.svg)

The rollercoaster of drug development and regulatory review for toripalimab is finally over. The rollercoaster of commercial development for Loqtorzi finally begins.

Coherus BioSciences and Junshi Biosciences announced an immuno-oncology collaboration in February 2021 and submitted their first biologics license application (BLA) for toripalimab in November 2021. But the fast start fizzled.

The pair received a dreaded complete response letter (CRL) from the U.S. Food and Drug Administration in May 2022, resubmitted the BLA in July 2022, and then were thwarted by COVID lockdowns in China that prohibited regulators from completing site inspections. Regulators finally made it to the manufacturing facility in May 2023 and completed clinical site inspections in August 2023, setting the stage for a long-awaited approval decision in October 2023.

Now branded as Loqtorzi in the United States, the asset is expected to become available in early 2024. The approval and upcoming commercial launch trigger various financial considerations, licensing opportunities, and value multipliers for in-house assets acquired from Surface Oncology.

Let's make sense of all the moving parts.

Revisiting Terms of the Junshi License

First, it helps to review the financial terms of the licensing agreement with Junshi Biosciences. Most of the original February 2021 terms remain in place, although key aspects were adjusted in 2022.

Here's where things stand as of November 2023.

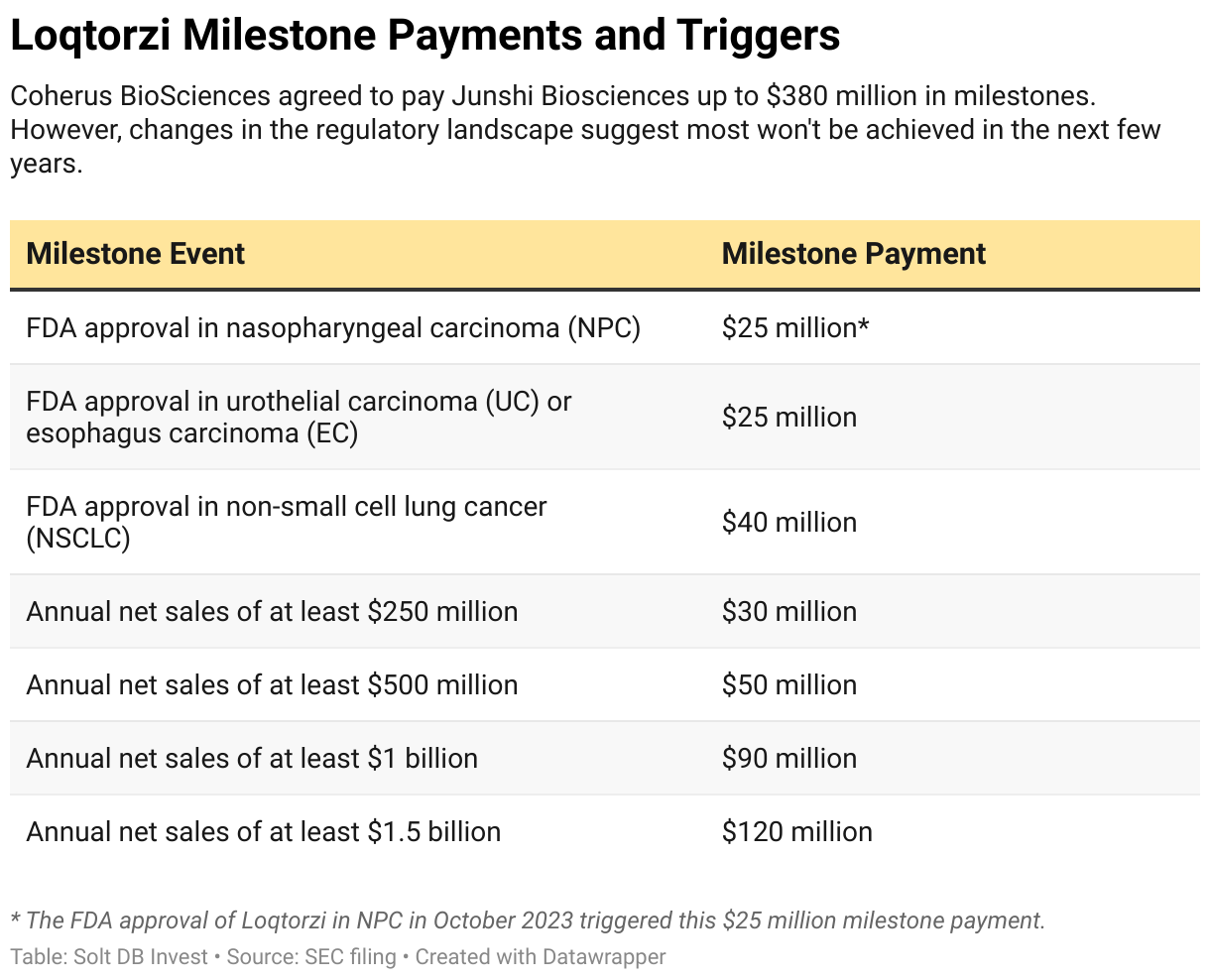

- Coherus BioSciences paid a $150 million upfront milestone payment for exclusive U.S. and Canada rights to toripalimab.

