.svg)

I was revisiting my research for casdozokitug ahead of this year's ASCO GI conference, which begins on January 23. I'll have to update my model either way.

Coherus BioSciences is set to present full data for a triplet that adds casdozo (an IL-27 inhibitor) to the standard of care doublet in first-line (1L) advanced hepatocellular carcinoma (HCC). Although this common liver cancer represents a sizable market opportunity, it's also very competitive. The standard of care – a combination of Roche's Tecentriq (atezolizumab) and Avastin (bevacizumab) – works relatively well. Doctors and scientists simply think it's possible to improve an objective response rate of 27% to 30% and a median progression free survival (mPFS) of 6.8 months.

I don't have high hopes for casdozo. Or I didn't.

Casdozo is the only clinical-stage IL-27 inhibitor globally, which usually isn't a good thing. However, upon revisiting my research, there's a clear correlation between elevated IL-27 levels and HCC progression. Perhaps being the lone drug candidate in the class isn't such a bad thing in this indication.

Investors also had preliminary data from the phase 2 study showing favorable responses (ORR of 38%) and duration of responses (mPFS of 8.1 months), which was reported in January 2024.

The Trade

Coherus BioSciences is considered a Growth (Speculative) position. I purchased 729.93 shares at $1.37 per share on January 21, 2025.

What Did the Data Say?

The abstract was published after market close on Tuesday, January 21, 2025.

Although the data did not include "full data" per se, they did show a slight improvement from the year-ago update. Adding casdozo to the triplet still showed an ORR of 38% and an mPFS of 8.1 months (in the same number of patients as the year-ago patients). But more patients converted from a partial response to a complete response.

The ORR is the rate of patients who have a partial response (a tumor reduction of at least 30%) or a complete response (a tumor reduction of 100%).

- At the time of the January 2024 data update, Coherus reported 3 patients with a complete response and 8 patients with a partial response. The ORR was 38% (11/29).

- At the time of the January 2025 data update, Coherus reported 5 patients with a complete response and 6 patients with a partial response. The ORR remained 38% (11/29).

This is promising. The standard of care had a complete response rate of 5.5% (18/327) in its pivotal study. Adding casdozo increased that to 17.2% (5/29) -- a meaningful difference, albeit with a small number of patients.

The plan going forward is to conduct a brand new phase 2 study evaluating casdozo plus toripalimab and bevacizumab. Both atezolizumab and toripalimab inhibit PD-1, so Coherus is simply swapping an external asset for one of its own.

In a phase 3 study from Junshi Biosciences, a combination of toripalimab and bevacizumab delivered an ORR of 32.7% and an mPFS of 9.9 months. That compares favorably to the standard of care, which had an ORR of 27% to 30% and an mPFS of 6.8 months. If the addition of casdozo adds a boost, then Coherus will be well positioned within the competitive landscape.

