.svg)

Drug development is synonymous with competition. That's especially true when a company adopts a "challenger" strategy, which attempts to clinically address limitations of existing treatments to de-risk commercial opportunities.

In the span of a week, Relay Therapeutics delivered a resounding win for its next-generation PI3K-alpha challenger RLY-2608 – and then found itself in an exciting competition with a fellow next-generation challenger from Scorpion Therapeutics.

The two challengers take a similar molecular approach by binding to an inactive ("allosteric") site on mutated PI3K-alpha, which is key to sparing non-mutated ("wild-type") PI3K-alpha proteins in healthy cells. Both assets have proven their hypothesis that increased selectivity is key to delivering better outcomes for patients.

Which one is better positioned? That's impossible to say in September 2024, although both have no-doubter data.

In its preliminary phase 1 data readout, STX-478 obliterated comparisons to other single-agent ("monotherapy") PI3K-alpha inhibitors. The challenge is Relay Therapeutics doesn't have equivalent monotherapy data, as its focus on breast cancer specifically dictated an earlier focus on combinations. There are key differences between study design and patient populations that make for dislocated comparisons at best.

That won't stop Wall Street from trying. Let's walk through the September 2024 data readout from RLY-2608 and make the most granular comparisons to STX-478 possible – explaining all the nuances along the way.

RLY-2608 Data Readout: Explain Like I'm Five

An estimated 14% of all solid tumor cancers harbor mutations in the PI3K-alpha gene. That makes it the largest undrugged target in oncology with up to 310,000 new diagnoses in the U.S. each year, including an estimated 150,000 diagnoses of HR+/HER2- breast cancer.

For comparison, an estimated 58,000 cancer diagnoses each year include a KRAS G12C alteration. Bristol Myers Squibb paid $4.8 billion to acquire Mirati Therapeutics and its KRAS G12C inhibitor Krazati.

Nerds in lab coats might protest the above claim that PI3K-alpha is an undrugged target. There are approved PI3K inhibitors, but they're not selective against wild-type or non-alpha protein structures ("isoforms"). That means existing treatments have tolerability issues and low efficacy.

RLY-2608 was designed to address those limitations by selectively inhibiting mutated PI3K-alpha while sparing wild-type PI3K-alpha and PI3K-other isoforms.

Relay Therapeutics has focused the early development of RLY-2608 on a combination with fulvestrant in patients with HR+/HER2- breast cancer. "HR+" means hormone positive, while fulvestrant mows down estrogen receptors on the surface of cells (estrogen is the hormone in "hormone positive").

