.svg)

The big print giveth, but the small print taketh away.

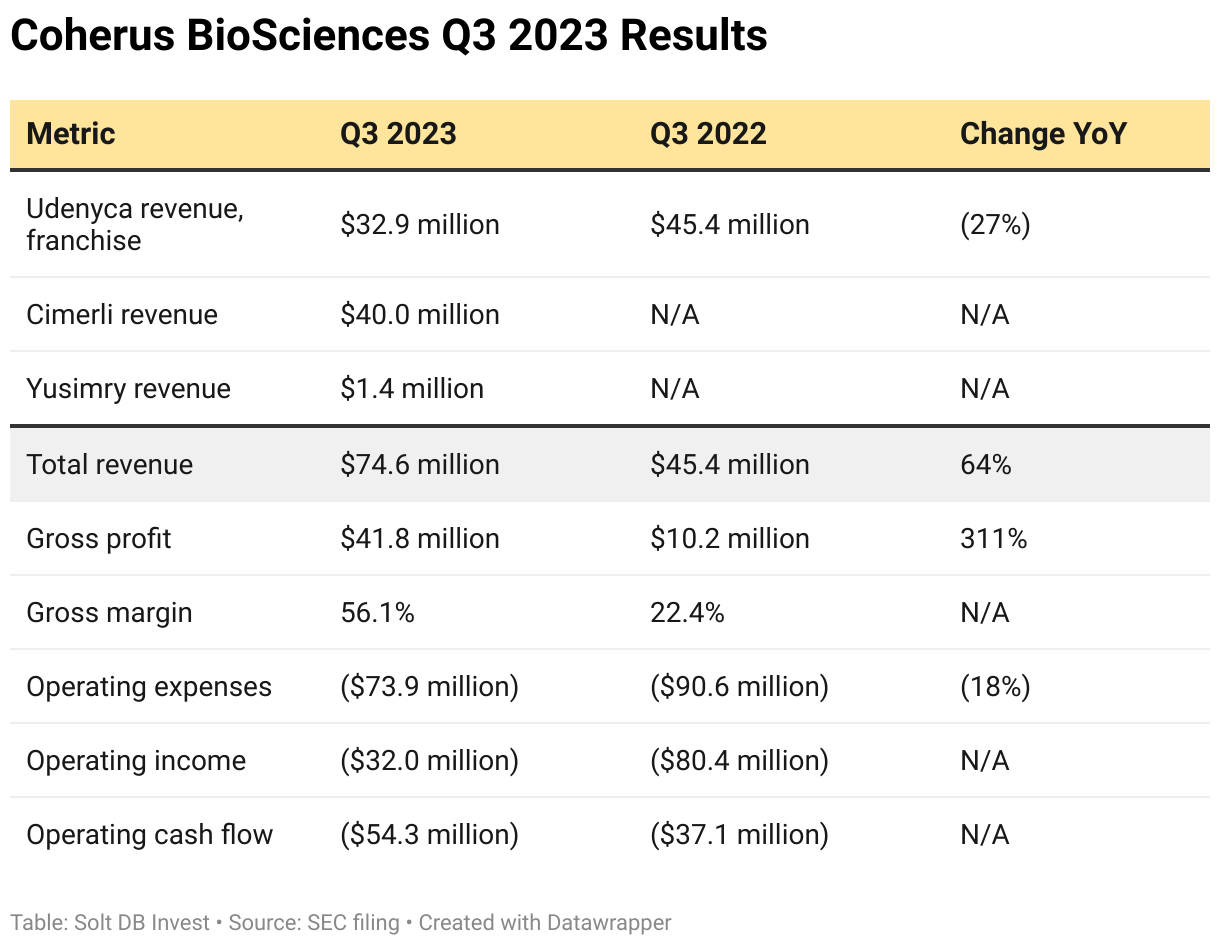

Wall Street analysts and individual investors were preparing for a blowout revenue print from Coherus BioSciences in the third quarter. Publicly-available information showed the Udenyca franchise grew pegfilgrastim market share from 12.2% at the end of the second quarter to at least 16% in late summer, which would represent the largest quarterly leap since the product launched years ago. Cimerli grew ranibizumab market share from 17% to at least 24% in the same period.

