.svg)

What's old is new again for Relay Therapeutics – at least when it comes to optimal dosing of its prized asset.

The U.S. Food and Drug Administration (FDA) signed off on the design for the first pivotal study of RLY-2608 in breast cancer. In an unusual move, regulators agreed to a 33% dose reduction compared to the mid-stage study. The new dose – 400 mg, twice daily – had already been tested by the precision medicine company. It then opted to sacrifice a little tolerability for higher efficacy with a recommended phase 2 dose (RP2D) of 600 mg, twice daily.

Preliminary phase 2 results announced in December 2024 supported the higher dose. An objective response rate (ORR) of 39% and a median progression free survival (mPFS) of 11.4 months easily outperformed existing treatments. More patients experienced side effects compared to lower doses tested, but grade 3 fatigue (9.4%), diarrhea (3.1%), and hyperglycemia (3.1%) were relatively rare.

Why make a change now?

Relay Therapeutics conducts unusually robust clinical trials for a precommercial drug developer. The idea is to generate as much high-quality data as early as possible to inform development decisions. If a program needs to be terminated or tweaked, then it's better to discover that soon after clinical entry – not years and hundreds of millions of dollars later.

In the case of RLY-2608, the company generated data showing a 400 mg dose taken twice-daily with food had similar rates of exposure to the RP2D of 600 mg taken twice-daily on an empty stomach (fasted). Relay Therapeutics thinks the new dose is optimized for the overall commercial opportunity: fewer pills with more convenient administration for patients, lower rates of upper gastrointestinal side effects like nausea and reduced appetite, and similar levels of efficacy compared to the RP2D.

Success in Drug Development is a Three-Legged Stool

Refining the dose of RLY-2608 immediately before the first pivotal study was only possible because Relay Therapeutics conducts unusually robust clinical trials.

A slew of emerging technology platforms combine experimental and computational data to de-risk drug discovery. That includes Dynamo from Relay Therapeutics, Recursion OS from Recursion Pharmaceuticals, and Ginkgo Bioworks' cell engineering services, among others.

Yet, amid all the hype, investors appear to be forgetting the simple reality of successful drug development: discovered molecules must become developed molecules must become commercialized molecules.

Execution in one area doesn't guarantee success in another – and few companies succeed at all three. The most important is commercial execution, for which AI drug discovery expertise offers no help at all.

Relay Therapeutics has demonstrated it excels at drug discovery. The FGFR2 inhibitor lirafugratinib earned FDA Breakthrough Therapy designation – the first AI-discovered molecule to do so – by doubling response rates in bile duct cancer. Meanwhile, the company's scientists solved the first full-length structure of the PI3K-alpha protein (one of the most important in human biology) and discovered a novel allosteric pocket, leading to RLY-2608 as the first pan-mutant PI3K-alpha inhibitor.

