.svg)

Exact Sciences didn't have a very strong first quarter. Revenue grew by single digits, operating cash flow turned negative for the first time in a year, and operating expenses surged. On the earnings call in May 2024, management told investors to remain patient and trust the company's internal analytics, which suggested the slowdown would be temporary.

Wall Street did what it always does: Remained calm, showed confidence in their models and underlying strength of the business, and agreed to patiently await the next quarterly update.

Just kidding.

Analysts panicked. Every price target was reduced by between 12% and 30% with each citing the looming threat of blood-based screening tools. All but one lowered price target was issued in late June or early July, which was after shares had already lost 33% of their value since the earnings call. Then, Guardant Health earned regulatory approval to stoke the narrative that Exact Sciences was about to crack – all before the company had the chance to "defend itself" with the next quarterly update.

When management got the opportunity on the second-quarter 2024 earnings call July 31, it delivered a knockout blow to doubtful analysts.

By the numbers

Exact Sciences remains a no-brainer investment. That might be doubly true as investors become increasingly nervous about stock valuations and the strength of the U.S. economy.

The business sold 1 million Cologuard tests in a quarter for the first time. Why is that important? There are only about 5 million colonoscopies performed annually in the United States – with a huge backlog and long wait times. The company is well positioned to become the standard of care for low-risk individuals. There's plenty of growth left, too. The business thinks it can eventually process 3.5 million Cologuard tests each quarter.

Although the Screening segment generates almost 75% of total revenue, the Precision Oncology segment is thawing at a fortuitous time. The segment provides clinical diagnostics to help guide treatment decisions for solid tumor cancers, led by the flagship Oncotype Dx for early-stage therapy selection. New launches under the Oncodetect (recurrence testing), OncoExtra (therapy selection using tissue biopsy), and Oncoliquid (therapy selection using liquid biopsy) brands in the coming years should reignite meaningful long-term growth.