- Coherus BioSciences will pay a 20% royalty on net sales of Loqtorzi and up to $380 million in one-time payments for various milestones, including up to $290 million for sales-based milestones.

The U.S. Food and Drug Administration (FDA) approval of Loqtorzi in NPC triggers a $25 million milestone payment to Junshi Biosciences. The remaining milestone payments have triggers that are unlikely to be met in the next few years, which should alleviate any concerns investors might have for cash flow challenges.

For example, the regulatory landscape has changed. Loqtorzi is no longer attempting to earn FDA approval in urothelial carcinoma, esophagus carcinoma, or non-small cell lung cancer as a monotherapy. Combination studies now underway with novel assets either exclude these indications or are in earlier development.

As for achieving the up to $290 million in sales-based milestones, Loqtorzi has peak annual sales potential of only $100 million to $200 million in NPC, which is below the first milestone threshold.

Once the product launches commercially in early 2024, Coherus BioSciences will be required to share 20% of net sales with its Chinese partner -- the primary impact of the licensing agreement for the foreseeable future.

What's Next for Loqtorzi?

The opportunities and challenges for Loqtorzi can be grouped into three categories:

- Launch and ramp

- Supplemental approvals

- Partnerships and external combinations

Launch and Ramp

Coherus BioSciences expects to launch Loqtorzi in NPC in early 2024.

The asset was broadly approved across all treatment settings, meaning it can be used as the first treatment a patient receives after being diagnosed (first line = 1L) or after other treatments (second line = 2L, or second-line plus = 2L+).

Generally speaking, the earlier the patient population a drug product can treat, the larger its revenue potential. Considering Loqtorzi is the first immunotherapy approved to treat NPC and the no-doubter data extending progression-free survival (PFS) and overall survival (OS), it's likely to become the standard of care for 1L NPC.

Coherus BioSciences expects Loqtorzi to reach its peak market potential in NPC within two to three years, which is blazingly fast. That's still sensible given the context. The company spent the last two years developing patient identification infrastructure while dealing with regulatory delays. Additionally, 65% of NPC patients are treated by oncologists who use Udenyca. These pre-existing relationships and account overlap create the potential for a fast launch and ramp.

Specifically in NPC, Loqtorzi has peak annual sales potential of $100 million to $200 million. The initial approval is a significant development, as it lays the groundwork for building commercial infrastructure for the asset. But supplemental approvals in new tumor types will be important for expanding the overall market opportunity.

Supplemental approvals

The primary revenue driver for a PD-LI asset is the potential to be combined with other drug products. For example, Merck's Keytruda has over 30 approvals -- the most of any oncology asset globally. That's expected to grow to 60 approvals in the next few years.