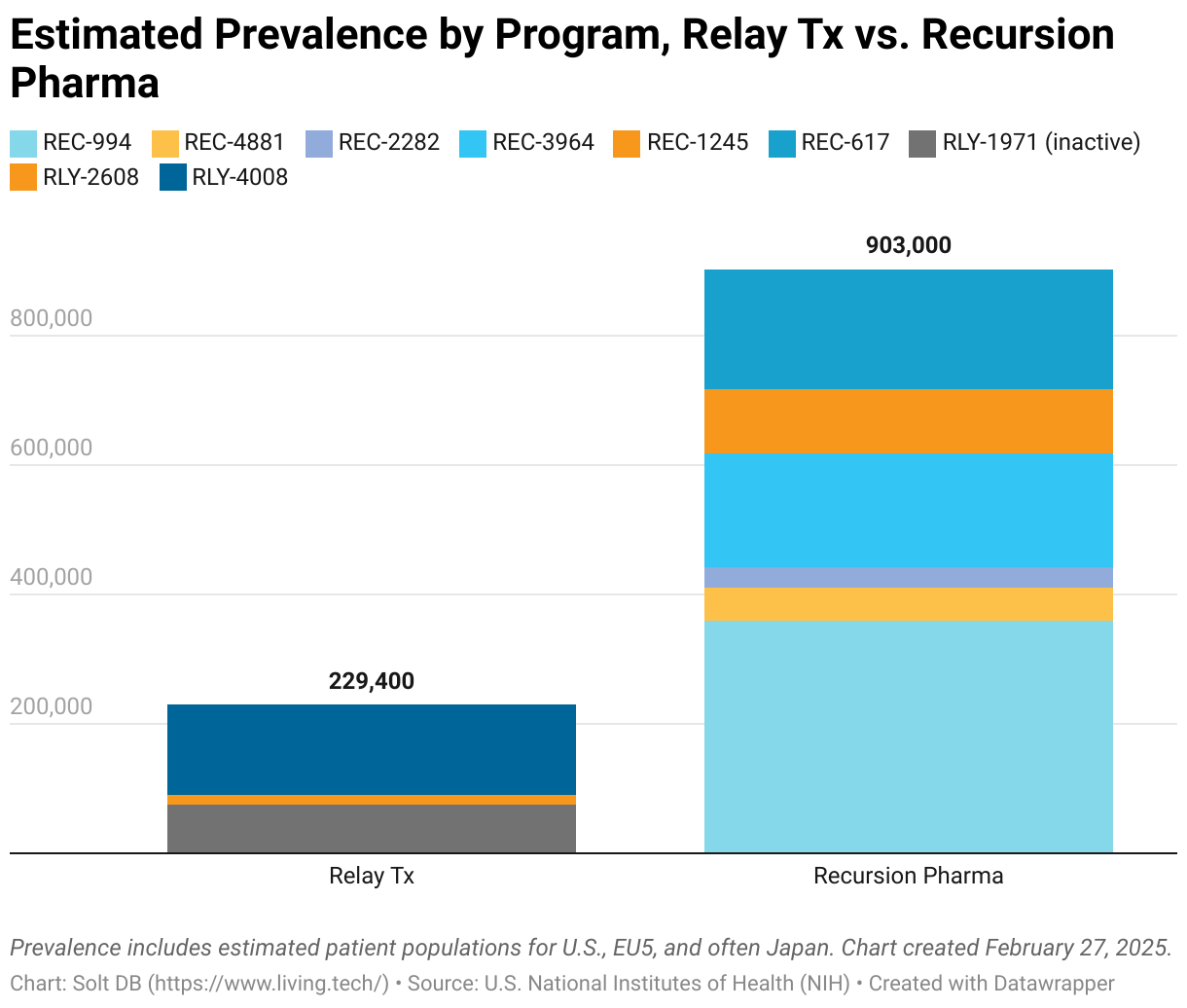

The company is also proficient in drug development. Its four clinical-stage assets were or are being evaluated in programs designed to enroll 1,701 patients total, according to data published by the National Institutes of Health (NIH). It has already dosed over 800 patients within its programs. By contrast, fellow supercomputer-wielder Recursion Pharmaceuticals expects to enroll 622 patients when evaluating its first seven assets.

Not all therapeutic indications are created equal. The clinical development of a rare disease program will enroll many fewer patients than one for a highly prevalent condition. These differences must be considered when comparing the robustness of clinical trial designs across pipelines.

But determining prevalence is more art than science. Consider that both Recursion Pharma and Relay Therapeutics aspire to treat cerebral cavernous malformations (CCM). The former estimates the patient population at 360,000 individuals in the United States, EU 5 (Germany, France, United Kingdom, Italy, and Spain), and Japan. The latter estimates 240,000 individuals.

Either number represents a significant commercial opportunity. But Recursion Pharma enrolled only 62 patients in a phase 1/2 study evaluating REC-994. Data shared in February 2025 demonstrated no clear efficacy signal. The lack of detail-rich data – stemming from a too-small study design – increases the risk of failure in a planned pivotal study.

