.svg)

Sell high, buy low.

Coherus BioSciences announced plans to sell Cimerli to Sandoz in a $190 million transaction, which includes an expected $20 million cash payment for inventory on hand. The ranibizumab biosimilar provided a significant boost to the business last year, generating full-year 2023 revenue of roughly $123 million and gross profit of nearly $52 million. It exited December with a ridiculous 38% market share.

But the structure of the ranibizumab market suggests the product will reach peak revenue in the next few quarters. It won't turn into the same slugfest as the pegfilgrastim market, but Cimerli's value will never be higher than right now.

The sale creates a win-win situation.

Sandoz acquires the leading biosimilar commercial infrastructure in ophthalmology, which it will use to accelerate the launch of its Eylea biosimilar. That's a much larger market opportunity, although Cimerli's revenue will make a solid contribution to the company's $2 billion in annual biosimilar sales.

Coherus BioSciences will grab $170 million in exchange for its commercial infrastructure and another $20 million for inventory on hand when the transaction closes. The business will reduce the balance of its term loans from $246 million to $76 million, save an estimated $25 million per year in interest expense, increase gross margin from 56% to over 80%, and reduce operating expenses by a yet-to-be-determined amount.

Scrambling every financial model on Wall Street will have some consequences. A slimmer Coherus will spend less, but also generate less revenue in the near term. It'll generate higher-quality revenue, but also have one less opportunity (ophthalmology) for future growth. The shift to focus solely on oncology isn't inherently good or bad, but it's different from expectations a few months ago. Different takes time to digest.

Nonetheless, the company's primary objective in 2024 remains the same. Coherus BioSciences needs to execute with core products and reset the negative narrative hanging over the stock.

Coherus is Selling at the Right Time

If the company was ever going to maximize the value of Cimerli in a sale, then now's the time to do it. To see that, it helps to understand the positive characteristics of the asset – and how they'll begin to fade away in 2024.

The swift success for the eye disease product was driven by a combination of factors.

- First, Coherus BioSciences nailed the launch timing. Although Cimerli was the second ranibizumab biosimilar to reach market, it secured interchangeability status. The regulatory designation isn't important for every therapeutic area, but it carried more value in ophthalmology where doctors were using biosimilars for the first time. That gave it an edge in the formation of the market, as evidenced by it securing 38% market share in its fifth quarter after launch.

- Second, the competitive landscape is relatively tame. There are only three ranibizumab products in the United States: Lucentis (the originator drug), Byooviz (a biosimilar) from Biogen, and Cimerli. This has provided more room to maneuver and quickly devour market share.

But some of the factors that drove success will create headwinds in the near future.

- First, one of the reasons for a lack of direct competition is that the direct market isn't very large. Lucentis corrals inflammation in eye diseases by inhibiting VEGF, but it commands less than 20% of all anti-VEGF unit sales. Biosimilars of Lucentis can only target this 20% pool of prescriptions. The remaining 80% goes to completely different anti-VEGF drug products.

- Second, there's also a slew of next-generation products providing indirect competition. Eylea owns a dominant 40% market share for all anti-VEGF products. It generates more revenue every quarter than Lucentis generated in its peak year. Convenience is the reason. Eylea can be dosed once every two to four months, whereas Lucentis and the gang of ranibizumab biosimilars are dosed every month. Patients will generally opt to reduce the number of injections into their eyeballs, even if that convenience costs more.

- Third, Eylea biosimilars are coming in 2025. That will significantly impact pricing and unit volumes for ranibizumab products. It could present a moderate headwind at best or an existential headwind at worst.

- Fourth, direct competition will increase significantly in 2024. Cimerli's exclusive interchangeability status expired. The designation provided an advantage in courting doctors during the first 12 to 16 months on the market, and those relationships remain intact. But the advantage will fade this year. Byooviz picked up interchangeability status in October 2023. Meanwhile, a third ranibizumab biosimilar, Xlucane from Xbrane Biopharma, is expected to earn U.S. Food and Drug Administration (FDA) approval in April 2024. It, too, will be interchangeable, which means every ranibizumab product will be on equal footing.

