.svg)

Legendary investors Howard Marks and Joel Greenblatt sat down for a chat during the roaring markets of the coronavirus pandemic. The exuberance at the time made it seem like their investing approaches – distressed debt investing and value investing, respectively – were antiquated.

Greenblatt countered with a simple analogy: investing is like catching a bus that doesn't arrive on time.

If you get the basics right – you checked the schedule, you accounted for service interruptions, and you have a bus pass to pay the fare – then you know a bus will eventually arrive. It'll just be a little late. But waiting sucks. If you grow impatient and walk to another bus stop around the block, then you might feel good about changing your strategy. You took action, dammit. But if you keep impatiently walking back and forth between stops, then you might never catch the damn bus.

In other words, Greenblatt is confident in his strategy so long as he gets the basics right. He has the track record to back it up. While presiding over Gotham Capital from 1985 to 1994, the famed value investor delivered annual returns of 30% net of fees. Not bad for a period that includes Black Monday and precedes the epic returns of the Dot Com Bubble.

Although "value investing" is today associated with boring companies like International Paper and The Clorox Company, Greenblatt followed a purer framework he called "The Magic Formula." He simply worked to uncover undervalued companies with high earnings yields and a high return on invested capital. And like many legendary investors, he wasn't afraid of concentrated positions in his highest conviction investments.

This is similar to my current investing style embodied by Finch Trades.

If I continue to find undervalued precommercial drug developers that successfully commercialize high-impact assets, then they'll have a high earnings yield in the future (based on my cost basis). The single-most important metric for uncovering undervalued precommercial drug developers is the probability of success of drug candidates, which, if I'm right, will lead to a high return on invested capital (based on R&D expenses relative to future drug product revenue).

As for concentration, two companies represent 88% of total invested capital in Finch Trades so far. That leads to significant volatility, but also creates the potential for significant outperformance.

Greenblatt is no stranger to volatility. I don't normally quote Wikipedia entries, but this blurb perfectly captures the risk and reward of concentrated positions in undervalued businesses:

Several studies from around the world have found Greenblat's formula tends to result in long-term outperformance relative to market averages, but is also associated with significantly higher short-term volatility and sharper drawdowns due to his concentrated approach.

I'm certainly feeling that right now, but as I argue in the Finch Trades review section below the current approach is well-positioned for outperformance.

I'm also aware that large drawdowns are uncomfortable, and my current approach wouldn't work if I ran a fund (or would lead to many angry phone calls and emails at best). That's why I'm working towards my Chartered Financial Analyst (CFA) designation. I want to formalize my financial knowledge and learn how to quantitatively adjust portfolios in any macroeconomic environment.

Although I won't earn a CFA until spring 2028 at the earliest, I'll begin to integrate learnings into my biotech-specific modeling frameworks starting this year.

Do Tariffs Impact Drug Developers?

Not really, but there are exceptions. Even then the impacts should be relatively minor.

The current Solt DB coverage ecosystem includes three types of companies:

- Mostly precommercial drug developers

- A few commercial drug developers hitting the sweet spot of their growth trajectory

- A couple of tools providers

Tariffs and precommercial drug developers

For the first group, tariffs have almost no impact. Companies like Relay Therapeutics and Kymera Therapeutics don't manufacture meaningful volumes of drug substance. Although they're building infrastructure today to satisfy their commercial ambition years from now, many emerging companies are investing in onshore or nearshore drug manufacturing following the events of the last five years. That means they're less likely to be impacted by tariffs in the future, which might not be true for companies with established footprints.

Precommercial drug developers might see minimal cost increases for specific types of R&D activities. The United States doesn't manufacture most of the plastics and chemical reagents that power lab consumables. This is likely to increase the costs of early discovery and preclinical work. Then again, most consumables are ridiculously overpriced, so perhaps vendors like Thermo Fisher will eat tariff-related cost increases out of the goodness of their price-gouging hearts.