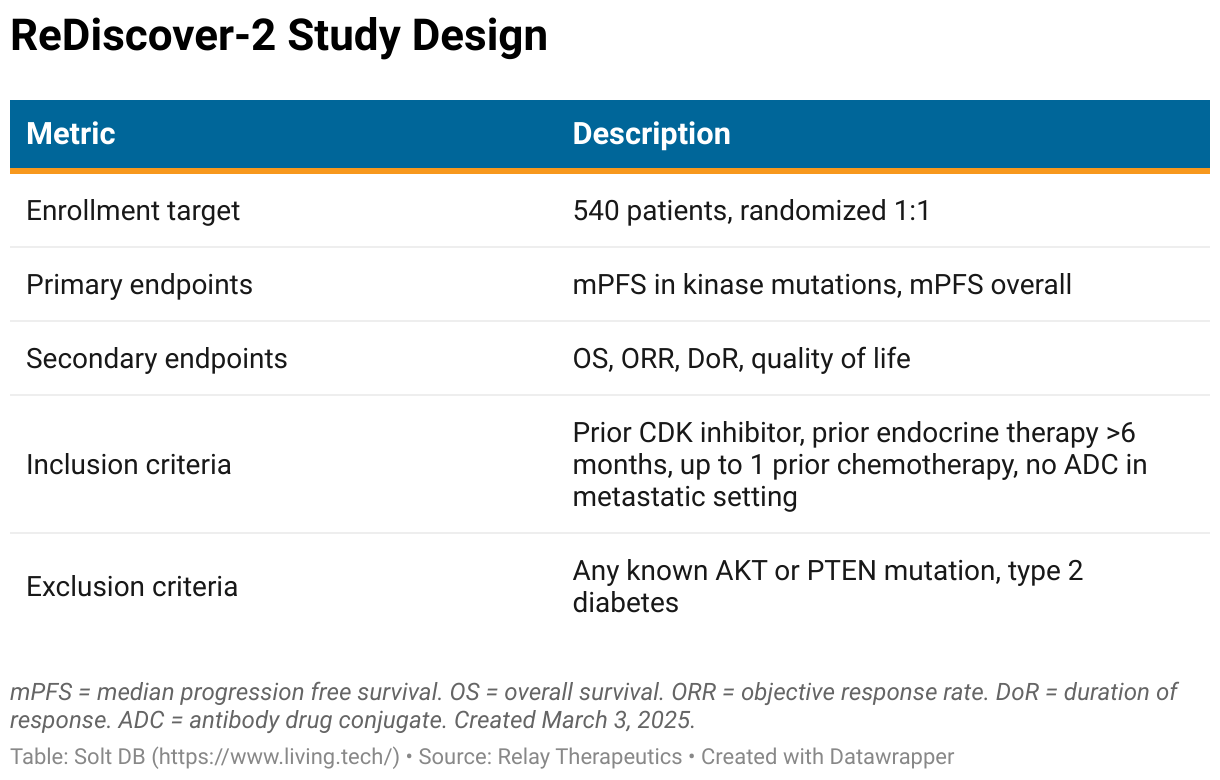

ReDiscover-2 Pivotal Study, Explained

Relay Therapeutics expects to begin enrolling patients in the first pivotal study of RLY-2608 in mid-2025.

The phase 3 clinical trial, named ReDiscover-2, will evaluate RLY-2608 plus fulvestrant in the second-line (2L) setting for patients with HR+/HER2- breast cancer. It will be compared directly to Truqap (capivasertib) plus fulvestrant, which is the standard of care.

Key elements of the study design include:

ReDiscover-2 has a favorable design for RLY-2608

Going head-to-head with Truqap is an ambitious move, but the final study design favors a positive outcome. To be blunt, it will be nearly impossible for Relay Therapeutics to fail the ReDiscover-2 study.

Consider a few key elements of the study design.

First, Truqap is an AKT inhibitor, not a PI3K inhibitor. ReDiscover-2 will exclude patients with known AKT or PTEN mutations, making for a true apples-to-apples comparison in the ability to inhibit PI3K-alpha mutations. This handicaps Truqap.

