.svg)

I've seen enough.

The market might be in a "wait-and-see" stance until the supply shortage impact becomes clearer, but investors have objectively seen enough to be confident in the company's commercial execution for 2025. The next seven weeks might represent the most favorable risk-reward for Coherus BioSciences ever.

While many investors remain cautious, they're missing several key insights into the strength of the commercial operations of the business and the Udenyca franchise. A significant loss of accounts is unlikely due to the mechanics of the American healthcare system (Udenyca and Neulasta enjoy preferred status), rebates offered by Coherus, a dominant competitive position driven by optionality and convenience, and favorable insurance coverage.

This is an awesome and rare scenario. Despite my large position, I'm not passing it up.

My current plan is to invest my entire Roth IRA contribution for 2025 into Coherus BioSciences in early January – the second consecutive year I've done so. Management promised to provide a Q4 revenue update and at least Q1 2025 outlook in January. I'm confident that trade will create a significant windfall by the end of 2026, which will cement my transparent track record for Finch Trades. That's important for Solt DB the business and my personal financial goals.

Solt DB will succeed or fail based on Finch Trades. The number one concern I see in my market research as an entrepreneur is doubt about investing in biotech stocks. Aren't those risky penny stocks? There's so much noise. Why do that when the S&P 500 can return 50% in 18 months?

Well, Finch Trades will be the answer. I want to prove – transparently and with no room for doubt – that investors can craft an investing strategy in biotech stocks (even if they only invest in biotech stocks) and outperform passive investing by a significant margin. Many investing platforms, newsletters, and gurus fade because selling the dream only works for so long. The bill always comes due. I don't want to sell the dream. I want to sell outperformance.

My goal is to eventually exit my position(s) in Coherus and reinvest almost all the proceeds into Relay Therapeutics and Arrowhead Pharmaceuticals. That will set up the next leg of outperformance for Finch Trades.

Let's dig in and see why investors should be excited about 2025.

By the Numbers

My model for the third quarter of 2024 was significantly ahead of Wall Street estimates. Coherus BioSciences was significantly ahead of both.

