.svg)

Well, I never thought we'd get here.

Coherus BioSciences had a market cap of roughly $86 million as of market close on October 29. An estimated 30.2% of all shares available for trading (called the "float") were being shorted as of October 15. There are only 43 stocks with a higher short interest on the entire U.S. stock market. Only 10 of them are drug developers.

Among the group of pharma undesirables, Coherus had first-half 2024 revenue of $142 million – while the other nine had sales of $66.5 million combined. One company, Tarsus Pharmaceuticals, accounted for $65.5 million of that total. It has a market cap of $1.67 billion. I don't make the rules.

What Coherus really needs is a spark. That could come from a favorable weather report at this point. But another unlikely source could provide a boost soon: the competitive landscape.

More specifically, the rise of an overlooked immuno-oncology target called CCR8. Multiple global clinical trials have demonstrated that inhibiting CCR8 can significantly increase response rates to PD-1 inhibitors such as toripalimab. Of the 15 global drug developers developing a CCR8 asset, only four own an approved PD-1 inhibitor: Bristol Myers Squibb, Roche, BeiGene, and Coherus BioSciences.

The Role of CCR8 in Tumor Growth

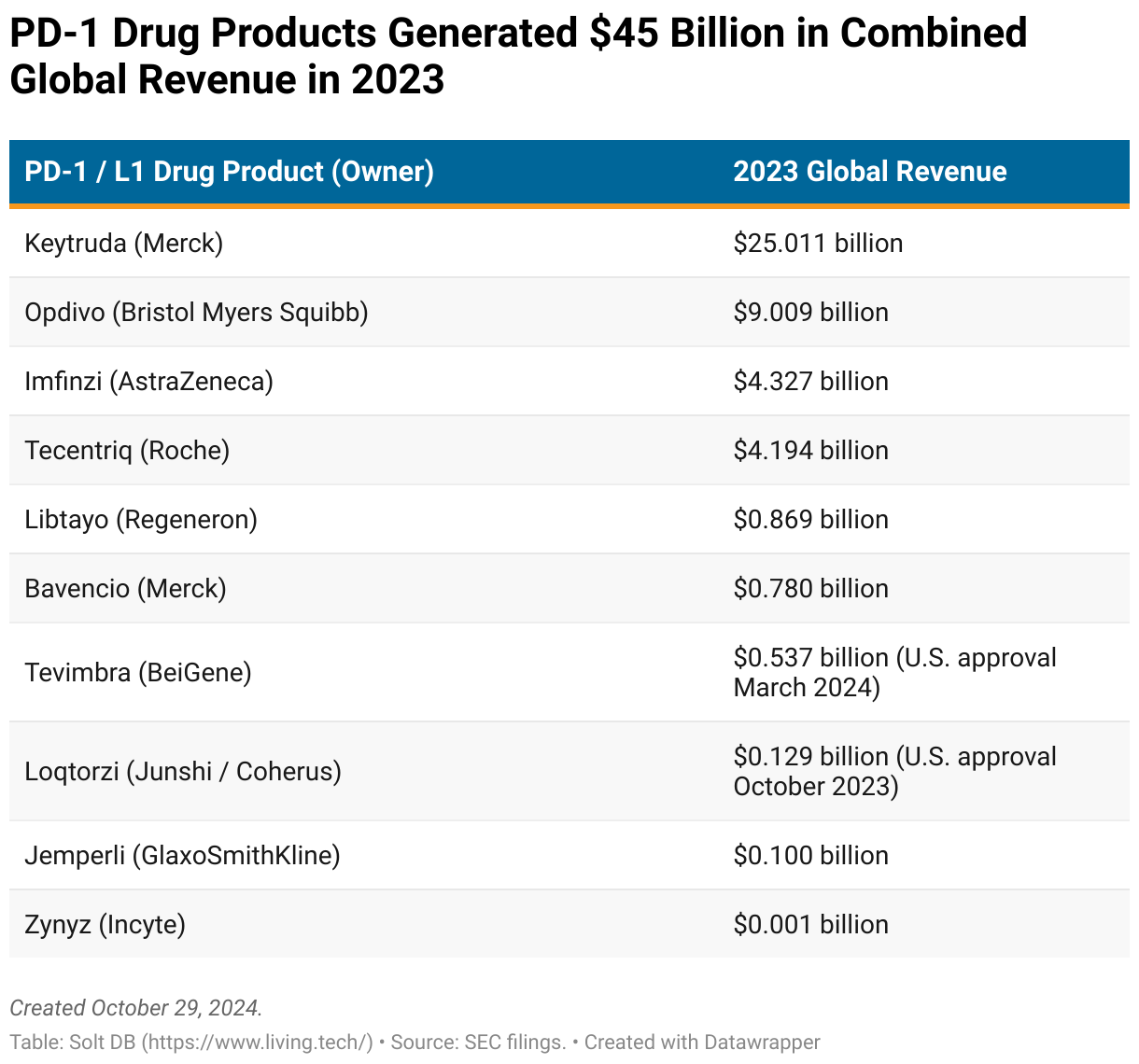

To understand the potential of CCR8 assets, it's important to first highlight the importance of PD-1 drug products.