Second, the FDA agreed to hierarchal primary endpoints. That means the first primary endpoint is median progression free survival (mPFS) in individuals with a kinase mutation. The second primary endpoint is overall mPFS. RLY-2608 should outperform Truqap on both metrics, but specifically including mPFS in kinase mutations provides at least one buttery-smooth path to approval.

- In its own pivotal study, Truqap plus fulvestrant demonstrated an mPFS of 7.2 months overall and 5.5 months in patients who had been previously treated with a CDK inhibitor. The latter mirrors the patient population that will be enrolled in ReDiscover-2.

- In the phase 2 study, RLY-2608 plus fulvestrant demonstrated an mPFS of 9.2 months overall in 2L patients and later, 11.4 months in 2L patients, and 11.4 months in all patients with a kinase mutation.

- Statistically speaking, the RLY-2608 doublet mPFS in kinase mutations was oh-so-close to being 18.4 months. A larger study could very well result in a much longer mPFS in kinase mutations than has been observed to date. It's likely to double Truqap on this metric.

In other words, RLY-2608 plus fulvestrant is very likely to emerge from the ReDiscover-2 study with at least a kinase-specific approval locked up. The total market opportunity for kinase mutations in 2L HR+/HER2- breast cancer is $1.5 billion – and Relay Therapeutics would be the first and only with a mutation-specific approval. If it secures approval regardless of mutation status, then the market opportunity would be nearly $3 billion.

Poised for rapid commercial success

A successful outcome in ReDiscover-2 would lay the foundation for a swift commercial ramp for RLY-2608.