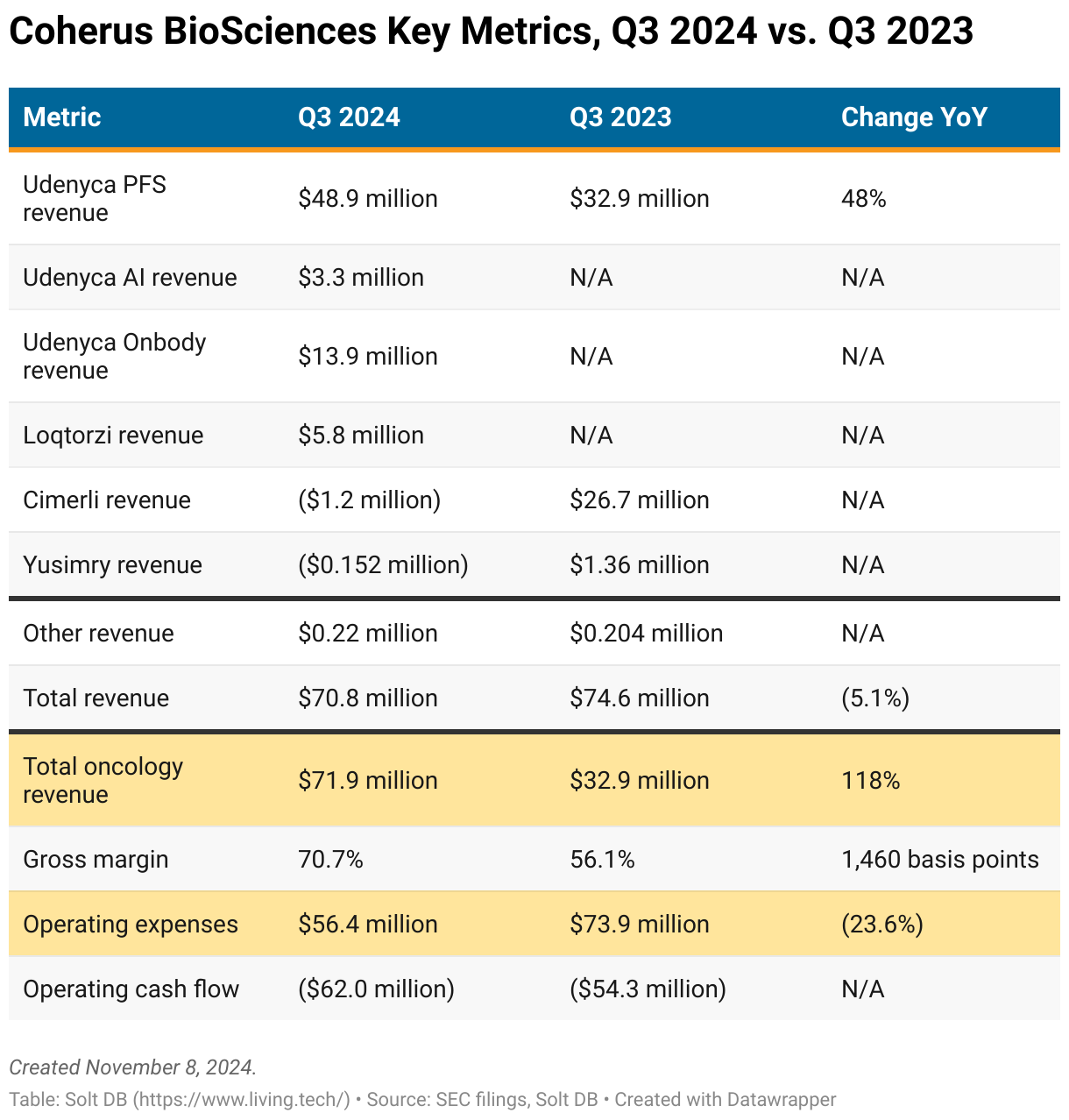

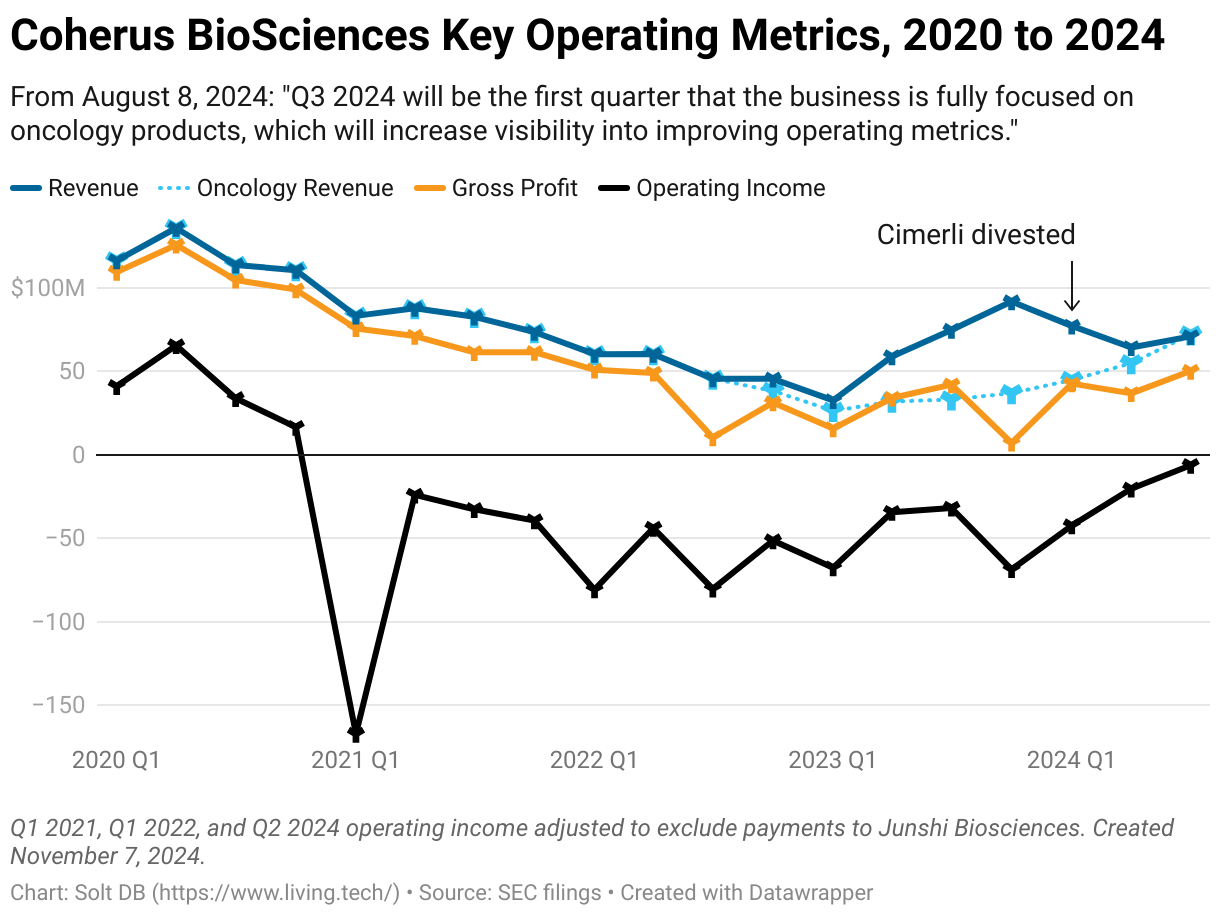

The business achieved total third-quarter 2024 revenue of $70.8 million. That actually included negative $1.4 million in revenue as the Yusimry and Cimerli divestments rolled off the books, which also made operating cash flow appear worse than reality due to one-time accounting charges. To be fair, the same made operating cash flow appear better than expected in Q2 2023.

Focusing on Loqtorzi and Udenyca, the business achieved total net revenue of $72.1 million. My model expected "just" $64.124 million. Temporary costs related to tech transfer for Loqtorzi manufacturing (moving it from China to the United States) also ceased in Q3 – well ahead of schedule. When coupled with higher-margin revenue for Udenyca Onbody, gross margin for the quarter soared to 70.7%. That was the highest since Q2 2022 and well ahead of my model, which conservatively expected 58.5%.

Going a level deeper provides more insights into the strength of commercial execution during the quarter.

Coherus delivered Udenyca PFS revenue of $48.9 million (well ahead of my model of $39.0 million), Udenyca AI revenue of $3.3 million (well below my model of $5.25 million), and Udenyca Onbody revenue of $13.9 million (in line with my model of $14.374 million). It seems Udenyca AI might be getting cannibalized by both PFS and Onbody, but they're the two more important products.

As a percentage of total franchise revenue, Udenyca PFS represented 74% (down from 76.5% in Q2), Udenyca Onbody soared to 21% (up from 13.5% in Q2), and Udenyca AI settled at 5% (down from 10% in Q2). For reference, Udenyca Onbody is expected to represent the dominant share of franchise revenue over time. My current 2025 model expects it to represent only 37.5% of franchise revenue by Q4 2025, which is relatively conservative.

