.svg)

Want an email alert every time a Finch Trade goes live? Sign up in your profile.

As distressed debt investor Howard Marks says, successful investing isn't about buying good things. It's about buying things well.

If you overpay for the best business in the world, then you might lose your shirt. Same for an overpriced building in the best part of town, or an uncompetitive degree from a top-ranked university. Conversely, it's possible to buy a steaming hot pile of garbage – whether stocks, real estate, or debt from companies on the skids – and generate solid returns. That's because the single-most important factor that determines investing returns in the price you pay.

I don't think Coherus BioSciences is the best business in the world, nor is it a steaming hot pile of garbage. But it should be valued significantly higher than $100 million, which is the exact level represented by this Finch Trade limit order at $0.86 per share. I took a nibble with the spare cash sitting in my HSA.

I have now purchased 5,363 shares of Coherus BioSciences in Finch Trades at a cost basis of $1.72 per share. That means my position will reach breakeven at a valuation of $199 million (using the current 116 million shares outstanding), or $249 million on a fully-diluted basis. Loqtorzi alone should contribute more than that to the valuation. If pipeline data readouts are favorable in the first half of 2026, then the business should earn a valuation between $500 million and $1 billion.

The Trade

Coherus BioSciences is considered a Growth (Speculative) position. I purchased 291 shares at $0.86 per share on March 27, 2025.

Scenario Analysis

My modeling is based on valuing assets, contextualizing competitive landscape dynamics, and weighing the probabilities of favorable and unfavorable scenarios. This trade was driven by the following considerations.

Loqtorzi de-risks pipeline development

Although the initial approval in nasopharyngeal carcinoma (NPC) isn't a large enough opportunity to fund the business in its entirety, Loqtorzi will de-risk pipeline development as it ramps.

When the asset reaches peak annual sales of roughly $150 million it should be generating at least $105 million in cash flow per year. The business might have total annual operating expenses of roughly $250 million to $300 million in the next few years, so Loqtorzi can offset a meaningful amount of cash burn.

Casdozo could be in pivotal studies by 2027

Coherus has two primary focuses between now and mid-2026: focus on commercial execution (its strength) for Loqtorzi and ensure clinical programs remain on track for timely data readouts.

The lead drug candidate, casdozo, demonstrated promising phase 2 data in advanced hepatocellular carcinoma (HCC) when added to the standard of care. The preferred first-line treatment of the liver cancer is a doublet comprising PD-1 inhibitor Tecentriq (atezolizumab) and VEGF inhibitor Avastin (bevacizumab). The proposed triplet combination with casdozo showed early signs of improvement:

- Objective response rate (ORR): 38% for the triplet vs. 28% for the standard of care

- Modified ORR: There's an adjusted ORR calculation for HCC specifically. The triplet notched an mORR of 43% vs. 33% for the standard of care.

- Complete response (CR) rate: 17% for the triplet vs. 5.5% for the standard of care

Coherus is now conducting a second phase 2 study that swaps in its own PD-1 inhibitor Loqtorzi to create a new triplet with casdozo and Avastin. The study is designed to evaluate 72 patients spread evenly across three cohorts:

- Cohort A will evaluate the triplet with a lower dose of casdozo

- Cohort B will evaluate the triplet with a higher dose of casdozo

- Cohort C will evaluate Loqtorzi plus Avastin to provide a baseline performance for the "standard of care" without any contribution from casdozo.

The phase 2 data readout is expected in the first half of 2026. The results will inform a final "go/no-go" decision on a pivotal study that could begin in early 2027. That should unlock meaningful value for shareholders and position the business for an acquisition.

The potential arrival of CCR8

In addition to casdozo, data readouts from the competitive landscape in the next few months promise to launch CCR8 onto the scene as a valuable target in combination with PD-1 inhibitors.

Coherus finds itself in an unusually de-risked position ahead of the first meaningful data readout.

LaNova Medicines evaluated its own CCR8 antibody, LM-108, with Loqtorzi in second-line gastric cancer. It shared promising results at the annual ASCO meeting in June 2024:

- ORR: 36% including first-line patients (n = 36)

- ORR: 63% in only second-line patients (n = 11)

- ORR: 87.5% in second-line patients with high CCR8 expression (n = 8)

This is marvelous. It's a rare insight into the potential combination of Loqtorzi with a CCR8 inhibitor, especially since the company hasn't yet evaluated its own combination. That'll change soon.

Coherus has designed multiple phase 1 studies to evaluate CHS-114 with Loqtorzi. One will look at second-line gastric cancer, while the other will observe patients with head and neck squamous cell carcinoma (HNSCC). Both cancers are known to have high levels of CCR8 in the tumor microenvironment, which makes them the obvious place to start for CCR8 development.

The company expects both data readouts to occur in the first half of 2026. As phase 1 studies, they're designed to demonstrate safety and tolerability endpoints, but investors will get an early look at efficacy endpoints like ORR too.