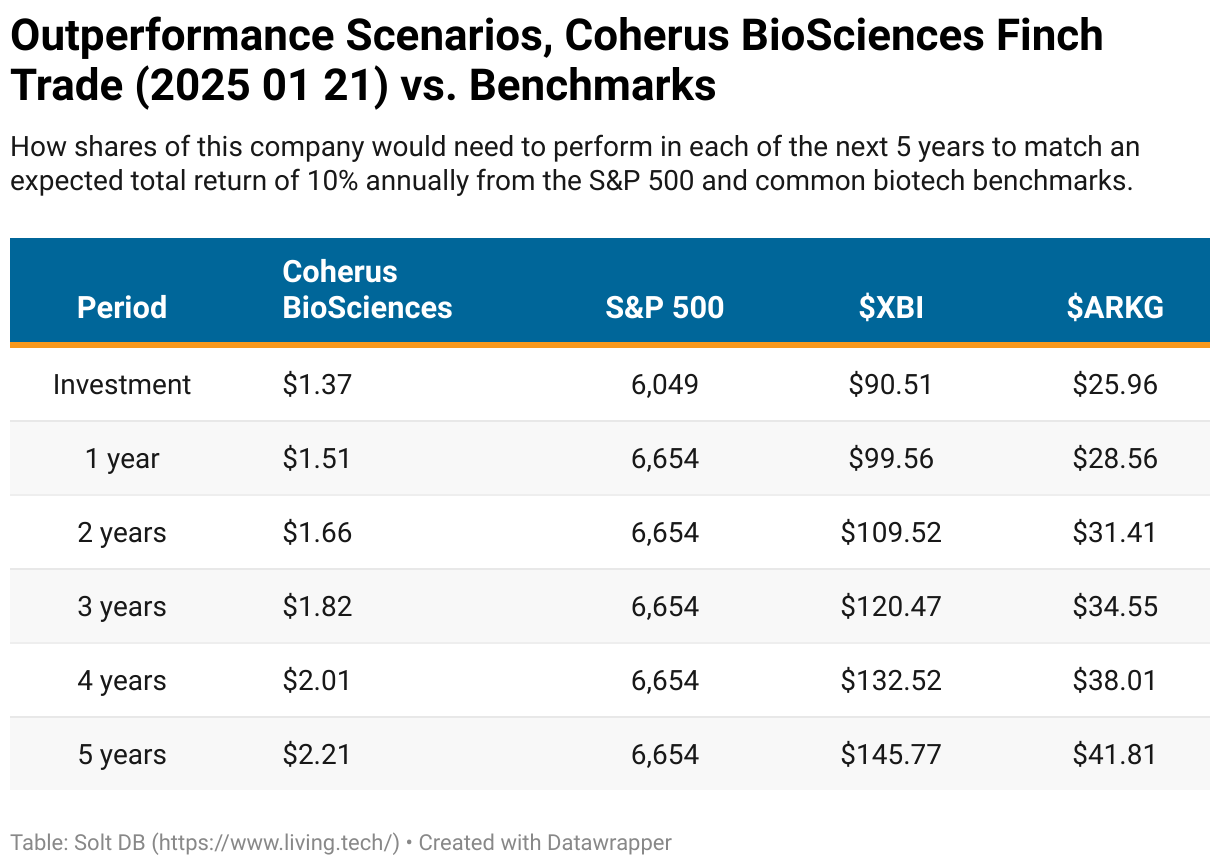

Outperformance Scenarios

Investing in individual stocks can be reduced to a simple question: "If I invest $1 in this individual stock at this price, will it outperform an equal passive investment in the S&P 500 at this level?"

If you keep emotions and expectations in check, then you might be surprised to learn you don't need to swing for the fences.

Here's how shares of Coherus BioSciences will need to perform for the money invested in this Finch Trade to outperform passive investing in the S&P 500 in the next five years.

Assumptions:

- The S&P 500 index gains 10% per year with dividends included – its historical average since 1990.

- Coherus BioSciences averages 14.2% dilution per year in the next five years – equivalent to a standard 17.5% dilutive event every 18 months. This is the historical average for precommercial and newly commercial drug developers.

- S&P 500 closing level on January 21, 2025 = 6,049

- Coherus BioSciences closing price on January 21, 2025 = $1.37 per share

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Speculative) position. The current modeled fair valuation for the company based on my 2025 model is below:

- Market close January 21: $1.32 per share

- Modeled Fair Valuation: $2.51 per share

- Allocation Range: Up to 10%

Coherus BioSciences reported 115.213 million shares outstanding as of October 31, 2024. The modeled fair valuation above assumes 120.974 million shares outstanding, which is equivalent to 5% dilution.

Further Reading

- January 2025 press release announcing the data readout to be presented at ASCO GI

- January 2024 press release announcing the preliminary data readout of the same phase 2 study

- May 2020 study results from the pivotal trial of the standard of care in 1L advanced HCC

.png)

-cropped.svg)