.svg)

Loqtorzi has started 2024 with a bang. It launched commercially and announced its first external clinical trial in the United States. The latter is being conducted by perpetually stumbling, solidly mediocre, rarely executing INOVIO Pharmaceuticals.

There's no risk to Coherus BioSciences. This isn't a partnership. There's no money changing hands. There are no additional expenses being incurred. The company will supply Loqtorzi for the phase 3 clinical trial in a specific type of throat cancer, but it's up to INOVIO to pay for the study and earn regulatory approval. If the combination earns approval years from now, then it creates an additional opportunity for Loqtorzi to generate revenue.

The bigger picture is more interesting.

Although Loqtorzi won't become the go-to PD-1 inhibitor for oncology combinations, a unique mechanism of action suggests it could ramp up more quickly than the laggards in its drug class.

Considering there were 4,652 clinical trials evaluating combinations with PD-1 inhibitors against nearly 300 molecular targets at the end of 2021, according to the Cancer Research Institute, there's plenty of room to maneuver within the crowded competitive landscape. Gaining even a little traction could significantly move the needle for Coherus BioSciences.

What Makes PD-1 Inhibitors So Important?

The complexity of biology has been driven by a molecular arms race that's been ongoing for the last 3 billion years.

At first, self-replicating molecules outcompeted others in the planet's primordial soup, sometimes stealing atoms from inferior chemical compounds. Eventually some of these complex molecules shielded themselves with protective membranes to gain an advantage from cannibalizing peers. Later, multiple systems combined to create more complex organisms with increasing defenses. The chloroplast that powers photosynthesis in plants and mitochondria that power human cells were both independent organisms at one point in evolution. And on and on life went.

This back-and-forth continued and branched out with incredible diversity, creating everything from the complex human immune system to the false eyes on the back of a Bengal tiger's ears to ward off predators. (What the hell was preying on a Bengal tiger?!?)

This arms race is what makes treating cancers so difficult. Tumor cells can defend themselves and adapt to attacks from the immune system or pharmaceutical interventions, which leads to metastasis (cancer spreading throughout the body) and resistance to treatment (tumor cells using different proteins for survival).

The PD-L1 receptor on the surface of tumors cells is one of the first lines of defense against the immune system. It sticks out like a flag, ready to link up with the PD-1 receptor on T cells (a type of immune cell). When the PD-L1 receptor on the surface of tumor cells binds to the PD-1 receptor on the surface of T cells, those T cells are blocked from doing their job – attacking cancer cells.

That's what makes PD-1 and PD-L1 inhibitors so important. These drug compounds are often antibodies engineered to replicate one of these complimentary receptors. Whether drug products are bound to tumor cells or T cells, blocking the interaction frees up T cells to do their job – attack tumor cells and rally the rest of the immune system to do the same.

It works really well. And because many solid tumors utilize PD-L1 as a central defense mechanism, these drugs often have activity across dozens of tumor types. That creates a huge market opportunity.

The Largest-Ever Drug Class by Revenue (By Far, So Far)

