.svg)

Hours before Coherus BioSciences announced full-year 2024 operating results, Checkpoint Therapeutics was acquired by India's Sun Pharma for $355 million. The timing couldn't have been better.

The immuno-oncology peer adopted an identical strategy to Coherus: earn approval for a PD-1 drug product, then develop a pipeline of potential combinations to grow revenue potential. Both PD-1 assets were initially approved in niche indications with no immuno-oncology competition and have peak annual sales potential of up to $200 million.

There are some notable differences.

The peer's Unloxcyt was approved in January 2025. By comparison, Loqtorzi should generate roughly $60 million in revenue this year. Coherus has one pipeline asset in phase 2 evaluation (casdozo) and another in phase 1 (CHS-114), whereas Checkpoint only has a single pipeline asset in the clinic. Coherus also ended 2024 with $125 million in cash, while Checkpoint exited the year with less than $10 million.

Sun Pharma's acquisition will pay $355 million upfront and up to $60 million in additional milestones, which could bring the total acquisition price tag to $415 million. Coherus sported a valuation of $106 million as of market close March 17. If the company had a $415 million market cap, then it would be trading at $3.60 per share – 290% higher than the most recent close.

The acquisition of Checkpoint Therapeutics highlights Coherus BioSciences' undervaluation from a persuasive arbitrator: the market. It likely explains why CEO Denny Lanfear made a rare comment about being unhappy with the share price at the beginning of the earnings conference call. He's not wrong, but subjecting analysts and investors to yet another strategic pivot hasn't helped the company's case.

Coherus could gradually earn respect – and a higher valuation – as the dust settles from the now-approved divestment of Udenyca. The transaction will allow the drug developer to remove all debt from its balance sheet and boost its cash runway through the end of 2026. The company simply needs to execute with the ramp of Loqtorzi this year and properly communicate the value of the pipeline ahead of data readouts next year.