Surprisingly, the significant leaps in market share didn't translate into a similar leap in revenue. The primary culprit was a decline in average selling price (ASP) for the Udenyca franchise. Despite growing market share by 35% on a volume basis from the second to third quarter, revenue only increased by 4% in that span.

Shares of Coherus BioSciences tumbled on the unexpected mismatch between market share gains and revenue growth, which overshadowed progress across financial and commercial metrics.

By the Numbers

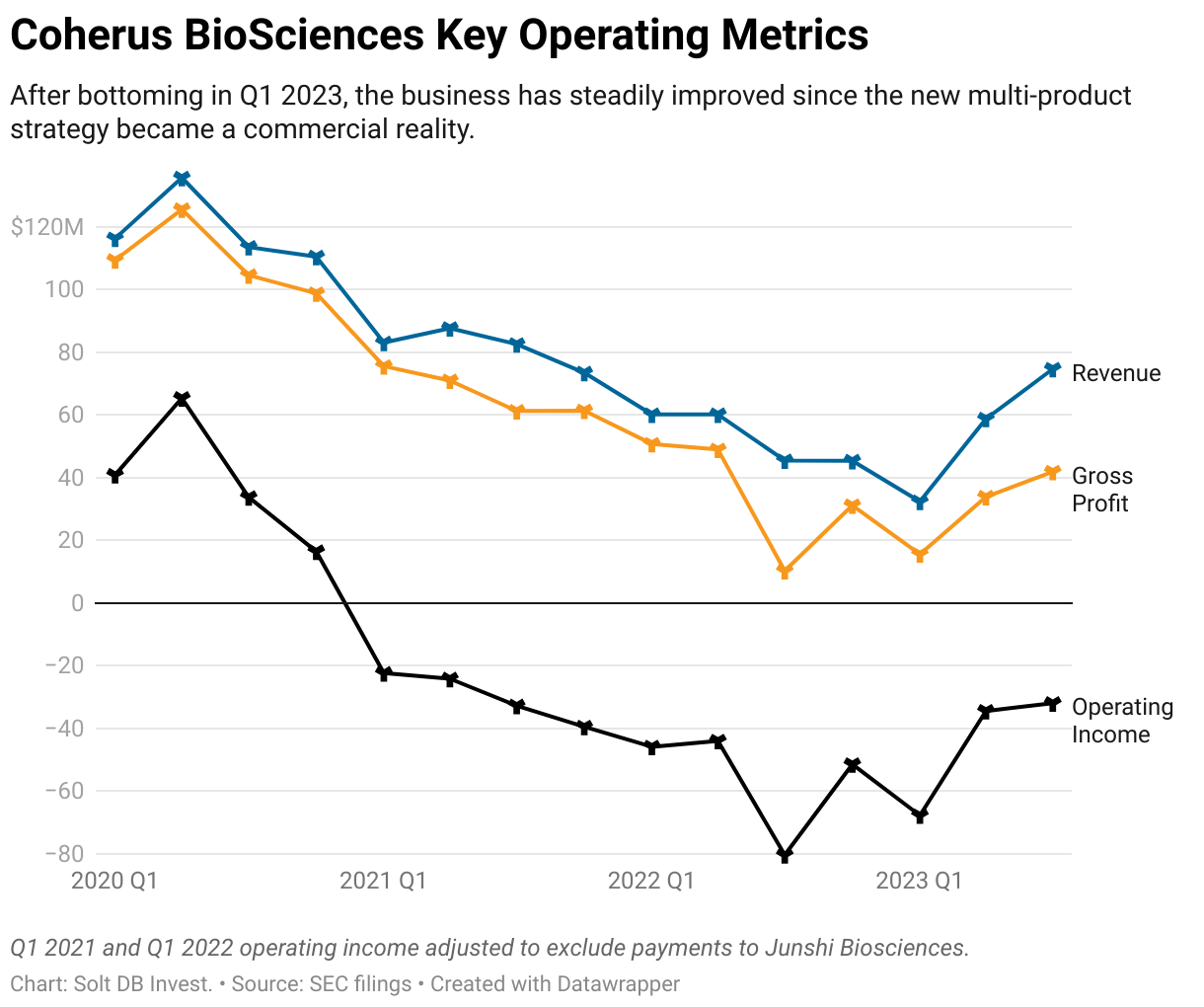

It might be difficult to tell by the share price, but aside from pegfilgrastim market dynamics that analysts including myself failed to accurately model, Coherus BioSciences turned in a solid performance during the third quarter of 2023.

The business generated the highest revenue since the third quarter of 2021, highest gross profit since the second quarter of 2022, and lowest operating loss since the second quarter of 2021. Recent progress coincides with the launch of a Q code for Cimerli in April 2023, simplifying billing for doctors, and the launch of an autoinjector (AI) formulation for Udenyca in May 2023.

How can investors measure success in the coming quarters? Management needs to control operating expenses while growing revenue. So far, so good.