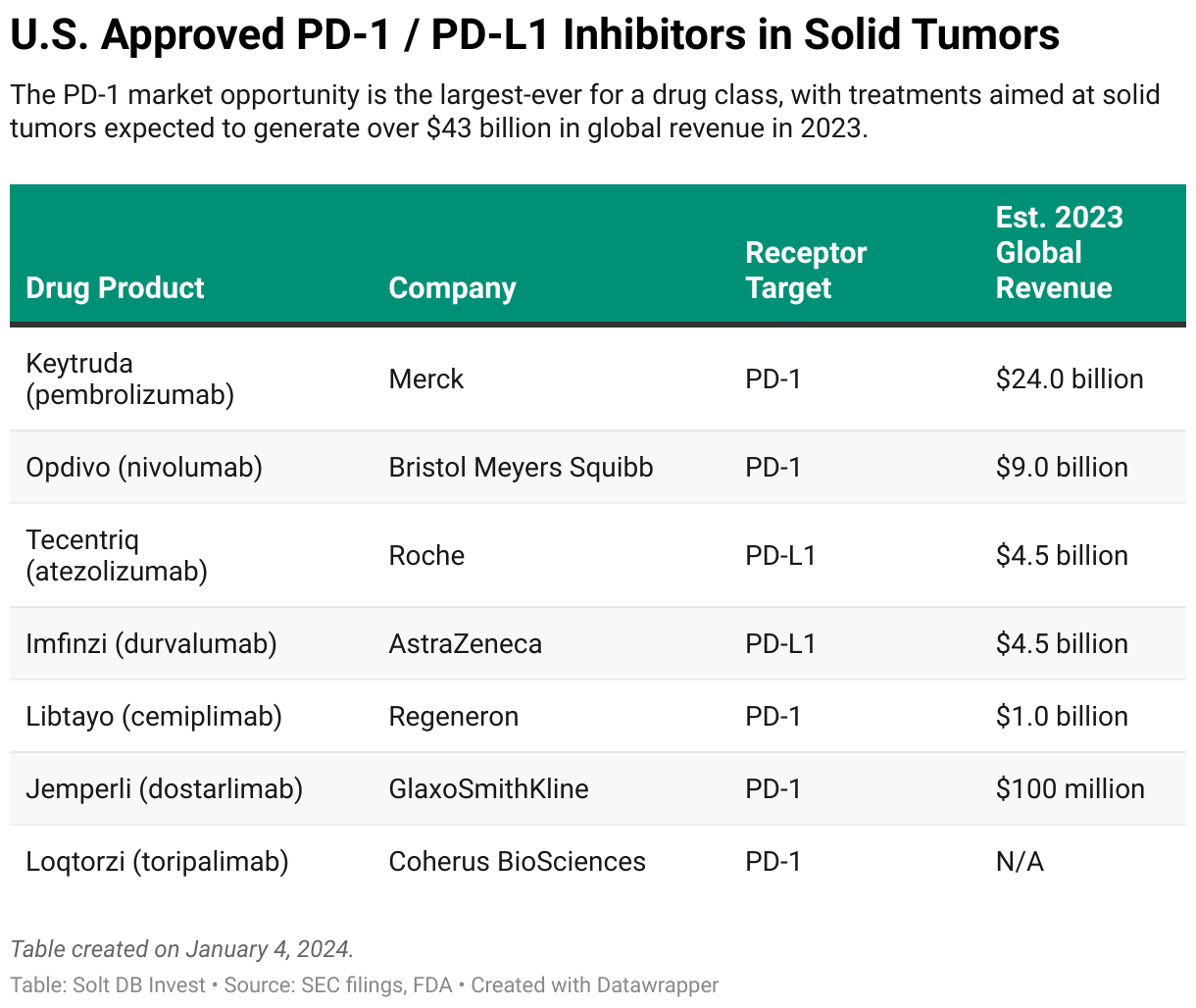

The ubiquity of PD-L1 has created an unusually large market opportunity. Keytruda from Merck likely had full-year 2023 revenue of at least $24 billion – making it the bestselling drug in the world.

However, the market opportunity is so unusually large that even the top competitors are among the world's bestselling drugs. Opdivo from Bristol Meyers Squibb likely had full-year 2023 revenue of nearly $9 billion. While Tecentriq from Roche and Imfinzi from AstraZeneca each notched about $4.5 billion in annual sales.

Those four drugs are the most direct comparisons to Loqtorzi, as all products are approved or being developed for multiple solid tumor cancers. Libtayo from Regeneron earned its first approval in squamous cell skin cancer, while Jemperli from GlaxoSmithKline secured its first U.S. approval in endometrial cancer. Jemperli is being studied in multiple tumor types as well.

Coherus BioSciences stands out among the crowded competitive landscape for two reasons. First, it's by far the smallest drug developer with a PD-1 / PD-L1 inhibitor. Loqtorzi won't dominate the drug class and is unlikely to dislodge Keytruda as the go-to for combination studies – but it doesn't have to. Ramping to $200 million (or $500 million, or...) in annual revenue would have a significant impact for the business, which is valued at $320 million as of this writing. That would be a rounding error for Merck or Bristol Meyers Squibb.

