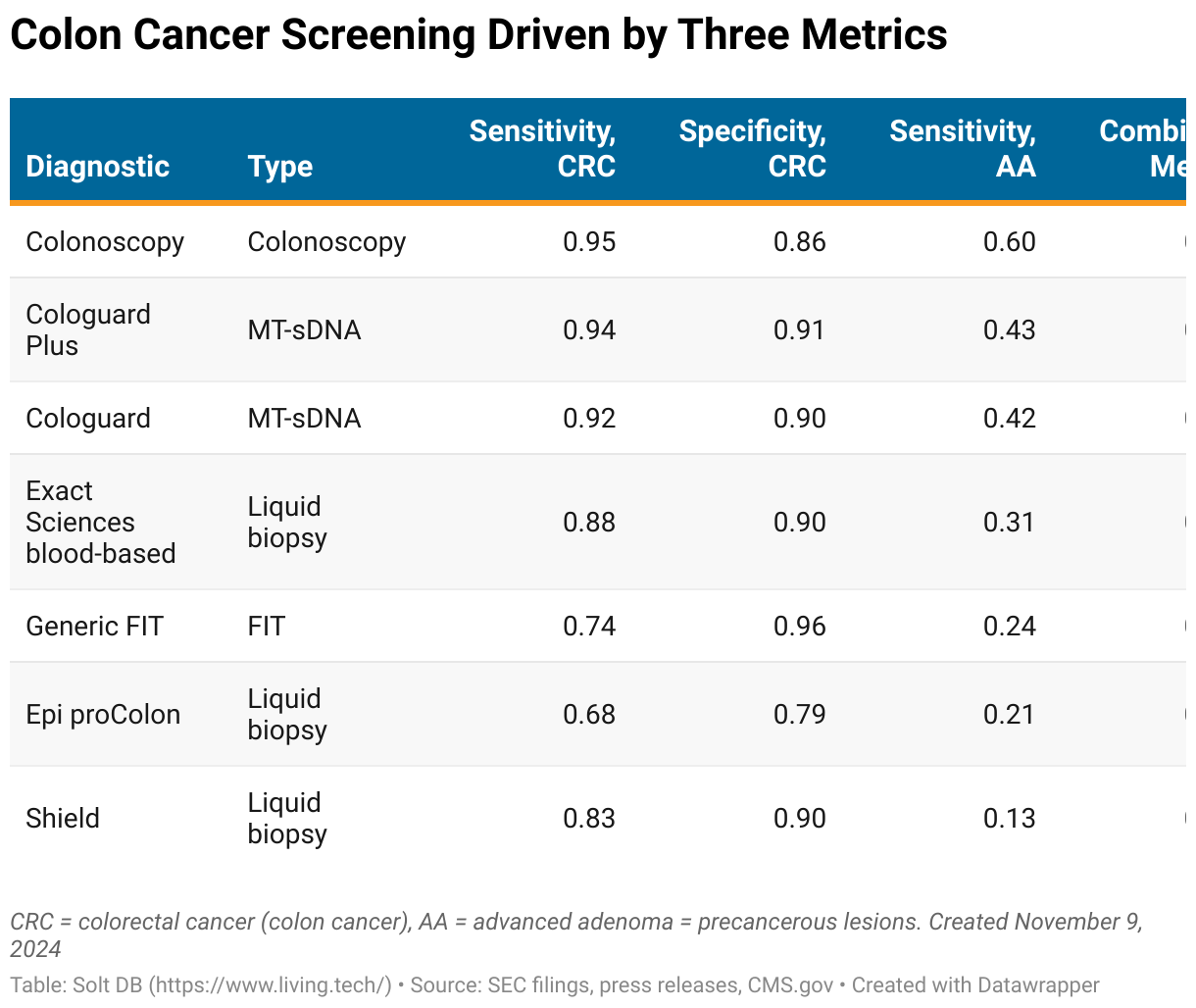

The business provided recent data for its blood-based colon cancer screening test. To recap:

- Sensitivity of colon cancer: The ability to correctly identify individuals with colon cancer. Overall sensitivity is most often communicated, which is the rate of detecting cancer at any stage. Tests are differentiated by their ability to detect early-stage cancers (Stage I and Stage II). It's easier to detect advanced cancers, which makes early-stage detection the biggest driver of overall sensitivity.

- Specificity of colon cancer: The ability to correctly identify healthy individuals. It's generally not great to scare the shit out of people by telling them they have cancer when they don't.

