.svg)

Finch Trades are posted to Discord as soon as they happen. Want an email alert every time a Finch Trade article like this goes live? Sign up in your profile.

Exact Sciences spooked investors with surprisingly slow growth for Cologuard in the first quarter of 2024. Screening revenue increased just 7.1% compared to the year-ago period. Meanwhile, operating expenses jumped 9.8% in that span as the company began hiring additional sales reps.

The slope change on the growth trajectory coincides with the upcoming regulatory approval of a blood-based colon cancer screening tool, Shield from Guardant Health.

I think everyone is getting a little too carried away here. If I can add Exact Sciences below $45 per share – a market valuation of just $8.3 billion – then I'm all over it.

The Trade

Exact Sciences is considered an Anchor position. I purchased 22.23 shares at $44.98 per share on May 29, 2024.

%20Confirmation.png)

Scenario Analysis

My modeling is based on valuing assets, contextualizing competitive landscape dynamics, and weighing the probabilities of favorable and unfavorable scenarios. This trade was driven by the following considerations.

Cologuard Remains a Dominant Brand (positive)

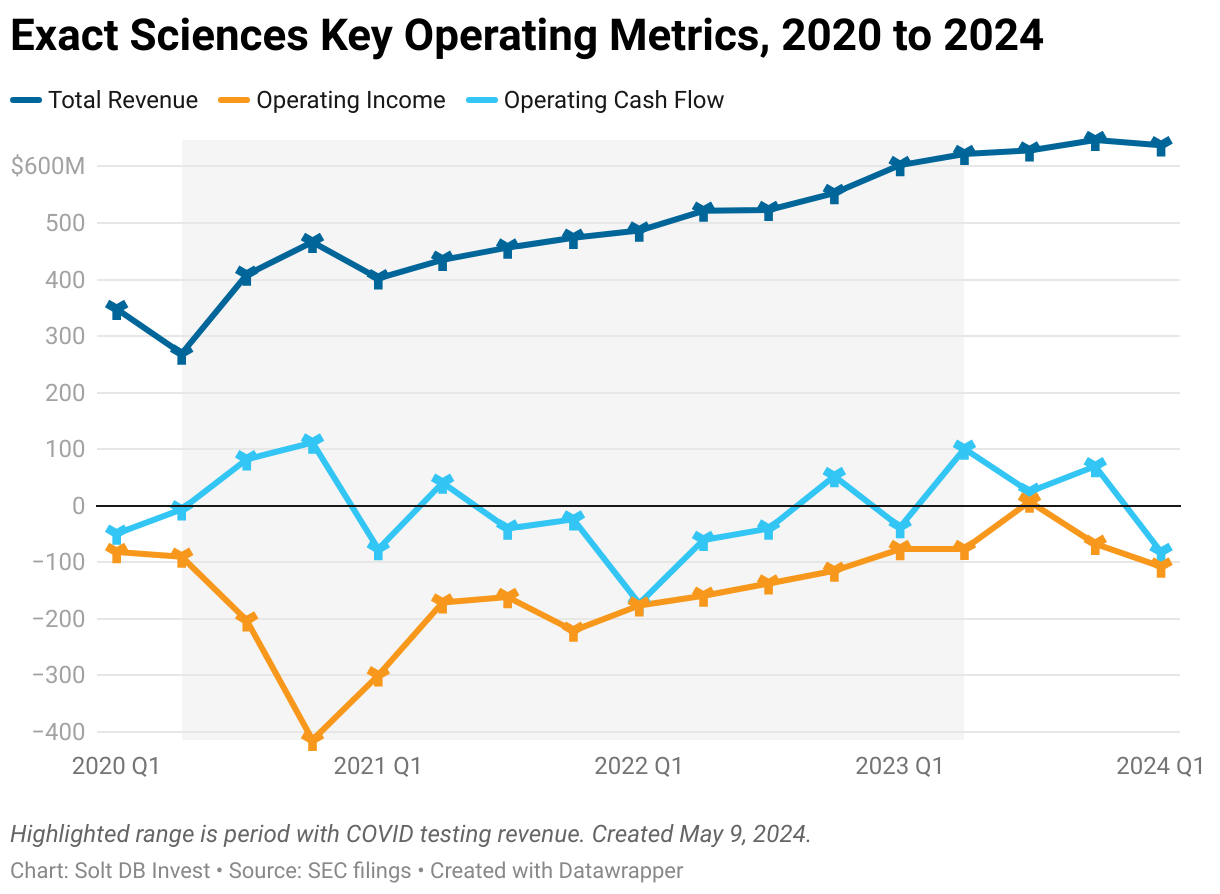

Exact Sciences generated 75% of its total revenue from Cologuard in 2023, so investors are right to be a little nervous about the inability to grow revenue in the last three quarters. But this has happened before.