Investors might not have to wait that long. Data readouts from the competitive landscape in 2025 could drum up excitement for Coherus' asset, especially since it's one of four drug developers armed with both a PD-1 inhibitor and CCR8 inhibitor. The other three? Roche, Bristol Myers Squibb, and BeiGene (BeOne Medicines).

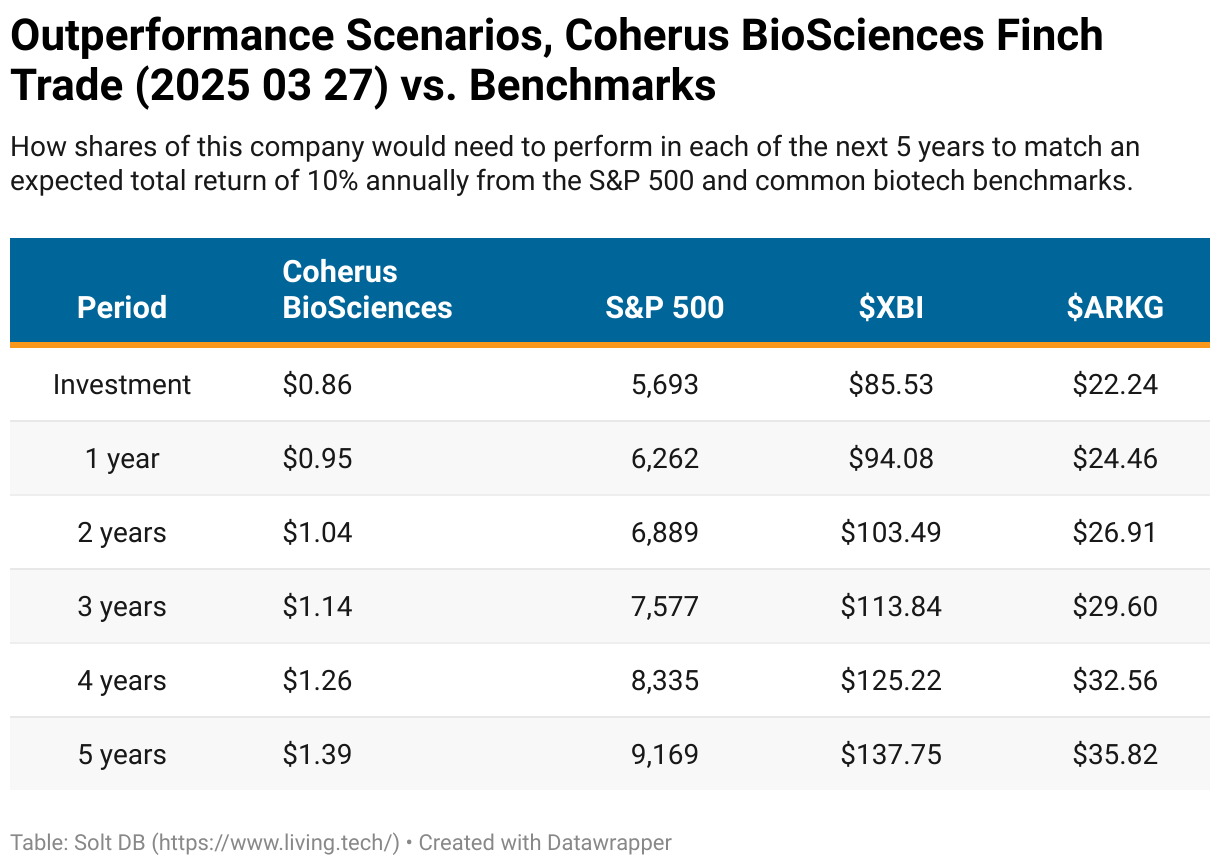

Outperformance Scenarios

Investing in individual stocks can be reduced to a simple question: "If I invest $1 in this individual stock at this price, will it outperform an equal passive investment in the S&P 500 at this level?"

If you keep emotions and expectations in check, then you might be surprised to learn you don't need to swing for the fences.

Here's how shares of Coherus BioSciences will need to perform for the money invested in this Finch Trade to outperform passive investing in the S&P 500 in the next five years.

Assumptions:

- The S&P 500 index gains 10% per year with dividends included – its historical average since 1990.

- Coherus BioSciences averages 14.2% dilution per year in the next five years – equivalent to a standard 17.5% dilutive event every 18 months. This is the historical average for precommercial and newly commercial drug developers.

- S&P 500 closing level on March 27, 2025 = 5,693

- Coherus BioSciences closing price on March 27, 2025 = $0.86 per share

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Speculative) position. The current modeled fair valuation based on my 2025 model is below:

- Market close March 31: $0.81 per share

- Modeled Fair Valuation: $2.78 per share

- Allocation Range: Up to 10%

Coherus BioSciences reported 115.896 million shares outstanding as of February 28, 2025. The modeled fair valuation above assumes 121.692 million shares outstanding, which is equivalent to 5% dilution.

Further Reading

- January 2025 press release announcing final phase 2 data for a triplet with casdozo in 1L HCC

- October 2024 research note explaining the therapeutic rationale for inhibiting CCR8 in the tumor microenvironment

.png)

-cropped.svg)