.svg)

Weak news flow has been a headwind for Relay Therapeutics since it went public in 2020. Part of that is the company's own doing.

Relay Therapeutics is the only drug developer using advanced computing to prove its approach adds real-world value in clinical trials, not just the first step of drug discovery. Recursion Pharmaceuticals, Exscientia, and Schrodinger – all companies covered by Solt DB Invest – don't have that yet. I think some can get there.

However, Relay Therapeutics doesn't associate itself with its "TechBio" peers, or talk much about artificial intelligence. It doesn't have a charismatic CEO. It hasn't empowered its marketing team to run wild across social media endearing itself to retail investors or become "This Cathie Wood Stock." (Don't you love the marriage of SEO and clickbait?) Heck, the company has held only a single quarterly conference call for its own shareholders. Ever.

A lack of news flow has been frustrating for investors. Don't think it matters? Relay Therapeutics is valued at $1.33 billion, whereas Recursion Pharmaceuticals is valued at $2.23 billion. Relay had more than twice the cash balance of Recursion ($810 million vs. $387 million) as of the end of September 2023 and has advanced one more asset into clinical trials (six vs. five). It was founded two years later than its peer.

I value the company's focus on execution, but periodic signs of life wouldn't be so bad either. Investors who agree should be careful what they wish for.

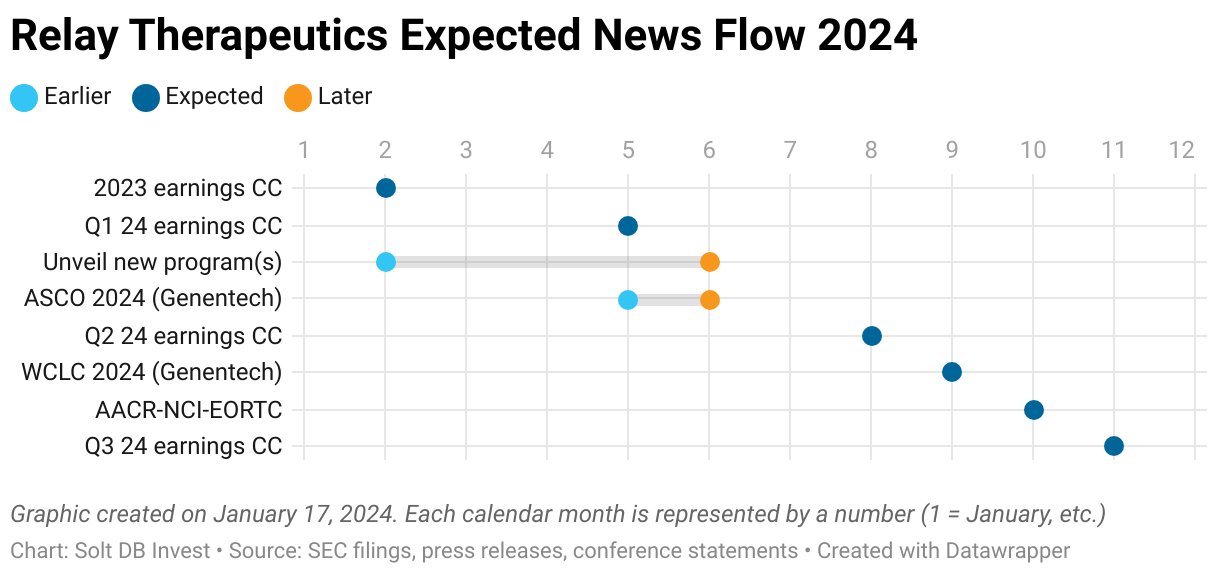

Relay Therapeutics will make investors suffer through a barren first half of 2024, then follow up with three significant data readouts in the second half. The clinical updates have the potential to make or break the company's ambitious plan to build the industry's most comprehensive breast cancer treatment portfolio.

This year mostly hinges on the second-most advanced asset, RLY-2608. It could end the year as one of the most valuable drug candidates in the global industry pipeline.