Think of a tumor as a living fortress. It has plenty of ways to defend itself against invaders, which in this case is your own immune system. The good guys are storming the gates in this analogy.

One mechanism is to block immune cells right before they attack. The surface of tumor cells is dotted with PD-L1 receptors, which intercept T cells by binding to their PD-1 receptors, like a lock and key.

Drug products can block this interaction by binding to either the PD-L1 receptor on tumor cells or the PD-1 receptor on T cells. By doing so, they can play a foundational role in many solid tumor and even several liquid tumor cancers. In 2023, these drug products had combined revenue of nearly $45 billion – by far the most of any drug class in history.

Despite their value, PD-1 / L1 inhibitors have some drawbacks. They're generally not very effective when used alone (as a "monotherapy") and tumor cells gradually develop resistance. Oopsies. However, both primary drawbacks can be explained by the simple fact that blocking PD-1 / L1 interactions is a last line of defense. It occurs right before T cells attack a tumor cell.

So, why not thwart tumor cell defenses further from the fortress gates?

This is where new immuno-oncology targets come into play. One of the most promising is CCR8, which is expressed on regulatory T cells. These cells, called Tregs for short, have a calming effect on the immune system. There's an inverse relationship between Tregs and T cells. Meaning, a higher number of calming Tregs results in a lower number of attacking T cells.

Tumors cells take advantage by bribing Tregs. The currency here is a molecule called CCL1, which binds to CCR8 receptors on the surface of Tregs.

Tumor cells excrete CCL1 to attract Tregs into the vicinity of the fortress, called the tumor microenvironment (TME). Tregs get rich and, in turn, reduce the number of T cells that have a chance to get close to the fortress gates. That alone makes the PD-1 / L1 mechanism – the last line of defense for tumor cells – more effective. If fewer T cells sneak into the TME, then tumor cells have a higher chance of capturing them through receptor interactions.

This is why drug developers are interested in developing CCR8 inhibitors. If a drug product can block the interaction between CCL1 molecules and CCR8 receptors, then tumor cells won't be able to bribe Tregs as easily. If there are fewer Tregs in the TME, then more T cells will have the chance to storm the fortress gates – increasing the chances to overwhelm tumor cells.

Even better, why not create combination therapies by administering both PD-1 / L1 inhibitors and CCR8 inhibitors? Cancerous fortresses might not be so impenetrable after all.

How Might This Impact Coherus?

Coherus hasn't exactly stuck the landing for building an immuno-oncology pipeline that could be combined with toripalimab (Loqtorzi). On the one hand, it's still transitioning in-progress clinical trials designed by Surface Oncology to incorporate toripalimab. That'll take some time. On the other hand, a dwindling cash balance has a funny way of self-imposing additional speed limits.

But if other drug developers continue to demonstrate the promise of CCR8 assets with various developments between now and mid-2025, then Coherus could get a much-needed spark.

Investors should pay attention to two specific events in the competitive landscape: the phase 2 study design of LaNova Medicines (or its ability to sell its CCR8 asset) and data readouts from Bristol Myers Squibb.

LaNova Medicines is a Chinese drug developer with one of the more impressive and competitively positioned pipelines globally. That includes LM-108, which is the second-most advanced CCR8 inhibitor on the planet. The asset has already reported impressive data in combination with PD-1 inhibitors – primarily toripalimab.

- In a phase 1 study, a combination of LM-108 and toripalimab achieved an objective response rate (ORR) of 39% overall in patients with advanced gastric (stomach) cancer.

- For reference, Keytruda and chemotherapy achieved an ORR of 51% in its pivotal clinical trial as a first-line treatment (meaning patients being treated for gastric cancer for the first time).

- However, patients with high levels of CCR8 had a response rate of 56% when given LM-108 and toripalimab. Patients with tumors that grew resistant to prior PD-1 treatment had an ORR of 87.5%. This is the primary market opportunity for CCR8 combinations – the ability to "turn cold tumors hot."

- As a phase 1 study, dosing for LM-108 or toripalimab was not yet optimized. Similarly, patients with low levels of CCR8 expression were included in the study, but will be excluded from later clinical trials.

When LaNova Medicines raised $42 million (an impressive haul for a Chinese drug developer) in mid-October 2024, it announced plans to begin a phase 2 study of LM-108 in the United States before the end of the year.

What PD-1 inhibitor will it choose?

