.svg)

Exhale.

Commercial execution is the core strength of Coherus BioSciences – and it was on full display in the second quarter of 2024.

The business provided an early glimpse of a simplified capital structure, which included operating expenses that were 5% lower than my model and well below Wall Street expectations. That helped to offset a slower-than-expected improvement in gross margin.

Importantly, both Loqtorzi and Udenyca Onbody have achieved a solid commercial foundation for their ongoing ramps.

Loqtorzi is now available in all 33 National Comprehensive Cancer Network (NCCN) centers in the United States, which treat an estimated 60% of all NPC patients. The number of patients on treatment doubled from the first quarter. The Centers for Medicare and Medicaid Services (CMS) granted a unique J Code on the first day of Q3 2024 that will improve ordering and reimbursement for hospitals. The product now has "no limitations" for national reimbursement – an impressive achievement just six months into launch.

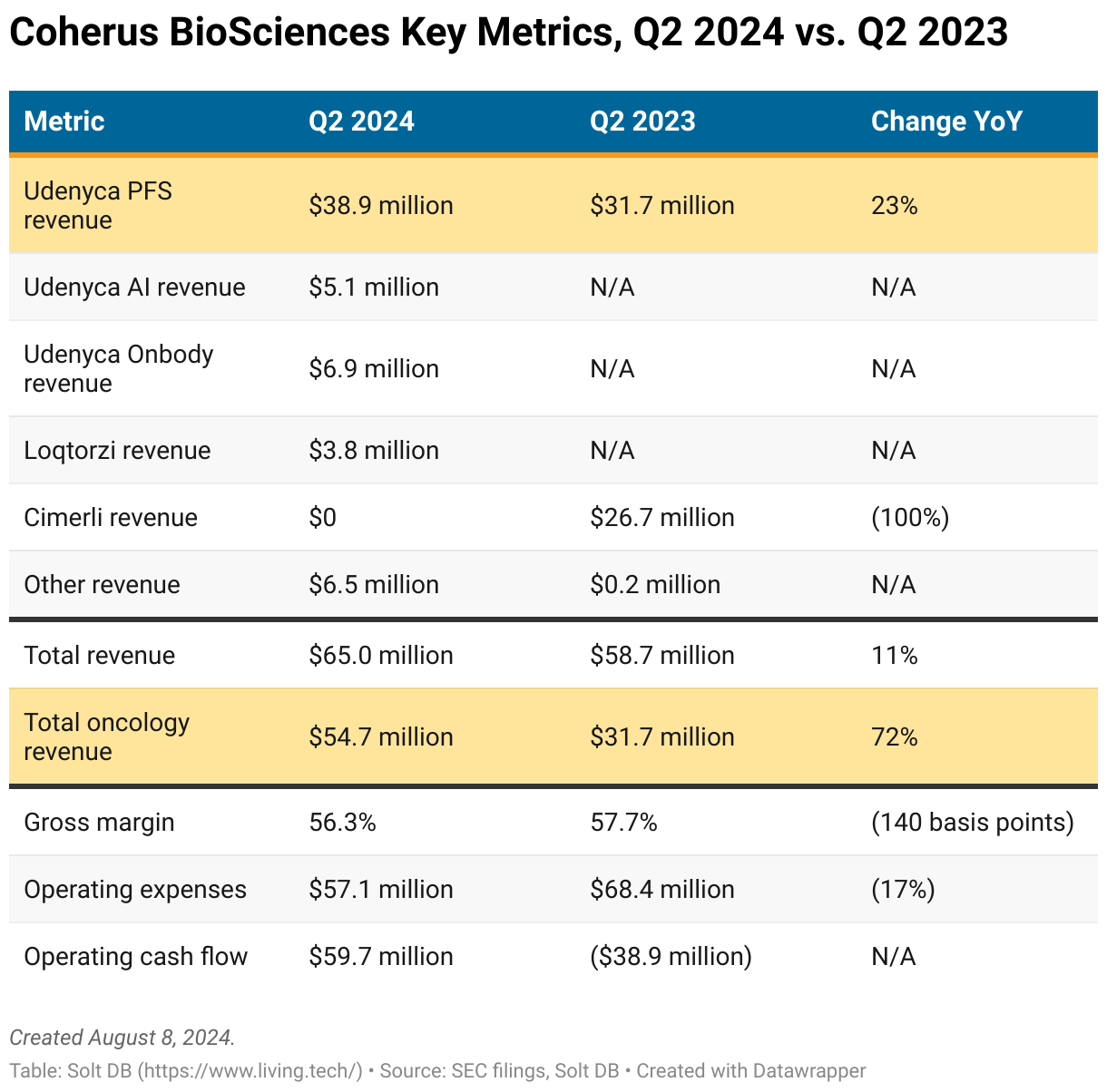

The Udenyca franchise gained market share across all three presentations despite being the highest-priced pegfilgrastim brand on the market. The prefilled syringe (PFS) formulation achieved its highest revenue level in two years, the autoinjector (AI) formulation grew revenue 49% quarter-over-quarter as management's unique strategy begins to gain meaningful traction, and Udenyca Onbody is now the company's second-bestselling product just four months into launch.

Meanwhile, an important phase 3 clinical trial for Loqtorzi is now underway in the United States that could more than triple the annual market opportunity to $500 million upon approval in 2027 – and Coherus BioSciences doesn't have to spend a penny.

I'm taking the opportunity to introduce several conservative refinements to my 2024 model, which could be proven wrong to the upside as the commercial ramp progresses in the second half of the year.

By the Numbers

Investors can be more confident in the commercial trajectory of both Loqtorzi and Udenyca Onbody. Coherus BioSciences will need to build on the strong start in the next few quarters, but there's less statistical fog to cloud expectations.