By the numbers

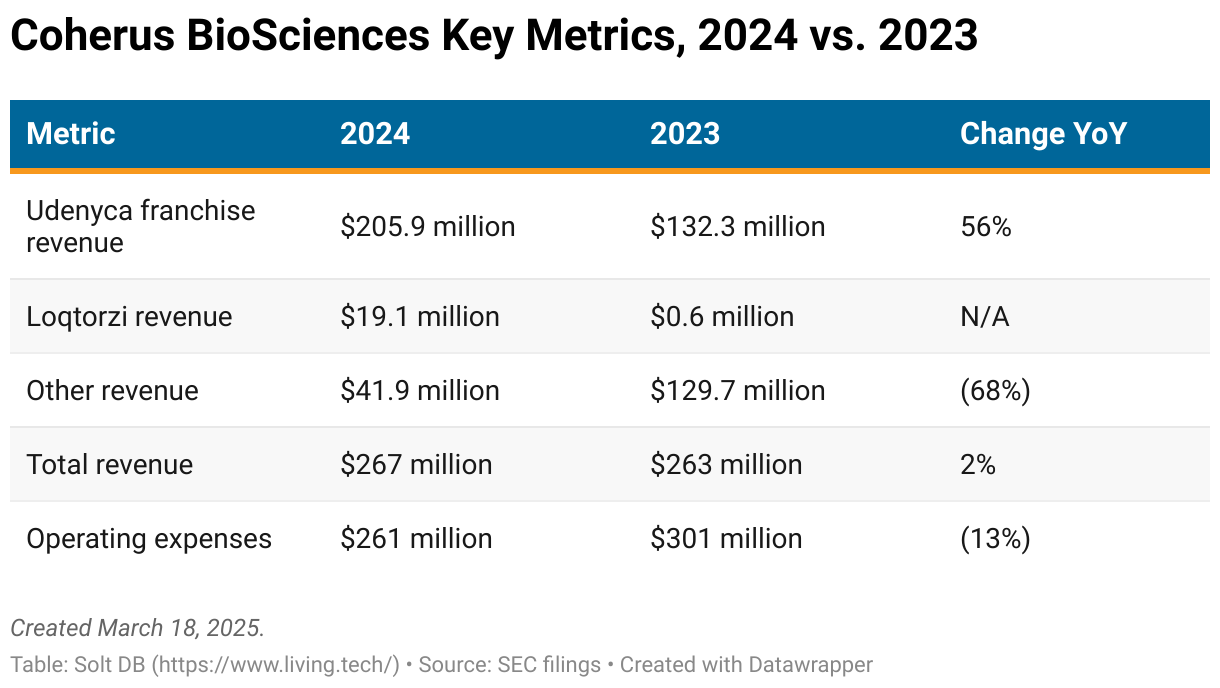

Despite a supply disruption in Q4 2024, the Udenyca franchise generated $46.3 million in quarterly revenue. Management reported that over 95% of prescribers returned to the brand once supply returned. The others simply may not have had new patients yet.

The decision to expedite shipping immediately after the resolution of the supply disruption proved expensive. The cost of goods sold (including Loqtorzi) jumped 64% to $33.9 million, up from $20.7 million in Q3 2024, even though Udenyca revenue declined 30% in that span.

The Udenyca franchise will make contributions through the end of Q1 2025, which will offer one more quarter of relief before cash burn picks up.

The now-lead asset Loqtorzi generated $7.5 million in revenue during the final period of 2024, equivalent to an annualized exit rate of $30 million. Quarterly sales will need to increase 5x to reach their peak potential in nasopharyngeal carcinoma (NPC).

A post-Udenyca business will have the upside of easier to follow income statements, as asset sales throughout 2024 clouded the ability to get a clear assessment of the business.

For the full year, Coherus reported net income of $28.5 million and an operating cash burn of $20.4 million. Both were driven by asset sales and will quickly reverse.

Management projects a cash position of roughly $250 million after the transaction closes, which should provide a runway into mid-2027. That's long enough to get through three important data readouts from the internal pipeline and additional interim data readouts from Junshi Biosciences.

Around the Horn

Once the dust settles from the Udenyca asset sale, investors will need to refocus on the commercial ramp of Loqtorzi and updates from the pipeline.

Udenyca asset divestment

On March 11, Coherus shareholders approved the sale of the Udenyca franchise to Intas Pharmaceuticals for up to $558.4 million, including:

- $365 million for intellectual property and trademarks

- $118.4 million for inventory, subject to adjustments upon transfer

- $37.5 million if Udenyca achieves cumulative revenue of $300 million from Q2 2025 through Q1 2026 (four full consecutive quarters), or Q3 2025 through Q2 2026 (four full consecutive quarters)

- $37.5 million if Udenyca achieves cumulative revenue of $350 million in any four consecutive quarters through the end of Q4 2026

How likely is it to earn the sales milestones payouts? Udenyca would need to average quarterly revenue of $75 million to achieve the first milestone and $87.5 million to achieve the second. The franchise generated $66 million in revenue during its last uninterrupted period, which included a still-ramping Udenyca Onbody.

But it's a little complicated. Some of the former sales team will transfer to Intas Pharmaceuticals and continue selling Udenyca. The rest will remain with Coherus to drive the ramp of Loqtorzi. It's also important to acknowledge that for all its flaws, the core competency of Coherus' management team is commercial strategy and execution.

Therefore, it's possible the commercial trajectory of Udenyca changes immediately after the divestment, and possibly permanently. Hopefully the advantages of Udenyca Onbody make it difficult to screw up sales growth.

Can Loqtorzi's ramp accelerate?

My current model expects Loqtorzi to reach peak annual sales of roughly $150 million by Q4 2027. Favorable updates to National Comprehensive Cancer Network (NCCN) guidelines could bring that up a quarter or two.

The cumulative effect of an accelerated trajectory could save up to one quarter of cash burn between Q2 2025 and achieving the peak sales milestone in 2027 – not much, but cash will be a premium asset in the next few years.