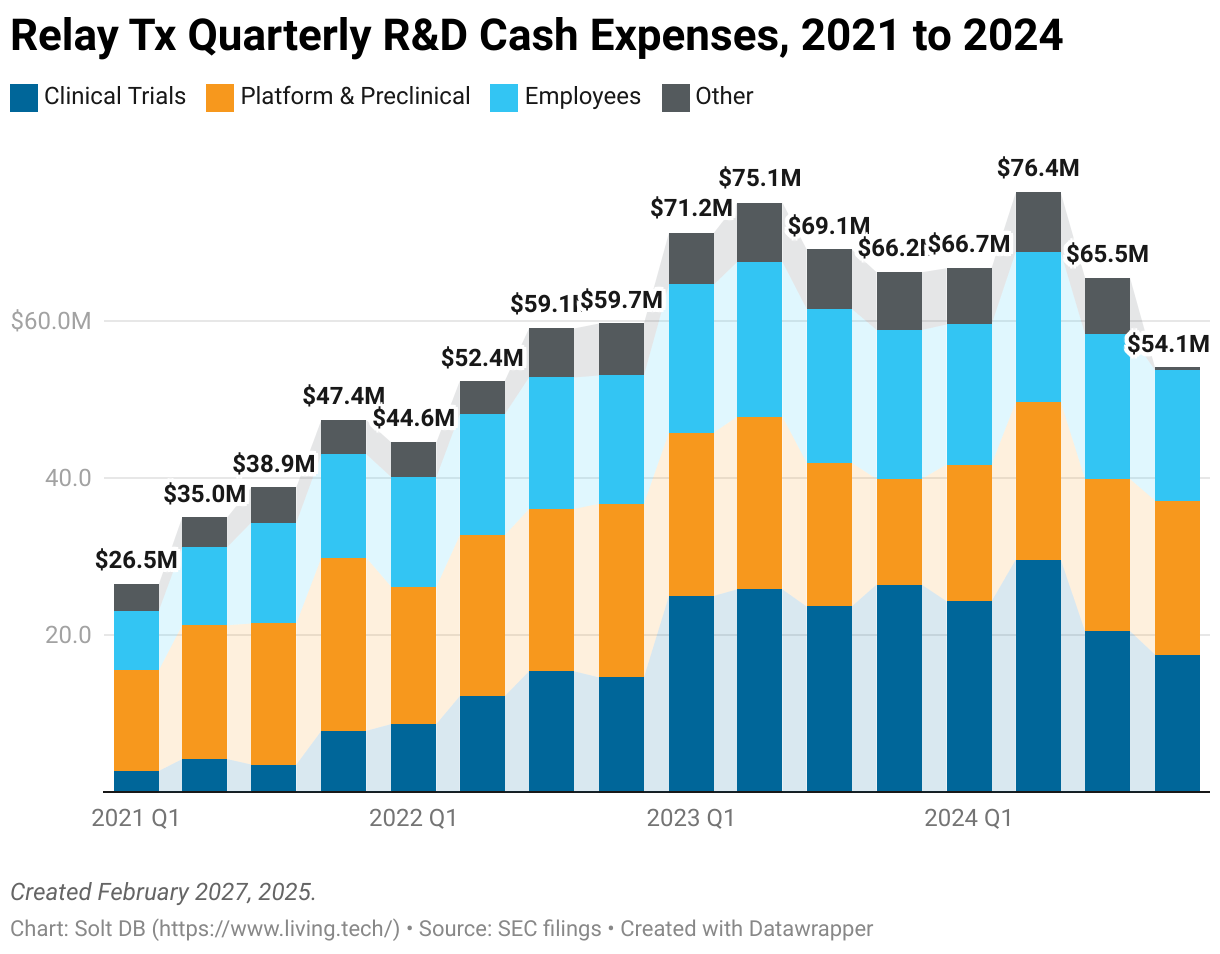

This can be illustrated by looking at companies that break down the components of R&D expenses. Here's the breakdown for Relay Therapeutics.