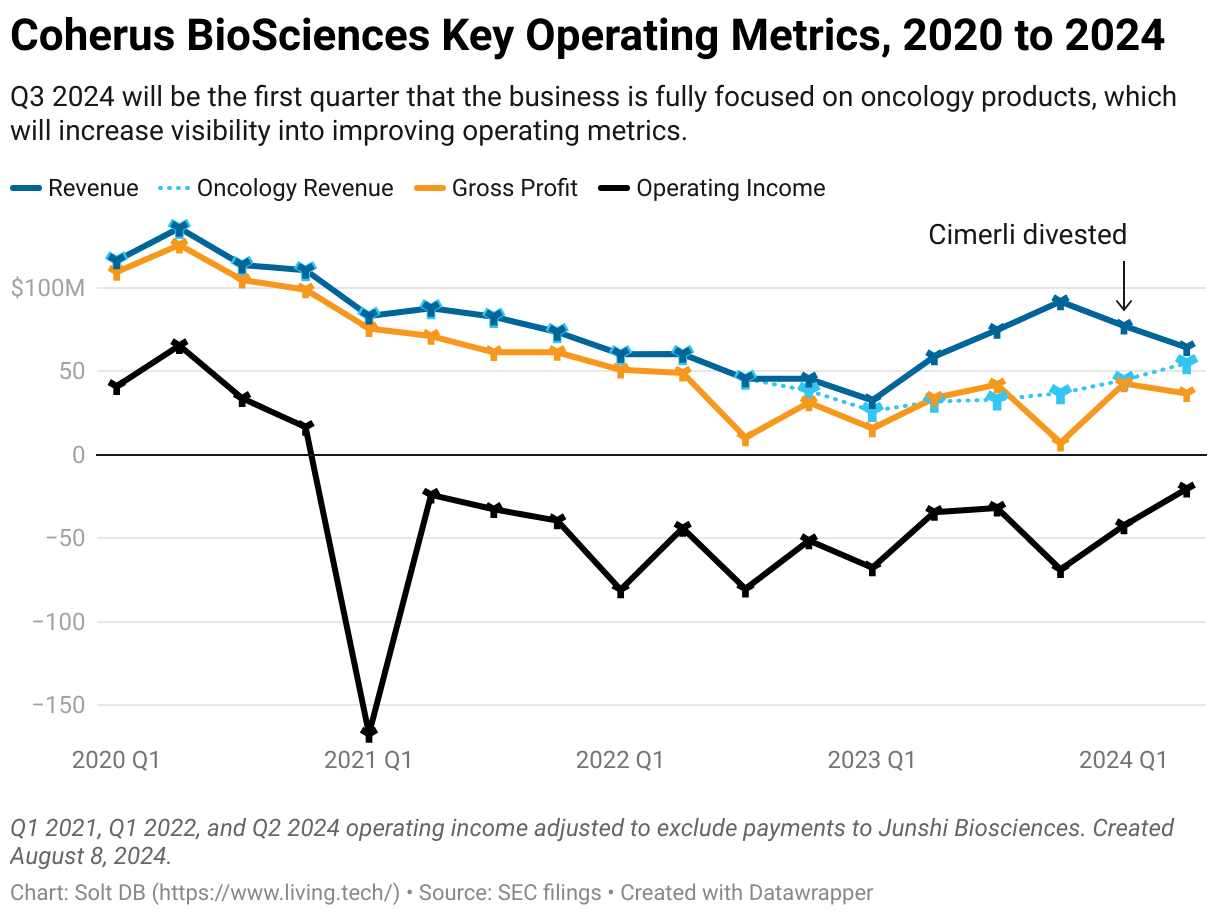

The second quarter of 2024 was the first without contributions from Cimerli and the last with contributions from Yusimry. The business still matched product revenue, delivered higher gross profit, and reduced operating expenses 16% compared to the year-ago period – when Cimerli contributed $26.7 million in revenue. That's exactly what's needed to win hearts and minds on Wall Street.

Products that didn't exist a year ago generated $15.7 million in Q2 2024 revenue, while Udenyca PFS grew sales by $7.2 million in that span. Total oncology revenue of $54.7 million was the highest since early 2022 and increased 72% year over year.

A changing product mix bodes well for introducing something the business has never had: durable revenue.

Loqtorzi's ramp to an estimated peak revenue opportunity of at least $150 million in NPC will be less susceptible to erosion, as there's no competition and it's the recommended treatment in all major guidelines. It's expected to reach the peak by the end of 2027, just as a new opportunity in small-cell lung cancer (SCLC) earns approval to more than triple the overall market opportunity.

Investors can expect the Udenyca franchise to grow revenue through 2025. Whether and where it stabilizes beyond that depends on factors that cannot be predicted at this time. For now, the brand ended June 2024 with 29% market share. Udenyca Onbody alone wields a 4% slice of the total pegfilgrastim market and roughly 9% of all OBI units sold.

Coherus ended Q2 2024 with a cash balance of $159.2 million, which was significantly higher than my projections of roughly $84.8 million. My estimate incorrectly accounted for the financial impact of one of the recent asset divestitures. I guess "gain-on-sale" accounting isn't my strength. So much for my future as a biotech CFO.

As a result, the business should be able to fund itself to cash flow breakeven operations. Investors can reduce their focus on the cash balance. Importantly, the company's historical operating income has mirrored total oncology revenue, which suggests profitable operations are within reach. Both breakeven operating cash flow and manageable operating losses are key de-risking events.