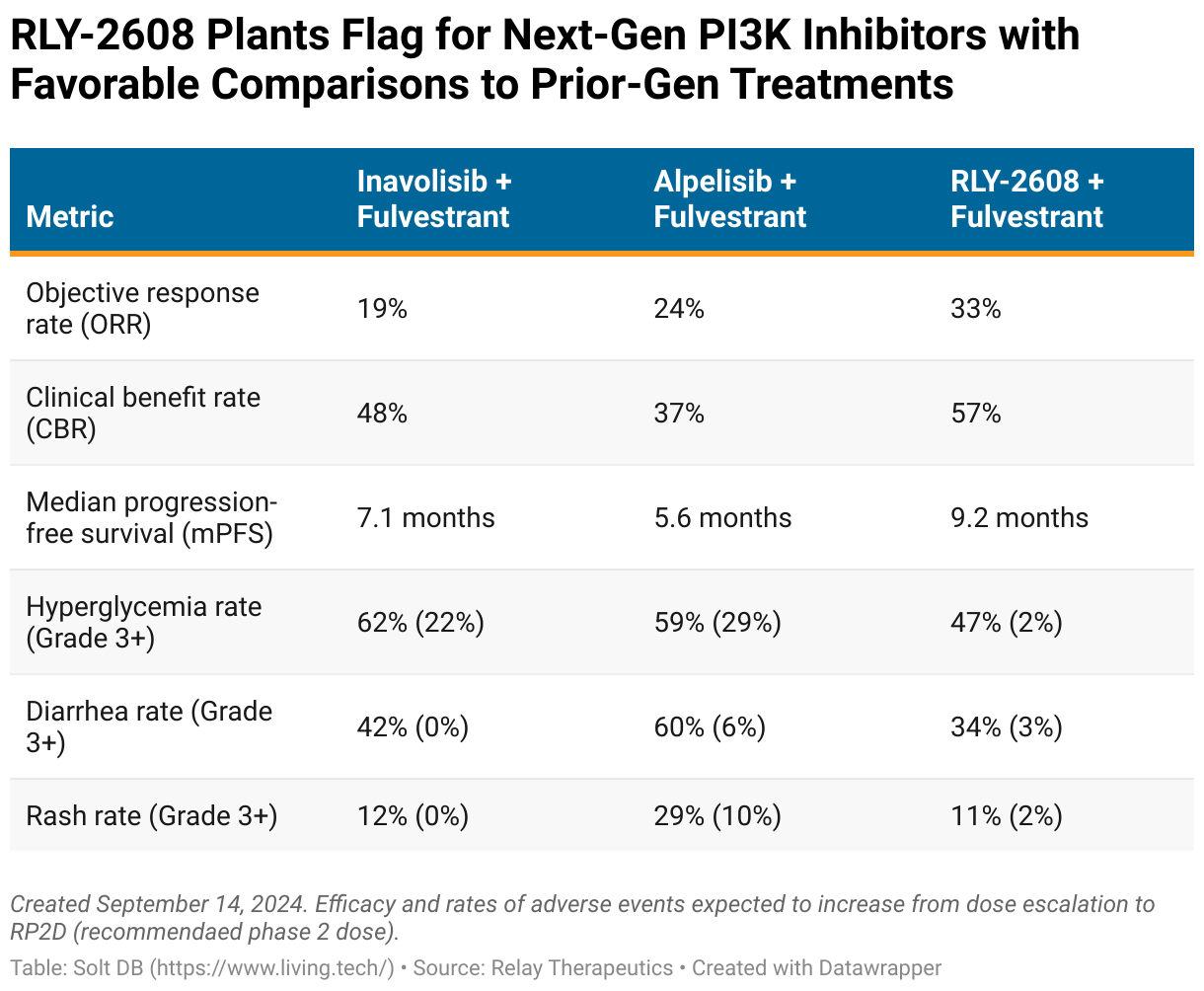

The September 2024 data readout clearly separates the RLY-2608 doublet from the competitive landscape at similar points of development. Non-selective competitors are too bogged down by tolerability issues to fully deliver on the promise of PI3K-alpha inhibitors.

The key metrics for measuring efficacy in this setting:

- Objective response rate (ORR) measures the number of patients who had a partial response or better, defined as tumor shrinkage of 30% or more

- Clinical benefit rate (CBR) measures the number of patients who had stable disease or a partial response

- Median progression-free survival (mPFS) measures the median length of time between a patient starting treatment and having their disease worsen

Tolerability is best demonstrated by rates of side effects, such as hyperglycemia and diarrhea, that limit existing treatments. A more selective inhibitor should have a more favorable tolerability profile.

Relay Therapeutics positioned its combination of RLY-2608 plus fulvestrant as the clear mark to beat. The doublet had an overall ORR of 33% (10/30) and a mPFS of 9.2 months, besting the highest marks from prior-generation competitors combined with fulvestrant. All data include the recommended phase 2 dose (RP2D) of RLY-2608 600 mg twice daily and patients with measurable disease (meaning no brain or bone lesions). The data exclude a complete response (meaning no evidence of disease) in a patient with non-measurable disease.