Cimerli will probably grow market share above 38% in the first half of 2024, but that won't be sustainable, especially once Xlucane launches. There aren't expected to be any additional near-term ranibizumab launches, so the market won't be quite as depressing as the pegfilgrastim slugfest, but a pricing battle is on the horizon.

The unique factors of the ranibizumab market mean Cimerli is likely to have a short-lived peak (within eight quarters of launching) before declining.

- Cimerli can likely generate $50 million to $100 million in annual revenue at steady state, depending on how Eylea biosimilars impact the market.

- The asset generated full-year 2023 revenue of $123 million.

- The asset had an annual revenue run rate of $204 million in the fourth quarter of 2023, but that highlights the sharp peak, not the long-term growth potential.

- I modeled full-year 2024 revenue of about $150 million, which included the start of the sales decline in the second half of the year.

- Cimerli might only have full-year 2025 revenue of $75 million to $125 million.

So, why would Sandoz want a product that will soon be in decline?

Sandoz filed for regulatory approval for its Eylea biosimilar in the second half of 2023, for which it expects to earn interchangeability status. The commercial infrastructure in ophthalmology – sales team, relationships with doctors, marketing, and so on – acquired from Coherus can be leveraged to greatly accelerate the launch of a much more lucrative product.

Don't forget, there are only two companies with commercial infrastructure for biosimilars in ophthalmology: Biogen and Coherus. Every other company eyeing the opportunity for Eylea biosimilars needs to invest in building that from scratch.

That's really the primary component of the transaction for Sandoz.

Going All-In Has Some Drawbacks

Divesting Cimerli isn't all lollipops and rainbows for Coherus BioSciences.

On the one hand, focusing all bandwidth on oncology products will lead to operating efficiencies. The company no longer has to maintain commercial infrastructure for an ophthalmology business unit. That avoids expenses for a sales team selling only a single product (the oncology sales team can sell four different products). For similar reasons investors should prepare for Yusimry, an adalimumab biosimilar to Humira, to be divested.

On the other hand, wielding the leading commercial infrastructure for biosimilars in ophthalmology provided a solid source of diversity and future growth potential. Coherus was also interested in commercializing an Eylea biosimilar and in-licensed rights to an asset from Klinge Biopharma. That would've been easier to pull off with the commercial infrastructure built for Cimerli, which was the same reason Sandoz was interested in a deal.

In simple terms, divesting Cimerli (and likely Yusimry) raises the stakes for execution within the oncology portfolio and pipeline. That's not a bad position to be in, but every quarterly report and data readout carries more weight now.

How Does This Change Plans for 2024 and Beyond?

The divestment will scramble Wall Street analysts' models.