The NCCN first included Loqtorzi in guidelines as one of the preferred options for first-line treatment of advanced nasopharyngeal carcinoma (NPC). That left wiggle room for off-label use of other PD-1 inhibitors that aren't formally approved in this indication, which gobbled up an estimate one in four prescriptions.

Not anymore. In November 2025, the NCCN revised its guidelines, making Loqtorzi the only preferred option for first-line NPC. It also added that Loqtorzi is now the only preferred option for all subsequent lines of treatment.

Coherus has to do the legwork of educating physicians in both academic and community settings of recent changes, but a combination of strong data and newly unambiguous NCCN guidelines make a pretty persuasive argument.

Expected pipeline data readouts

Coherus BioSciences expects three important data readouts in the first half of 2026. That includes combination study data readouts for casdozo in hepatocellular carcinoma (HCC, a type of liver cancer), and CHS-114 in both head and neck cancer (HNSCC) and gastric cancer (stomach cancer).

When asked about the ability to forecast data readout dates relatively far out, management explained the studies are being conducted by an experienced contract research organization (CRO) that Coherus has tapped before. Nonetheless, investors shouldn't be surprised if the actual data readouts occur in Q3 or even Q4 2026.

Adverse opinion from accounting firm

The annual report filed with the U.S. Securities and Exchange Commission (SEC) contains an adverse opinion from the accounting firm that completed the audit. That means the accounting firm wants to draw attention to a deficiency and save its ass in case things go off the rails.

Adverse opinions issued for financial statements can kill companies. Luckily, that's not the case here. The accounting firm's statement reads:

In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Company at December 31, 2024 and 2023, and the results of its operations and its cash flows for each of the three years in the period ended December 31, 2024, in conformity with U.S. generally accepted accounting principles.

However, accountants struggled to confirm estimated rebates and chargebacks for drug products that were divested. These values are estimated when units of a product are sold, but must be adjusted as a product makes its way through distribution channels. These calculations were complicated by the asset sales of Cimerli and Yusimry in 2024, which made it trickier to estimate transaction values for products still in distribution channels.

The accounting firm issued its adverse opinion specifically relating to management's internal controls for these transactions. Essentially, it thinks management could have tracked and modeled these transactions better.

Forecast & Modeling Insights

(Revised.)

The updated 2025 model makes a downward revision to Loqtorzi revenue. The asset generated $7.5 million in Q4 2024 revenue, while I expected $8.5 million.

My model also accounts for slightly increased value for casdozo following the positive phase 2 study update from January 2024. The asset is more effective than I expected, which is great. Despite clearing its mid-stage study – where the overwhelming majority of drug candidates fail – I'm hesitant to value it accordingly, as Coherus is running another phase 2 study that swaps in Loqtorzi as the PD-1 inhibitor. I'll await the results from that study in 2026.

- Full-year 2025 net product revenue for Loqtorzi is now expected to be at least $60 million (vs. approximately $69 million previousy). That includes Q4 2025 revenue of $21.5 million representing an annualized exit rate of $86 million.

- I expect full-year 2026 net product revenue of roughly $120 million from Loqtorzi.

Investors will need to wait for the Udenyca asset sale to conclude before getting a better sense of steady-state operating expenses.

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Speculative) position. The current fair valuation for the company based on my 2025 model is below:

- Market close March 17: $0.91 per share

- Modeled Fair Valuation: $2.78 per share (vs. $2.51 per share previously)

- Allocation Range: Up to 10%

Coherus BioSciences reported 115.896 million shares outstanding as of February 28, 2025. The modeled fair valuation above assumes 121.692 million shares outstanding, which is equivalent to 5% dilution.

Further Reading

- March 2025 press release announcing 2024 operating results

- March 2025 regulatory filing (10-K) detailing 2024 operating results

- December 2024 research note analyzing the divestment of the Udenyca franchise

.svg)

.png)

.png)

-cropped.svg)