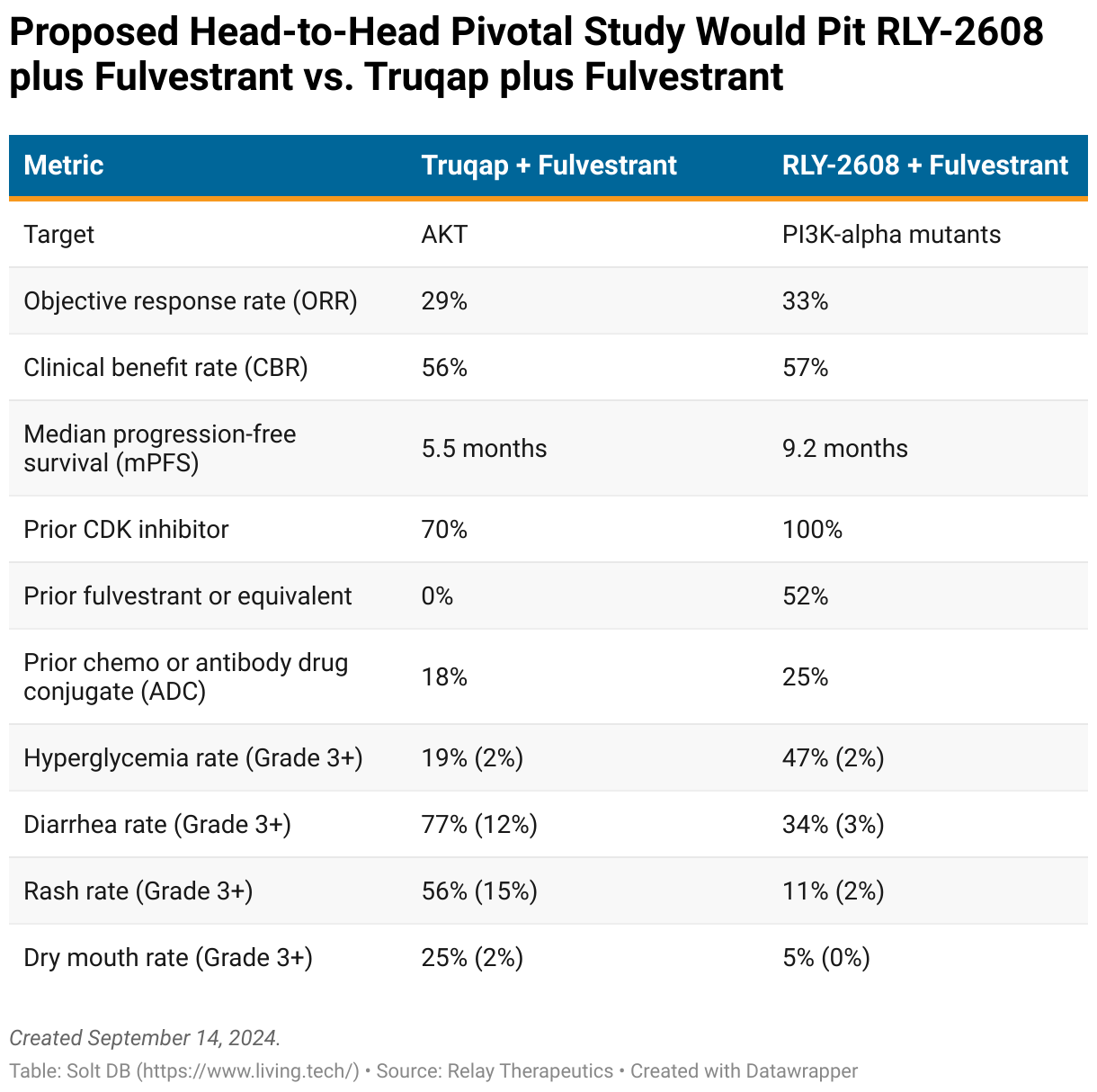

The promising data have the company dreaming of regulatory approval. Relay Therapeutics plans to conduct a pivotal study of RLY-2608 plus fulvestrant going head-to-head with Truqap plus fulvestrant in HR+/HER2- metastatic breast cancer. This specific indication represents an estimated 14,000 diagnoses per year and serves as proof of concept to treat even larger patient populations.

The irony is that Truqap is an AKT inhibitor, not a PI3K inhibitor. But it's currently the least bad option despite, or perhaps because, it only indirectly inhibits PI3K. It's specifically approved to treat PI3K/AKT/PTEN altered tumors in breast cancer.

The plan is to square off against Truqap in patients with PI3K-alpha mutations and no known PTEN or AKT mutations, which reduce response rates of PI3K inhibitors. That alone might handicap Truqap's combination with fulvestrant.

Relay Therapeutics proposes using mPFS as the primary endpoint, with overall survival (the FDA's preferred metric in pivotal studies) and ORR as the leading secondary endpoints. An eventual head-to-head study might not deliver a similarly decisive blow as the mPFS suggested in the table below, but the design favors RLY-2608 plus fulvestrant.

As the September 2024 data readout suggests, the selectivity of RLY-2608 makes it favorably positioned against prior-generation treatment options. The next challenge will be maintaining a competitive posture against other next-generation drug candidates like STX-478 from Scorpion Therapeutics.

RLY-2608 Data Readout: Talk Nerdy to Me

Relay Therapeutics provided datasets for specific patient populations that will be important for next-generation approval opportunities.