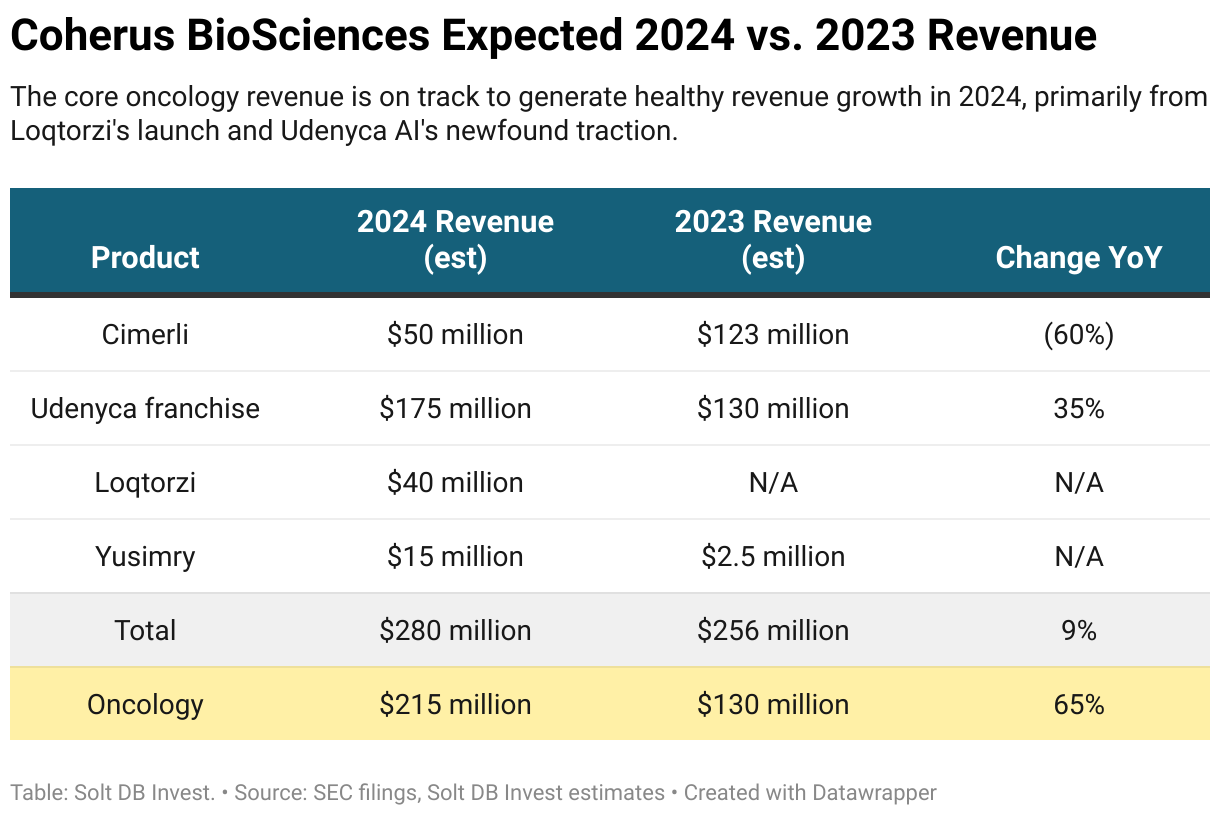

Instead of penciling in $150 million of revenue contributions from Cimerli in 2024, analysts will now need to significantly lower expectations. The asset is likely to contribute a full quarter of revenue before the transaction with Sandoz closes in the second quarter.

Investors can gauge execution in 2024 by focusing on revenue from oncology products (the Udenyca franchise and Loqtorzi) and total operating margins.

- Udenyca AI saw significant traction at the end of 2023 that has carried into early 2024, which will help to increase the franchise's total revenue and pegfilgrastim market share. My 2024 model expects Udenyca PFS and Udenyca AI to generate $175 million in revenue.

- My 2024 model assumes Udenyca Onbody generates $0 in revenue due to an expected legal challenge from Amgen. If the product does launch in the first quarter, then it could generate full-year 2024 revenue of $75 million to $100 million.

- Loqtorzi revenue is expected to generate full-year 2024 revenue of $35 million to $45 million as it launches and ramps.

Although the lost revenue from Cimerli will hurt the top line, Coherus can replace the margin contribution with half the revenue.

The business had a gross margin of 42% on net sales of Cimerli. That's because it paid a 53% royalty on gross profits for the asset. In other words, the company doesn't need to generate $150 million in revenue from oncology products to replace the impact of Cimerli.

- Let's say Cimerli was going to generate $150 million in revenue in 2024. At a gross margin of 42%, investors could've expected $63 million to trickle down the income statement as gross profit – a pretty solid haul.

- But Udenyca products will have a gross margin of 85% in the first half of 2024. When a royalty paid to Amgen expires at the end of June 2024, Udenyca products will have a 90% gross margin.