A Strategic Focus on Breast Cancer

Breast cancer is the most common cancer diagnosis among Americans. It represented 15% of roughly 2 million new cancer cases in 2023. Although advances in screening and treatment have significantly improved patient outcomes, the malignancy was responsible for 7% of all U.S. cancer deaths last year.

Relay Therapeutics wants to keep driving that number closer to zero. To do so, it's set out on an ambitious strategy to combine advanced computational models with real-world experimentation. The goal is to develop multiple next-generation treatments to help nearly every treatment stage in an evolving standard of care.

More specifically, the drug developer has its eye on HR+ / HER2- breast cancer. This funny acronym is used by nerds in lab coats to describe the genetic composition of tumors and guide treatment decisions.

- HR+ means "hormone receptor positive." Hormone receptors on breast cancer cells bind to the hormones estrogen or progesterone. These hormones promote cell growth, which drives cancer proliferation. Roughly 80% of HR+ breast cancer is estrogen receptor positive (ER+).

- HER2- means "human epidermal growth factor receptor 2 negative." Tumors with no or low levels of HER2 receptors cannot be adequately treated by drugs that block the HER2 receptor, which helps doctors focus on other treatment options. Roughly 85% of all breast cancers are HER2-.

An estimated 75% to 80% of all breast cancers are HR+ / HER2-, which makes it a good place to concentrate efforts for maximizing patient outcomes.

Patients who have breast tumors removed often receive adjuvant therapy to increase the chances cancer was beaten into submission. When breast cancer spreads to other parts of the body (called "metastatic breast cancer"), then it often requires more significant pharmaceutical intervention.

Whether adjuvant therapy or early treatment for metastatic tumors, the current standard of care progresses through a series of treatments each intended to box in the genetic defenses of breast cancer cells, so the immune system can clear cancer cells and tumors.

- Endocrine therapy (ET): If HR+ breast cancer partially survives on hormones, then ET can be used to starve cancer cells and significantly slow cell growth.

- CDK inhibitors: The CDK (cyclin-dependent kinase) family of proteins is important for cell growth in healthy and tumor tissues. CDK4/6 inhibitors block two of the proteins in this family, which can significantly slow cancer cell growth. CDK4/6 inhibitors are often combined with ET.

- Antibody drug conjugates (ADCs): Drug developers are increasingly interested in using ADCs for treating late-stage and early-stage breast cancers, although these products currently target HER2+ tumors.

However, the standard of care for treating metastatic HR+ / HER2- breast cancer is evolving with advances in genomics and the ability to design more selective drug compounds. The industry is eager to develop next-generation treatments, including:

- CDK4 or CDK2 inhibitors: The current standard of care utilizes CDK4/6 inhibitors, but ideally patients would receive a highly selective blocker for CDK4 or CDK2. Many HR+ breast cancer tumors are actually driven by CDK2. When these patients are treated with standard CDK4/6 they often have poor responses and worse outcomes.

- Estrogen receptor (ER) degraders: Protein degradation has emerged as a promising approach to targeted inhibition of disease-driving molecules. For HR+ / HER2- breast cancer patients, ET might one day be replaced with targeted estrogen receptor-alpha degraders, which could reduce side effects and improve responses.

- PI3K inhibitors: This is the most common undrugged target in cancer. An estimated 14% of all solid tumor cancers have mutated PI3K-alpha proteins, including 35% of HR+ / HER2- breast cancers. There are no treatment options. The industry has struggled to develop drugs that target PI3K-alpha while sparing similar-looking family members, which is problematic considering PI3K regulates glucose metabolism. It's one of the largest remaining opportunities in all of drug development.

Relay Therapeutics is not developing antibody-drug conjugates. It is developing next-generation treatments for every other aspect of an evolving standard of care in HR+ / HER2- breast cancer.

The company paused development of its CDK2 inhibitor (RLY-2139), which can begin a phase 1 clinical trial within 30 days upon resuming. It also paused development of its ER-alpha degrader (RLY-1013) prior to choosing a development candidate, which occurs at the end of the drug discovery process immediately before progressing into preclinical studies. The decisions were intended to preserve and extend the cash position while focusing limited bandwidth on near-term programs.