PI3K-alpha mutations are classified into two primary categories:

- Kinase mutations (primarily H1047R)

- Helical mutations (primarily E542X and E545X)

Breast cancers with PI3K-alpha mutations are equally likely to be kinase or helical, although some patients have both. That split makes it important to demonstrate efficacy in both types of mutations. Unfortunately, selective PI3K-alpha inhibitors appear to be struggling with helical alterations.

Here's how the September 2024 data readout for RLY-2608 plus fulvestrant looks when dissected between types of mutations.

- Among 30 evaluable patients with measurable disease (meaning no brain or bone lesions), half had kinase mutations (15/30) and half had helical mutations (15/30).

- The ORR among tumors harboring kinase mutations was 53% (8/15). At least three patients with ongoing responses at the data cutoff had the potential to improve to partial responses, which would lift the ORR to as high as 73% (11/15).

- The ORR among helical mutations was 13% (2/15).

Importantly, these data exclude patients with PTEN or AKT mutations, which decrease response rates to PI3K inhibitors. The dataset for this specific patient population will set up crucial future comparisons to emerging next-generation competitors such as STX-478 from Scorpion Therapeutics.

What About Scorpion Therapeutics and STX-478?

Any company that shares a co-founder with precision oncology pioneer Loxo Oncology deserves to be taken seriously.

Scorpion Therapeutics presented the first clinical data for its own next-generation PI3K-alpha inhibitor at the European Society for Medical Oncology (ESMO) annual meeting on September 15, 2024. STX-478 delivered impressive data that will make it a very competitive asset.

Unfortunately, the only thing imprecise about Scorpion Therapeutics and Relay Therapeutics is the ability to make meaningful comparisons between them due to differences in phase 1 study design.

- Monotherapy vs. combination: The first clinical data readout for STX-478 focused on its ability alone ("monotherapy") to treat various types of solid tumors with a PI3K-alpha alteration. The equivalent data readout for RLY-2608 at the American Association for Cancer Research (AACR) Annual Meeting in April 2023 instead prioritized combinations with fulvestrant in breast cancer.

- Restrictions on target mutations: The ESMO 2024 data readout for STX-478 only included patients with kinase or helical mutations, whereas the equivalent study for RLY-2608 allowed patients without these specific mutations. Tumors with kinase mutations respond better to PI3K-alpha inhibitors.

- Restrictions on pathway mutations: The phase 1 study for STX-478 excludes patients with a PTEN alteration and activating mutations in AKT, whereas the equivalent study for RLY-2608 that readout in April 2023 did not. The former population responds better to PI3K-alpha inhibitors.

- Restrictions on diabetic patients: The phase 1 study for STX-478 had less restrictive enrollment criteria for diabetic patients, whereas the equivalent study for RLY-2608 excluded patients above a certain blood-glucose threshold. Half of all individuals with HR+/HER2- breast cancer are prediabetic or diabetic, which makes it an important next-generation approval opportunity.

At ESMO 2024, Scorpion Therapeutics reported STX-478 monotherapy achieved an ORR of 21% in all tumor types (9/43) and 22% in HR+/HER2- metastatic breast cancer (5/23). This was from a dose escalation therapy, meaning the company hasn't optimized dosing yet. These are very strong data.

At AACR 2023, Relay Therapeutics reported RLY-2608 monotherapy achieved an ORR of 25% in HR+/HER2- metastatic breast cancer (1/4). But one non-responder didn't have a kinase or helical mutation, while that patient and another had non-measurable disease. In other words, RLY-2608 delivered an ORR of 50% (1/2) in an equivalent patient population. We don't know the PTEN or AKT mutation status of the remaining two patients, either.

I hope investors can see the absurdity of drawing comparisons to two to four patients.

Let's simplify things.

- Scorpion data will improve: Similar to RLY-2608, investors can expect response rates to increase for STX-478 once it has a RP2D level and is combined with fulvestrant and/or CDK inhibitors.

- Tolerability separability?: In preclinical testing, STX-478 preferred to bind to the H1047R mutation over healthy PI3K-alpha by 14-to-1. That's a little better than RLY-2608's selectivity of 11-to-1, which may allow for higher target coverage and lower levels of hyperglycemia. However, both assets observed similar rates of hyperglycemia in their respective dose escalation studies.

- Convenience could win: In a future where both assets deliver equivalent tolerability and efficacy in a given patient population, the advantage would go to STX-478 due to its once-daily dosing schedule. RLY-2608 is dosed twice daily.