- Sensitivity of precancerous lesions: The ability to detect benign masses that can become cancer. Precancerous lesions are more important for some cancers (cervical or colon) than others (lung).

The company's blood-based colon cancer screening tool delivered sensitivity of 88%, specificity of 90%, and precancerous lesion detection of 31%. Guardant Health has touted significant commercial interest in its first-to-market test Shield, but it has objectively worse performance. Shield had sensitivity of 83%, specificity of 90%, and precancerous lesion detection of just 13%.

That seems like an easy win for Exact Sciences, although the company has long played down the blood-based opportunity in the market. #awkward

Exact Sciences expects to launch its first Oncodetect MRD test in the first half of 2025, followed by a steady cadence of launches in specific tumor types through the rest of the decade. The MRD market is expected to represent a multi-billion dollar opportunity and fundamentally change cancer care. The company promises to be a dominant player in the market's formation.

The first Oncodetect data have been accepted for publication in a major scientific journal. The data are under embargo, but management teased it will reveal them publicly in January 2025. That could line up with the JP Morgan Healthcare conference, which typically sees major product announcements.

Finally, Cologuard Plus is expected to launch in the first half of 2025. There are some questions about the company's ability to earn favorable pricing for the product. To be clear, it will earn at least the same pricing as the current Cologuard test. It also has a lower cost of goods sold, which means it'll have higher margins even without a price increase.

Exact Sciences is simply seeking a meaningful increase in reimbursement. There are multiple regulatory pathways to do so, but one takes years and the other could be implemented immediately. Investors will have to patiently await an update.

Forecast & Modeling Insights

(Reduced.)

When I build risk-adjusted net present value (rNPV) models for precommercial drug developers, I need to convert molecules into numbers before I can understand the attractiveness of an opportunity. Although the molecules can change in value due to competitive positioning and internal data readouts, these models are inherently forward looking.

A business like Exact Sciences has revenue, profits, and cash flows; which means it can be modeled like a "traditional" business. It also has a lot of data and a relatively well-defined market opportunity, which makes it easier to model multiple years into the future with more confidence relative to a precommercial drug developer.