That includes the lead drug candidate, RLY-4008 (FGFR2 inhibitor), which doubled the competitive landscape's objective response rate (ORR) in bile duct cancer. The asset was barreling toward a pivotal trial before the company decided to reset and focus on a larger tumor-agnostic opportunity, which delayed development by at least 12 months.

The near-term focus also includes RLY-2608, a first-in-class PI3K-alpha inhibitor that will serve as the foundation for the company's breast cancer strategy. Two data readouts in 2024 will determine the trajectory for the overall pipeline and, at least in the near term, the fate of Relay Therapeutics.

It All Comes Down to RLY-2608

Drugging PI3K-alpha has proven an insurmountable challenge for drug developers to date. The problem is two-fold.

- First, PI3K-alpha regulates glucose metabolism. That's key to it being a valuable target in treating cancer. If you can disrupt PI3K-alpha in cancer cells, then you can disrupt a key source of fuel (glucose) for tumor growth. The problem is that inhibitors developed to date aren't selective for mutated copies of PI3K-alpha used by cancer cells. That means they also whack wild-type copies (healthy working proteins in normal cells), which leads to too much glucose in the blood (hyperglycemia). This is the same side effect that characterizes Type 2 diabetes. As a result, diabetic or prediabetic patients were excluded from phase 3 trials of the leading PI3K inhibitor drug candidate. That alone would exclude 50% of the HR+ / HER2- breast cancer patient population.

- Second, PI3K proteins have multiple isoforms, or 3D structures, which are designated by Greek letters. The alpha isoform is most often indicated in cancers. Inhibitors that sloppily whack the delta isoform risk gastrointestinal side effects that force patients off treatment.

It's been almost as frustrating as weak news flow. Drug developers know that inhibiting PI3K-alpha can have meaningful efficacy, but they've struggled to selectively target the protein in cancer cells. That's forced drug developers to reduce doses to manage side effects, but higher (and safer) doses could have a much greater impact.