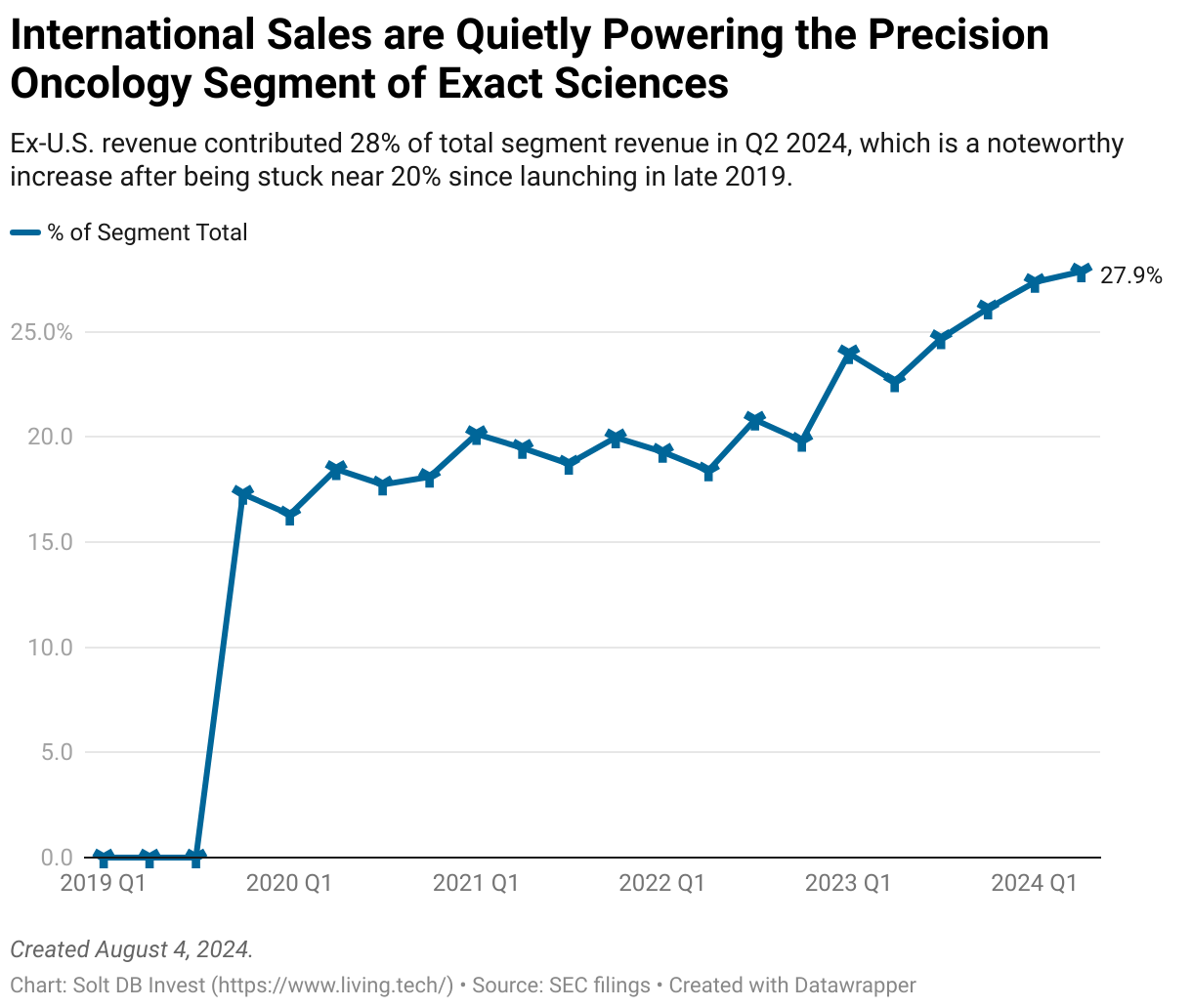

In the meantime, a faster-than-expected commercial ramp in Japan has led to a 64% increase in international revenue since the fourth quarter of 2022. International sales now comprise 28% of the segment's total revenue, which is noteworthy considering it was "stuck" near 20% for nearly three years.