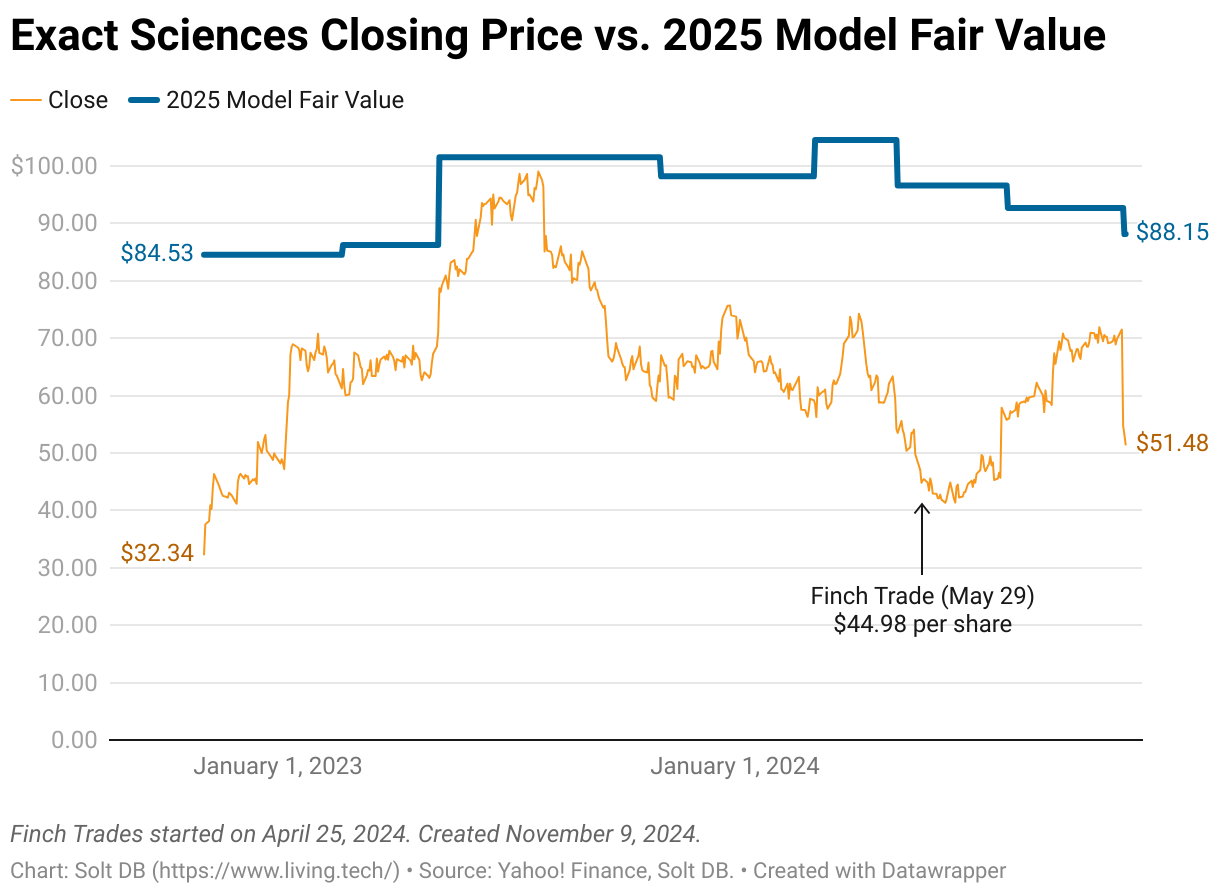

The fair value estimate for Exact Sciences has been based on a 2025 model since late 2022. The model has been refined based on the best information available at the time and shifts in the growth trajectory.

There's always a balance between showing members how the sausage gets made and simplifying what gets communicated. At the end of the day, you and I primarily care about making money. But hopefully this visualization helps show the modeling is objective and that the sky isn't falling just because the fair value estimate has been revised lower.

Now that we're in late 2024, the current 2025 model is less forward-looking than it was two years ago. That means there's more confidence in the model and less room for variability, since there are less assumptions and more hard data baked in.

The new 2025 model expects (all year-over-year calculations use the midpoint of 2024 revenue guidance):

- Full-year 2025 revenue of $3.126 billion, representing YoY growth of 14.1%

- Screening revenue of $2.384 billion, representing YoY growth of 16.5%

- Precision Oncology revenue of $701.4 million, representing YoY growth of 7.5%

- Total operating expenses of $2.317 billion, representing YoY growth of 4.4%. This includes an estimated $50 million in intangible asset impairment charges, but that could be significantly higher (see below).

- Operating loss of $64.719 million, compared to an operating loss of $215.871 million in 2024

- Although I don't have a reliable way to model operating cash flow due to various adjustments, investors can expect between $350 million and $500 million based on the other modeled metrics shared above

Investors might expect some adjustments in the next few years to the intangible assets and goodwill balances on the balance sheet. These represent non-cash charges, but essentially write-off the value assigned to previous acquisitions.

It can look ugly (because net income falls by the amount written off), but these write downs are primarily paper adjustments and don't have much impact on cash balances or cash flow. It's still important to understand.