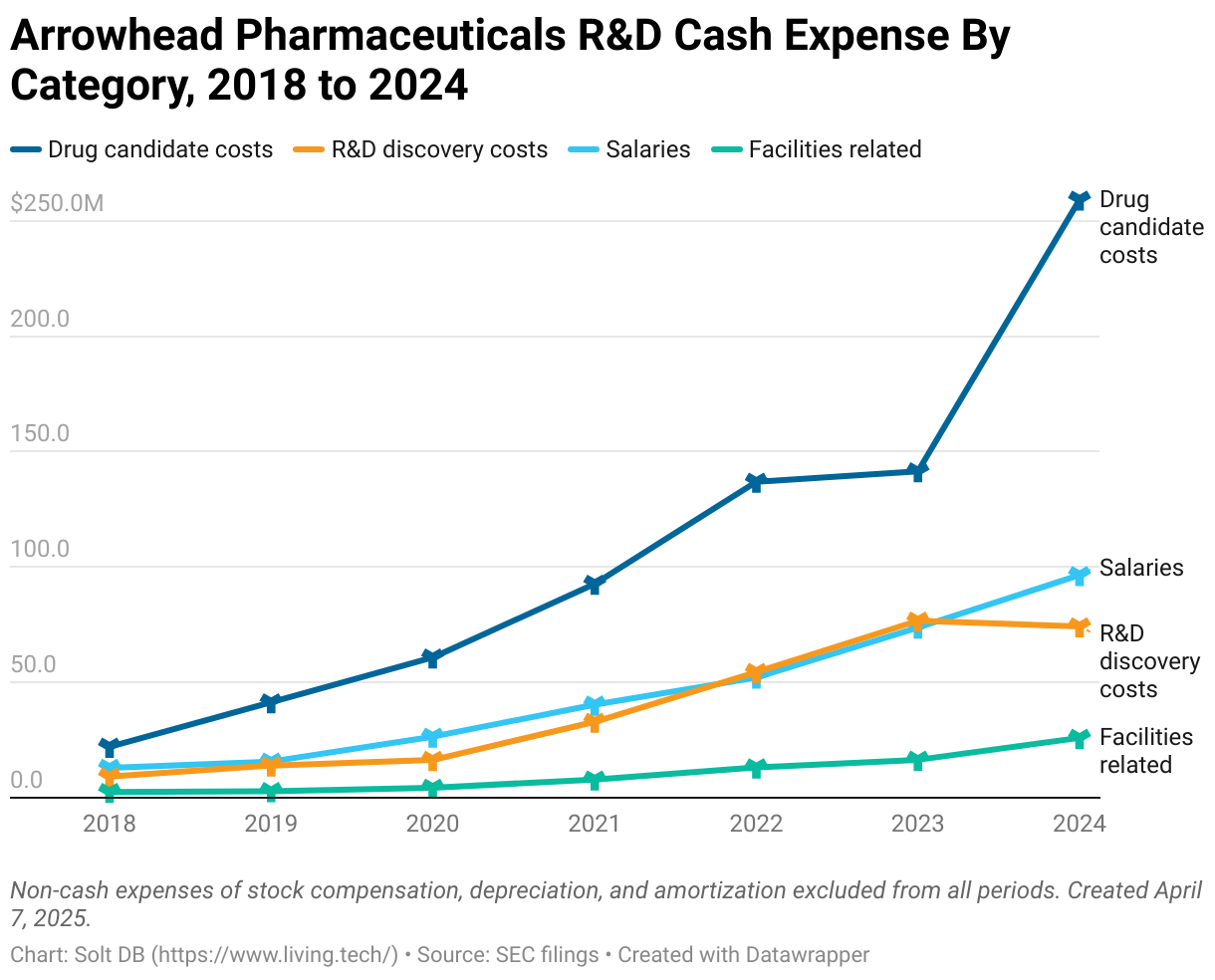

And here's the breakdown for Arrowhead Pharmaceuticals. The large increase was due to preparing assets for the Sarepta Therapeutics licensing deal in the last 24 months. That weird spike is because some expenses were recategorized in Q4 2024, again due to the licensing deal, but I haven't found a reconciliation to make a pretty chart.

Tariffs and commercial drug developers

Tariffs could impact the cost of some drug products in the coverage ecosystem. For example, SpringWorks Therapeutics manufactures a portion of Ogsiveo and Gomekli volumes in China. Day One Biopharma manufactures almost all Omjemda in China.