Second, Coherus BioSciences is the only company that in-licensed a Chinese PD-1 asset and earned U.S. Food and Drug Administration (FDA) approval. By choosing toripalimab and focusing on nasopharyngeal carcinoma (NPC) as the first cancer target, the asset was granted regulatory flexibility. That gives it a beachhead from which to expand.

The asset was granted regulatory flexibility because NPC is most common in Asian populations, so the Chinese clinical trial data were deemed representative of the patient population in the United States. Regulators felt uneasy about offering the same leeway in lung cancer, which was the beachhead other drug developers with in-licensed Chinese assets sought to build around. Would clinical data from Chinese patients really represent the patient population among a random selection of Americans? Individuals of Asian descent, especially men, have responded differently to immunotherapy than individuals of European descent in previous clinical trials.

Choosing lung cancer as an initial market backfired. The FDA's rejection of Chinese clinical trial data left other drugmakers in a bind. Novartis in-licensed tisleizumab from BeiGene, Eli Lilly in-licensed sintilimab from Innovent, and EQRx in-licensed sugemalimab from Cstone Pharmaceuticals. All decided to walk away rather than conduct large, lengthy clinical trials in the United States – despite spending hundreds of millions of dollars on upfront license payments.

That removed significant competition from the PD-1 inhibitor landscape, which benefited Coherus BioSciences more than any other company. It's now in an exclusive group of companies armed with a PD-1 inhibitor. That's good, because biology's arms race doesn't stop there.

Combination Treatments Drive the PD-1 Landscape

Although there's a clear divide between companies with and without a PD-1 inhibitor in immunotherapy, things aren't so simple.

Treatment might be effective at first, or even help patients become cancer free. But tumors treated with a PD-1 inhibitor can become resistant to treatment. Instead of relying on PD-L1 receptors to thwart T cells, they can leverage other defense mechanisms. That can make prolonged or future treatment (even years later) ineffective. Sometimes it can result in worse outcomes for patients.

Therefore, having a PD-1 inhibitor is important because it becomes the foundation for a successful immuno-oncology portfolio. Combination therapies that combine a PD-1 inhibitor with one or two other drugs can attack tumor cells in multiple ways, reducing their ability to mount a meaningful defense.

That leaves Merck, Bristol Meyers Squibb, Roche, AstraZeneca, GlaxoSmithKline, and tiny little Coherus BioSciences well positioned to develop internal pipelines using their own PD-1 and other assets. Importantly, it also forces every other drug developer to come to them when seeking a PD-1 inhibitor to pair with their development-stage oncology assets.

The Cancer Research Institute tracks the development landscape among PD-1 / PD-L1 inhibitors. At the end of 2021, there were 4,652 clinical trials evaluating combinations with the drug class. These studies had an estimated 300 molecular targets in addition to PD-1.

Notice the breadth of combinations – there's an opportunity to combine the drug class with everything from chemotherapy to radiopharmaceuticals, precision inhibitors to mRNA cancer vaccines.

This also helps to reinforce the value of the Surface Oncology acquisition. Coherus BioSciences snagged mid- and late-stage assets that it can immediately pair with Loqtorzi, while retaining more of the economic opportunity (it doesn't have to pay licenses or split revenue – aside from Junshi Biosciences of course).

Investors might not be terribly impressed with INOVIO Pharmaceuticals (I'm certainly not), but spreading Loqtorzi around the industry creates significant growth opportunities with no risk to Coherus BioSciences. That's the benefit of being one of the few companies with a PD-1 inhibitor.

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Quality) position. The current modeled fair valuation for the company based on our 2024 model is below:

- Market close January 4: $2.92 per share

- Modeled Fair Valuation: $13.15 per share

- Allocation Range: Up to 15%

Coherus BioSciences reported 111.364 million shares outstanding as of October 31, 2023. The modeled fair valuation above assumes 116.932 million shares outstanding, which is equivalent to 5% dilution.

Further Reading

- November 2023 research note evaluating FDA approval of Loqtorzi

- June 2023 research note evaluating the unique mechanism of Loqtorzi, specifically the ability to work in tumors with low PD-L1 expression

.svg)

.png)

.png)

-cropped.svg)