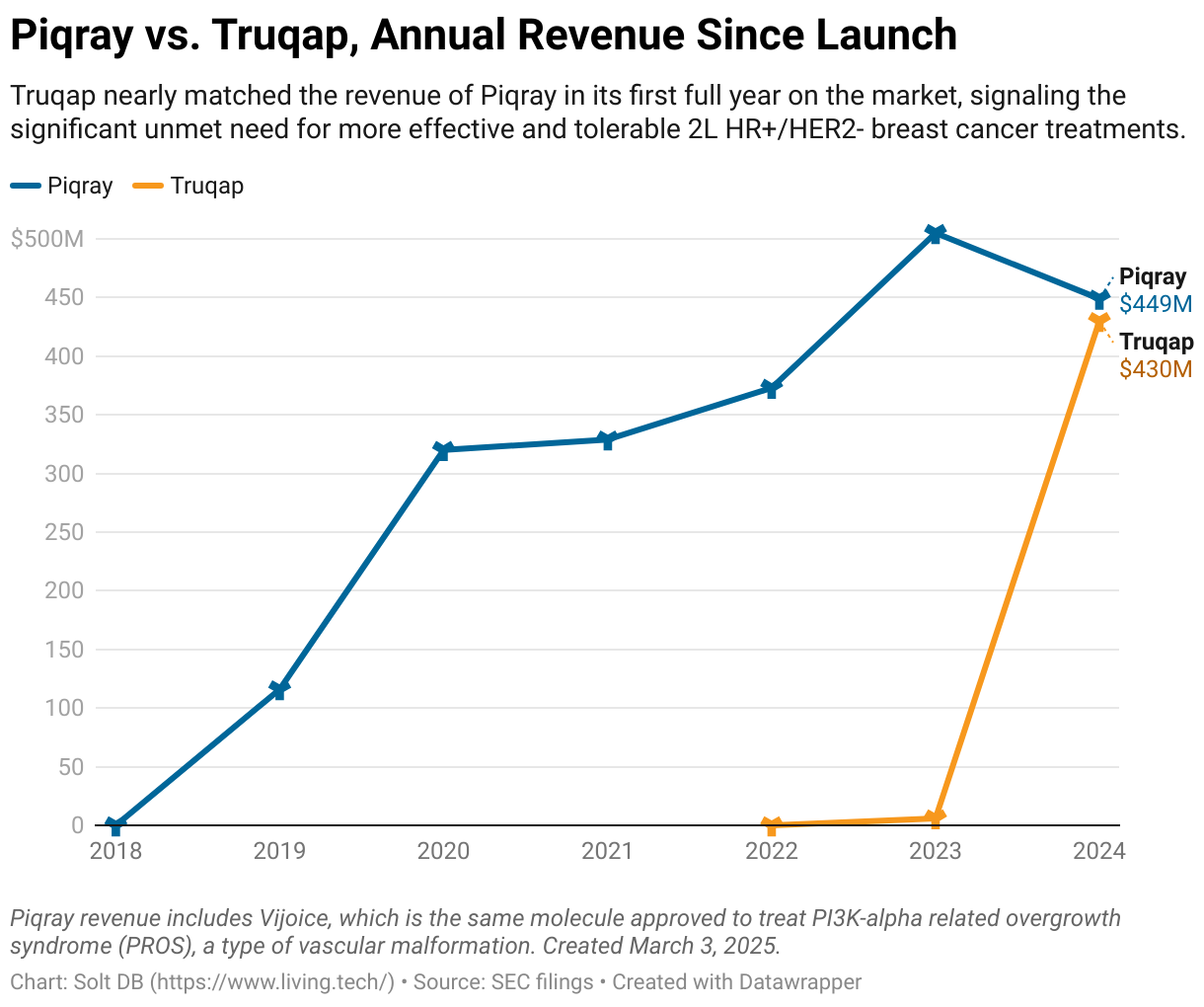

Truqap has enjoyed a flawless commercial launch. AstraZeneca reported full-year 2024 revenue of $430 million, an impressive haul for its first full year on the market. The product's immediate domination of the 2L setting has derailed the blockbuster trajectory of the former market leader, Piqray from Novartis, which was the first PI3K inhibitor to earn regulatory approval.

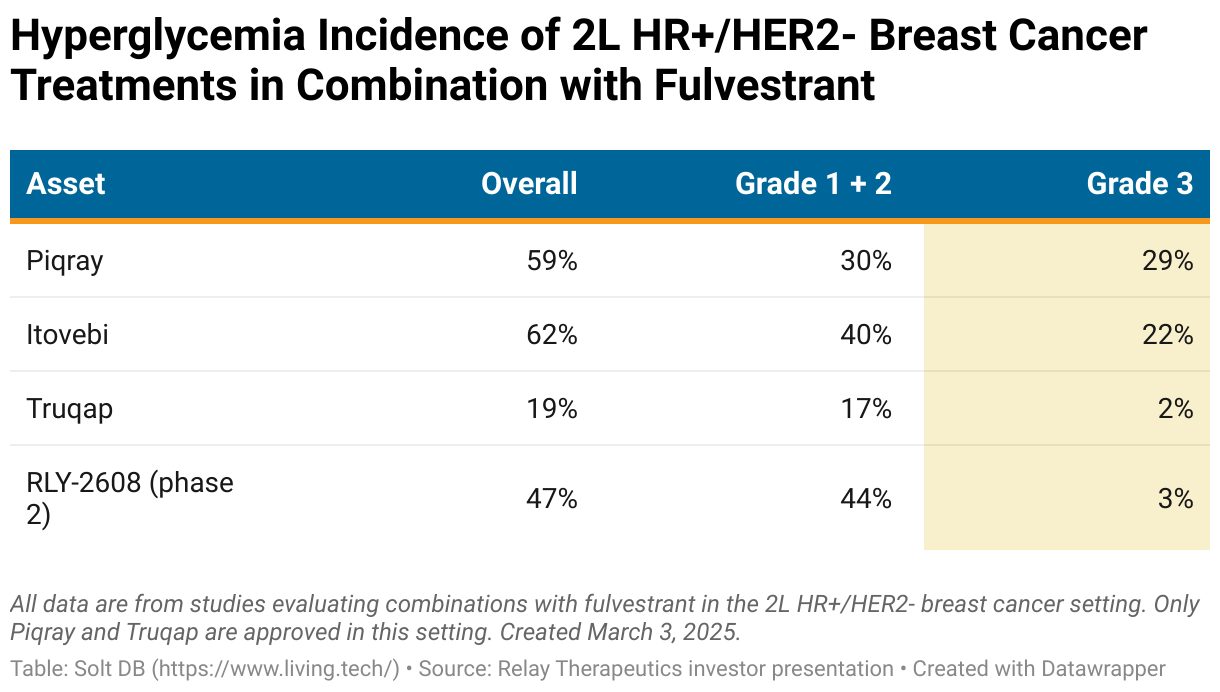

Commercial success in this specific indication is driven by avoiding grade 3 hyperglycemia. Grade 1 and grade 2 hyperglycemia can be managed by oncologists and usually only require observation. More serious occurrences require an endocrinologist to get involved.