But if you haven't been living under a rock, then you know a little secret: drug products have big markups.

SpringWorks Therapeutics reported cost of goods sold of $12.6 million in 2024. That's all it took to generate $172 million in revenue, good for a gross margin of 93%. Day One Bio had a gross margin of 91% last year.

Tariffs get applied to the declared value of the drug substance that's imported, which is roughly the cost of goods sold. So, $12.6 million for SpringWorks and $5.3 million for Day One. If there were 100% tariffs, then these costs would've been $25.2 million and $10.6 million last year. Hardly catastrophic considering gross margin would dip to 85% and 81%, respectively.

Aside from increasing the cost of consumables used in specific R&D activities, tariffs won't have a meaningful impact on drug developers.

Tariffs and tools providers

Okay, well this group is kind of screwed.

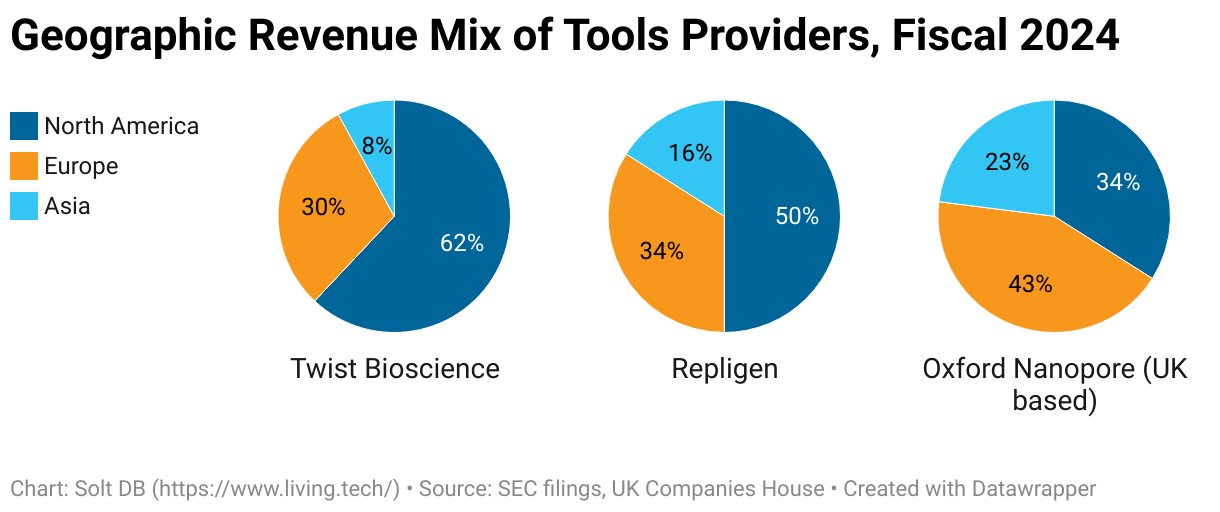

Companies that sell physical stuff across borders face tariff risks. For example, Twist Bioscience generates only 62% of revenue from the United States, with another 30% from Europe, Africa, and the Middle East and the remaining 8% from the Asia Pacific region. But it also generates 19% of revenue from academic customers, who face significant uncertainty due to funding cuts and political friction.

Repligen generates only 50% of revenue from North America – and that's an improvement from 43% in 2022. It leans on Europe for 34% of sales and Asia for another 16%.

Both Twist Bioscience and Repligen also import plastics and chemicals to manufacture their respective goods, so they'll see higher costs on top of needing to charge customers higher prices to absorb tariffs.

There are some bright spots, but investors might need to look at companies based outside of the United States. Oxford Nanopore is headquartered in the United Kingdom. It's not immune to tariffs, as it needs to import NVIDIA chips and other American components for some instruments. But it's well insulated against tariffs risks.

In 2024, the nanopore sequencing pioneer generated just 34% of revenue from the United States – a good thing for a U.K. company in the current moment. That means two-thirds of the company's revenue is essentially tariff free. Oxford Nanopore could also gain market share as customers shy away from tariff-saddled instruments from its competitors Illumina, PacBio, and Element Biosciences. Tariffs could also be great news for Swiss-based Roche, which recently unveiled a hybrid nanopore sequencing technology.