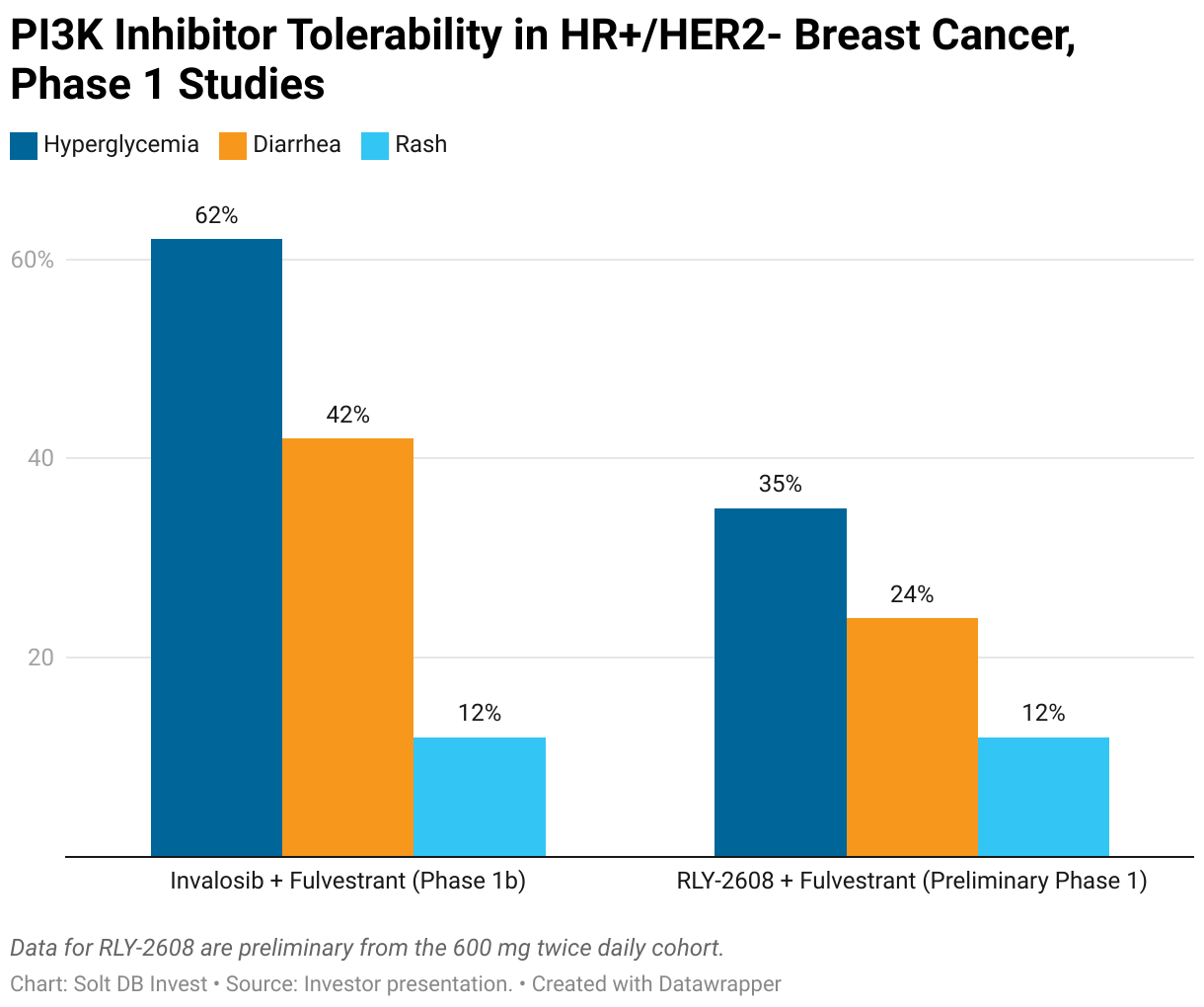

Genentech wields the leading PI3K-alpha inhibitor drug candidate, but it's not mutant or isoform selective. As a result, 62% of patients receiving inavolisib plus fulvestrant (an ET) in a phase 1b clinical trial experienced hyperglycemia (a sign it wasn't selective for mutants), 42% experienced diarrhea (a sign it wasn't selective for the alpha isoform), and 12% developed rash (an on-target side effect).

Relay Therapeutics is developing RLY-2608 as the industry's first pan-mutant PI3K-alpha inhibitor. "Pan" is Latin for "across," similar to Pangea, pandemonium, or Pantera. That means the molecule has activity across multiple mutations in the PI3K-alpha protein (such as E542K and E545K) that are often observed in breast tumors, but is more likely to spare the wild-type (working healthy copies) of the protein.

The early results were encouraging, albeit incomplete. Investors only have partial data from the dose escalation part of a phase 1 clinical trial, which evaluates various doses to get a better sense of tolerability and begin identifying a dose level for future studies. The data include only a handful of patients at each dose level, including dose levels that are too low to be meaningful for tolerability (higher doses will have more side effects) or efficacy (higher doses could be more effective).

In a preliminary phase 1 data readout, only 35% of patients taking RLY-2608 (600 mg twice daily) plus fulvestrant experienced hyperglycemia, 24% experienced diarrhea, and 12% experienced rash.

Although the dose escalation portion of a phase 1 study isn't meant to draw conclusions about efficacy, it's still important to see early signals.

Relay Therapeutics reported two partial responses, one in the 400 mg group and one in the 600 mg group, both taken twice daily. Among patients with at least six months of follow up in the 600 mg cohort, the objective response rate (ORR) was 20%. While that's identical to non-selective PI3K inhibitors, it included only five patients. The company thinks a cleaner tolerability profile could allow patients to remain on treatment for longer, especially if RLY-2608 can be studied in earlier lines of treatment (not just the advanced and heavily pretreated patient populations experimental drugs are usually studied in).

That's not farfetched. The company reported an ORR of 50% for its lead drug candidate, RLY-4008, based on a similarly early patient population. When results were updated from more patients treated for longer at the optimized dose, the ORR jumped to 83%.

Delivering a competitive ORR will be important. But a favorable tolerability profile for RLY-2608 creates opportunities for combination therapies.