As an AKT inhibitor, Truqap interferes with oncogenic mutations in the PTEN/PI3K/AKT pathway without directly inhibiting PI3K-alpha, which results in much lower rates of hyperglycemia compared to the competitive landscape.

In its own pivotal study, Truqap plus fulvestrant reported an overall hyperglycemia rate of 19%. Only 2% qualified as grade 3 events. That's much lower than non-selective PI3K inhibitors Piqray (59% overall, 29% grade 3) and Itovebi (62% overall, 22% grade 3).

It's also lower than the 600 mg, twice-daily fasted dose of RLY-2608, although both have very low rates of severe hyperglycemia (47% overall, 3% grade 3). Investors should expect the 400 mg, twice-daily fed dose in ReDiscover-2 to have similar rates of hyperglycemia.

A favorable study design, low rates of grade 3 hyperglycemia, and a significant unmet need all bode well for Relay Therapeutics. The most difficult part for investors will be the wait.

A significantly higher mPFS than the competitive landscape would allow patients to remain on treatment for longer, which would result in compounding revenue over multiple years. The asset could become a blockbuster (>$1 billion) by its third year on the market, which is an uncommon trajectory matched only by some of the world's bestselling drugs including Humira, Keytruda, and Eliquis.

If RLY-2608 achieves a similar level of sales in its first full year on the market as Truqap, then Relay Therapeutics will earn a valuation greater than $5 billion based on the asset alone. There aren't many opportunities to achieve investing outcomes like this in a short five- to six-year period – and they're rarely so well-timed with market downturns, allowing even more attractive entry points.

Around the Horn

Precommercial drug developers cannot be evaluated using typical financial metrics like revenue, cash flow, and income. Investors should still pay attention to certain line items and trends within financial statements.

Relay Therapeutics ended 2024 with $781 million in cash, which can fund the current operating plan into the second half of 2027. Management is prepared to go all-in completing the pivotal study of RLY-2608 even if it means pausing all other programs.

That might not be the most encouraging way to look at things, but the first potential approval for RLY-2608 in 2L HR+/HER2- breast cancer could make Relay Therapeutics a $5 billion company by the end of the decade. It's a rare opportunity that makes sense to protect – and management is treating it accordingly.