A Word on Market Volatility

Panic. Sell. Everything.

All right, kidding. Here are a few things to remember:

Keep it simple

The fundamentals of investing don't change whether markets are soaring, imploding, or moving sideways. The most important driver of investing performance is the price you pay. If you buy an asset for less than its worth, now or in the future, then you'll earn a positive return.

Markets were historically expensive before tariffs

The markets aren't crashing against a backdrop of completely rational valuations, steady growth, and equal capital distribution across global markets. They were historically expensive before April 2025.

The AI bubble reversed all progress made in 2022 injecting some sanity into market valuations. The United States fared the best among major economies in recent years, with lower inflation and better growth, due to significant government spending. It was a benefit, but it wasn't sustainable and masked other deficiencies lurking in the economy. Meanwhile, global capital was overwhelmingly weighted to U.S. stocks.

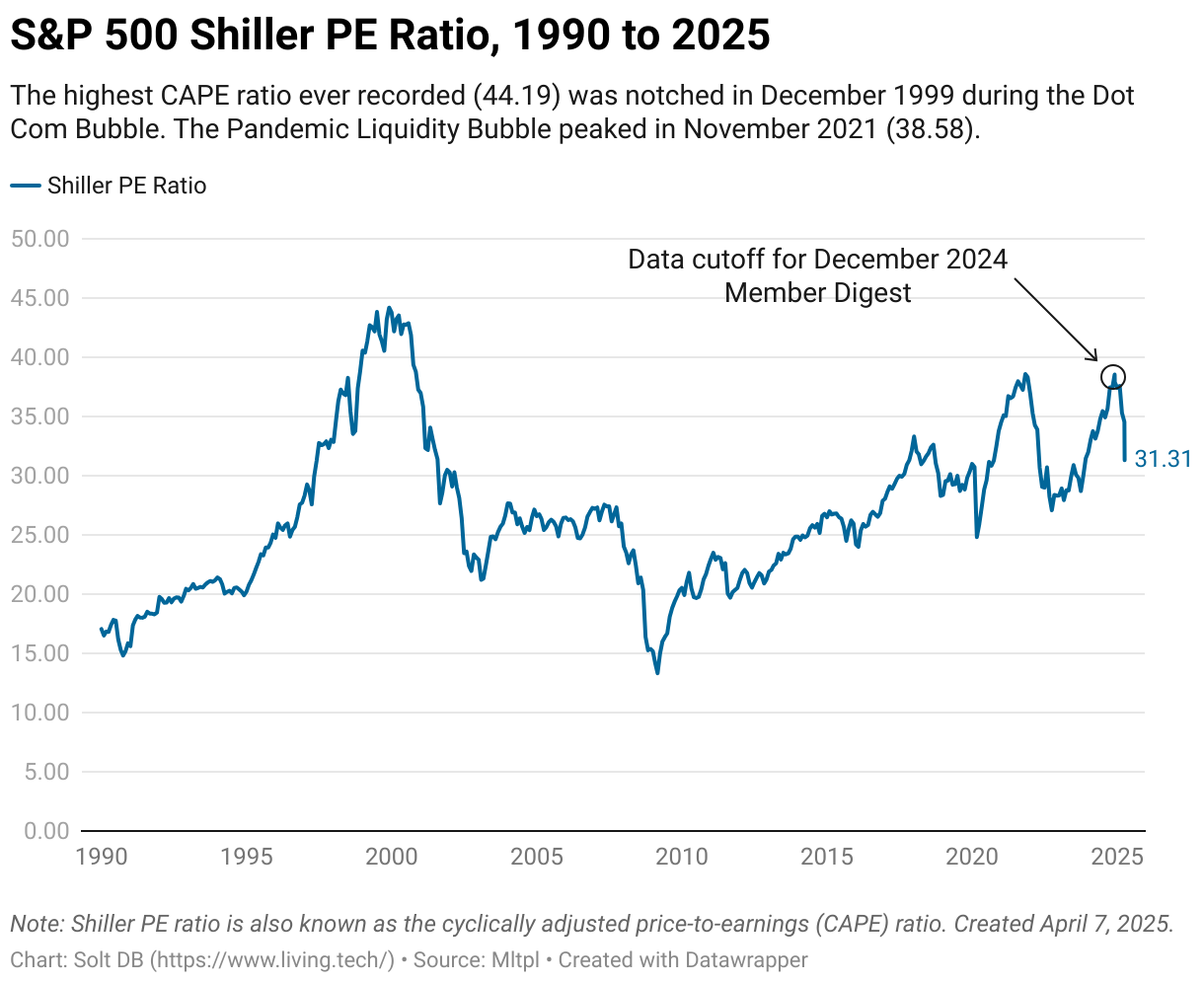

This was the topic of the last Member Digest in December 2024, titled "The Case for a Strategic Cash Position." Hopefully some members were in a position to build one. Coincidentally, the Shiller PE ratio peaked almost exactly to the day the last time I made this interactive data visualization. This metric has abruptly corrected.

Remember that the Shiller PE ratio is based on earnings, which means the current metric might be too generous. If tariffs and global trade disruptions ding the earnings of the S&P 500 by 10%, then the Shiller PE ratio right now would be 34.4. To return to more rational valuation metrics, the S&P 500 might need to drop to the low 4,000s or high 3,000s. That would mark another 20% to 30% decline from market close on Friday, April 4, 2025 (5,396).

A decline in stock market valuations was also predictable based on forward earnings.

The following graph from J.P. Morgan Asset Management has been widely shared; I plucked this from an Oaktree Capital memo published in January 2025. It plots the annualized 10-year returns against the forward PE ratio of the S&P 500 each month from 1988 to 2014 (10 years ago).

During the observation period, every time the index reached an excessive valuation annual returns settled between 2% to negative 2% for the next 10 years.

In other words, investors might expect the S&P 500 to close between 7,300 and 4,900 in January 2035.