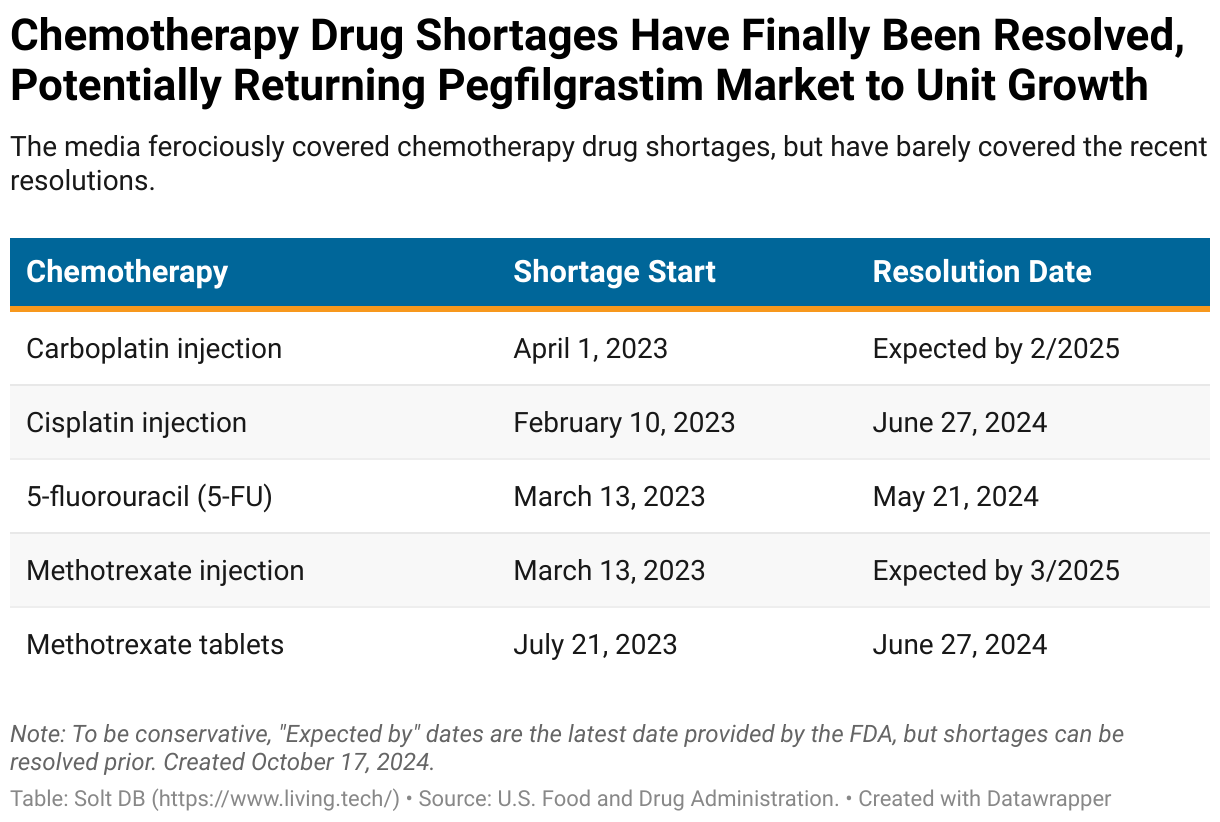

At the end of September 2024, the Udenyca franchise held 28% market share. This is down from 29% at the end of June 2024, despite quarter-over-quarter revenue growth of 30%. That's good news. The overall value of the pegfilgrastim market grew as the longstanding chemotherapy shortage ended and Amgen had a change of heart, increasing the selling price of Neulasta. The originator product had revenue of $84 million in Q3 vs. $75 million in Q2.

Loqtorzi is tracking well with my model. The brand has been prescribed by 80% of National Comprehensive Cancer Network (NCCN) hospitals and is now the preferred treatment option for nasopharyngeal carcinoma (NPC) in all centers.

Importantly, Loqtorzi plus chemotherapy provides a relatively long duration of treatment of over 36 months in the first-line (1L) treatment setting. That makes it important to prescribe the brand to new patients. They'll drive revenue growth during the ramp, but will also provide a significant foundation of revenue over time. A significant number of patients that begin 1L treatment today will still be receiving treatment in November 2027 – the effectiveness of treatment creates a compounding effect for revenue.

However, this also slows the ramp a bit. Patients being treated with other PD-1 inhibitors off label (Loqtorzi is the only drug in the class formally approved for NPC) will not be switched to Loqtorzi. That's why the ramp will be slow-and-steady for three to four years. Nonetheless, although the peak revenue opportunity in NPC of $150 million is relatively low, it's almost unheard of to achieve peak revenue in such a short period. It would be even faster without this dynamic.

My gross margin model of 58.5% for Q3 2024 came with a significant caveat. As explained in the August 2024 research note analyzing Q2 2024 results:

Gross margin of 58.5% (vs. 56.3% in Q2). This includes no improvement for either brand compared to Q2. Rather, the cost of goods sold is expected to decline as one-time charges totaling $5.9 million roll off. Management expects gross margin to steadily improve, but I cannot reliably model it during the commercial ramp.

My model expected operating expenses of roughly $57 million, whereas the business delivered operating expenses of $56.42 million. I have a good read on expenses right now, aided by discussions with management. Who knows what the fuck Wall Street analysts getting paid way more than me are doing.

Coherus coughed up an operating loss of just $6.4 million during the third quarter, which will be more reflective of operating cash burn beginning in 2025. The dust is still settling from the transition away from Yusimry and Cimerli, layoffs, and restructuring. As a result, the business reported operating cash burn of $62.016 million. It's just accounting though. The recent result was offset by a favorable operating cash inflow of $59.7 million in Q2.

By the Molecule

Analysts seemed suddenly interested in the company's IL-27 inhibitor casdozokitug. There were no new updates from Coherus, but several disappointing developments in the next-generation hepatocellular carcinoma (HCC) competitive landscape appeared to boost the company's positioning. It helps more because casdozo is the only IL-27 inhibitor, which means worse-than-expected results from competing combinations don't necessarily impact the results achieved to date for the asset.