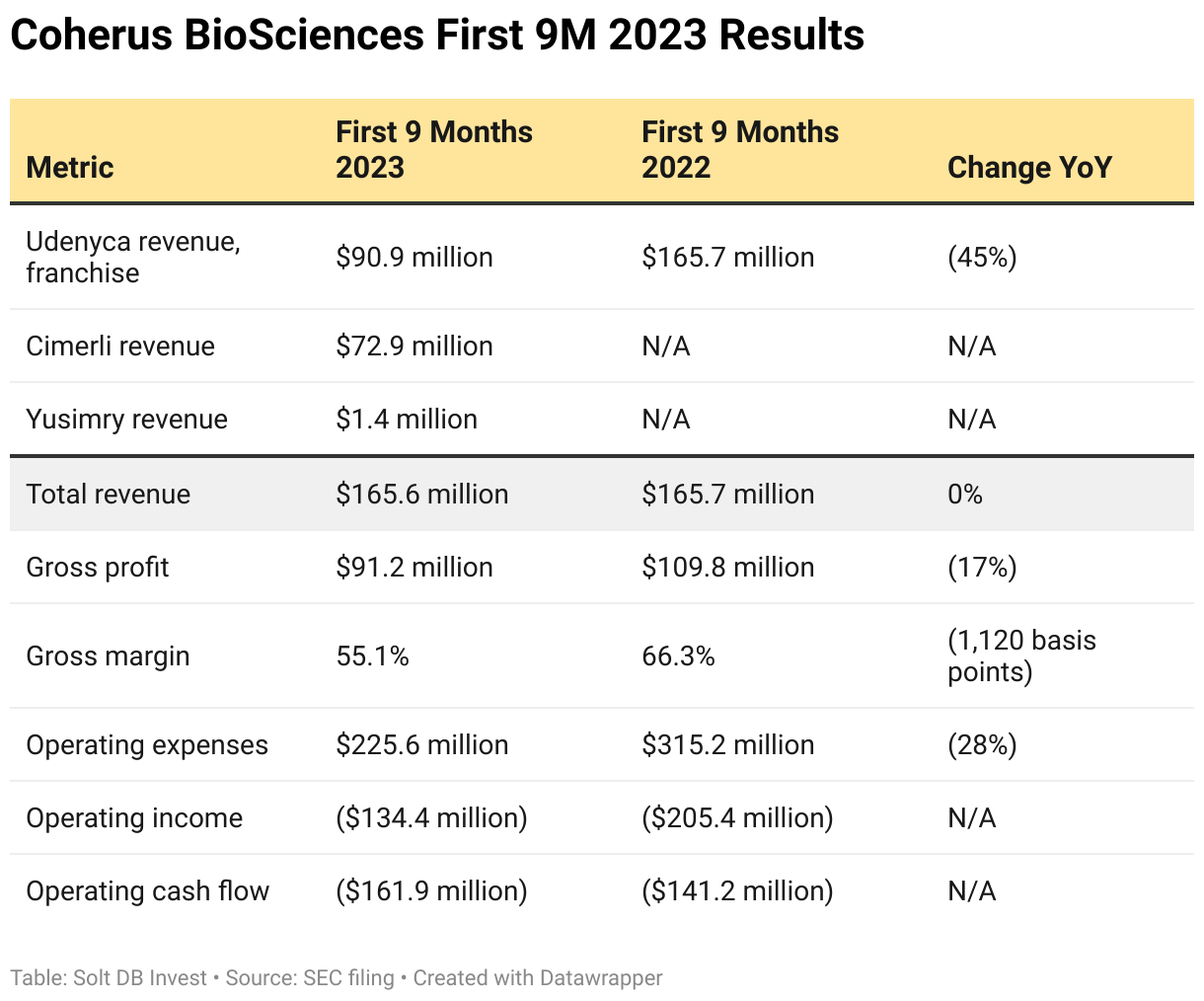

A multi-product strategy is both growing revenue back to historical levels and diversifying it. Diversification of the revenue mix introduces new wrinkles when interpreting financial results, as each product has a unique margin profile. For example, Cimerli is powering revenue growth in 2023, but half of gross profits are split with Bioeq. That drags down the overall gross margin for the company.

Comparing operating results through the first nine months of the last two years highlights the shifting revenue mix and potential to develop multiple, diverse growth drivers as new products launch.