To be clear, Relay Therapeutics set a high bar.

The initial "apples-to-apples" comparison between the two assets will be in the specific patient population of HR+/HER2- metastatic breast cancer including kinase or helical mutations of PI3K-alpha and excluding PTEN and AKT mutations. Nerds, amiright?

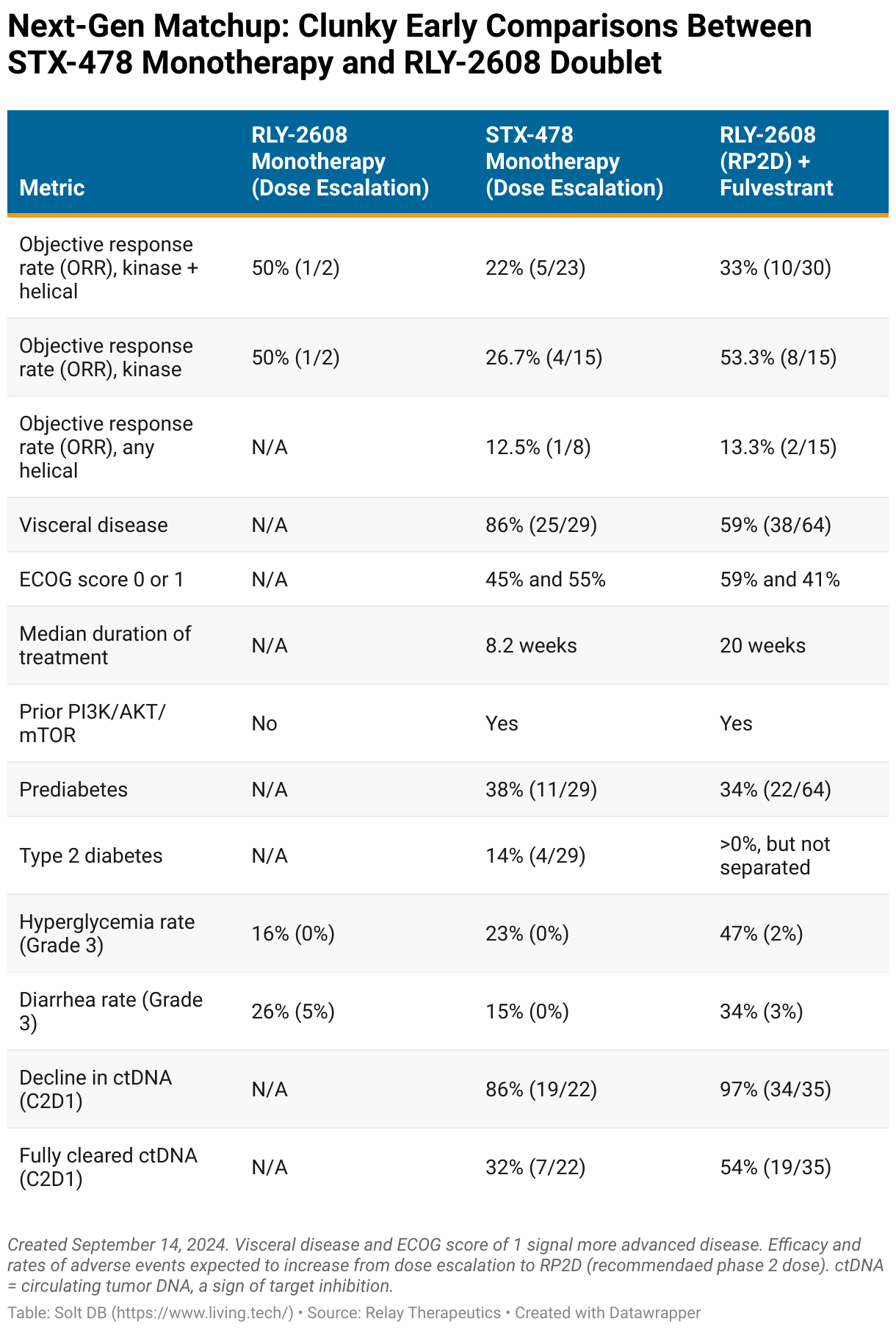

- The doublet of RLY-2608 plus fulvestrant notched an ORR of 33% (10/30) overall, 13% in helical mutations (2/15), and 53% in kinase mutations (8/15).