More data are needed to confirm the company's competitive ranking, but it could boost the value of casdozo both internally or for international (or planetary) licensing discussions.

Meanwhile, management provided more details for the development plan for CHS-114. This is the more important asset according to my current modeling, which I detailed in a recent research note. Coherus is one of the few companies that wields both a PD-1 asset (Loqtorzi) and a CCR8 asset (CHS-114). Very encouraging results and upcoming data readouts from the competitive landscape in 2025 are expected to provide a significant boost in valuation for the business.

Coherus will announce new biomarker data from the phase 1 study in November 2024. It's also actively enrolling a phase 1b study combining CHS-114 with Loqtorzi, which will have preliminary data in the second half of 2025. Importantly, the company is optimizing dosing of the combination therapy further as part of the phase 1b and phase 2 study, which alleviates my key concern with the asset's development.

Investors will be able to rank the data alongside Bristol Myers Squibb, LaNova Medicines, and Roche by then – all good company to be in. Encouragingly, CHS-114 is designed similarly to the two leading global assets, BMS-986340 from Bristol and LM-108 from LaNova.

It appears increasingly likely LaNova Medicines will license U.S. rights to LM-108, which could fetch a significant nine-figure ($XXX million) upfront payment. That would easily boost Coherus in sympathy and put CHS-114 on the radar of investors, although clinical data rule in the end.

Forecast & Modeling Insights

(Introduced 2025 model.)

My new model for Q4 2024 is pretty ugly. It might be too conservative, but investors should prepare for achieving one-fourth of a normal quarterly period's performance. This ugliness is also what drives the opportunity.

For transparency, the fourth-quarter 2024 model assumes:

- Total product revenue of $27.095 million (vs. $72.1 million achieved in Q3)

- Revenue includes roughly $12.5 million for Udenyca PFS (vs. $48.906 million in Q3), $0.750 million for Udenyca AI (vs. $3.304 million in Q3), and $5.345 million for Udenyca Onbody (vs. $13.879 million in Q3).

- Revenue includes approximately $8.5 million for Loqtorzi (vs. $5.832 million in Q3). I didn't increase my model despite being outperformed in Q3, which means my model is conservative for this asset. But there is some seasonality here with holidays and, in the midst of the commercial ramp, it's impossible to model accurately. I'll always lean conservative.

- Gross margin of 44.6% (vs. 70.7% in Q3). Cost of goods sold is expected to be roughly $15 million (vs. $20.741 million in Q3).

- Operating expenses of roughly $60 million (vs. $56.420 million in Q3).

- (New) Operating cash flow of negative $47.905 million (vs. negative $6.387 million in Q3) bringing the cash balance to $49.785 million at the end of 2024.

For transparency, the new full-year 2025 model assumes (2024 totals include Q4 modeled values):

- Total product revenue of $363.125 million (vs. $232.864 million achieved in 2024)

- Revenue includes roughly $174.250 million for Udenyca PFS (vs. $138.758 million in 2024), $10.750 million for Udenyca AI (vs. $12.560 million in 2024), and $109.125 million for Udenyca Onbody (vs. $26.950 million in 2024).

- Revenue includes approximately $69.0 million for Loqtorzi (vs. $20.109 million in 2024).

- Gross margin of 60.6% (vs. 58.9% in 2024). Cost of goods sold is expected to be roughly $143.044 million (vs. $98.695 million in 2024).

- Operating expenses of roughly $250 million (vs. $258.542 million in 2024).

- (New) Operating cash flow of negative $29.919 million (vs. negative $86.048 million in 2024).

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Speculative) position. The current modeled fair valuation for the company based on my 2025 model is below:

- Market close November 7: $0.82 per share

- Modeled Fair Valuation: $9.13 per share

- Allocation Range: Up to 10%

Coherus BioSciences reported 115.213 million shares outstanding as of October 31, 2024. The modeled fair valuation above assumes 133.513 million shares outstanding, which is equivalent to 16% dilution.

Further Reading

- November 2024 press release announcing Q3 2024 operating results

- November 2024 regulatory filing (10-Q) detailing Q3 2024 operating results

October 2024 research note analyzing the preliminary opportunity in CCR8 - September 2024 research note analyzing the Udenyca supply shortage

- August 2024 research note analyzing Q2 2024 operating results

.svg)

.svg)

.png)

.svg)

.png)

.svg)

.svg)

.svg)