.svg)

Fresh off a licensing deal for NDA-ready lirafugratinib, there are subtle hints Relay Therapeutics isn't done monetizing its R&D engine. Maybe the hints aren't so subtle if investors look at 2025 guidance.

The precision medicine company expects:

- three (3) new development candidates to be unveiled

- three (3) new investigational new drug (IND) applications to be filed

- three (3) new clinical starts in 2025

The math implies the remaining breast cancer assets, specifically RLY-2139 (CDK2 inhibitor) and RLY-1013 (estrogen receptor degrader), are excluded from these projections.

Management has explicitly discussed the goal to initiate clinical trials for the vascular malformations, NRAS inhibitor, and Fabry disease programs in 2025. None of these have IND filings yet, which is required to begin a clinical trial. Although the vascular malformations program will begin with RLY-2608, it still requires an indication-specific IND. That means IND and clinical start guidance refers to these three programs.

Nor can RLY-2139 and RLY-1013 represent two of the three new development candidates in projections, as they themselves are development candidates. No matter how you toss around your abacus, the remaining breast cancer assets are clearly excluded from guidance.

This is awkward. Both assets are further in development than the three new programs set to enter the clinic next year. Both are presumably important for combinations with the company's prized asset, the pan-mutant PI3K-alpha inhibitor RLY-2608, in HR+/HER2- breast cancer. Both will need to complete initial clinical trials before being studied in RLY-2608 combinations.

Why are these assets deemed lower priority given the company's overall focus on and prioritization of breast cancer?

A few possible scenarios:

- Scenario A: Relay Therapeutics will never push these assets into clinical trials. That seems a little improbable considering RLY-1013 was taken off the shelf after a long pause and is actively completing IND-enabling studies.

- Scenario B: Relay Therapeutics is advancing multiple new programs to clinical trials because it intends to monetize at least one of them, which would provide more resources and bandwidth to focus on RLY-2139 and RLY-1013. The NRAS inhibitor or Fabry disease program makes the most sense if the goal is to go all-in on breast cancer.

- Scenario C: Relay Therapeutics is positioning its entire breast cancer pipeline -- RLY-2608, RLY-2139, and RLY-1013 -- for a partnership. Such a transaction would be worth a significant upfront payment and meaningful economics for the life of the assets, potentially including a 50/50 split of costs and profits.

Bottom-Up Signals Suggest a Breast Cancer Partnership Makes Sense

Assuming RLY-2608 continues development, finding a blue-chip partner to ease the financial burden of development and (especially) commercialization efforts of the overall breast cancer portfolio seems like a plausible path forward.

A few bottom-up signals raise eyebrows.