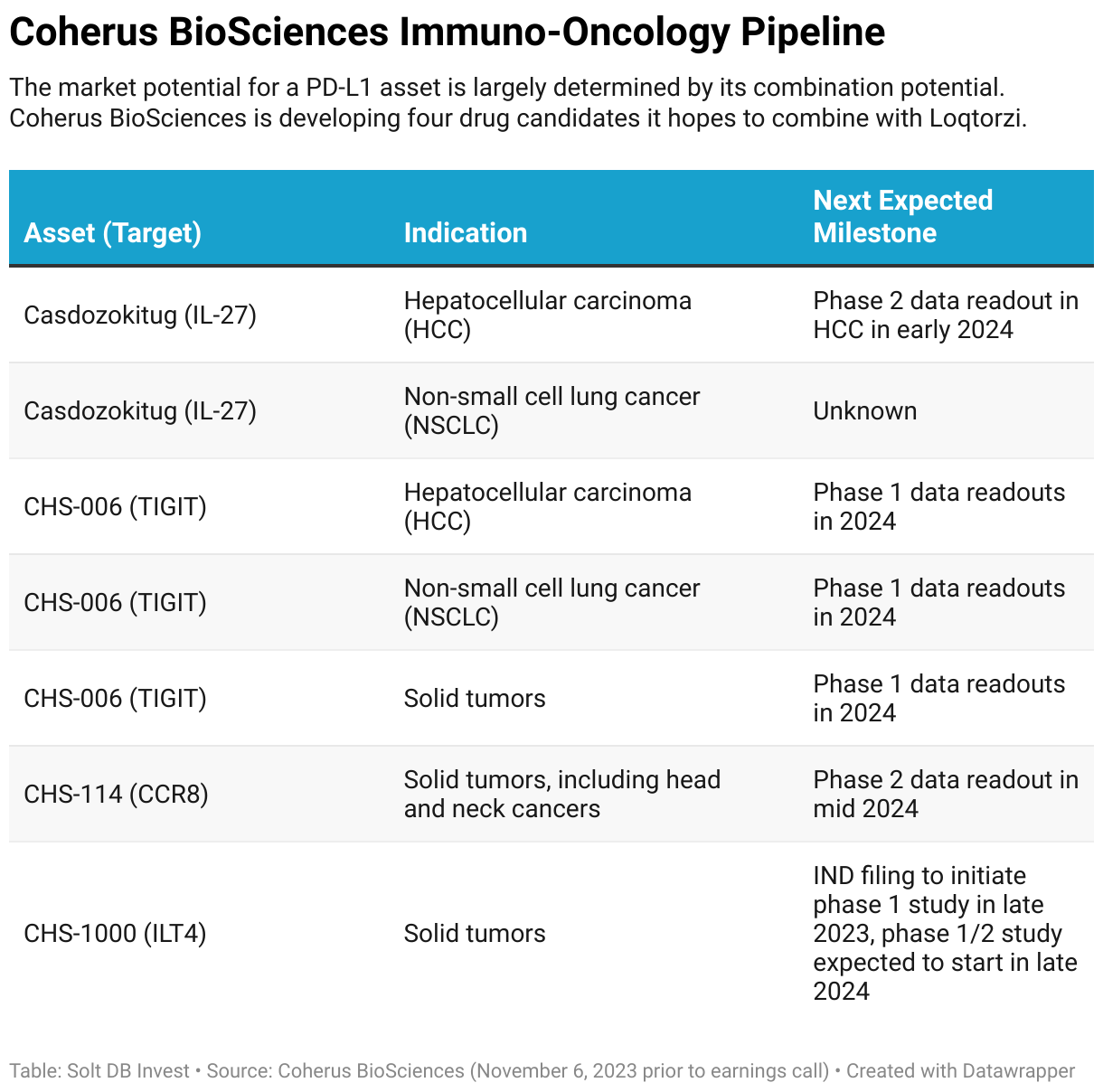

Initially, supplemental approvals are most likely to be sourced from internal assets already in clinical trials. Coherus BioSciences has four unique drug candidates it will explore in combination with Loqtorzi across at least seven different tumor types. Not all studies listed in the table are specifically evaluating combinations with Loqtorzi as of November 2023.

There's significant potential to expand Loqtorzi's reach beyond NPC. Junshi Biosciences has evaluated the asset in at least 17 unique tumor types.

However, the development and commercialization strategy in the United States has shifted. Coherus BioSciences is now interested in positioning Loqtorzi as a next-generation PD-L1 asset, not merely another competitor to Keytruda. That opens the opportunity to find external development partners.

Partnerships and external combinations

Coherus BioSciences is in discussions with multiple drug developers expressing interest evaluating their own immuno-oncology assets in combination with Loqtorzi. It's important to understand what that does and doesn't mean.

- Licenses to use Loqtorzi in external clinical trials might not have meaningful financial impact in the near term. Investors are used to exclusive licensing deals where a drug candidate's rights are sold. This is different. Coherus BioSciences might only supply Loqtorzi (for a fee) to partners, although it could carve out exclusive rights for specific tumor types and combinations. The latter would be more lucrative.

- The potential long-term financial impact could be more meaningful. If Loqtorzi is successfully positioned as a next-generation PD-L1 asset with activity in low PD-L1 tumors, then the company could enjoy multiple future approvals from partners. Investors should acknowledge the first such approvals, if any, won't occur until the second half of this decade.

Forecast & Modeling Insights

(No change.)

Solt DB Invest has modeled full-year 2024 revenue of $35 million for Loqtorzi, which is in line with management's most recent expectation to achieve peak annual sales in NPC within two to three years. We'll refine our model as more data and market insights become available in the first half of 2024.

In the meantime, the most significant news flow for Loqtorzi will pertain to data readouts across the immuno-oncology pipeline. Not all of these will initially evaluate combinations with Loqtorzi, but will set the stage for future expansion cohorts in existing studies and late-stage clinical trials for combinations.

Margin of Safety & Allocation

(Our 2024 model will be published after earnings on November 6, 2023.)

Coherus BioSciences is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2023 model is below:

- Market close November 3: $3.61 per share

- Modeled Fair Valuation: $13.31 per share

- Allocation Range: Up to 15%

Coherus BioSciences reported 110.476 million shares outstanding as of September 8, 2023. The modeled fair valuation above assumes 116.000 million shares outstanding, which is equivalent to 5% dilution.

Further Reading

- October 2023 press release announcing FDA approval of Loqtorzi in NPC

- August 2023 research note analyzing second-quarter 2023 operating results

- June 2023 research note analyzing the company's development and commercial strategy for toripalimab / Loqtorzi

- May 2023 research note analyzing first-quarter 2023 operating results

.svg)

.png)

.png)

-cropped.svg)