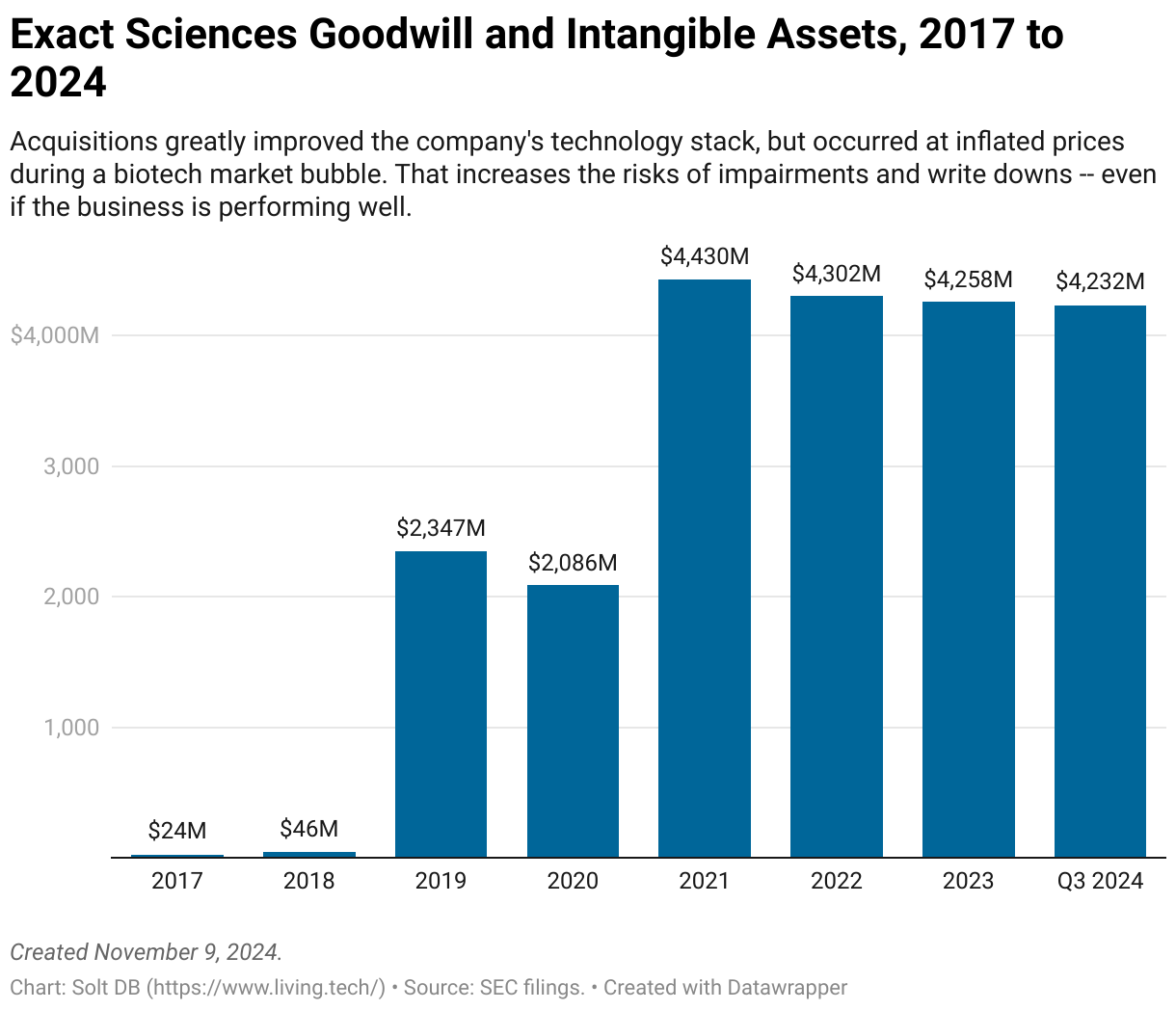

Exact Sciences went on an acquisition spree in recent years to build its technology stack. Many of those acquisitions have benefited the business, including reducing the cost of goods sold for Cologuard Plus, improving the performance of MRD tools launching next year, and giving the business a multi-cancer early detection (MCED) platform to compete with GRAIL.

Acquisitions typically occur at a premium. From an accounting perspective, that premium (the difference between the book value of the acquired business and the acquisition price) is recorded on the balance sheet as an asset, specifically as a goodwill or intangible asset line item.

These assets are slowly amortized ("rolled off the books") by recording an additional non-cash operating expense each quarter. For example, Exact Sciences recorded $71 million in amortization costs in the first nine months of 2024.

However, the company ended September 2024 with $2.367 billion in goodwill and $1.864 billion in intangible assets (some unrelated to acquisitions). That's a lot.

On the one hand, it made some big acquisitions in recent years. Many of those can provide significant value in the near future, justifying the acquisition at a high level. On the other hand, many acquisitions were made at inflated prices during a bubbly market for biotech. And a smaller acquisition or two have already not panned out.

Investors might expect some large, one-time impairment charges in the next few years to adjust the value of goodwill and intangible assets on the balance sheet. It would result in a hilariously bad operating loss, but to reiterate, it wouldn't impact real-world operations.

Margin of Safety & Allocation

Exact Sciences is considered an Anchor position. The current modeled fair valuation for the company based on my updated 2025 model is below:

- Market close November 8: $51.48 per share

- Modeled Fair Valuation: $88.15 per share

- Allocation Range: Up to 15%

Exact Sciences reported 185.076 million shares outstanding as of November 4, 2024. The modeled fair valuation above assumes 186.927 million shares outstanding, which is equivalent to 1% dilution by the end of 2025.

Further Reading

- November 2024 press release announcing Q3 2024 operating results

- November 2024 regulatory filing (10-Q) detailing Q3 2024 operating results

- August 2024 research note analyzing Q2 2024 operating results

.png)

-cropped.svg)