Historical industry data

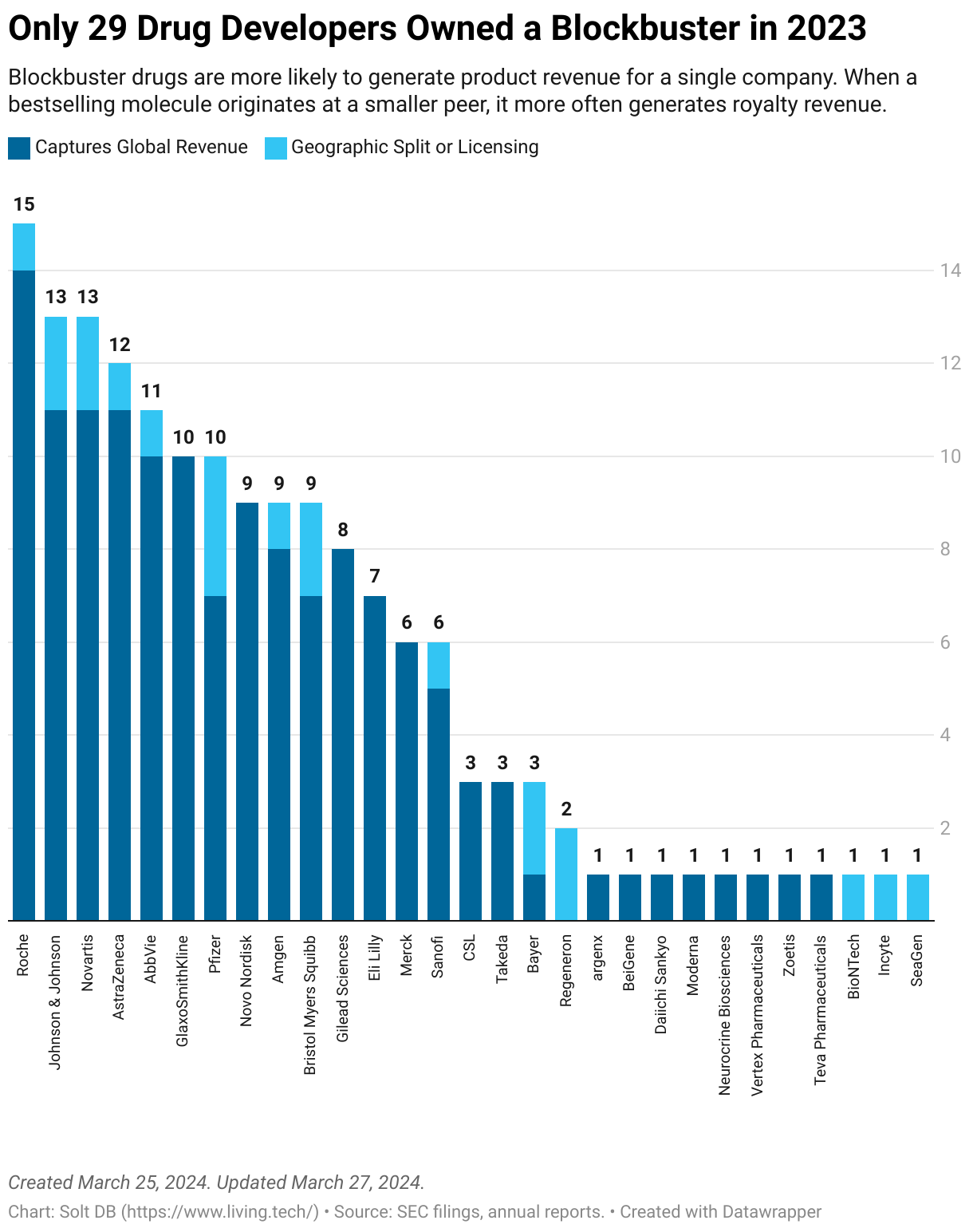

In March 2024, I compiled the first complete dataset of global blockbuster drugs, which uncovered many granular insights and patterns. One of the most relevant here: Many precommercial drug developers lucky enough to join the blockbuster club do so through partnerships. This has been true for both oncology newcomers to make the list in recent years, Incyte and SeaGen.

Although investors drool over the blockbuster potential of promising drug candidates, such outcomes are only realized through significant investments of time and money. It's fun to dream of 10-digit revenue figures, especially for a pre-revenue business. It's easy to forget the part about spending over a decade and 10-digit expense figures to seize the opportunity, which is virtually impossible to pull off for a pre-revenue business.

Sum of the parts for "yet another" SERD

It's curious that Relay Therapeutics took RLY-1013 off the shelf to get it ready for an IND filing, only to exclude it from 2025 guidance. Development of both RLY-2139 and RLY-1013 were paused in November 2023 when the company refocused R&D efforts to extend its cash runway by one year. The CDK2 inhibitor was already IND-ready.

Competitive dynamics make the decision more curious. It will be difficult for yet another selective estrogen receptor degrader (SERD) to stand out in a very crowded late-stage landscape. Roche, Eli Lilly, Pfizer (Arvinas), and others are all eyeing the opportunity for oral SERDs to disrupt the standard of care endocrine therapy Faslodex (fulvestrant), which is administered via inconvenient intramuscular injections.

Oral SERDs will be important pieces of next-generation combinations for HR+/HER2- breast cancer. Future first-line (1L) and second-line (2L) treatments are likely to include combinations mixing and matching SERDs, CDK inhibitors, and PI3K-alpha inhibitors. The total current U.S. market opportunity for 1L and 2L combinations exceeds $7 billion, while future approvals could grow it to over $10 billion.

My blunt assessment is RLY-1013 only has value within a wholly-owned treatment stack, otherwise the brutal competitive landscape suggests it shouldn't progress into clinical trials at all.

CDK2 inhibitors emerge as must-have assets

The sum-of-the-parts argument applies to RLY-2139, too, although a CDK2 inhibitor is potentially more valuable than an oral SERD. The emerging class of molecules promises to address tumor resistance to existing CDK4/6 inhibitors. That's a lucrative hypothesis considering CDK4/6 brands Ibrance, Verzenio, and Kisqali had global full-year 2023 revenue of $4.753 billion (global rank: 28), $3.863 billion (global rank: 42), and $2.080 billion (global rank: 77), respectively.