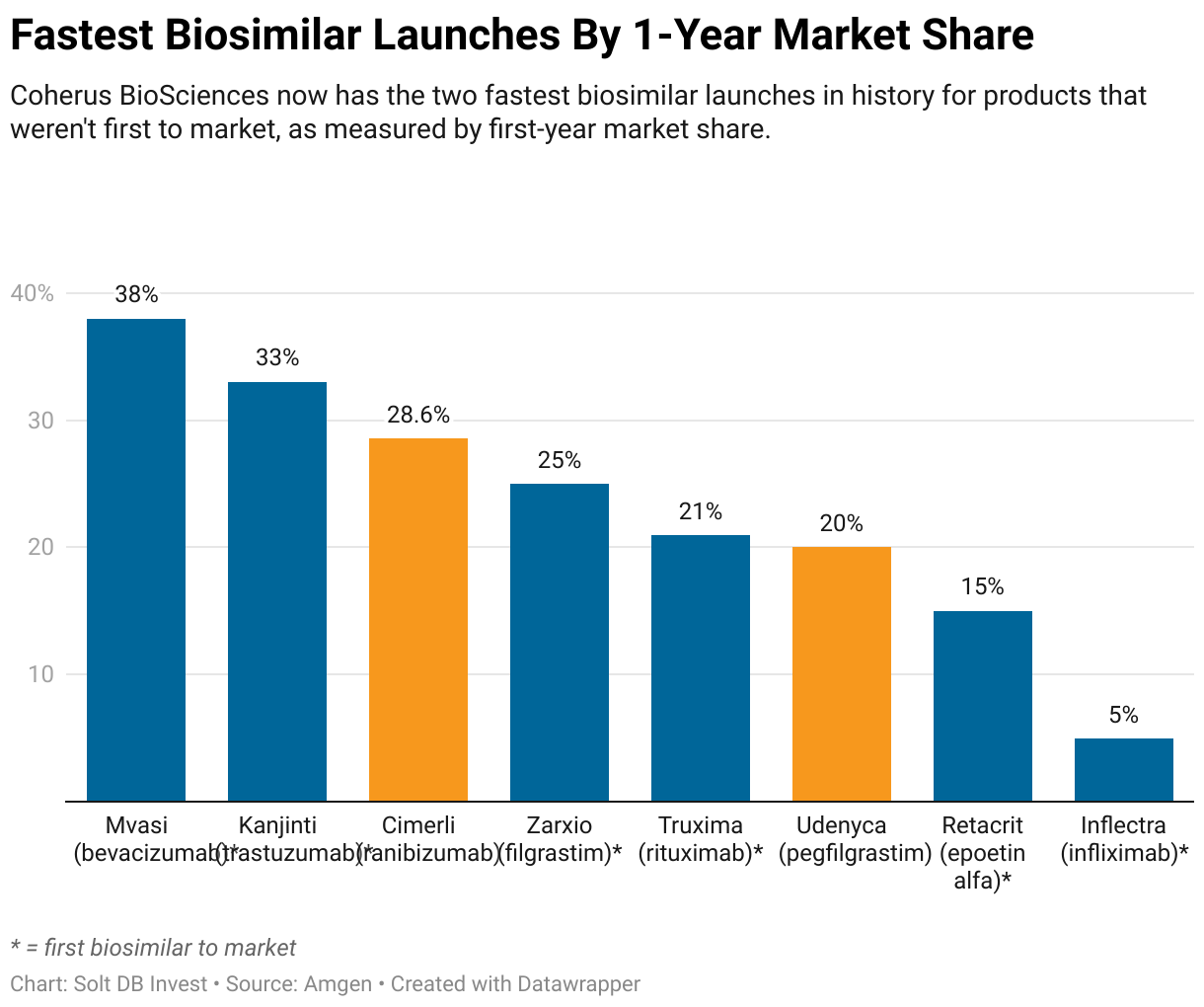

A positive financial trajectory is being driven by increasing market share for marketed products. The Udenyca franchise ended the third quarter with pegfilgrastim market share of 16.5%, marking the highest since the first quarter of 2021. Cimerli wrapped up the third quarter and its first full year on the market with ranibizumab market share of 28.6%. That marks the third-fastest rise for a biosimilar in history. It was the fastest-ever for a biosimilar that wasn't first to market.

The company will look to replicate its strong track record of commercial execution with the ramps of Udenyca AI, Loqtorzi, and (potentially) Udenyca OBI throughout 2024.

Financial Guidance (2023)

Coherus BioSciences reduced full-year 2023 revenue guidance and operating expense guidance.

- Prior guidance projected full-year 2023 revenue of at least $275 million and operating expenses (R&D, selling, general, and administrative) of $315 million to $335 million.

- New guidance projects full-year 2023 revenue of $250 million to $260 million and operating expenses of $300 million to $310 million.

Prior revenue guidance assumed Loqtorzi and Udenyca OBI would launch in late 2023, but regulatory delays pushed both product launches into early 2024. The reduced revenue guidance reflects a shift in revenue generation timelines, not a deterioration in business dynamics.

Portfolio and Pipeline Snapshot

Coherus BioSciences will have heavy news flow in 2024 as it seeks to increase market share for six product formulations and provide data readouts for novel immuno-oncology assets. The latter can add significant value in the first half of the year.

For example, consider the lead drug candidate casdozokitug ("Casdozo"). The asset is the most mature IL-27 inhibitor in the global pipeline. The first data readout will be from an ongoing phase 2 study evaluating a triple combination of Casdozo, a PD-L1 inhibitor, and a VEGF inhibitor in first-line (1L) hepatocellular carcinoma (HCC).

- Preliminary results from the triple combo in 1L HCC demonstrated an objective response rate (ORR) of 27%. That's better than the standard of care, Bayer's Nexavar, which boasts an ORR of 11% in the same treatment setting.

- The competitive landscape is shifting, however.

- A triple combination of a PD-L1 inhibitor, a VEGF inhibitor, and Nexavar achieved an ORR of 30% in 1L HCC, according to data published in summer 2022.