Focus on the big picture

It's tempting to scour message boards for reasons this or that stock is plunging. Our monkey brains go to dark places when stocks are falling. We question the strategy, the management team, and why no one seems to be coming to the rescue.

This is normal, but it's not very helpful.

Things I'm not concerned about:

- Will the divestment of Udenyca fall apart?

- Will Relay Therapeutics become obsolete from technology developments in drug discovery?

- Is Arrowhead Pharmaceuticals going to run out of cash?

- Does the failure of vepdeg from Arvinas mean PROTAC degraders won't work?

Things I'm monitoring as an investor:

- Can Loqtorzi remain on a solid growth ramp in 2025? Will the data readouts in mid-2026 show casdozo and CHS-114 remain well positioned in the competitive landscape?

- Can Relay Therapeutics stick to its commitment to "sprint" to the finish line with the first pivotal study of RLY-2608? The first patient in (FPI) should occur in the next two months.

- Will Arrowhead demonstrate favorable results for the phase 2 data readout of ARO-RAGE in inflammatory lung diseases? Data are due in the next two months. Will obesity assets show solid initial progress with early readouts later this year?

- How quickly can Arvinas demonstrate progress for its wholly-owned programs targeting higher value, less competitive indications than vepdeg and HR+/HER2- breast cancer? That's why the company licensed it to Pfizer in the first place – and it snagged $1 billion in cash for doing so.

Drug developers are valued based on assets. There are a few more steps involved in converting molecules to dollars, which can then be tossed into more traditional financial models. But biotech investing is rather simple.

The problem is that the overwhelming amount of content and information you can find about biotech companies is noise. In reality, there are only a handful of meaningful de-risking events for a single asset across its 10-year development timeline. We can count those days on both hands. Considering there are 2,510 trading days every decade, that means you're adjusting your thesis 0.3% of the time, or maybe 1% of the time if you factor in developments from the competitive landscape. You must patiently sit there and do nothing the other 2,500 days.

Be careful buying the dip

Many investors are depressed because they learned stocks don't always go up. A modern-day Greek tragedy.

