.svg)

It's come to this. The divestment of the Udenyca franchise marks the end of era – and the end of an error.

Coherus BioSciences was founded in 2010 to commercialize biosimilars, which were enabled as part of the Affordable Care Act. The company absorbed its fair share of lumps before launching its first product at the end of 2018. It was an immediate success.

Udenyca generated $356 million in full-year 2019 revenue, making it the best global drug launch of the year.

Fast forward half a decade – through many more lumps – and Coherus has decided to divest Udenyca for $365 million. It will receive an additional $118.4 million for inventory and is eligible to receive $75 million in sales milestones. The total deal consideration is roughly $483.4 million upfront or up to $558.4 million if sales milestones are achieved.

Coherus, founded to commercialize biosimilars, now owns no biosimilars.

The debt overhang proved to be a good cudgel. The decision to avoid dilution years ago by issuing convertible notes proved to be a big error in hindsight, which forced the company's hand. Management decided to clean up almost all debt on the balance sheet and go all-in on tomorrow. Now refashioned as an immuno-oncology drug developer, investors must decide if they're willing to stick around for the new thesis. Four data readouts by the end of 2025 will provide plenty of data to evaluate management's new strategy.

Udenyca Transaction Details

Coherus agreed to sell the Udenyca franchise to Intas Pharmaceuticals for up to $558.4 million, including:

- $365 million for intellectual property and trademarks

- $118.4 million for inventory, subject to adjustments upon transfer

- $37.5 million if Udenyca achieves cumulative revenue of $300 million from Q2 2025 through Q1 2026 (four full consecutive quarters), or Q3 2025 through Q2 2026 (four full consecutive quarters)

- $37.5 million if Udenyca achieves cumulative revenue of $350 million in any four consecutive quarters through the end of Q4 2026

My pre-divestment model expected full-year 2025 Udenyca revenue of $294.125 million, which was relatively conservative for Udenyca Onbody in the second half of the year. On the one hand, that suggests at least the first sales milestone is achievable. On the other hand, that model required the commercial expertise of Coherus. Intas Pharma's ability to deliver is an unknown variable.

If the transaction is terminated by Coherus (it still requires shareholder approval), then the company must pay Intas a termination fee of $16.8 million.

Plans to Reduce Debt Amounts

Upon closing of the transaction, Coherus plans to clean up the balance sheet and remove the royalty stream on Udenyca.

- As of September 2024, the business had an outstanding balance of $227.9 million for the 2026 Convertible Notes. There will be extra fees for repurchasing the debt early as part of the customary "make whole" covenants in debt note transactions.

- The business will also pay $49.1 million to buy out the future 5% royalty stream placed on Udenyca on July 1, 2024.

To be clear, Coherus is not paying off the term loan due May 2029. It's only buying out the royalty stream due to the financer as it relates to Udenyca sales.

Remember, the business secured a term loan of $38.7 million in May 2024 (to pay off the remaining portion of the old term loan) by placing a 5% royalty on Udenyca and Loqtorzi sales through June 2029. That turned out to be an expensive transaction in hindsight.

When the dust settles at the end of March 2025, Coherus should have roughly $248 million in cash less cash burn from Q1 2025. Management expects to have enough cash on hand to fund the business through the end of 2026.

Now What?

Coherus is forcing investors to fix their gaze on three things:

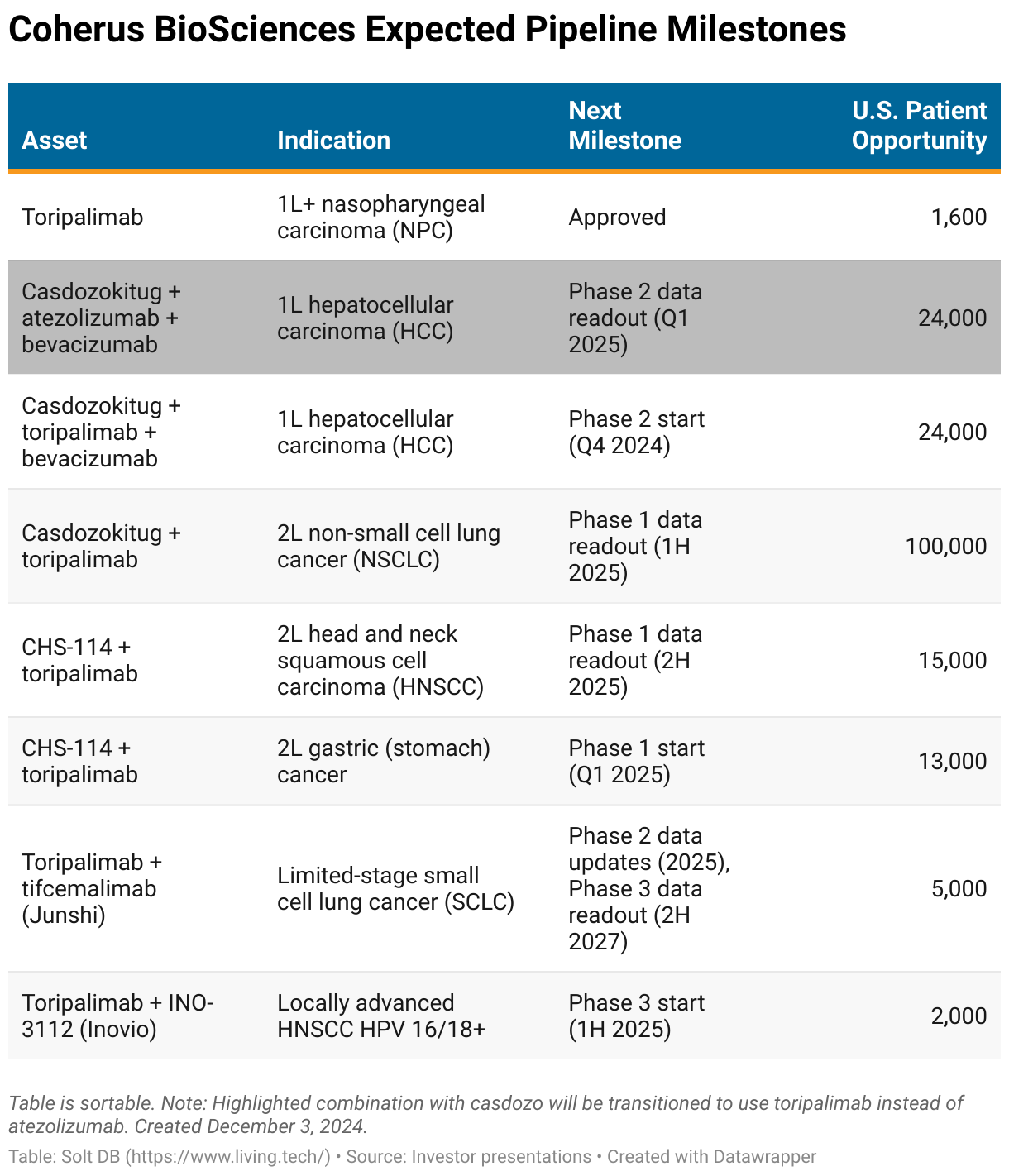

- Loqtorzi's continued ramp in nasopharyngeal carcinoma (NPC)

- External combinations with Loqtorzi (toripalimab – the brand name isn't used in external clinical studies)

- The early-stage pipeline

Loqtorzi in NPC

First, Loqtorzi's continued commercial ramp in NPC. The opportunity is relatively small, but that also means there's no direct competition and nothing in the industry pipeline. The asset has a smooth ramp trajectory to peak sales in 2027.

- My 2025 model expects revenue of $69 million, which contributes $251.160 million ($2.07 per share) to the valuation.

- The peak sales opportunity in NPC is valued at roughly $150 million in 2027, which would contribute roughly $546 million ($4.51 per share) to the valuation. Wall Street can and usually does factor in peak sales opportunities in high-certainty scenarios like this, but I'm not updating this component of my model just because Udenyca was divested. Those two things are unrelated.

External Combinations with Toripalimab

Second, external combinations with Loqtorzi (toripalimab). The primary value of wielding a PD-1 inhibitor is the ability to combine it with, well, almost anything else.

It's a low-risk way to increase the asset's revenue opportunity. Coherus doesn't have to spend a penny, third parties assume all the risk of conducting clinical trials, and if any combinations earn approval, it increases the revenue potential of Loqtorzi.