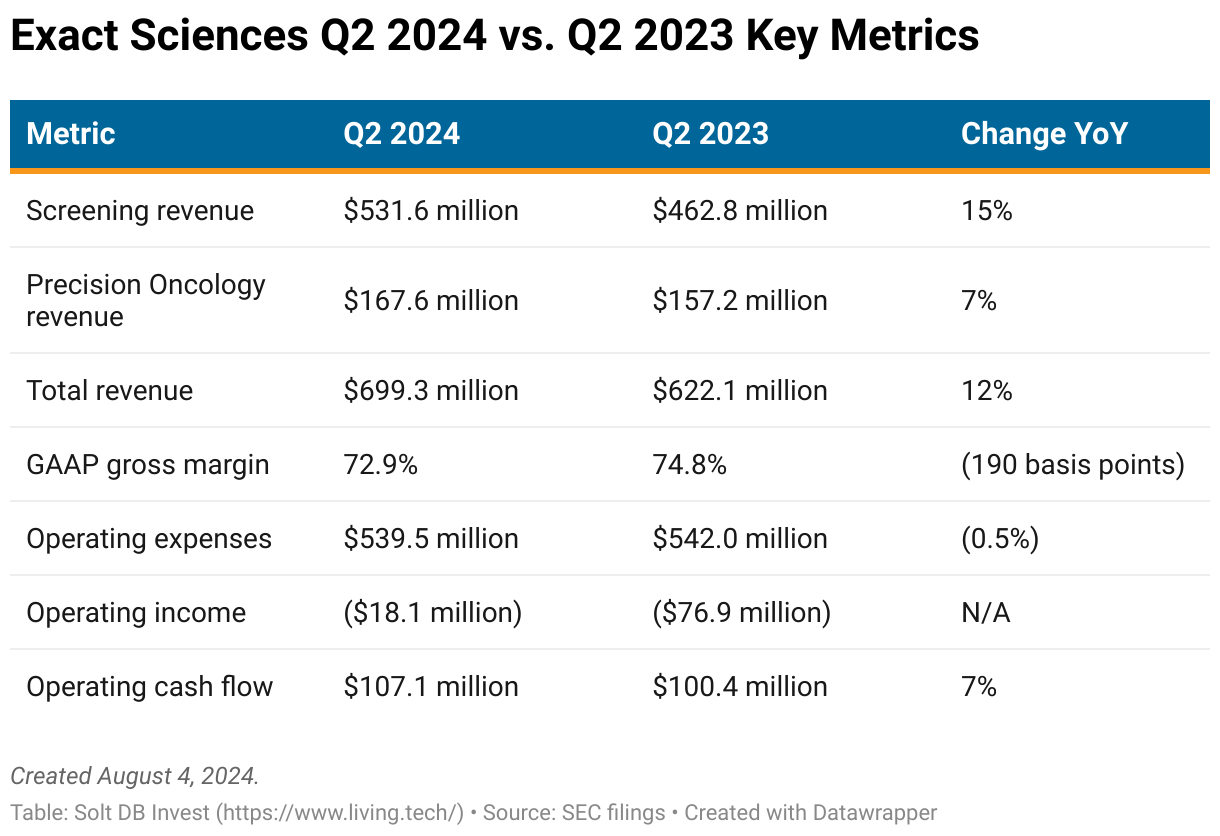

The strong showing in the second quarter resulted in year-over-year growth of 15% in the Screening segment, 7% in the Precision Oncology segment, and 12% overall. Operating expenses were flat from the year-ago period, which led to the highest operating margin ever – at negative 2.6%. The business also generated $110 million in operating cash flow and ended June 2024 with $947 million in cash, compared to a cash balance of $604 million a year ago.

Exact Sciences has plenty of internal growth opportunities to invest in, but the company also has the financial flexibility to make strategic acquisitions or quickly address any commercial snags for upcoming product launches.