But what's happening now isn't going to be isolated to a couple days in April. This is one of those once-a-decade events where markets are forced to recalibrate. It happens. It's predictable. The show goes on… eventually.

There will be bounces and pops in the midst of the carnage. There always is. If you're buying companies at a great price, then have at it. But don't be surprised to see volatility in both directions after bounces and pops. Essentially, understand the gravity of the moment and set your expectations accordingly.

Recent De-Risking Events Roundup

Here's a review of de-risking events since the last Monthly Digest, recapped in alphabetical order:

- Arcus Biosciences raised $150 million from a public offering in February 2025. Gilead Sciences participated to bump its ownership stake to 35% -- the most it can swallow according to the collaboration agreement. Coverage will initiate this spring.

- Arrowhead Pharmaceuticals closed its licensing deal with Sarepta Therapeutics, which will see it earn $1.125 billion in cash by early 2026. That's a nice haul, especially given the high cost of capital.

- Arvinas imploded when vepdeg monotherapy failed its first pivotal study. It still has commercial potential and might perform better in certain combinations, but it appears intramuscular injection of a selective estrogen receptor degrader (SERD) like fulvestrant outperforms oral SERDs and oral PROTACs. Investors can expect vepdeg development to be terminated if Pfizer walks away. Coverage will initiate this spring.

- AVITA Medical recently launched Cohealyx, which could allow it to capture significantly more revenue from each procedure. The dermal matrix product can generate up to $20,000 per procedure, compared to $6,500 for ReCell alone. First, the company needs to collect data from an economic outcomes study now underway.

- Codexis signed up its first commercial customer for the ECO Synthesis platform, which manufactures RNAi drug products using enzymatic reactions. It was likely Alnylam Pharmaceuticals due to announcements from both companies, but the specific customer wasn't revealed.

- Exact Sciences launched Cologuard Plus. It will boost margins from a lower COGS and a higher selling price, but the effects will be felt between now and the end of 2026, rather than all at once.

- Guardant Health received advanced diagnostic laboratory test (ADLT) status for its Shield test in colon cancer screening. The designation limits how much Medicare prices can fall in the near term, which is favorable considering the test sells for $1,495 – 7x more than the predicted value provided. The downside is that the company might need to repay the difference if the real-world value is found to be sharply lower in the future, which seems likely in this case. Coverage will initiate this spring.

- Relay Therapeutics laid off another 25% of its workforce in early April. The move might save $42 million in the next three years total, which might be reallocated to the phase 1 clinical trial of a new program, or simply to cushion the development of RLY-2608.

- SpringWorks Therapeutics received a best-case approval for Gomekli in February, which was greenlighted for both pediatric and adult patients. Although the stock leapt higher after investors learned Merck was considering an acquisition, most of those gains have evaporated. Coverage will initiate this spring.

Upcoming De-Risking Events Roundup

Here's a preview of de-risking to keep an eye on, in order of nearest to furthest:

- Arrowhead Pharmaceuticals should announce phase 2 data from ARO-RAGE in the next few months. This is an increasingly important asset for the business.

- Relay Therapeutics should enroll the first patient into the first pivotal study of RLY-2608 by mid-2025. A topline data readout would be expected by summer 2028, although the study design suggests the trial could be stopped early if patients receiving the drug candidate have sharply improved progression-free survival than Truqap.

- Verve Therapeutics should announce early phase 1 dose escalation data for VERVE-102 during Q2. However, the highest-dose cohorts will be the most important, but will not be included in the upcoming data readout.

Finch Trades Review

Finch Trades are how I share my real-world investing transactions in real time with members.

- Each transaction confirmation is shared on Discord as soon as the transaction closes, so I cannot cherry-pick my track record. Follow-up research notes are published soon after.

- The all-time returns of Finch Trades will be reported vs. what would've happened if I invested in the S&P 500 instead. I want to demonstrate biotech investing can outperform a passive investing approach.

As of market close on Friday, April 4, 2025, Finch Trades are underperforming the S&P 500 by 44%.

Finch Trades has deployed $32,971 of capital since initiation in April 2024. That principal has declined 54% to $15,206 in that span. It would've decreased 10% to $29,796 if I invested in the S&P 500 instead.