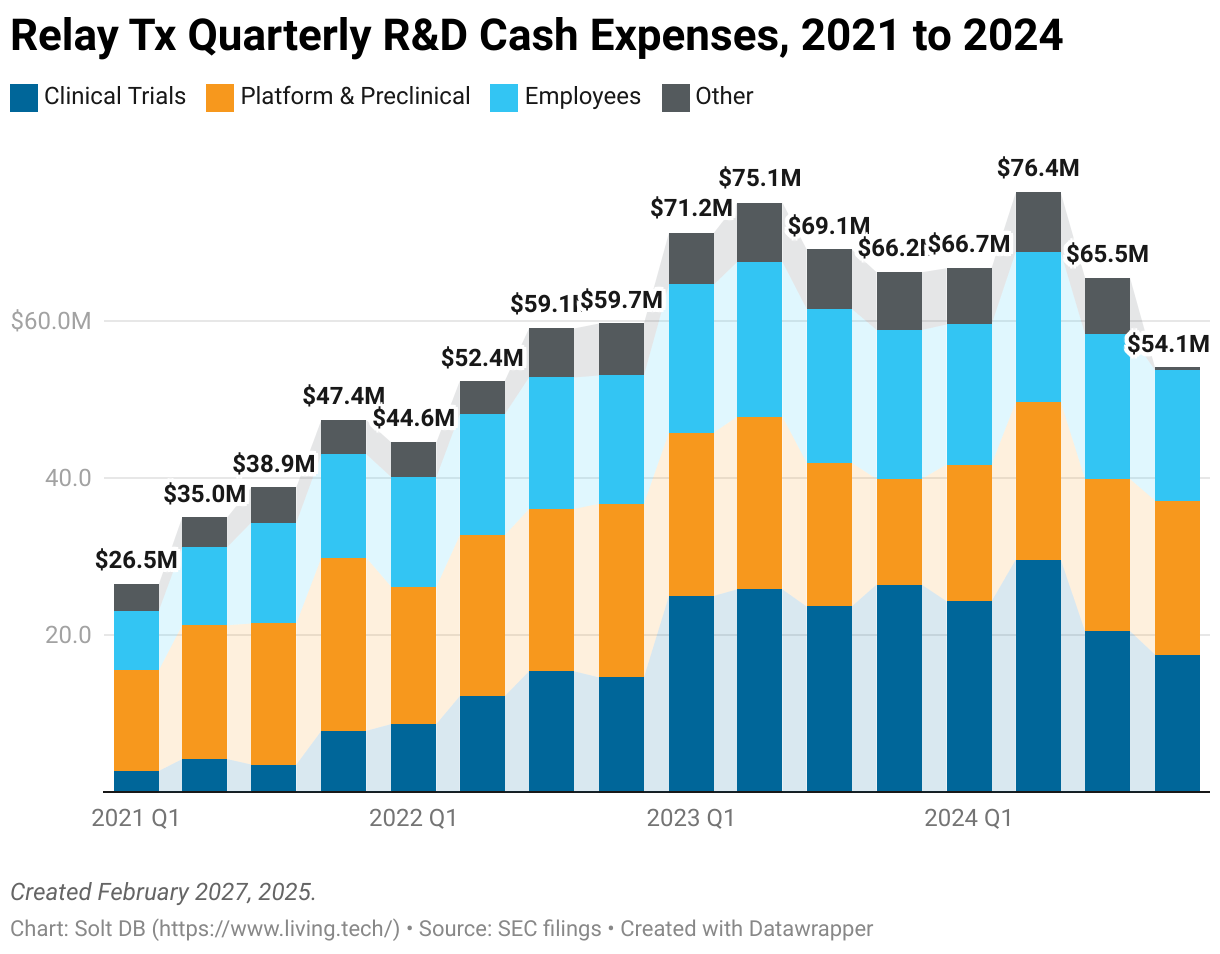

The precision medicine company reported just $54.1 million in R&D cash expenses in Q4 2024, which marked the lowest since Q2 2022. Licensing lirafugratinib has reduced clinical trial expenses. Meanwhile, the business counted 261 employees at the end of 2024, or roughly 20% lower than each of the previous two years.

Investors should be encouraged by the fiscal restraint of management. Investors should also acknowledge that clinical trial expenses will increase when the new NRAS inhibitor program and Fabry disease program transition out of preclinical development. The company can delay clinical starts for these assets to mitigate increases in clinical trial expenses, if needed.

Vascular malformations study to begin in March 2025

Relay Therapeutics is on track to begin a phase 1 clinical trial in vascular malformations by the end of Q1 2025. Initial development programs will use RLY-2608 as a proof of concept, but a distinct molecule may be swapped in for pivotal studies.

Unlike breast cancer, vascular malformations require longer-term and potentially lifelong maintenance treatment. Therefore, it could make sense to design a molecule that has once-daily dosing, is amenable to liquid formulations, or has fewer side effects.

NRAS program is now RLY-8161

The company has chosen a development candidate for the NRAS program. While PI3K-alpha in breast cancer makes nearly every other indication seem small in comparison, RLY-8161 represents a meaningful market opportunity with an estimated 28,000 patients per year.