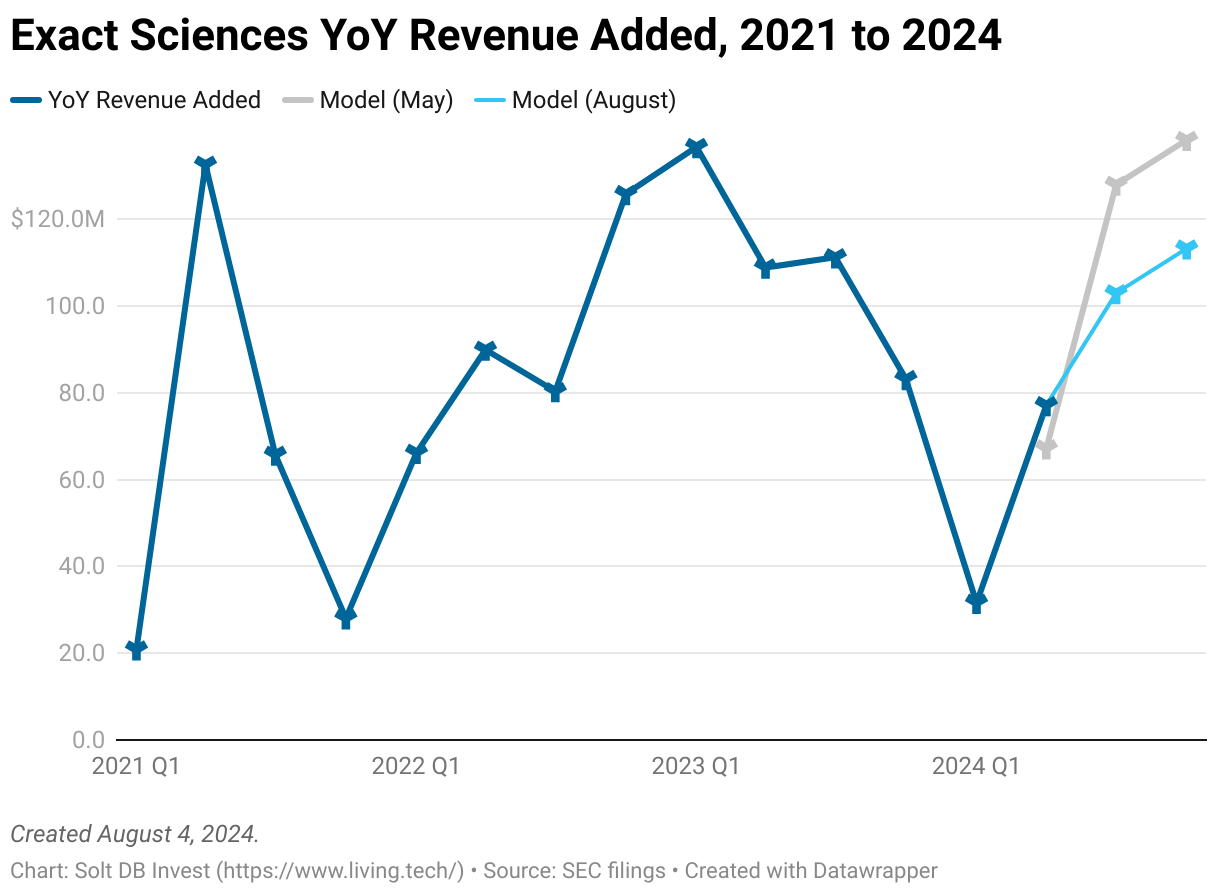

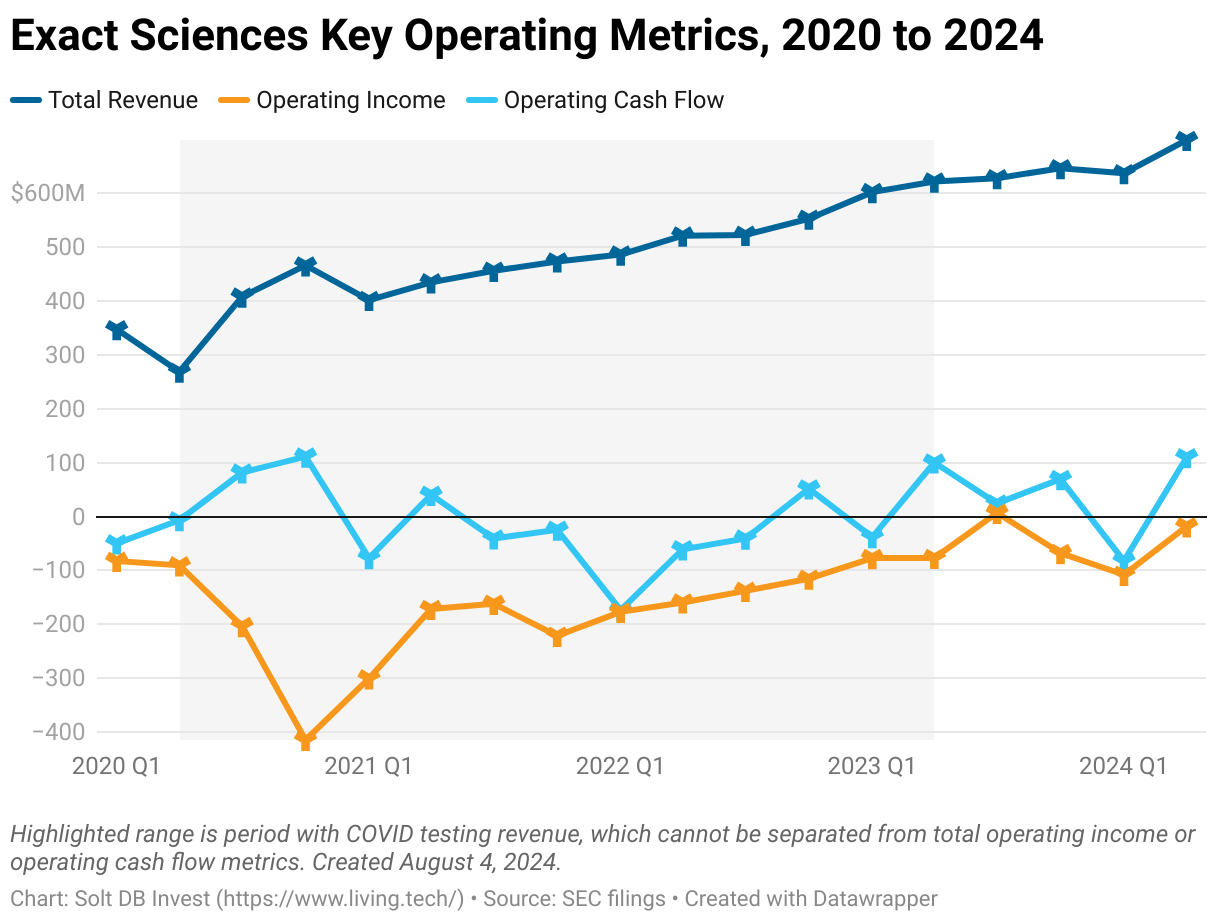

The business struggled with some tough year-over-year comparisons in the first quarter. To objectively determine if investors should have been panicking, I looked at historical patterns across six key metrics with a series of data visualizations in the May 2024 research note discussing last quarter's operating results. That analysis revealed no cause for concern or alarm. Revisiting the same data visualizations shows that was the right conclusion – and transparently shows I'm not just making shit up.

First, I directed the gaze of investors at the level of revenue added from year-ago periods. This helped to visualize the difficult year-over-year comparisons from Q1 2024. It also showed the company had encountered similar dynamics in the past, but swiftly recovered each time. In fact, the business outperformed the recovery anticipated by my Q2 2024 model.