As poor as it looks, the comparison is impacted by the heavy concentration in Coherus BioSciences (28% of Finch Trades capital) and Relay Therapeutics (60%), which combine for 88% of total invested capital so far. I expect to greatly increase my position in Relay Therapeutics through the first topline pivotal data readout for RLY-2608 expected in mid-2028.

Concentration exposes a portfolio to significant volatility, but it works both ways. Let's consider scenarios where all company valuations remain the same as of market close Friday, April 4, but one or both of the top allocations become more fairly valued.

- Only Coherus: If Coherus BioSciences was valued at $407 million ($3.51 per share), then Finch Trades would be outperforming the market. My cost basis is $1.72 per share.

- Only Relay: If Relay Therapeutics was valued at $562 million ($3.27 per share), then Finch Trades would be outperforming the market. My cost basis is $4.84 per share.

- A mix of both: If Coherus BioSciences was valued at $200 million ($1.72 per share) and Relay Therapeutics was valued at $487 million ($2.83 per share), then Finch Trades would be outperforming the market.

Concentration also creates the opportunity for significant outperformance – if you're right.

Consider a conservative scenario into summer 2030. Relay Therapeutics keeps executing, all other Finch Trades stocks trade flat, and the S&P 500 delivers 10% annual gains.

- The S&P 500 would sit at a level of 8,133. That's 61% higher than today.

- If Relay Therapeutics launches RLY-2608 in the second half of 2029, then 2030 would be the asset's first full year on the market.

- If it can match the performance of Truqap, then it would have first-year revenue of at least $400 million. That level of commercial execution would result in a fair valuation of at least $5 billion with no contributions from any other asset.

- If the business uses a combination of a massive public stock offering and a large non-dilutive debt offering to prepare for its looming commercial transition, then it would have roughly 215 million shares outstanding. That would result in a fair valuation of roughly $23.50 per share.

In the above scenario, Finch Trades made from inception through this Member Digest would have a total return of 212% vs. 45% for the S&P 500. That would be an outperformance of 167%.

That's equivalent to an annual return of 25.6% for five years. It would normally require 12 years of passive investing, earning an average annual return of 10%, to achieve the same performance.

This would require the S&P 500 to buck historic trends that predict a negative total return through 2034, global markets to ignore the end of 80 years of American economic hegemony, the U.S. credit rating to remain the same in the face of widening deficits, me to not make any additional Finch Trades (which have the potential to greatly increase overall performance), and for me to really suck at my job otherwise.

I like my odds.

Finch Trades Goal for Relay Therapeutics

Due to the opportunity outlined above, my goal is to purchase 20,000 shares of Relay Therapeutics in Finch Trades. That's twice the previously communicated goal. The recent market plunge makes that more realistic for less capital. Members can expect me to begin deploying my strategic cash position in April or May.

Personal Update

I was laid off at my day job. Carnegie Mellon University and Emerald Cloud Lab (my employer) collaborated on the CMU Cloud Lab, but the university decided to terminate the contract two years early. My last day is this Friday, April 11.

Bummer. But I really hated my two-hour daily commute, my boss was a dick, I served two roles since November with no consistent schedule, and I was burning out from all of it.

This spring and summer I'll be refocusing on Solt DB and studying for CFA exam. My goal is to introduce coverage of all ecosystem companies, relaunch the Solt DB Biotech Company Database, and have more consistent free content.

For my next day job adventure, my network has overwhelmingly encouraged me to deploy my unique understanding of living technology to help companies develop market strategies. Loud and clear. I'll be consulting a couple startups.

That includes a new contract development and manufacturing organization (CDMO) in the Bay Area focused on biologics. It was founded by an engineer who scaled-up the manufacturing processes for Udenyca from Coherus BioSciences, Daxxify from Revance Therapeutics, and several others. There's a solid opportunity to serve smaller and mid-tier drug developers, especially with many scrambling to onshore scale-up and quality control work. If we execute in the next few months, then I could have the opportunity for a new (fully remote) day job that actually leverages my skillset and network. And no more two-hour daily commute.

.svg)

.png)

-cropped.svg)