Due to the prevalence of PI3K-alpha mutations, especially in HR+ / HER2- breast cancer, the value of a pan-mutant and alpha selective molecule will come from combination therapies.

- Doublet combination: Relay Therapeutics is now studying RLY-2608 (600 mg twice daily) plus fulvestrant in 40 patients.

- Doublet combination: Relay Therapeutics is now studying RLY-2608 (400 mg twice daily) plus fulvestrant in 20 patients. This cohort had promising results in the preliminary study, including a partial response, and might have more favorable side effects compared to the 600 mg dose.

- Triplet combination: Relay Therapeutics is studying RLY-2608 (400 mg twice daily or 600 mg twice daily) in combination with fulvestrant and a CDK4/6 inhibitor (Kisqali (ribociclib)).

Whereas the doublet combinations have potential in treating second-line or higher HR+ / HER2- breast cancer, the triplet combination could potentially become a first-line treatment option. A patient receiving treatment for the first time is considered first line, whereas a patient receiving treatment for the second time is considered second line, and so on. Generally speaking, the earlier the line of treatment, the larger the patient population available for treatment.

In the second half of 2024, Relay Therapeutics expects to report updated data for the dose escalation study of RLY-2608 plus fulvestrant (not very meaningful now), data from an expansion cohort receiving 600 mg twice-daily plus fulvestrant, and data from the triplet combinations. The doublet combination of the 400 mg twice daily dose isn't expected in 2024, but could be important for determining the pivotal dose in a future study.

That means investors can expect three meaningful data readouts in 2024:

- RLY-2608 (600 mg twice daily) doublet safety and efficacy

- RLY-2608 (400 mg twice daily or 600 mg twice daily) triplet safety data

- RLY-4008 tumor-agnostic data with more patients

If the data readouts for RLY-2608 disappoint, then investors will question the breast cancer strategy for Relay Therapeutics and wonder why they should stick around. If the data readouts are positive, then it establishes a meaningful foundation to build upon and builds confidence in the company's ambitious strategy.

Expected News Flow for 2024

In 2024, Relay Therapeutics will have a relatively quiet first half followed by a flurry of meaningful data readouts in the second half.

Unveiling an additional asset (or two)

Despite pausing multiple programs to preserve cash, Relay Therapeutics has teased an additional seven programs in drug discovery or preclinical development. The company expects to publicly unveil one or more programs in 2024, which could help an otherwise stagnant first-half news flow.

Previously, the company teased work in oncology (potentially outside of HR+ / HER2- breast cancer) and rare diseases. These programs could help to supplement or diversify the strategic focus on breast cancer, especially if RLY-2608 flops. To be clear, these won't make up for a very negative reaction if data readouts disappoint.

New and potentially non-core programs also create partnership opportunities. Relay Therapeutics might not have much desire to develop wholly-owned rare disease assets, but it could outlicense them for upfront milestone payments to monetize its efforts and raise cash.

Genentech SHP2 update (or not)

Another Relay-generated asset could have an update in 2024: GDC-1971. The SHP2 inhibitor formerly known as RLY-1971 was outlicensed to Genentech (Roche) in December 2020.

Relay Therapeutics snagged $75 million upfront, has earned $35 million in upfront milestone payments, and can receive up to $685 million in additional milestone payments, plus royalties on sales. There are separate milestones available if Genentech's KRAS G12C inhibitor GDC-6036 earns approval in combination with the asset. Although Relay had the right to opt-in and share development costs, it elected not to do so last year. It still has the right to combine GDC-1971 with its own assets.

Genentech bought rights to the asset because SHP2 sits at the juncture of many of the most important metabolic pathways that drive solid tumor cancers. GDC-1971 is being studied in three separate combination studies:

- KRAS: A combination with GDC-6036 (divarasib) was initiated in July 2021 as part of a larger study. This cohort (Arm F) could be completed in 2024, although Genentech may not publicly share data.

- PD-1/L1: A combination with Tecentriq, a PD-1/L1 inhibitor, was initiated in August 2022. Tecentriq likely generated nearly $4.5 billion in revenue for Roche in 2023.