The company conducted a small U.S. study of LM-108 combined with Keytruda in the past, but toripalimab (Loqtorzi) hadn't earned approval yet. Will it choose toripalimab this time around? That would be a big boost for Coherus. Although the two are technically competing with CCR8 assets, any approved combination therapy that includes toripalimab will generate revenue for Coherus.

There are also some signs that LaNova Medicines might opt to sell the U.S. rights to LM-108. As one of the most advanced CCR8 assets, such a deal could provide a significant haul with >$100 million in upfront cash. That would spur interest in the entire competitive landscape, lifting Coherus. This would be a more favorable outcome than having toripalimab included in the phase 2 study design, especially since it could allow Coherus to sell or find a development partner for CHS-114 for its own large cash infusion.

The second event to watch is the next data readout(s) from Bristol Myers Squibb, which should begin trickling in during the first half of 2025. The pharma giant has the most advanced CCR8 asset globally, called BMS-986340, and is eager to combine it with its PD-1 inhibitor Opdivo, the 11th-bestselling drug product on the planet.

Large pharma companies are entirely different animals. They have dozens of drug candidates in development at any given time. This means they often only report progress or make a big fuss about late-stage assets that are closer to earning regulatory approvals. It's virtually unheard of to see a large pharma say much of anything about early-stage drug candidates.

Not so for BMS-986340. Bristol Myers Squibb dedicated individual slides in investor presentations for the asset as early as September 2023. It didn't even have phase 1 data at that point in time. For reference, the company has 55 individual molecules in its pipeline – and it still chose to highlight the CCR8 asset very early in development.

BMS-986340 is currently the second asset listed in the company's entire pipeline. It's ranked ahead of CAR-T cell therapies, antibody drug conjugates, KRAS inhibitors, PRMT5 inhibitors, and many other popular targets with more clout.

CCR8 is a big deal. You will hear about it in 2025.

In a somewhat helpful footnote for Coherus, CHS-114 has a very similar design to LM-108 and BMS-986340. It's optimized in the same way, specifically targeting Tregs in the tumor microenvironment (TME) and sparing Tregs further away from tumor cells. That increases the likelihood for impressive results from the competitive landscape to lift Coherus, either by driving excitement for its development or allowing the company to find a development partner.

Forecast & Modeling Insights

(No change.)

Forget my models for a second.

Wall Street expects Coherus to achieve roughly $300 million in full-year 2025 revenue. If it makes no improvement in gross margin compared to the first half of 2024, then it would generate $165 million in gross profit. If the business has cash operating expenses (excluding non-cash expenses like stock options for employees) of $260 million, then it would only burn about $55 million in cash throughout 2025.

That's not great, but the business could cut things reallllyyy close if needed and fund itself through the end of next year – buying time for commercial execution and pipeline development. This includes eating one additional quarter of cash burn from the Udenyca shortage encountered in Q4 2024.

In other words, although very uncomfortable, this is hardly a failing business to me. It's certainly worth more than $85 million. Does it need cash? Yes. Does it need to refinance its convertible debt by April 2026? Yes. But it has ways – some much better than others – to solve these problems without excessive dilution.

For transparency, the third-quarter 2024 model assumes:

- Total product revenue of roughly $64.124 million (vs. $58.472 million in Q2 or $54.706 million excluding Yusimry).

- Revenue includes $39.0 million for Udenyca PFS (vs. $38.952 million in Q2), $5.250 million for Udenyca AI (vs. $5.092 million in Q2), and $14.374 million for Udenyca Onbody (vs. $6.874 million in Q2).

- Revenue includes $5.500 million for Loqtorzi (vs. $3.789 million in Q2).

- Gross margin of 58.5% (vs. 56.3% in Q2). This includes no improvement for either brand compared to Q2. Rather, the cost of goods sold is expected to decline as one-time charges totaling $5.9 million roll off. Management expects gross margin to steadily improve, but I cannot reliably model it during the commercial ramp.

- Operating expenses of roughly $57 million (vs. $57.120 million in Q2).

- Operating income is expected to steadily improve through the end of 2025, albeit with operating margins remaining negative.

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Speculative) position. The current modeled fair valuation for the company based on my 2024 model is below:

- Market close October 29: $0.74 per share

- Modeled Fair Valuation: $8.72 per share

- Allocation Range: Up to 10%

Coherus BioSciences reported 115.208 million shares outstanding as of July 31, 2024. The modeled fair valuation above assumes 133.508 million shares outstanding, which is equivalent to 5% dilution.

Further Reading

- September 2024 research note preliminarily updating fair value to account for Udenyca shortage

- August 2024 research note analyzing Q2 2024 operating results

- August 2024 regulatory filing (10-Q) detailing Q2 2024 operating results

- June 2024 data readout (slide deck) for LM-108 plus PD-1 inhibitors at ASCO

.svg)

.svg)

.svg)

.svg)

.png)

.svg)

.png)

.svg)

.svg)

.svg)