In September 2024, Roche handed $850 million in cash to Regor Therapeutics for rights to two next-generation CDK inhibitors, headlined by the CDK2 asset RGT-419B.

Pfizer stands alone among large pharmaceutical companies developing a CDK2 inhibitor in-house, but a slew of smaller companies including Incyte, Blueprint Medicines, Ensem Therapeutics, Cedilla Therapeutics, Incyclix Bio, and others are actively developing assets.

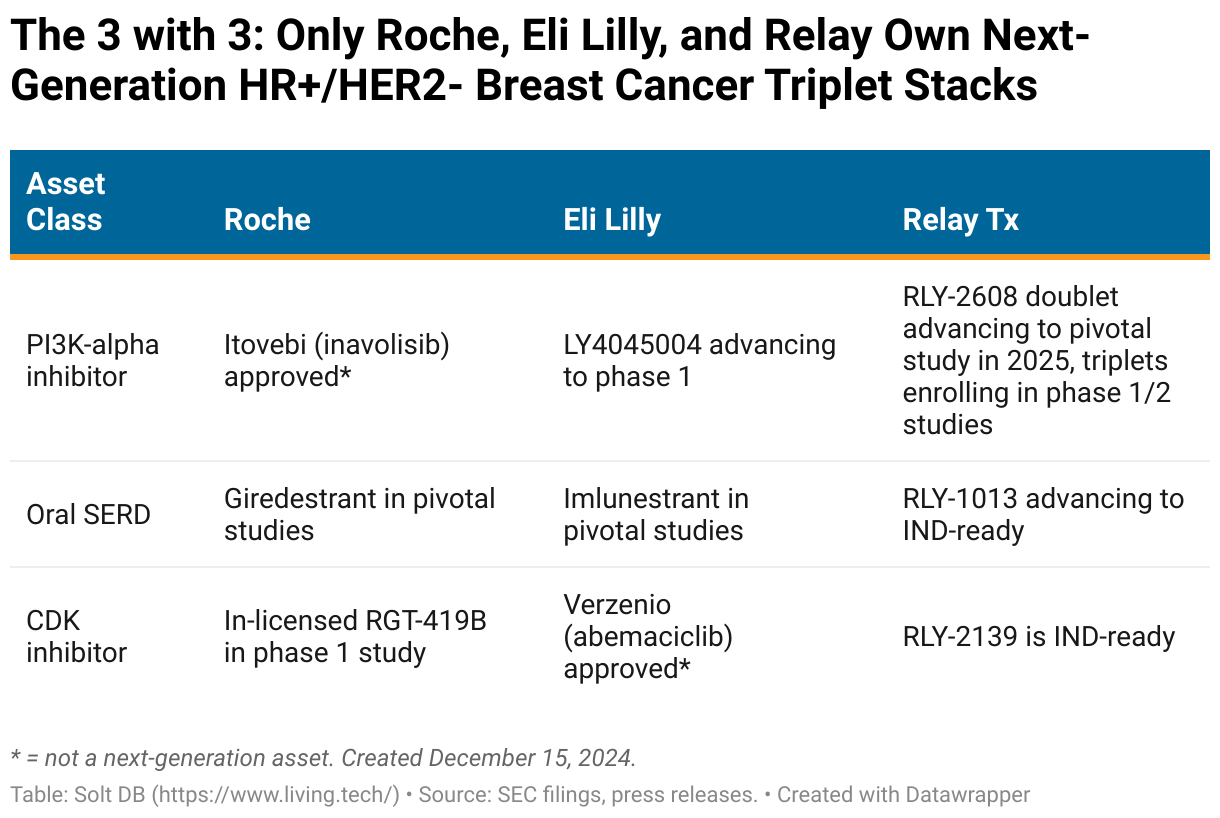

A full stack opportunity for a global partner

Although large pharma companies are beginning to plant flags in the landscape of next-generation HR+/HER2- breast cancer combinations, only Roche and Eli Lilly wield two of the three components. Relay Therapeutics is the only company that owns full rights to a pan-mutant PI3K-alpha inhibitor, oral SERD, and CDK2 inhibitor.

Roche wields the PI3K-alpha inhibitor Itovebi (inavolisib), the oral SERD candidate giredestrant, and in-licensed the CDK2 inhibitor asset RGT-419B in September 2024.