Revenue flatlined from the third quarter of 2019 through the first quarter of 2020. Quarter-over-quarter revenue growth was negative three other times since the beginning of 2019 – and I've excluded the pandemic from that. The recent trend seems a little surprising because the business had enjoyed an uninterrupted run of revenue for eight straight quarters. That's two years of "up and to the right."

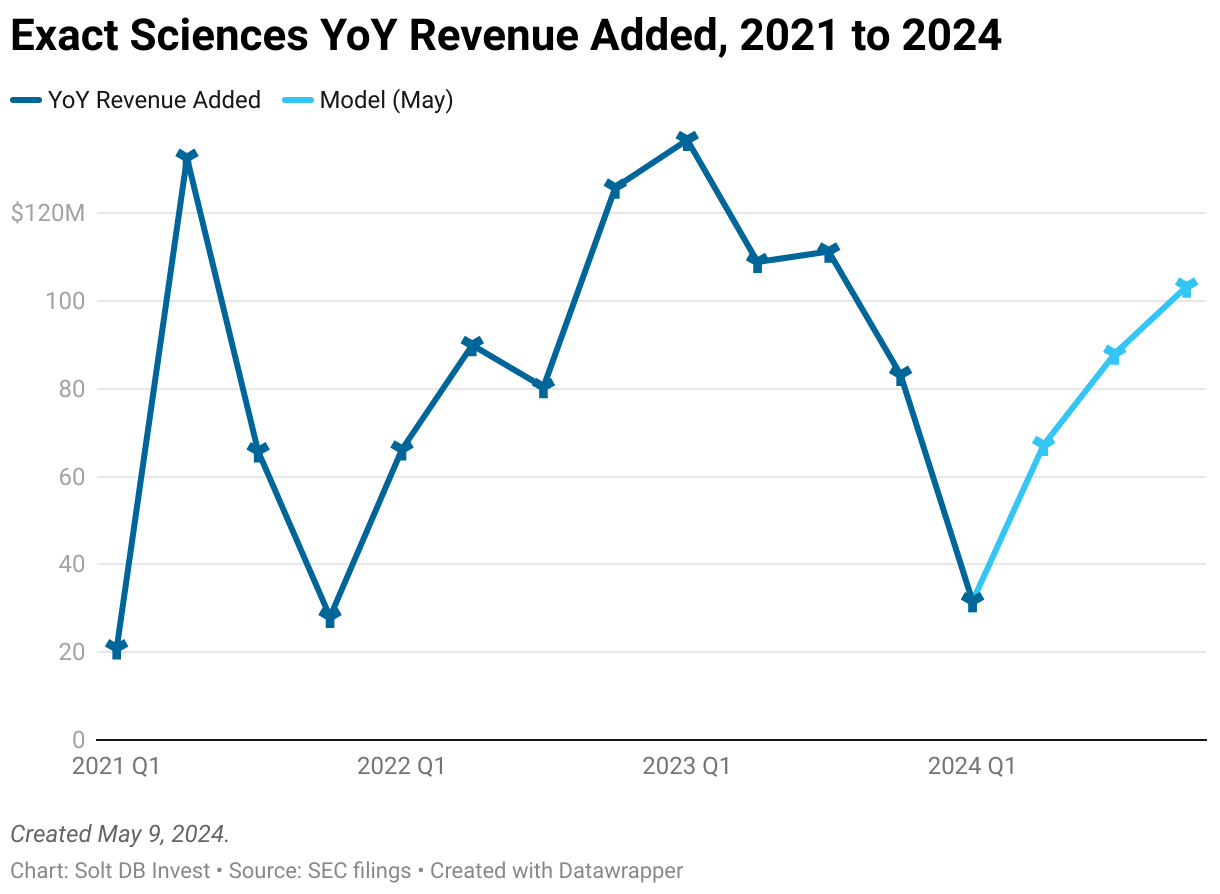

There's also been a "peak-and-trough" trend in Cologuard's growth. Revenue surges are awesome when they happen, but create a difficult comparison for the same period in the future. If that continues, then the first quarter of 2024 isn't alarming or out of place. This can be visualized by comparing year-over-year revenue added, where troughs represent difficult comparisons and a surge in prior-year revenue.

Although I'll be keeping an eye on this trend, I'm confident there's plenty of room for Cologuard to continue growing for the rest of the decade. If management's long-term goal of capturing 40% of the colon cancer screening market is realized, then Cologuard would generate annual revenue of $7.2 billion. It generated $1.8 billion in revenue in 2023.

Gastroenterologist offices are understaffed, which has forced many to turn away low-risk individuals for colonoscopies. In fact, doctors are now beginning to use Cologuard as a first-line treatment for this patient population.

Cologuard Plus, formerly Cologuard 2.0, offers meaningful improvements to the current product. That can help to mitigate competitive pressures and continue winning over doctors. Meanwhile, the company has already begun developing Cologuard 3.0.

The Business is Healthy (positive)

Investors balked at management's plan to increase the sales team. Hiring for expected growth can backfire if growth doesn't materialize – just look at AVITA Medical. It's generally better to hire when growth leaves no other option; a business is bursting at the seams and needs more hands on deck.

I think a key difference is the size and maturity of Exact Sciences. Management has orders of magnitude more data and experience than, say, AVITA Medical about how its business operates, and what levers to pull, when.

Exact Sciences is also financially healthy. The business generated $156 million in operating cash flow in 2023. The sales team hiring spree could dent that this year, but the company can comfortably self-fund growth and take a calculated risk with expansion.