- EGFR: A combination with two different EGFR inhibitors was initiated in January 2024. One of the combinations is with Tagrisso, the bestselling drug for AstraZeneca, which likely generated just under $6 billion in revenue in 2023.

The chemical name has also been revealed (migoprotafib). Earlier-stage assets are generally only known by their pipeline identifier (GDC-1971), so this is sometimes a sign that there's more commitment to an asset. It can also simply mean the core intellectual property is in place, which takes a few years to hammer out.

How Relay Therapeutics Can Succeed and Fail in 2024

For Relay Therapeutics, this year all comes down to the data readouts for RLY-4008 and (especially) RLY-2608. The outcomes will determine the trajectory of the stock, but also for the business in 2025 and beyond.

Achieving success looks like

If the data disclosures for RLY-2608 are convincingly favorable, then Relay Therapeutics would see its valuation reset significantly and durably higher. Our modeled fair valuation of $3.5 billion would be within reach by the end of 2024.

Sweeping the data readouts with successful outcomes would also alter the near-term trajectory for the business. Many future developments hinge on favorable data for RLY-2608.

- Relay Therapeutics would likely take advantage of a higher valuation with a large public offering of common stock (>$250 million if no partnerships are announced prior). The funds would extend the cash runway into 2027 or 2028.

- More important, the funds would allow development to be resumed for RLY-2139 (CDK2 inhibitor), RLY-1013 (ER-alpha degrader), and the unnamed PI3K-alpha inhibitor aimed at the H1047R mutation (which is spared by RLY-2608). All are important for the strategic focus on next-generation breast cancer treatments.

- RLY-2139 could begin a clinical trial within 30 days of resuming activity. One of its first clinical trials could be an expansion cohort in the triplet combination for RLY-2608, simply replacing the CDK4/6 inhibitor – a big step for the overall strategy.

In addition to the gravitational pull of RLY-2608, Relay Therapeutics would benefit from separate developments.

- It sure would be nice if Genentech shared data for GDC-1971, although the timing of clinical trials might push this into late 2024 or early 2025. So much for news flow.

- Unveiling new programs in drug discovery could give investors more to look forward to beyond breast cancer, especially if these programs are partnered off to quickly monetize their potential.

Failing to deliver looks like

Like it or not, 2024 is all about delivering favorable results for RLY-2608. The scenarios where results are mixed or unfavorable wouldn't be so great for investors.

- If data readouts for RLY-2608 fail to convince investors, then the near-term trajectory would be significantly impacted. Although the current valuation could be justified on RLY-4008 alone, a lack of mature assets beyond that means investors would be waiting for yet more data for RLY-2608 in 2025 or, in a worst-case scenario, several years for meaningful data readouts from emerging assets. That would drag on the company's valuation.

- Unveiling new programs in drug discovery could backfire. If the programs aren't significant or lack external partners, then what the f*nch was the point of pausing development for core programs in HR+ / HER2- breast cancer? It makes much more sense to outlicense rare disease programs and focus on breast cancer, so if the business doesn't court partners, it'll be easy to question the strategy.

- I expect Genentech won't be able to make a go / no-go decision for GDC-1971 until 2025, but a no-go decision in 2024 would abort a meaningful economic opportunity for Relay Therapeutics.

Margin of Safety & Allocation

(Refined to account for Nextech investment and dilution.)

Relay Therapeutics is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2023 model is below:

- Market close January 17: $10.42 per share

- Modeled Fair Valuation: $25.31 per share

- Allocation Range: Up to 15%

Relay Therapeutics reported 123.269 million shares outstanding as of October 27, 2023. The modeled fair valuation above accounts for an additional 2.5 million shares purchased by Nextech in a private placement announced in January 2024 and an additional 10% dilution, for a total of 125.769 million shares outstanding.

Further Reading

- January 2024 investor presentation from the J.P. Morgan Healthcare Conference

- October 2023 research note analyzing the data readout for RLY-4008 in FGFR2-altered cancers

- April 2023 research note analyzing the data readout for RLY-2608 in PI3K-alpha altered cancers

.svg)

-cropped.svg)