Forecast & Modeling Insights

(Refined.)

The 2024 model has been refined across several key metrics and assumptions as the commercial ramp becomes clearer. Note that many refinements are conservative and may underestimate performance if commercial execution continues:

- Loqtorzi is now expected to reach peak sales by the end of 2027, which is one year longer than the prior model. Full-year 2024 revenue is now expected to be roughly $19.77 million vs. prior model of $40 million.

- I can now separate models for Udenyca PFS and Udenyca AI, which were previously combined.

- Udenyca Onbody is now included in the model. This presentation is expected to achieve more than 25% OBI market share by the end of 2024 and nearly 40% market share by the end of 2025. It adds full-year 2024 revenue of $43.975 million vs. prior model of $0.

- Gross margin expectations have been refined lower to account for new ramp trajectory of Loqtorzi, technology transfer to the United States for Loqtorzi, and working through higher-cost inventory for the Udenyca franchise. The 2024 model now expects no improvement to gross margin in the second half of 2024, primarily because it's difficult to model. Management expects significant improvement in gross margin from a Q2 2024 baseline but offered no guidance.

- Due to conservative refinements to revenue and gross margin, my modeling no longer expects operating income in 2024 or 2025. However, a much higher-than-expected cash balance means the business can fund itself (including new clinical trials) to positive operating cash flow. The cash runway is no longer a key focus for investors.

In addition to the potential sources of upside mentioned above, Coherus BioSciences quietly retained its patent estate for manufacturing adalimumab proteins despite divesting the rights to Yusimry. That's interesting because Pfizer licensed the intellectual property in 2019.