Lirafugratinib licensing terms

Relay Therapeutics received $5 million upfront from Elevar Therapeutics for licensing rights to FGFR2 inhibitor lirafugratinib, according to the company's annual report. It's eligible to receive $495 million in regulatory and commercial milestone payments, including $70 million in regulatory milestones, and double-digit royalties on sales.

Elevar Therapeutics is responsible for conducting a pivotal study for the tumor-agnostic setting, which represents 96% of the total patient population.

Will a new agreement be reached with D.E. Shaw Research?

The Anton supercomputer architecture is a crucial piece of technology enabling motion-based drug development (MBDD) and the overall Dynamo platform. But the original research agreement with the supercomputer's creator, D.E. Shaw Research, expires in August 2025. Considering there's no way to replace Anton at the moment, investors should closely watch what happens next.

It's important to understand what an expiring research agreement means and doesn't mean.

- Relay Therapeutics maintains exclusive rights to targets (such as PI3K-alpha) so long as molecules remain in active development or commercialization. No other company can leverage Anton to discover PI3K-alpha inhibitors, ER-alpha degraders, alpha-Gal chaperones, and so on.

- Investors don't want the R&D engine to seize up, but the investment thesis would survive. If RLY-2608 earns an approval in just kinase-mutated 2L HR+/HER2- breast cancer and enjoys a smooth launch, then the company could be valued at $5 billion. If the asset is successfully developed and commercialized across all settings, then Relay Therapeutics would be valued in the tens of billions of dollars – making it one of the largest 40 drug developers on the planet.

- Relay Therapeutics has disclosed one preclinical program might not make sufficient progress by the August 2025 expiration, essentially axing the program.

- In a worst-case scenario, Relay Therapeutics might not be able to discover new molecules without redesigning internal workflows. It might be "stuck" with the existing pipeline and four unnamed preclinical assets.

Relay Therapeutics cannot replace Anton quickly or easily. What options are on the table?

Forging a new collaboration agreement with D.E. Shaw Research is the least disruptive path forward. An alternative "program-by-program" agreement is also a possibility, such that the drug developer pays for services as a customer rather than a partner.

Barring that, the precision medicine company might be able to purchase time on the Anton 2 parked at the Pittsburgh Supercomputing Center. It's the only publicly known machine not directly under the control of D.E. Shaw Research.

Given the euphoria for all things related to AI, a window might exist to find an investment partner and build an Anton machine in house – if D.E. Shaw Research allows it.

If Relay Therapeutics cannot get access to an Anton machine, then it will need to recalibrate. It does have exploratory collaborations with industry and academic researchers, but admits they cannot replace its prized computational tool.

Anton uses application-specific integrated circuits (ASICs), which enable the greatest floating-point precision for molecular dynamics simulations. Anton 2 and Anton 3 machines can simulate 164x and 406x longer timescales per day, respectively, than the highest-performance graphics processing units (GPUs). In other words, cozying up to NVIDIA wouldn't help much. It would actually extend drug discovery time by years.

There's a third supercomputer architecture possibility based on field-programmable gate arrays (FPGA), which, unlike ASICs, can be reconfigured once built. This might make the most sense for an in-house machine, but the drug developer isn't exactly equipped to build one from scratch by itself.

Margin of Safety & Allocation

Relay Therapeutics is considered a Growth (Quality) position. The current fair valuation for the company based on my 2025 model is below:

- Market close March 3: $3.21 per share

- Modeled Fair Valuation: $16.75 per share

- Allocation Range: Up to 15%

Relay Therapeutics reported 169.522 million shares outstanding as of February 21, 2025. The modeled fair valuation above assumes 177.998 million shares outstanding, which is equivalent to 5% dilution.

Further Reading

- February 2025 press release announcing Q4 2024 operating results

- February 2025 regulatory filing (10-K) detailing 2024 operating results

- December 2024 research note analyzing potential to form global breast cancer partnership

- December 2024 press release announcing updated interim phase 2 results for RLY-2608 plus fulvestrant

- December 2024 press release announcing the licensing agreement with Elevar Therapeutics

- May 2023 pivotal study results for Truqap plus fulvestrant

.svg)

-cropped.svg)