Additionally, the business exchanged convertible notes in April 2024. The transactions increased the cash balance by $266.8 million. For reference, Exact Sciences reported negative operating cash flow of $301 million combined during the four years spanning 2019 to 2022. Guardant Health burned through $325 million in 2023 alone.

Competition is Heating Up (negative)

Exact Sciences will have meaningful competition for the first time since Cologuard launched. Guardant Health is likely to earn regulatory approval for Shield, a blood-based screening tool. Geneoscopy earned regulatory approval for ColoSense, the only other multi-target stool DNA (mt-sDNA) tool aside from Cologuard.

ColoSense does look like it could be very competitive, so a lower list price could force Exact Sciences to lower its prices, too.

Competition isn't necessarily a bad thing. In this case, it's a sign of the large overall market opportunity for colon cancer screening tools, which is estimated at $18 billion per year. But it could make the market a little less predictable until analysts and companies better understand how the competitive dynamics shift.

To be fair, Exact Sciences is developing its own blood-based screening tool, although this format will be used for slightly different patient populations than Cologuard. The company is also suing Geneoscopy for infringing multiple patents.

It's also important for biotech investors to remember the most important metrics for success: commercial infrastructure and execution. Exact Sciences is much better positioned to leverage its size, infrastructure, experience, and healthy business to thwart competitive threats than either Guardant Health or Geneoscopy (partnered with the much larger Labcorp).

Margin of Safety & Allocation

Exact Sciences is considered an Anchor position. The current modeled fair valuation for the company based on my 2025 model is below:

- Market close July 3: $43.19 per share

- Modeled Fair Valuation: $96.61 per share

- Allocation Range: Up to 15%

Exact Sciences reported 184.529 million shares outstanding as of May 7, 2024. The modeled fair valuation above assumes 186.400 million shares outstanding, which is equivalent to 1.0% dilution by the end of 2025.

Further Reading

- May 2024 research note analyzing Q1 2024 operating results

- May 2024 press release announcing Q1 2024 operating results

- May 2024 regulatory filing (10-Q) detailing Q1 2024 operating results

- April 2024 press release announcing debt exchange

.svg)

.svg)

.avif)

.png)

.svg)

.svg)

.svg)