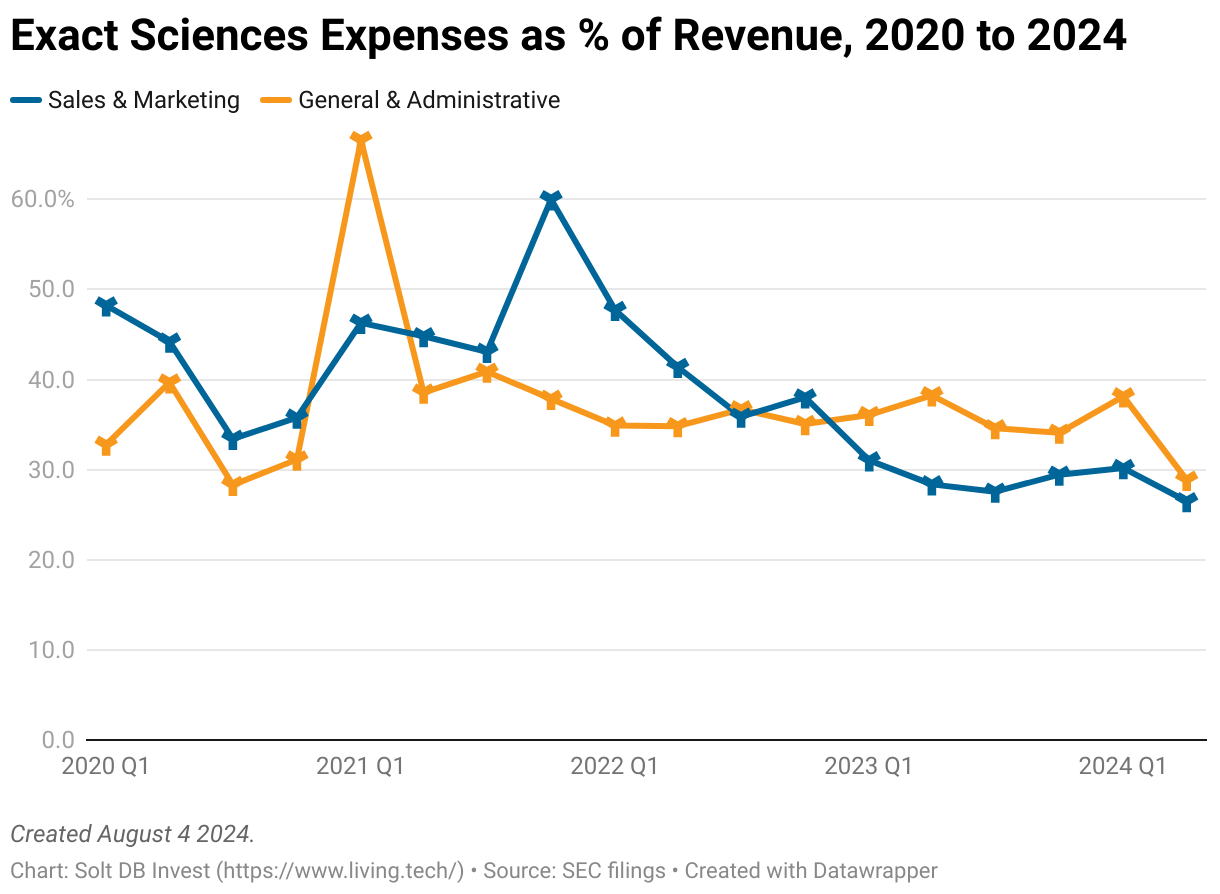

Second, analysts were concerned about a sudden increase in sales and marketing expenses and general and administrative expenses. These metrics should be evaluated as a percentage of revenue for a growing business such as Exact Sciences. There was an uptick in Q1 2024, but both fell to multi-year lows in Q2 2024.

Third, it's always important to keep an eye on key operating metrics: revenue, operating income, and operating cash flow. If management was right about the first-quarter deterioration being transient, then investors didn't have much reason to worry as the underlying business remained strong. There was no doubt about the recovery in Q2 2024.

Forecast & Modeling Insights

(Reduced 2024 and 2025 models.)

To reiterate, I've refined my models for Exact Sciences to improve the accuracy for 2025 performance. There's nothing wrong with the business. My job is simply to provide the most accurate outlooks, not to stubbornly stick to past models just because they might be more favorable.

The updated models reflect lower revenue to account for slower Cologuard growth, primarily because the numbers are getting larger. The brand is still expected to add at least $300 million in revenue in each 2024 and 2025. This refinement may end up being too conservative if Cologuard Plus gains market share more rapidly than expected in 2025 and beyond, but I'll let commercial execution prove me wrong to the upside.

Meanwhile, management has done a masterful job keeping operating expenses in check, which is forcing me to pull forward improvements in operating margin. The business could achieve its first-ever quarterly operating profit in 2024 (without favorable adjustments). The business is close enough to profitable operations and can fund itself, so it may dip in and out of profitability as it plows into growth opportunities. That wouldn't be a cause for concern for me.

It may not show up on financial statements, but the increasing strength and cash generation makes the business more resilient, too – an important consideration for investors.

Highlighted metrics from the updated 2024 model (the Margin of Safety is based on the 2025 model):

- Full-year 2024 revenue is now expected to be $2.854 billion vs. a prior model of $2.902 billion (-2%). The company's guidance has a midpoint of $2.832 billion.

- Full-year 2024 operating expenses are now expected to be $2.208 billion vs. a prior model of $2.333 billion (-5%). This results in an operating loss of less than $100 million and an operating margin of negative 3.5%. The last time the business had an operating loss below $100 million it sported an operating margin of negative 1,128%.

Highlighted metrics from the updated 2025 model (the Margin of Safety is based on this model):

- Full-year 2025 revenue is now expected to be $3.283 billion vs. a prior model of $3.420 billion (-4%).

- Full-year 2025 operating expenses are now expected to be $2.282 billion vs. a prior model for $2.401 billion (-5%). This results in operating income of $178 million vs. a prior model of $345 million.

Margin of Safety & Allocation

Exact Sciences is considered an Anchor position. The current modeled fair valuation for the company based on my 2025 model is below:

- Market close August 2: $57.35 per share

- Modeled Fair Valuation: $92.71 per share (reduced from $96.61 per share)

- Allocation Range: Up to 15%

Exact Sciences reported 184.770 million shares outstanding as of July 30, 2024. The modeled fair valuation above assumes 186.618 million shares outstanding, which is equivalent to 1% dilution.

Further Reading

- August 2024 press release announcing Q2 2024 operating results

- August 2024 regulatory filing (10-Q) detailing Q2 2024 operating results

- May 2024 Finch Trade in which I purchased $1,000 of Exact Sciences at $44.98 per share

- May 2024 research note analyzing Q1 2024 operating results

.png)

-cropped.svg)