- Scorpion Therapeutics doesn't yet have data for a doublet of STX-478 and fulvestrant, but the drug candidate proved impressively effective by itself. STX-478 monotherapy notched an ORR of 22% overall (5/23) spread across various dose levels. That included an ORR of 13% when helical mutations were present (1/8) and 27% in kinase mutations (4/15).

Comparisons are a bit clunky due to RLY-2608 lacking comparable monotherapy data and STX-478 monotherapy data being biased to patients with kinase mutations.

The two primary types of mutations have roughly equal real-world prevalence in HR+/HER2- breast cancer, which was reflected in the RLY-2608 doublet data. Helical mutations and kinase mutations were each present in exactly half of all evaluable patients. However, the patient population for the STX-478 monotherapy data readout was split more favorably, with 65% of patients having only a kinase mutation and 35% having a helical mutation.

With those nuances in mind, here's how data readouts for RLY-2608 monotherapy, STX-478 monotherapy, and RLY-2608 plus fulvestrant appear side by side.

Forecast & Modeling Insights

My updated model for Relay Therapeutics now assigns an estimated fair valuation of $3.151 billion (vs. $3.5 billion) after several refinements.

- Updated to reflect lirafugratinib peak annual sales opportunity of $400 million in a tumor-agnostic patient population, which has been converted to a 20% royalty stream.

- Updated to reflect increased probability of success for RLY-2608 plus fulvestrant (67.5% now vs. 30.1% prior).

- Updated to reflect initial contributions from vascular malformations and first-line potential for triplets with CDK inhibitors. For perspective, Piqray / Vijoice (alpelisib) from Novartis generated $505 million in full-year 2023 revenue from both its doublet with fulvestrant and as a monotherapy in vascular malformations. It had peak annual revenue potential of roughly $1.5 billion before Truqay was approved.

- Updated to reflect recent dilution from public stock offering.

Competition is omnipresent

Drug development rarely has all-or-nothing or even winner-take-most outcomes. Outside rare examples, large opportunities often support multiple successful drug products.

Case in point: There are nine approved PD-1/L1 inhibitors. Five are expected to have full-year 2024 revenue of at least $1 billion, while the second drug in the class to earn approval currently outsells the first-approved drug by more than 2:1.

Will Relay go all-in on breast cancer?

Relay Therapeutics has been positioning itself to go all-in on HR+/HER2- breast cancer specifically, which represents roughly half of all solid tumors with a PI3K-alpha mutation. The breast cancer opportunity hinges on combinations, which is why the company has a next-generation estrogen degrader (RLY-1013) and next-generation CDK2 inhibitor (RLY-2139) ready to begin clinical trials. It's unclear if either will advance or if the company will settle for combinations with more mature external assets.

Monetization opportunities

The business will enter Q4 2024 with an estimated cash balance of $846 million following the latest capital raise. There are two opportunities to extend the cash runway even further.

First, Relay Therapeutics plans to monetize rights to lirafugratinib (FGFR2 inhibitor), which could fetch a meaningful upfront cash payment of $50 million to $100 million. Additional cash milestones would likely be due if the tumor-agnostic data earn a supplemental approval later.

Second, investors might expect Relay Therapeutics to find a partner to explore the opportunity in non-breast tumors. That would provide funding and free bandwidth to focus on an extensive breast cancer portfolio – and strategic opportunities to diversify the overall pipeline assets unrelated to RLY-2608.

Margin of Safety & Allocation

Relay Therapeutics is considered a Growth (Quality) position. The current modeled fair valuation for the company based on my 2024 model is below:

- Market close September 13: $7.60 per share

- Modeled Fair Valuation: $17.99 per share (vs. $22.73 per share prior)

- Allocation Range: Up to 15%

Relay Therapeutics reported 133.890 million shares outstanding as of August 2, 2024. The modeled fair valuation above assumes 175.084 million shares outstanding, which includes dilution from the recent public stock offering, dilution from the optional shares in the public stock offering, and an additional 5% dilution.

Further Reading

- September 2024 press release announcing preliminary phase 1/2 data for RLY-2608 plus fulvestrant in breast cancer

- September 2024 research note providing a "cheat sheet" ahead of the RLY-2608 data readout

- September 2024 press release announcing preliminary phase 1 data for STX-478 monotherapy in breast cancer and other tumor types

- April 2023 press release announcing preliminary phase 1 data for RLY-2608 monotherapy and RLY-2608 plus fulvestrant in breast cancer and other tumor types

.svg)

-cropped.svg)