Pfizer must pay the company royalties on sales of its adalimumab biosimilar, Abrilada, which is one of three interchangeable products. It only launched on the first day of 2024, but if it secures favorable status at pharmacy benefit managers (PBMs) and ramps in the next few years, then Coherus could claw back some of its overall investment in Yusimry or monetize the revenue stream in a future transaction. The messy adalimumab market means I cannot responsibly factor this into my modeling, but it's something to watch in the next 24 months.

It should also be noted that Wall Street models will need to increase. The consensus for Q3 2024 product revenue is $58.98 million, which would represent growth of just $0.5 million from Q2 2024. That's incompatible with the commercial ramp of Loqtorzi and Udenyca, which added $9.9 million in revenue from the first to second quarter.

And if you ever needed real-world evidence for my claims that small-cap biotech companies are primarily covered by junior Wall Street analysts, then consider an exchange on the Q2 2024 conference call. An analyst asked a series of questions about royalties for Loqtorzi, which is information that's clearly written in multiple press releases and SEC filings since 2021. To their credit, management painstakingly answered the questions, but appeared a bit surprised.

That's what we're dealing with here. This is a strong signal that the market is wrong, which is a characteristic of many of my best investments.

For transparency, the third-quarter 2024 model assumes:

- Total product revenue of roughly $64.124 million (vs. $58.472 million in Q2 or $54.706 million excluding Yusimry).

- Revenue includes $39.0 million for Udenyca PFS (vs. $38.952 million in Q2), $5.250 million for Udenyca AI (vs. $5.092 million in Q2), and $14.374 million for Udenyca Onbody (vs. $6.874 million in Q2).

- Revenue includes $5.500 million for Loqtorzi (vs. $3.789 million in Q2).

- Gross margin of 58.5% (vs. 56.3% in Q2). This includes no improvement for either brand compared to Q2. Rather, the cost of goods sold is expected to decline as one-time charges totaling $5.9 million roll off. Management expects gross margin to steadily improve, but I cannot reliably model it during the commercial ramp.

- Operating expenses of roughly $57 million (vs. $57.120 million in Q2).

- Operating income is expected to steadily improve through the end of 2025, albeit with operating margins remaining negative.

For transparency and to maintain the format of prior research notes, the new full-year 2024 model assumes:

- Total product revenue of roughly $282.040 million

- Revenue includes $156.352 million for Udenyca PFS and $19.235 million for Udenyca AI. These were combined in the prior model, but exactly match the total ($175 million). Modeling is easier when you don't have to account for messy commercial ramps.

- Revenue includes $43.975 million for Udenyca Onbody. Although this product wasn't included in the prior 2024 model, this value is less than the preliminary expectation of $62 million shared in research notes. That's still possible, but I'll let commercial execution prove me wrong to the upside.

- Revenue includes $19.777 million for Loqtorzi (vs. $40.000 million in the prior model). The change reflects expectations for a longer ramp to peak sales, which are now expected in 2027 instead of 2026. Management is confident the milestone could still be achieved in 2026, but I'll let commercial execution prove me wrong to the upside.

- Gross margin of 56.9% (vs. 59.9% in the preliminary model that included Udenyca Onbody). This is likely too conservative, but I'll let commercial execution prove me wrong to the upside.

- Operating loss of $98.590 million (vs. $89.818 million in the preliminary model that included Udenyca Onbody). Note that 64% of the full-year 2024 operating loss was generated in the first half of the year. It also includes $40 million in non-cash expenses.

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Quality) position. The current modeled fair valuation for the company based on my 2024 model is below:

- Market close August 8: $1.29 per share

- Modeled Fair Valuation: $10.12 per share (vs. $10.02 per share)

- Allocation Range: Up to 15%

Coherus BioSciences reported 115.208 million shares outstanding as of July 31, 2024. The modeled fair valuation above assumes 133.508 million shares outstanding, which is equivalent to 5% dilution plus full accounting of the 2026 convertible notes. If the convertible debt is restructured, then the impact would be reduced (increasing the estimated fair value on a per share basis).

Further Reading

- August 2024 press release announcing Q1 2024 operating results

- August 2024 regulatory filing (10-Q) detailing Q1 2024 operating results

- June 2024 research note discussing the divestment of Yusimry

- May 2024 research note analyzing Q1 2024 operating results

- March 2024 research note analyzing full-year 2023 operating results

.svg)

.png)

.svg)

.png)

-cropped.svg)