- The combination of a PD-L1 inhibitor and Nexavar achieved an ORR of 43% in 1L HCC, according to data presented at the 2023 International Liver Cancer Association Conference in September. The PD-L1 inhibitor was Loqtorzi.

The next-generation treatment landscape in HCC illustrates the race to evaluate immuno-therapy combinations anchored by a PD-L1 inhibitor in solid tumors. It provides context for the pursuit of Loqtorzi from Junshi Biosciences and the acquisition of Surface Oncology.

Now armed with multiple immuno-oncology assets, Coherus BioSciences will swap in Loqtorzi for future Casdozo clinical trials, while also considering new combinations with its TIGIT inhibitor (HCC is the lead indication) and external assets from the industry (potentially including Nexavar).

The phase 2 data readout for the triple combination in HCC will be followed by a data readout in non-small cell lung cancer (NSCLC), which is evaluating Casdozo as a monotherapy. This, too, follows the broader development path for the company's pipeline. Both Loqtorzi and the TIGIT inhibitor have data or are being evaluated in NSCLC, providing potential combinations to explore in lung tumors.

Forecast & Modeling Insights

(Introducing 2024 model.)

Solt DB Invest is introducing our 2024 model for Coherus BioSciences, which will now be the basis for calculating the Margin of Safety.

The model expects continued market share gains and revenue growth for the Udenyca franchise (excluding Udenyca OBI) and Cimerli. The launch of Loqtorzi in early 2024 will set a foundation for immuno-oncology revenue, which, being driven by novel assets, won't be subjected to the same competitive pricing dynamics as biosimilars. The ramp of Yusimry will be meaningfully slower than previously expected, as Humira is expected to retain over 95% market share in 2024.

Solt DB Invest's current model for Coherus BioSciences expects full-year 2024 net product revenue of at least $365 million, representing an increase of 46% from the year-ago period (assuming $250 million in revenue).

- Udenyca franchise revenue of at least $175 million, representing an increase of 34% from the year-ago period. This excludes contributions from Udenyca OBI, which isn't expected to generate revenue until 2025. If the formulation launches and avoids legal entanglements with Amgen, then Udenyca franchise revenue will be meaningfully higher in 2024.

- Cimerli revenue of at least $150 million, representing an increase of 27% from the year-ago period.

- Loqtorzi revenue of $25 million to $45 million following launch in early 2024. This represents a trajectory allowing full market share in NPC within two to three years, as expected by the company.

- Yusimry revenue of $15 million, compared to $2.4 million in 2023. This assumes Humira maintains formulary coverage through 2024. The growth of adalimumab biosimilars such as Yusimry is expected to meaningfully accelerate in 2025, due primarily to changes from the Inflation Reduction Act (IRA) and evolving competitive dynamics for pharmacy benefit managers (PBMs).

Coherus BioSciences is expected to return to cash flow operations in the second half of 2024, although the return to profitability may not occur until 2025.

In addition to product revenue, the business has the potential to generate licensing revenue. Mid-stage data readouts for both casdozokitug ("Casdozo") and CHS-114 in the first half of 2024 create the opportunity to close international licensing deals before the end of the year. Such deals might only generate an upfront payment of roughly $25 million.

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close November 6: $2.47 per share

- Modeled Fair Valuation: $13.15 per share

- Allocation Range: Up to 15%

Coherus BioSciences reported 111.364 million shares outstanding as of October 31, 2023. The modeled fair valuation above assumes 116.932 million shares outstanding, which is equivalent to 5% dilution by the end of 2024.

Further Reading

- November 2023 press release announcing third-quarter 2023 operating results

- November 2023 regulatory filing (10-Q) detailing third-quarter 2023 operating results

- November 2023 research note analyzing Loqtorzi's approval and trajectory

- August 2023 research note analyzing second-quarter 2023 operating results

.svg)

.svg)

.svg)

.svg)

.png)

.svg)

.png)

.svg)

.svg)

.svg)