The Swiss pharma giant secured U.S. Food and Drug Administration (FDA) approval for its PI3K-alpha inhibitor Itovebi (inavolisib) in November 2024 as part of a 1L triplet combination with current-generation SERD and CDK4/6 drug products. Management projects peak annual sales of $2.3 billion. The asset isn't technically a pan-mutant selective PI3K-alpha inhibitor, but it has a favorable tolerability profile aside from the prevalence of grade 3 hyperglycemia. Next-generation assets such as RLY-2608 or Scorpion Therapeutics' STX-478 appear to have an advantage in efficacy and avoiding severe hyperglycemia.

Eli Lilly recently terminated the development of LOXO-783, which belonged to a subclass of kinase-specific PI3K-alpha inhibitors. It's now focusing on a pan-mutant PI3K-alpha inhibitor candidate LY4045004.

The world's most valuable drug developer unveiled promising data for its late-stage oral SERD imlunestrant at the San Antonio Breast Cancer Symposium (SABCS) in mid-December 2024. It appears to lead the landscape. Meanwhile, Eli Lilly owns the current-generation CDK4/6 asset Verzenio (abemaciclib), which generated $3.863 billion in global revenue in 2023.

Relay Therapeutics is led by RLY-2608, the most-advanced pan-mutant PI3K-alpha asset globally. The company expects to initiate a pivotal study of the doublet with fulvestrant in 2025. The goal is to go head-to-head against the current standard of care in the 2L setting, Truqap (capivasertib) plus fulvestrant. The asset is on pace to generate full-year 2024 revenue of over $350 million for AstraZeneca – not bad for its first full year on the market.

Meanwhile, RLY-2608 triplet combinations taking aim at 1L treatment settings are currently being explored in clinical trials. Relay Therapeutics is exploring combinations with current-generation CDK4/6 inhibitors Kisqali and Ibrance, as well as a combination with next-generation CDK4 inhibitor candidate atirmociclib. The latter represents the first time Pfizer's prized CDK asset has been explored in a triplet combination.

A Breast Cancer Partnership Would Cement Relay's Top-Tier Status

Wall Street isn't properly valuing development-stage molecules right now. Large pharma companies haven't been so shy. They speak the language of molecules, after all.

A global partnership for Relay Therapeutics' breast cancer pipeline could fetch a significant upfront milestone payment ($500 million to $1 billion) while retaining meaningful economics. For example, splitting expenses and profits 50/50 would significantly reduce the company's financial burden.

Lower expenses and doubling the cash runway through the rest of the decade would free resources for more diverse bets better tuned to today's viscous capital markets, which show no signs of loosening anytime soon. The vascular malformations program is positioned to quickly generate clinical proof-of-concept (it will begin with RLY-2608) before advancing to pivotal studies (with a new molecule optimized for chronic treatment). It targets a large and mostly unaddressed chronic treatment population across four distinct types of overgrowth malformations.

Similarly, the Fabry disease program could quickly differentiate itself from the market-leading product Galafold (migalastat). Clinical trials would be far smaller than those for breast cancer, although they may require more time for observation depending on regulatory feedback.

Meanwhile, the world's first NRAS-selective inhibitor represents an attractive development opportunity – larger than lirafugratinib, smaller than RLY-2608, but potentially easily differentiated. It's right-sized for both viscous capital markets and to be the first wholly-owned oncology asset brought to market by Relay Therapeutics.

Investors aren't expecting RLY-2608 to be partnered off, but the company's 2025 guidance and recent pipeline activities, as well as deals within the competitive landscape, could suggest a breast cancer partnership is on the horizon.

Margin of Safety & Allocation

Relay Therapeutics is considered a Growth (Quality) position. The current modeled fair valuation for the company based on my 2024 model is below:

- Market close December 13: $4.71 per share

- Modeled Fair Valuation: $15.65 per share

- Allocation Range: Up to 15%

Relay Therapeutics reported 167.383 million shares outstanding as of November 1, 2024. The modeled fair valuation above assumes 175.752 million shares outstanding, which is equivalent to 5% dilution.

Further Reading

- December 2024 press release announcing updated phase 1/2 data for RLY-2608 plus fulvestrant at SABCS

- September 2024 research note analyzing the phase 1/2 data for RLY-2608 plus fulvestrant presented at AACR

.svg)

-cropped.svg)