There are three external combinations ongoing right now. None are currently factored into my 2025 model. The two most important:

- Junshi Bioscience is conducting a U.S. study of tifcemalimab and toripalimab in limited stage small cell lung cancer. Phase 2 data presented at ASCO 2024 demonstrated an objective response rate (ORR) of 100% in patients with PD-1 expression (37/37) and an overall ORR of 84.5% (32/37). The current standard of care in SCLC achieves an ORR of 60% to 65%. Tifcemalimab has a high probability of success in this indication, but approval is unlikely until mid-2028 at the earliest.

- Inovio Pharmaceuticals is conducting a study of INO-3112 and toripalimab in viral-driven head and neck squamous cell carcinoma (HNSCC). I don't think highly of Inovio, but toripalimab is uniquely positioned for head and neck cancers. After all, NPC falls into that category.

The opportunity in limited-stage SCLC is important for future value creation. That can triple the peak sales opportunity for Loqtorzi to roughly $600 million and contribute $2.184 billion ($18.04 per share non-diluted) to the valuation. Of course, shareholders must wait until 2028 or 2029 for an approval decision and market launch.

Early-Stage Pipeline

My 2025 model continues to value the entire pipeline at $52 million. I'm awaiting data readouts to update the model – the divestment of Udenyca is unrelated.

Investors can expect a rich slate of activity in the next 12 months. That includes an expected update by the end of this month.

To be honest, I might be a little too harsh on casdozo. The asset has demonstrated activity as a monotherapy (when used alone to tease out the effect). I still lean toward being conservative.

Casdozo is the only IL-27 inhibitor in clinical trials globally. That makes it difficult to slot into my frameworks, which use competitive landscape dynamics and data to narrow the model. Interleukins have a mixed history in oncology. Additionally, Coherus is focusing on large, competitive markets like hepatocellular carcinoma (HCC) (a type of liver cancer) and non-small cell lung cancer (NSCLC). Positive results will amplify the opportunity, but it's also more difficult to compete.

I'm most interested in the CCR8 inhibitor. CHS-114 is the third-most advanced asset in the class globally behind Bristol Myers Squibb and LaNova Medicines – it also has a very similar structure to the two rivals. Recent data show CHS-114 might be more selective.

I won't rehash the research note dedicated to the CCR8 opportunity, but an important phase 1 data readout by the end of 2025 paired with developments in the competitive landscape could bode well for Coherus.

I don't value CHS-1000 in the current 2025 model. Coherus may choose to terminate the asset in favor of more robust investment in casdozo or CHS-114.

Forecast & Modeling Insights

(Reduced to reflect Udenyca divestment.)

The new 2025 model removes Udenyca's contribution to operating leverage and reduces the expectation for dilution, which previously reflected full dilution from the 2026 Convertible Notes.

For transparency:

- Full-year 2025 net product revenue of $69 million from Loqtorzi. That includes Q4 2025 revenue of $22.5 million representing an annualized exit rate of $90 million.

- I expect full-year 2026 net product revenue of roughly $120 million from Loqtorzi.

- I was tearing it up modeling Coherus' operating expenses, now I have to tear up that model. The business is now expected to cough up significant cash burn in 2025.

Investors will await the January 2025 update from management for more details about the near- and long-term trajectory.

Margin of Safety & Allocation

Coherus BioSciences is considered a Growth (Speculative) position. The current modeled fair valuation for the company based on my 2025 model is below:

- Market close December 3: $1.71

- Modeled Fair Valuation: $2.51

- Allocation Range: Up to 10%

Coherus BioSciences reported 115.213 million shares outstanding as of October 31, 2024. The modeled fair valuation above assumes 120.974 million shares outstanding, which is equivalent to 5% dilution by the end of 2025.

Further Reading

- December 2024 press release announcing the Udenyca divestment

- December 2024 regulatory filing (8-K) announcing the Udenyca divestment

- December 2024 regulatory filing exhibit detailing the transaction details

- November 2024 research note evaluating Q3 2024 operating results and introducing the old 2025 model

- October 2024 research note introducing the opportunity for CCR8 inhibitors including CHS-114

.svg)

.png)

.png)

-cropped.svg)