- Loqtorzi will have a gross margin of 70% to 75%, which includes the royalty paid to Junshi Biosciences.

That means Coherus can replace the gross profit that would've been generated from Cimerli ($63 million in gross profit for every $150 million in revenue) with just $72 million in additional annual revenue from Udenyca or $90 million in annual revenue from Loqtorzi.

Using the expected revenue growth from Udenyca and new revenue from Loqtorzi in my 2024 model, these products will add full-year 2024 gross profit of $67.5 million. Remember, that excludes contributions from Udenyca Onbody.

So, the company's oncology products are already on track to replace the gross profit contributions expected from Cimerli during its peak year of revenue. The advantage widens when investors look to 2025. I expect Cimerli revenue will decline, while Udenyca Onbody begins making contributions and Loqtorzi more than doubles revenue in its second year of ramp.

Forecast & Modeling Insights

(Reduced product revenue, adding pipeline assets)

My 2024 model for Coherus BioSciences now includes the following from the commercial portfolio:

- Total full-year revenue of at least $275 million compared to previous expectations for total full-year revenue of at least $375 million.

- Cimerli will generate revenue of approximately $50 million generated prior to being divested in Q2 2024. This is down from a previous expectation for roughly $150 million in revenue before the asset sale was announced.

- Udenyca PFS and Udenyca AI will generate revenue of approximately $175 million, representing no change from the previous model.

- Udenyca Onbody will not contribute revenue in 2024, representing no change from the previous model.

- Loqtorzi will generate revenue of $35 million to $45 million in 2024, representing no change from the previous model.

- Yusimry will generate revenue of approximately $15 million, representing no change from the previous model.

The updated 2024 model takes a hit from sharply lower revenue expectations, which is partially offset by assigning a higher valuation to the higher quality revenue that remains.

Whereas the previous model valued the commercial portfolio at $1.537 billion, the updated model assigns a value of $1.200 billion on the nose.

The updated 2024 model also introduces valuation estimates from the immuno-oncology pipeline.

- The total immuno-oncology pipeline contributes an additional value of $52 million as of January 22, 2024.

- The positive phase 2 clinical data readout for the Casdozo triplet in first-line liver cancer means the asset contributes roughly $38 million to the company's valuation.

- The remaining pipeline comprises Casdozo's monotherapy in squamous cell non-small cell lung cancer (NSCLC), CHS-114 in head and neck cancers, and CHS-1000 in undisclosed solid tumor cancers. These combine for an additional $14 million in valuation – they're very early-stage assets.

The updated 2024 model values the commercial portfolio at $1.200 billion and the emerging immuno-oncology pipeline at $52 million, which means Coherus BioSciences has an estimated fair valuation of $1.252 billion. This is based on expected 2024 operating performance and existing data readouts from the pipeline.

Additional sources of upside include:

- Udenyca Onbody launching in 2024 and generating more than $0 in revenue

- A potential asset divestment of Yusimry. This wouldn't generate meaningful upfront value like the recent transaction for Cimerli, but would be more likely to have a long-term royalty component payable to Coherus BioSciences.

- Coherus BioSciences might be able to court a large drug developer without a PD-1/L1 inhibitor for exclusive pairings with Loqtorzi. That could include Novartis or Eli Lilly.

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close January 19: $2.44 per share

- Modeled Fair Valuation: $10.71 per share

- Allocation Range: Up to 15%

Coherus BioSciences reported 111.364 million shares outstanding as of October 31, 2023. The modeled fair valuation above assumes 116.932 million shares outstanding, which is equivalent to 5% dilution.

Further Reading

- January 2024 press release announcing Cimerli transaction

- January 2024 research note explaining why the value of PD-1/L1 inhibitors is primarily based in combination treatments

- December 2023 research note analyzing the launch timeline for Udenyca Onbody and how Amgen might complicate launch

.svg)

.svg)

.svg)

.svg)

.png)

.svg)

.png)

.svg)

.svg)

.svg)